Protecting your hard-earned benefits requires recognizing the sophisticated tactics fraudsters use to steal your personal information. Social Security scams rob Americans of millions of dollars each year by exploiting fear and confusion surrounding retirement benefits. Criminals increasingly use caller ID spoofing and official-looking emails to convince you that your Social Security number has been suspended or that you owe immediate fines. Once you understand their precise methods, you can quickly shut down these attacks before any damage occurs. By learning to identify the exact warning signs of phone and email fraud, you guarantee your financial security and maintain total control over your identity throughout your retirement years.

The Anatomy of a Social Security Phone Scam

Phone scams remain the most prevalent method criminals use to target older adults. The attack typically begins with an unsolicited phone call, often from a number that appears completely legitimate. Scammers manipulate telecommunications systems to display “Social Security Administration” or a local Washington D.C. area code on your caller ID; a technique known as spoofing. They rely heavily on your assumption that caller ID technology is secure and accurate.

When you answer the phone, the interaction usually follows one of several highly polished scripts designed to trigger immediate panic. The most common script involves a severe robotic voice or a stern live operator informing you that your Social Security number has been connected to criminal activity—usually money laundering or drug trafficking—in a distant state. The caller will claim that a warrant has been issued for your arrest and that your benefits will be terminated by the end of the business day unless you resolve the issue immediately.

Another frequent tactic centers on cost-of-living adjustments (COLA) or imaginary overpayments. The caller will cheerfully announce that you qualify for a substantial increase in your monthly benefit, but you must first pay a small processing fee or verify your banking details to facilitate the transfer. Alternatively, they might claim the agency overpaid you last year and demand instant repayment to avoid a disruption in your upcoming checks. In every scenario, the criminal steers the conversation toward an urgent demand for money or sensitive data.

The hallmark of a phone scam is the requested method of payment. Federal agencies operate through the United States Treasury and process payments via standard banking channels. Scammers, however, demand untraceable funds. They will instruct you to purchase retail gift cards—such as those from Target, Apple, or Google Play—and read the numbers over the phone. Some will direct you to a local cryptocurrency ATM to deposit cash, or demand you send funds via wire transfer services like Western Union. The moment a caller demands payment via retail gift cards or cryptocurrency, you are speaking to a criminal.

Decoding Fraudulent Social Security Emails and Texts

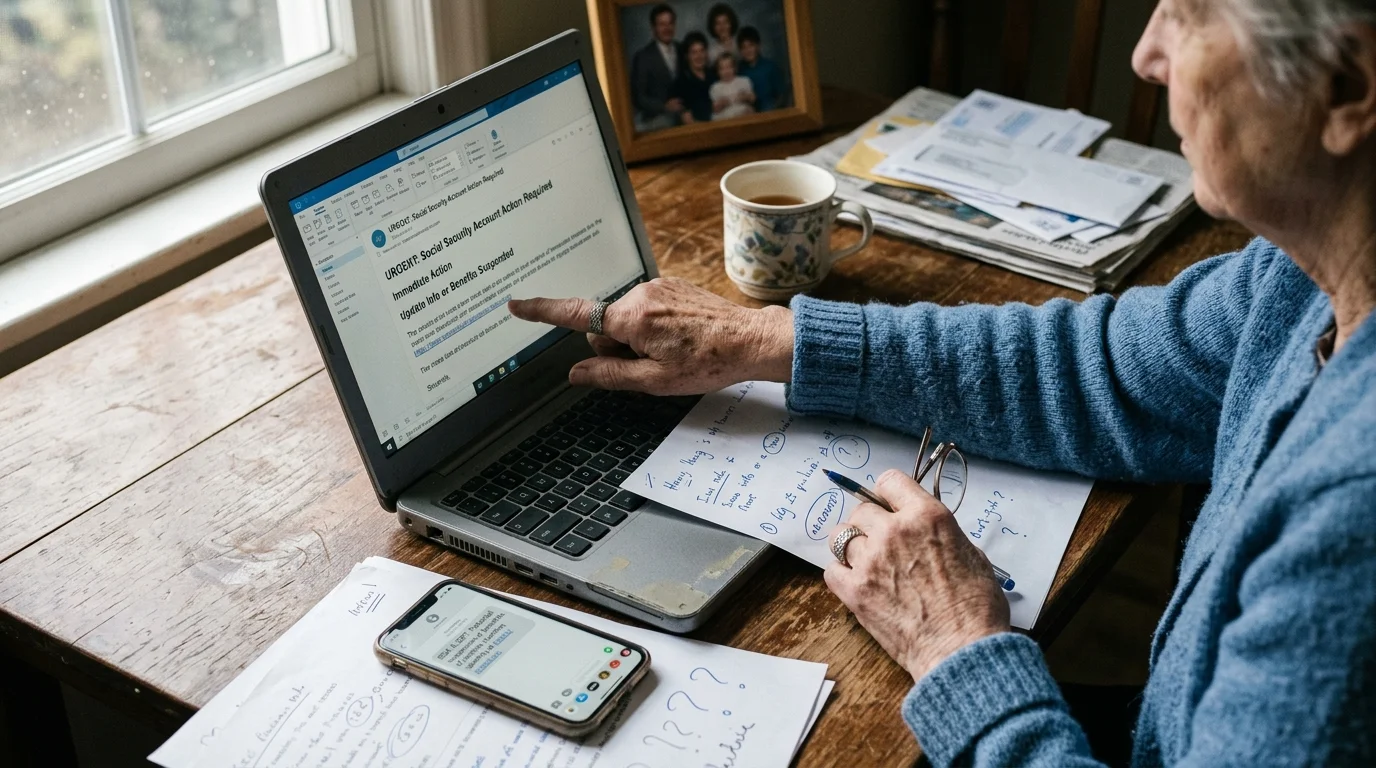

While phone calls rely on verbal intimidation, email and text message scams—known as phishing and smishing—use visual deception to trick you into compromising your own security. These digital attacks often arrive in your inbox bearing the official logo of the Social Security Administration, utilizing formatting and language stolen directly from legitimate government correspondence.

A fraudulent email typically features a deeply concerning subject line, such as “Urgent: Your Benefits Will Be Suspended,” “Action Required: Verify Your Identity,” or “Notice of Unpaid Federal Fines.” The body of the email will brief you on an urgent problem and provide a highly visible link or button directing you to a “secure portal” to resolve the issue. If you click the link, it takes you to a counterfeit website that looks identical to the official login page for a my Social Security account.

Once you arrive at this fake portal, the site will prompt you to enter your Social Security number, date of birth, mother’s maiden name, and banking details. The moment you hit submit, your personal information is instantly transmitted to the scammers, who will use it to access your actual retirement accounts, open unauthorized credit lines, or redirect your monthly benefit deposits into their own bank accounts.

Text message scams operate on the same principle but are condensed for mobile devices. You might receive a text stating, “SSA Alert: Your profile requires immediate verification due to suspicious activity. Click here to secure your account.” Because text messages feel more personal and immediate than emails, people frequently click these malicious links without applying their usual scrutiny.

To detect a fraudulent email, closely examine the sender’s actual email address, not just the display name. A legitimate email from the agency will always originate from an address ending in “.gov”. Scammers often use addresses that look vaguely official but end in “.com”, “.org”, or use convoluted domain names like “support@ssa-benefits-update.com”. Furthermore, legitimate government emails rarely include attachments you did not request. If an email contains a PDF labeled “Benefit Verification” or “Suspension Notice,” do not open it; it likely contains malware designed to scan your computer for financial passwords.

Psychological Manipulation: How Scammers Force Compliance

Understanding the technical execution of a scam is only half the battle; recognizing the psychological warfare they employ is equally vital. Fraudsters do not simply ask for your information; they engineer an emotional state where critical thinking becomes exceptionally difficult.

First, they establish authority. The caller will confidently provide a fake badge number, recite federal statutes, and use bureaucratic jargon to convince you of their legitimacy. They lean on the inherent respect most citizens have for federal institutions and law enforcement. By positioning themselves as powerful government agents, they create an uneven dynamic where questioning their demands feels like a violation of the law.

Second, they manufacture extreme urgency. A scammer will never give you time to think, consult a family member, or call the agency back to verify their claims. They insist that the problem must be resolved during this exact phone call. They might explicitly command you not to mute the phone, hang up, or speak to anyone else, claiming that doing so will result in an immediate dispatch of local police to your home. This artificial time constraint forces you into a reactive state, bypassing the logical centers of your brain that would normally spot the glaring inconsistencies in their story.

Finally, they weaponize your financial security. For millions of retirees, Social Security represents a primary source of income. The mere suggestion that this financial lifeline could be severed creates a profound sense of panic. Scammers exploit this vulnerability mercilessly, knowing that the fear of losing your retirement income will drive you to comply with completely irrational demands, such as buying thousands of dollars in prepaid gift cards.

“It takes 20 years to build a reputation and five minutes to ruin it. If you think about that, you’ll do things differently.” — Warren Buffett, Investing and Retirement Wisdom

Comparison: Legitimate SSA Communication vs. Scammer Tactics

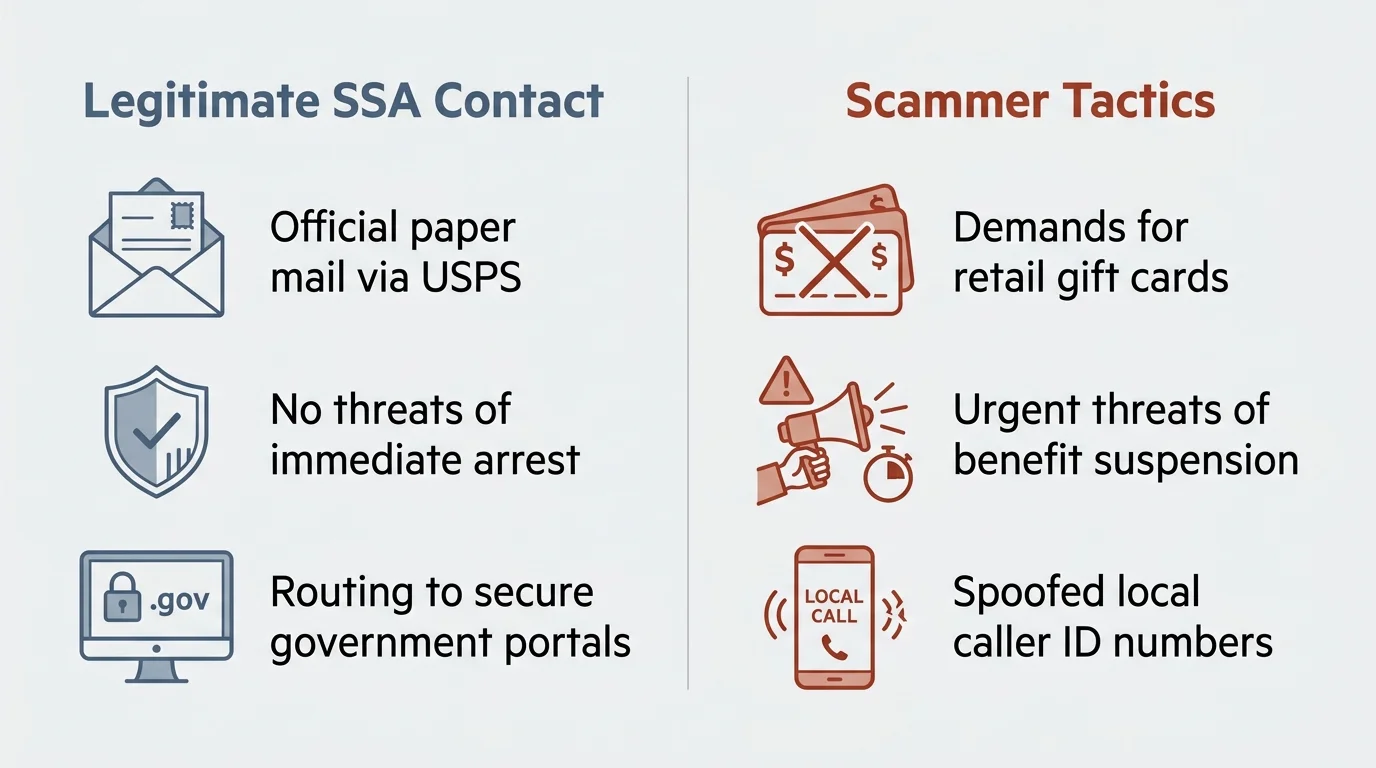

To protect yourself effectively, you must understand the stark differences between how the actual Social Security Administration operates and how criminals impersonate them. The table below outlines the key distinctions you can use to immediately evaluate any communication.

| Communication Feature | Legitimate Social Security Administration | Scammer Tactics |

|---|---|---|

| Initial Contact Method | Almost always by physical mail via the U.S. Postal Service. Phone calls only occur if you requested a call or have ongoing business. | Unexpected, unprompted robocalls, live phone calls, text messages, or urgent emails. |

| Tone and Demeanor | Professional, calm, and informative. Representatives are trained to assist, not to interrogate. | Aggressive, hostile, and pressuring. Uses threats of arrest, legal action, or physical detainment. |

| Payment Demands | Never demands immediate payment. Offers formal appeal processes. Accepts standard treasury payments by check or direct electronic transfer. | Demands immediate compliance. Requires retail gift cards, prepaid debit cards, wire transfers, or cryptocurrency deposits. |

| Verification Requests | May ask you to verify your identity, but usually only when you initiate the phone call. | Demands your full Social Security number, banking details, or passwords to “prove” your identity. |

| Account Suspension | Social Security numbers are never “suspended” or “frozen.” | Frequently claims your Social Security number has been suspended due to criminal activity. |

| Time Constraints | Provides deadlines in written notices, typically giving you 30 to 60 days to respond or appeal. | Forces you to act immediately while on the phone, refusing to let you hang up. |

Why Retirees Are the Primary Targets for Identity Theft

Criminal organizations run their operations like businesses, focusing their resources on targets that offer the highest return on investment. Retirees are disproportionately targeted for several systemic and demographic reasons.

Financially, older adults have typically accumulated more wealth than younger demographics. You likely own your home, possess substantial savings, manage investment portfolios, and have excellent credit scores built over decades of responsible financial behavior. A stolen identity belonging to a retiree allows a criminal to secure large loans, drain extensive retirement accounts, and file fraudulent tax returns that yield massive refunds.

Additionally, retirees interact with government agencies far more frequently than younger populations. Between navigating Medicare enrollment, managing Social Security benefits, and handling required minimum distributions from retirement accounts, communication with federal entities feels routine. Scammers exploit this familiarity. An email claiming to be about a benefit update seems highly plausible when you are actively managing your retirement income.

There is also a generational divide in technology adoption. While many retirees are highly tech-savvy, criminals cast a wide net, hoping to catch individuals who might be less familiar with the nuances of digital phishing, caller ID spoofing, or the mechanics of peer-to-peer payment apps. They use confusing technological jargon to disorient their victims, making the scam feel legitimate through sheer complexity.

Proactive Measures: Securing Your Identity Online

The most effective defense against Social Security fraud is establishing a secure digital perimeter before scammers can target you. Taking control of your online presence removes the opportunities criminals rely upon.

Your first critical step is establishing your official my Social Security account directly through Social Security Administration. Even if you are not yet retired or do not plan to claim benefits for several years, creating this account is a powerful defensive maneuver. Once you claim your online profile, a scammer cannot create one in your name. Criminals frequently use stolen personal information to set up accounts for victims who haven’t done so yet, allowing the fraudster to redirect benefit payments to their own debit cards.

Next, implement a routine of monitoring your credit reports. You are entitled to free weekly credit reports from the three major bureaus (Equifax, Experian, and TransUnion) through AnnualCreditReport.com. Reviewing these documents allows you to catch unauthorized credit checks or newly opened accounts before the financial damage cascades. If you discover an account you did not open, you can immediately contest it with the creditor.

Consider placing a permanent credit freeze on your files. A credit freeze locks your credit report, making it entirely inaccessible to lenders unless you temporarily lift the freeze using a secure PIN. Because most lenders will not issue new credit without checking your report, a freeze stops identity thieves in their tracks, even if they have successfully stolen your Social Security number and date of birth. Freezing and unfreezing your credit is completely free under federal law and is widely considered the single most effective tool against financial identity theft.

“When you protect your money, you protect your life.” — Suze Orman, Retirement Planning

Pitfalls to Watch For

Even cautious individuals can stumble into carefully laid traps. Scammers constantly evolve their methods, turning common courtesy and modern convenience against you. Be extremely vigilant regarding these specific pitfalls:

- Trusting Caller ID Implicitly: The technology that displays incoming numbers is fundamentally flawed and easily manipulated. Never assume an incoming call is genuinely from the government simply because the screen reads “SSA” or displays a Washington D.C. area code.

- Engaging with Robocalls: If you answer a call and hear a recorded message instructing you to “press 1 to speak to a representative” or “press 2 to be removed from our list,” hang up immediately. Pressing any button signals to the automated system that your phone number is active and monitored, which will result in your number being sold to other scam networks, drastically increasing the volume of fraud calls you receive.

- Clicking “Unsubscribe” in Suspicious Emails: Much like pressing a button on a robocall, clicking an “unsubscribe” link at the bottom of a phishing email verifies your email address as an active target. If you suspect an email is fraudulent, do not interact with any links; simply mark it as spam or block the sender.

- Attempting to Outsmart the Scammer: Some individuals realize they are speaking to a scammer and attempt to keep them on the line to waste their time or gather information. This is a dangerous game. Scammers record these calls and can capture snippets of your voice—specifically you saying the word “Yes”—to authorize fraudulent charges or bypass voice-recognition security systems used by some banks.

- Confirming Partial Information: A caller might say, “I just need to verify the last four digits of your Social Security number.” If they already possess the first five digits from a previous data breach, you have just provided the missing piece they need to steal your identity. Never confirm partial information with an unverified caller.

Immediate Steps to Take if You Suspect Retirement Fraud

If you realize you have engaged with a scammer, time is of the essence. Emotions will run high, but taking swift, methodical action can contain the situation and prevent financial loss.

If you are still on the phone with the suspected fraudster, hang up instantly. Do not offer an excuse, do not argue, and do not threaten them. Simply sever the connection. If you clicked a malicious link in an email or text message, disconnect your device from the internet immediately to interrupt any malware downloads.

If you provided banking details, credit card numbers, or purchased gift cards, contact your financial institution the moment you hang up the phone. Inform their fraud department exactly what happened. They can freeze your checking accounts, cancel compromised credit cards, and attempt to stop pending wire transfers. If you gave the scammer the numbers off a gift card, contact the retailer (e.g., Apple, Target) directly. While recovering gift card funds is notoriously difficult, acting within minutes occasionally allows the retailer to freeze the card balance before the scammer drains it.

If you disclosed your Social Security number, you must immediately place a fraud alert on your credit profile. You only need to contact one of the three major credit bureaus; federal law requires the bureau you contact to notify the other two. A fraud alert forces lenders to take extra steps to verify your identity before opening any new accounts or extending credit.

Finally, document everything. Write down the phone number the scammer called from, the exact time of the call, the names or badge numbers they used, and the specific demands they made. Save any fraudulent emails or text messages, taking screenshots if necessary. This documentation will be crucial when filing reports with federal authorities and disputing fraudulent charges.

Getting Expert Help

Navigating the aftermath of an attempted or successful scam is not something you have to do alone. Several federal agencies and advocacy groups are dedicated to tracking these crimes, prosecuting the offenders, and assisting victims with recovery.

Reporting Imposter Scams to the SSA: If you receive a fraudulent call, text, or email impersonating the agency, you should report it directly to the Social Security Administration’s Office of the Inspector General (OIG). They use these reports to track scam trends and build cases against criminal networks. You can file a detailed report online through their dedicated fraud portal.

Managing Financial Recovery: If your banking information was compromised or a scammer successfully opened accounts in your name, the Consumer Financial Protection Bureau provides extensive, step-by-step guidance on recovering from financial identity theft. They offer templates for disputing fraudulent charges and instructions for dealing with uncooperative financial institutions.

Finding Community and Legal Support: Advocacy organizations like the National Council on Aging offer robust resources for older adults facing financial exploitation. They can connect you with local elder justice programs, legal aid services, and community support groups designed to assist victims of sophisticated fraud.

Reporting General Fraud: For broader identity theft issues beyond just Social Security, the Federal Trade Commission’s IdentityTheft.gov website creates a personalized recovery plan based on the specific information you lost. It pre-fills forms and letters you can use to notify creditors, debt collectors, and law enforcement agencies.

Frequently Asked Questions

Will the Social Security Administration ever call me directly?

The agency will generally only call you if you have recently requested a call back, if you have ongoing business with them (such as an active application for benefits), or if a representative needs clarification on paperwork you recently submitted. They will never call you out of the blue to threaten you, demand immediate payment, or inform you of a sudden account suspension.

Can my Social Security number actually be suspended or canceled?

No. Your Social Security number is permanently assigned to you for life. The government does not suspend, freeze, or cancel numbers due to criminal activity, unpaid taxes, or any other reason. Any claim that your number will be suspended is a definitive sign of a scam.

What should I do if a scammer knows my address and family members’ names?

Scammers frequently use publicly available information from data brokers, property tax records, and social media to make their threats sound credible. Knowing your address or the names of your children does not mean they have compromised your official accounts. Do not let this tactic panic you. Hang up and do not confirm any of the details they recite.

Do these same scams target Medicare benefits?

Yes. Criminals frequently adapt these exact scripts for Medicare. They will call claiming your Medicare card has expired, that you must pay a fee for a new plastic card with a microchip, or that your health coverage will be canceled if you do not immediately verify your Medicare number. The same rules apply: hang up and verify any issues directly via Medicare.gov or by calling the number on the back of your official card.

Securing your retirement involves more than managing your investments and filing paperwork; it requires diligent defense against those actively trying to steal what you have built. By understanding how criminals operate, refusing to engage with unsolicited contacts, and establishing protective measures like credit freezes, you construct an impenetrable barrier around your identity. Stay informed, remain skeptical of urgent demands, and always maintain direct control over your personal information.

This is educational content based on general retirement and financial principles. Individual results vary based on your situation. Always verify current benefit rules, tax laws, and eligibility requirements with official sources like SSA, Medicare.gov, or the IRS.

Last updated: March 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply