The new federal initiative offering a $1,000 retirement match has generated massive headlines, but it is not the silver bullet many Baby Boomers are hoping for. If you are nearing retirement with a savings shortfall, you need to understand how this program works and why it cannot solve a six-figure retirement gap alone. Promoted through the TrumpIRA platform, this benefit evolves the federal Saver’s Match to help workers without employer-sponsored plans build wealth. Claiming your $1,000 match is a smart move, but relying on it entirely will leave you underfunded. You must combine this government incentive with aggressive catch-up strategies and strategic Social Security timing to truly secure your financial future.

The Mechanics of the $1,000 Federal Retirement Match

Lawmakers created the Federal Saver’s Match as part of the bipartisan SECURE 2.0 Act to replace the older, non-refundable Saver’s Credit. Historically, millions of Americans never claimed the old credit because it was complicated to calculate on tax returns and offered no immediate cash benefit. By converting the tax credit into a direct federal match, the government removed the friction of saving. To accelerate public access, the April 2026 executive order launched the TrumpIRA platform. This federal hub connects part-time workers, independent contractors, and employees at small businesses with high-quality, low-cost individual retirement accounts.

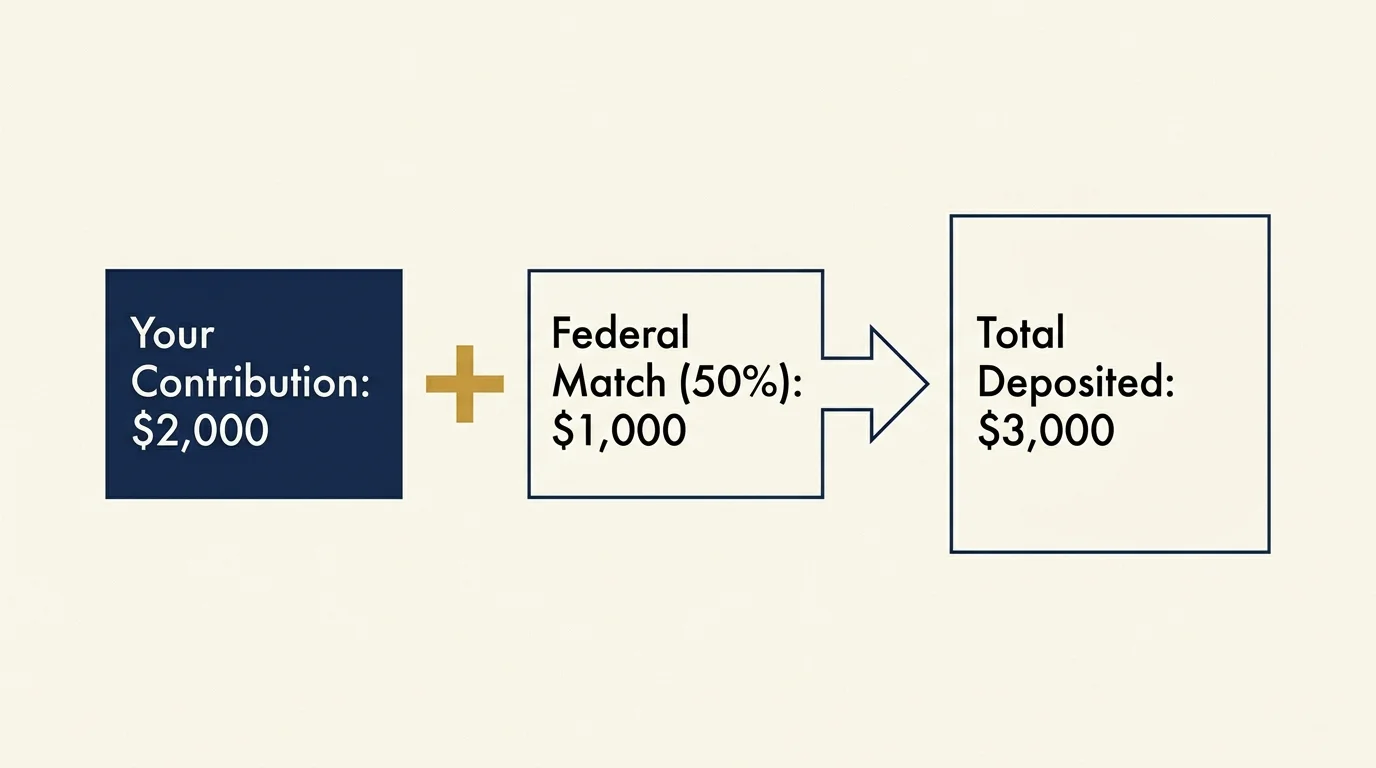

The financial mechanics are highly favorable if you qualify. When you deposit $2,000 of your own money into an eligible IRA, the Treasury adds a 50% match, placing $1,000 directly into your account. These funds bypass your checking account entirely; they lock into your retirement portfolio where they can grow tax-deferred until you reach age 59 and a half. However, the government heavily restricts this benefit based on income. The match phases out entirely as your modified adjusted gross income increases. You must review the exact phase-out brackets on the Internal Revenue Service (IRS) website to ensure your household qualifies before building this match into your financial plan.

Why a $1,000 Match Cannot Erase the Boomer Retirement Gap

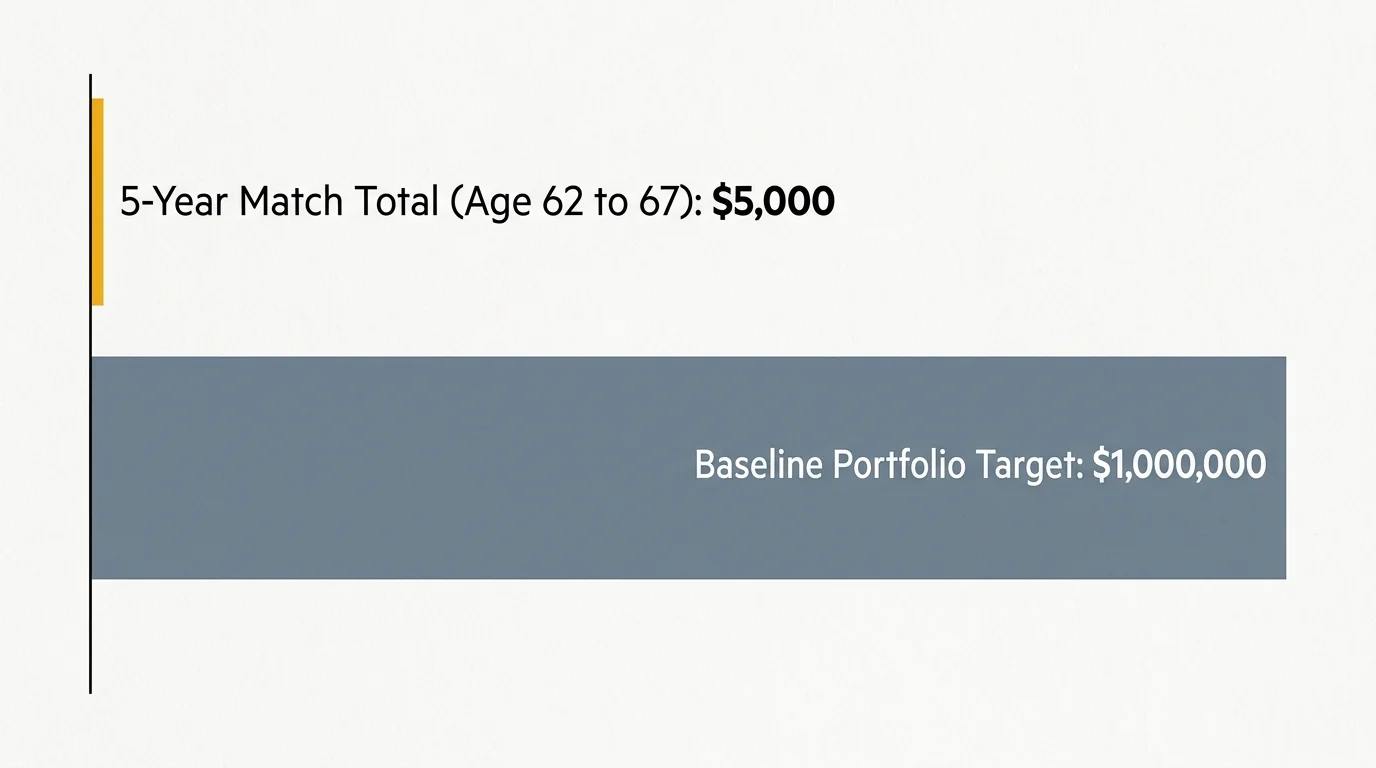

Claiming free money from the government is always a wise decision, but viewing this program as a comprehensive retirement solution is a dangerous miscalculation. The median retirement savings balance for adults in their sixties hovers far below what is required to sustain a modern, multi-decade retirement. When financial planners model inflation, property taxes, and living expenses, they frequently set baseline portfolio targets near the $1 million mark. A six-figure shortfall requires aggressive, compounding intervention.

Time is the most critical asset in investing, and Boomers are rapidly running out of it. If you are 62 years old and secure the $1,000 federal match every year until you retire at 67, you will have added just $5,000 in principal to your portfolio. Even assuming stellar market returns, that balance will not generate enough passive income to cover a single month of skilled nursing care. Younger generations can leverage decades of compounding interest to turn small deposits into vast wealth, but late-stage savers must focus on capital preservation and massive principal accumulation.

Healthcare expenses aggressively consume retirement budgets, further widening the gap. Medicare provides a fantastic baseline, but it leaves significant coverage holes. Retirees shoulder the burden of Part B premiums, Medigap or Advantage plan costs, Part D prescription deductibles, and out-of-pocket maximums. Fidelity Investments estimates a healthy couple retiring today will spend hundreds of thousands of dollars on medical care alone during their golden years. A minor federal match barely scratches the surface of these impending liabilities.

Real Strategies to Close Your Retirement Shortfall

To build a resilient retirement, you must take total ownership of your financial trajectory. Waiting for external bailouts or small legislative matches will leave you vulnerable to inflation and market shocks.

“Retirement is not an age; it is a financial number.” — Dave Ramsey, Personal Finance Expert

Instead of relying on the baseline, implement these high-impact strategies to rapidly accelerate your wealth before you exit the workforce:

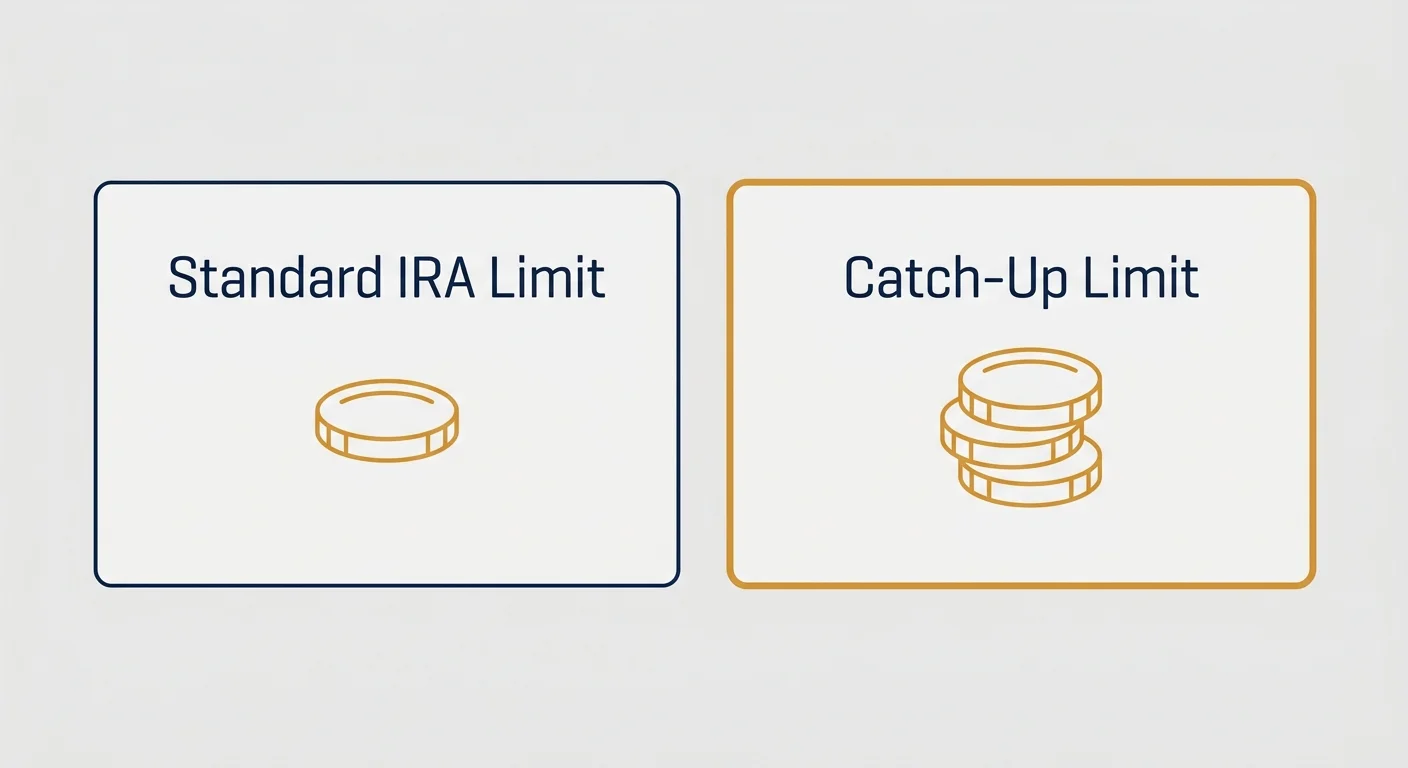

- Maximize Annual Catch-Up Contributions: The IRS recognizes that older adults need to accelerate their savings. Once you turn 50, you unlock the ability to make substantial catch-up contributions. You can add thousands of extra dollars to your 401(k) and traditional IRAs every year. If you fall into the 60 to 63 age bracket, recent tax law changes allow for even higher super catch-up limits within workplace plans.

- Leverage Health Savings Accounts (HSAs): If you utilize a High Deductible Health Plan, an HSA serves as a stealth retirement account. Contributions go in tax-free, grow tax-free, and withdraw tax-free when used for qualified medical expenses. Because healthcare represents your largest unpredictable expense, aggressively funding an HSA protects your standard retirement portfolio from medical shocks.

- Adopt a Phased Retirement: Instead of halting work abruptly, transition into a part-time consulting or freelance role. Earning just $20,000 a year from part-time work provides the exact same cash flow as withdrawing 4% from a $500,000 portfolio. This preserves your principal and allows your investments to continue compounding during the critical early years of retirement.

- Execute Aggressive Debt Elimination: Entering retirement with a mortgage, massive auto loans, or carrying credit card balances destroys your monthly cash flow. Every dollar you spend servicing debt is a dollar you cannot spend on your lifestyle. Target high-interest consumer debt immediately, then systematically pay down your mortgage before your final day of work.

- Evaluate Geographic Arbitrage: Your physical location dictates your financial reality. Relocating from a high-tax coastal city to a state with no income tax and lower property valuations can instantly add years of longevity to your portfolio. Downsizing your primary residence simultaneously frees up trapped home equity, allowing you to invest that capital into income-producing assets.

Comparing Your Savings and Catch-Up Options

Understanding how different savings vehicles stack up allows you to deploy your capital efficiently. Review the table below to see how the federal match compares to the aggressive contribution limits available to older adults. Using these options synergistically provides the fastest route to closing your retirement gap.

| Strategy | Maximum Annual Boost (2026 Limits) | Best Fit For |

|---|---|---|

| Federal Saver’s Match | Up to $1,000 federal deposit | Lower- to middle-income earners without a workplace plan. |

| IRA Catch-Up | $1,000 extra individual contribution | Individuals aged 50+ maxing out standard IRA limits. |

| 401(k) Catch-Up | $7,500 extra individual contribution | Workers aged 50+ with employer-sponsored plans. |

| Super Catch-Up (Ages 60-63) | $11,250 extra individual contribution | Workers aged 60-63 leveraging SECURE 2.0 workplace provisions. |

Social Security: The Most Powerful Lever You Control

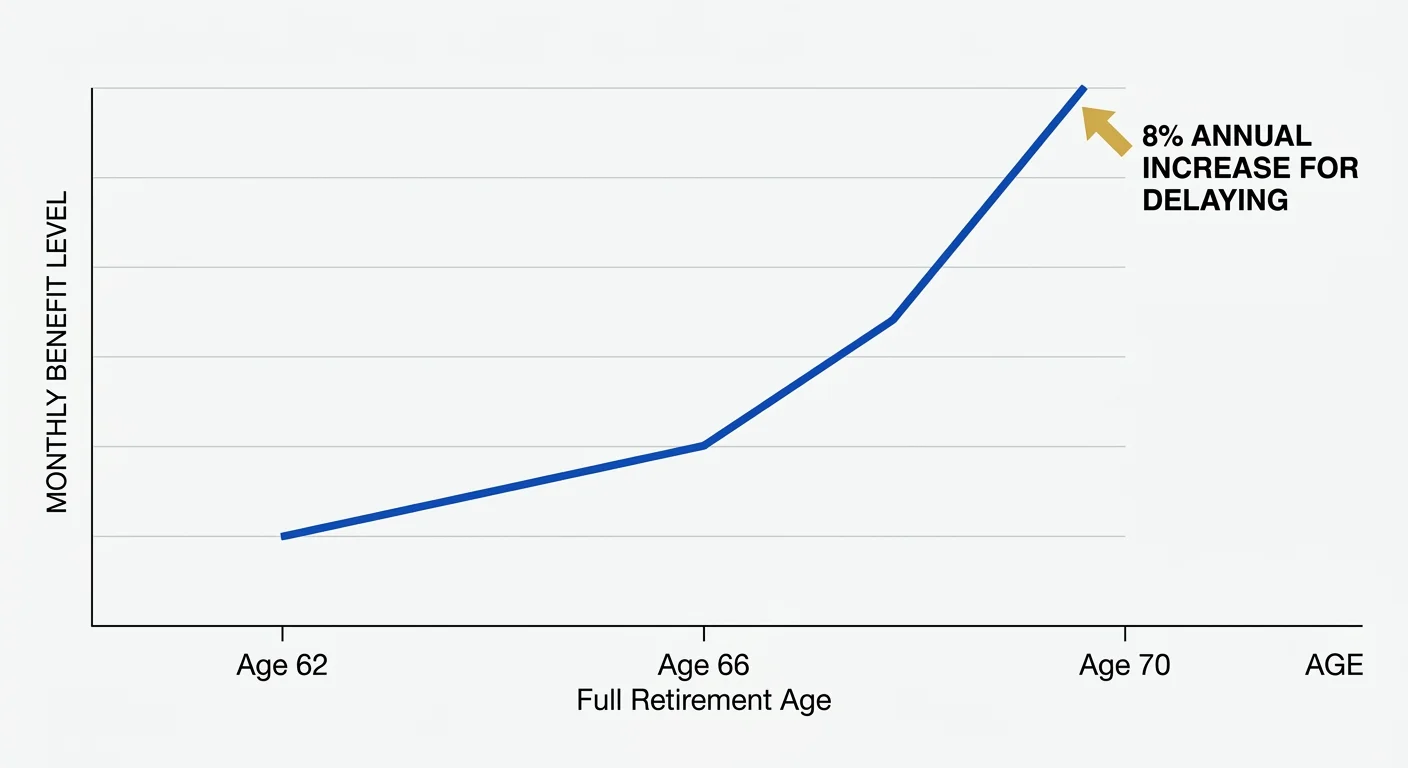

Your portfolio size only tells half the retirement story. Guaranteed income streams provide the ultimate protection against outliving your money, and Social Security remains the bedrock of American retirement. Unfortunately, millions of Boomers permanently handicap their financial security by claiming benefits at the earliest possible age of 62.

Filing at 62 results in a permanent reduction of your monthly check—often by as much as 30%. Furthermore, if you claim early and continue working, you trigger the earnings test. The government will withhold $1 in benefits for every $2 you earn above an annual limit, severely penalizing attempts to double-dip. Conversely, practicing patience yields massive financial rewards. For every year you delay claiming past your Full Retirement Age (FRA), the government increases your benefit by a guaranteed 8%. This delayed retirement credit stops accumulating at age 70, making that the optimal claiming age for maximizing your lifetime payout.

If you face a massive savings shortfall, working a few extra years and delaying your claim to age 70 is mathematically superior to chasing high-risk investments in the stock market. You lock in a significantly higher monthly baseline that adjusts annually for inflation. Coordinate your claiming strategy with your spouse to maximize survivor benefits, and always utilize the calculators provided directly by the Social Security Administration (SSA) before making an irreversible filing decision.

Navigating Medicare and Hidden Healthcare Costs

Ignoring the complexities of healthcare funding is a guaranteed way to drain your retirement accounts. You become eligible for Medicare at age 65, and the decisions you make during your Initial Enrollment Period dictate your costs for the rest of your life. This window opens three months before your 65th birthday, includes your birthday month, and extends three months after. Missing this window triggers severe, lifetime late enrollment penalties.

Original Medicare consists of Part A (hospital insurance) and Part B (medical insurance). While Part A is generally premium-free for most workers, Part B requires a monthly premium deducted directly from your Social Security check. If your retirement income exceeds specific thresholds, you will also face the Income-Related Monthly Adjustment Amount (IRMAA). This hidden surcharge can drastically inflate your healthcare costs if you execute large Roth conversions or sell real estate without proper tax planning.

Furthermore, Medicare does not cover routine dental care, vision care, or long-term nursing home stays. You must proactively evaluate supplemental Medigap policies or Medicare Advantage plans to cap your financial exposure. Explore the official plan finder on Medicare.gov to compare premiums, out-of-pocket maximums, and prescription drug formularies specific to your zip code.

When DIY Isn’t Enough

Managing a small IRA balance is relatively simple, but coordinating a multi-decade drawdown strategy requires advanced expertise. You should hire a fiduciary financial planner if you encounter the following scenarios:

- Executing Complex Tax Strategies: Moving money from traditional tax-deferred accounts into Roth IRAs requires precise tax bracket management. A professional prevents you from accidentally triggering massive tax bills or irreversible Medicare surcharges.

- Navigating Pension Payouts: Deciding between a lump-sum pension payout and a lifetime annuity involves complex actuarial math. You need an expert to analyze interest rates, inflation risks, and survivor benefit options.

- Designing a Withdrawal Sequence: Pulling funds from taxable, tax-deferred, and tax-free accounts in the wrong order accelerates portfolio depletion. A professional calculates the exact sequence of returns to minimize your lifetime tax burden.

- Estate and Legacy Planning: If you intend to pass wealth to heirs, protect a family business, or establish charitable trusts, you need legal and financial professionals to shield those assets from probate and estate taxes.

The Securities and Exchange Commission’s Investor.gov portal provides excellent tools and databases for verifying the credentials of any financial professional you consider hiring.

Avoiding Common Errors with Government Matches and Retirement

As you finalize your late-stage financial plan, sidestep the critical errors that frequently derail Boomers transitioning into retirement:

- Confusing the Saver’s Match with ‘Baby Bonds’: Do not confuse the adult retirement matching program with the heavily publicized 530A ‘Trump Accounts’ launching in 2026. The 530A accounts provide a $1,000 federal seed deposit specifically for eligible children born between 2025 and 2028. The Saver’s Match is strictly for working adults with earned income.

- Failing to Monitor Income Limits: The federal match is not a universal benefit. If you take a part-time consulting job or execute a large stock sale that pushes your adjusted gross income over the federal threshold, you immediately forfeit the matching funds for that tax year.

- Adopting an Excessively Conservative Portfolio: Fearing market volatility, many older adults shift entirely into cash and bonds too early. Because a modern retirement can easily last 30 years, inflation will quietly destroy your purchasing power if your portfolio does not include growth-oriented equities.

Frequently Asked Questions

Who qualifies for the $1,000 federal Saver’s Match?

Lower- and middle-income taxpayers who contribute to an eligible retirement account like an IRA or 401(k) may qualify. The match phases out at higher income levels, so you must review current IRS guidelines based on your exact tax filing status.

Is the Trump $1K Senior Account the same as the Trump Account for children?

No. The highly publicized ‘Trump Accounts’ launching in 2026 are 530A investment vehicles that provide $1,000 in federal seed money for eligible children. The adult retirement match is a completely separate program designed to boost workforce savings.

Can I get the retirement match if I already have a workplace 401(k)?

Yes. While the TrumpIRA platform specifically targets those without workplace access, the underlying Federal Saver’s Match is available to anyone who meets the income requirements and contributes to a qualifying 401(k) or IRA.

Securing your financial future requires action, discipline, and a clear understanding of the tools at your disposal. Claiming the $1,000 federal retirement match is an excellent first step, but it must be part of a much broader strategy. Maximize your catch-up contributions, optimize your Social Security claiming strategy, and fiercely protect your assets from excessive taxation and healthcare costs. The effort you invest today directly dictates the freedom you will experience tomorrow.

This is educational content based on general retirement and financial principles. Individual results vary based on your situation. Always verify current benefit rules, tax laws, and eligibility requirements with official sources like SSA, Medicare.gov, or the IRS.

Last updated: July 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply