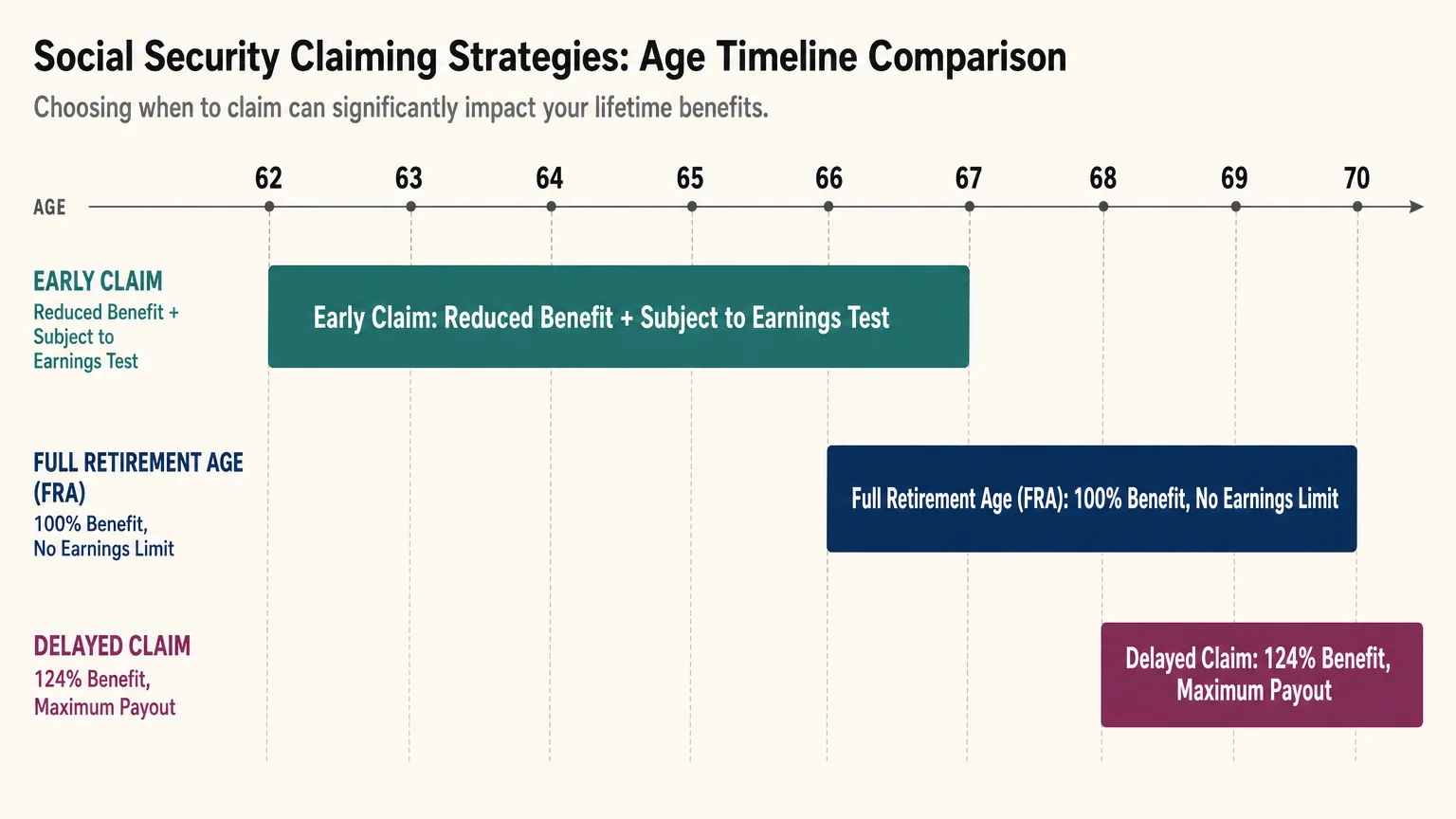

Comparing Claiming Strategies: Working While Receiving Benefits

To navigate these interconnected rules, you must align your claiming strategy with your lifestyle goals and employment status. The decision to claim early while working triggers immediate consequences but also alters your long-term financial trajectory. The table below outlines how different approaches impact your immediate cash flow, lifetime payout, and tax obligations.

| Strategy | Immediate Income Impact | Long-Term Benefit Impact | Tax Implications |

|---|---|---|---|

| Claim Early + Work Full-Time | High risk of checks being completely withheld due to the earnings limit. | Permanent reduction in base monthly benefit for claiming before FRA. | High probability that up to 85% of retained benefits are taxed. |

| Claim Early + Work Part-Time | Benefits paid in full as long as earnings stay under the annual threshold. | Permanent reduction in base monthly benefit for claiming before FRA. | Moderate risk of taxation depending on spouse’s income and investments. |

| Delay to FRA + Work Full-Time | Zero benefits withheld. You keep 100% of your earnings and your benefits. | You receive your full 100% standard benefit amount for life. | Benefits likely taxed due to high combined income from working. |

| Delay to Age 70 + Keep Working | Maximum wage income now, zero Social Security income until age 70. | Maximum possible monthly benefit (up to 124% of your base amount). | Lower tax burden later in life if you stop working at age 70. |

Leave a Reply