Where you live during your career heavily influences the size of your Social Security check. Because the Social Security Administration calculates your monthly benefit using your 35 highest-earning years, states with higher median wages naturally produce retirees with larger checks. If you spent your career in the Northeast or Mid-Atlantic, you are statistically more likely to receive a payout well above the national average. While moving to a new state after retirement will not increase your federal benefits, understanding how lifetime income and filing age shape regional averages can help you maximize your claiming strategy. Here is a closer look at the states leading the nation in median Social Security payouts and the economic factors driving those higher numbers.

The Mechanics Behind High-Benefit States

You might wonder why two people retiring in the same country can experience vastly different retirement incomes. The federal government does not issue larger checks simply because a retiree lives in an expensive ZIP code. Your geographic location at the exact moment you retire plays absolutely no role in the underlying math of your benefit.

Instead, the disparity across state lines comes down to demographics, regional economies, and local labor markets. The Social Security Administration tracks your earnings throughout your entire working life. When you apply for benefits, they adjust your historical earnings for inflation, pull out your 35 highest-earning years, and calculate your Average Indexed Monthly Earnings (AIME). This figure then runs through a formula to determine your Primary Insurance Amount (PIA)—the baseline monthly check you receive at full retirement age.

Because the formula relies entirely on wage history, regions that sustain high-paying industries over decades naturally produce populations with maximized earnings records. Three core factors heavily skew these averages:

- Industrial and Economic Hubs: States anchoring major industries—such as technology, biotechnology, aerospace, and high finance—pay premiums for specialized talent. Workers in these sectors frequently hit the Social Security taxable maximum early in their careers.

- Education Levels: States with dense concentrations of advanced degree holders reliably show higher median lifetime earnings.

- Delayed Claiming Patterns: High-income earners often have the luxury of robust personal savings, 401(k)s, and pensions. This financial cushion allows them to delay claiming Social Security until age 70, which permanently increases their monthly benefit check.

At a Glance: The Top 10 States for Social Security Benefits

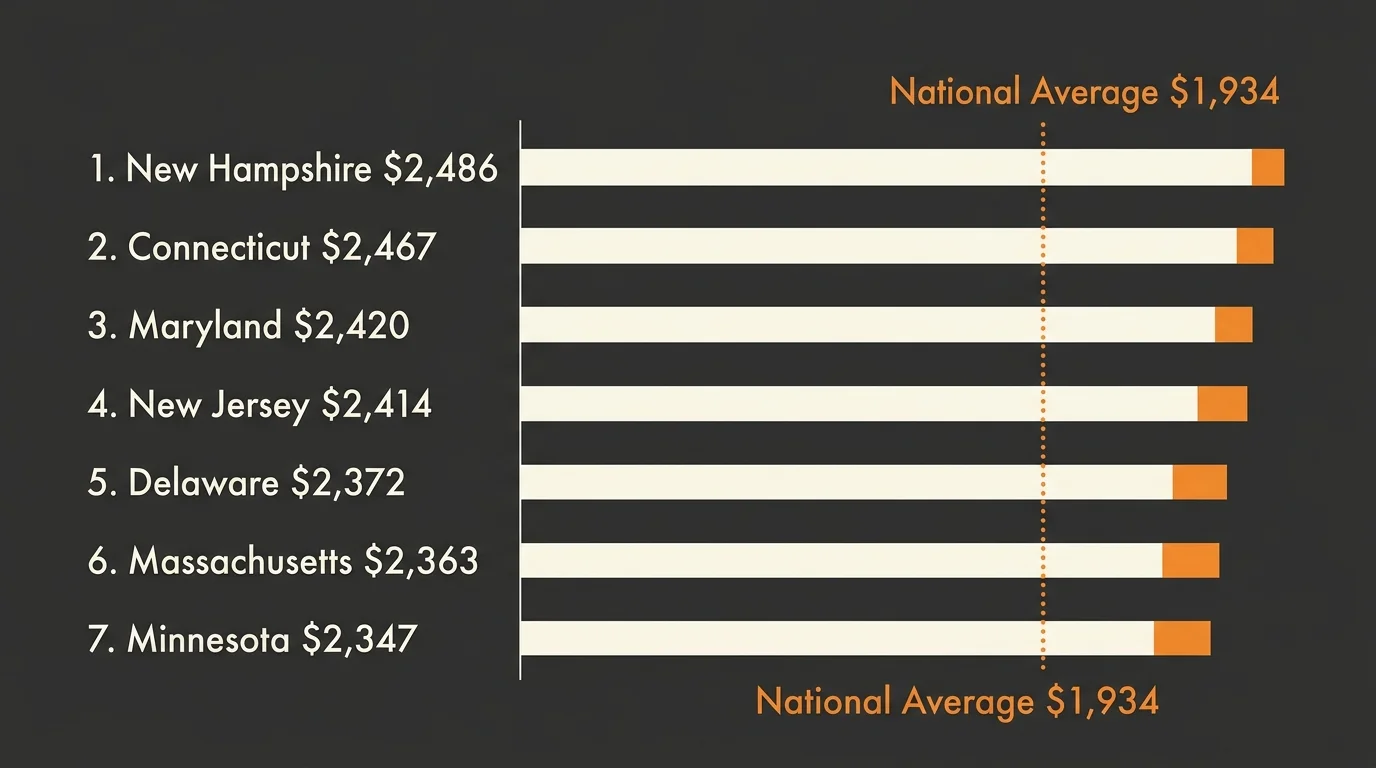

When you look at the national landscape, the average monthly Social Security benefit sits near $1,934. However, the top-tier states blow far past that baseline. The following states boast the highest estimated median monthly benefits for retirees in 2026.

| Rank | State | Estimated Monthly Benefit (2026) | Key Economic Drivers |

|---|---|---|---|

| 1 | New Hampshire | $2,486 | Tech manufacturing, regional Boston spillover, no state wage tax |

| 2 | Connecticut | $2,467 | Hedge funds, insurance, advanced corporate finance |

| 3 | Maryland | $2,420 | Federal contracting, defense, bioscience |

| 4 | New Jersey | $2,414 | Pharmaceuticals, proximity to NYC financial sectors |

| 5 | Delaware | $2,372 | Corporate law, banking, chemical manufacturing |

| 6 | Massachusetts | $2,363 | Higher education, biotechnology, healthcare technology |

| 7 | Minnesota | $2,347 | Medical technology, diversified Fortune 500 headquarters |

| 8 | Washington | $2,328 | Tech giants, software engineering, aerospace |

| 9 | Rhode Island | $2,310 | Healthcare, financial services, Northeast corridor alignment |

| 10 | Virginia | $2,294 | Dulles tech corridor, defense, Pentagon leadership |

A Closer Look at the Leading Economies

Statistics alone rarely tell the full story. To understand why these exact regions consistently produce the highest Social Security checks, you have to look at the economic engines powering their local labor forces.

1. New Hampshire

New Hampshire frequently claims the top spot for retiree benefits. The state boasts a remarkably robust economy anchored by precision manufacturing and specialized technology sectors. Geographically, its southern border benefits massively from the Boston economic spillover, allowing workers to command premium New England salaries. Furthermore, New Hampshire levies no state income tax on regular wages. This tax environment encourages high-earning professionals to remain in the state long-term, thereby cementing their 35 years of high earnings within the local demographic data.

2. Connecticut

Connecticut has long been synonymous with high finance. The Hartford and Fairfield County corridors serve as global hubs for hedge funds, insurance companies, and wealth management firms. Because Social Security benefits are directly tied to an individual’s lifetime earnings, a population saturated with highly compensated financial executives naturally skews the median benefit upward. Retirees in Connecticut frequently hit the maximum taxable earnings limit year after year, building formidable retirement records.

3. Maryland

Proximity to the nation’s capital heavily influences Maryland’s commanding position on this list. The state is home to numerous federal agencies, massive defense contractors, and highly specialized bioscience firms. Government contractors, cybersecurity experts, and tech workers in areas like Bethesda and Rockville command premium salaries. Maryland also holds one of the highest concentrations of residents with advanced academic degrees in the country; higher education reliably correlates with elevated lifetime earnings, pushing their retirement checks past the $2,400 mark.

4. New Jersey

Acting as a primary residential hub for professionals commuting into New York City, New Jersey captures the retirement data of some of the highest earners in the global corporate and financial sectors. The state itself also hosts a massive pharmaceutical and telecommunications industry. While the cost of living in New Jersey is notoriously high, the corresponding salaries demanded during the working years result in robust Social Security checks when those workers finally leave the labor force.

5. Delaware

While geographically small, Delaware punches far above its weight class economically. Known broadly as the corporate capital of America, the state houses massive banking, legal, and chemical manufacturing sectors. These high-paying corporate headquarters generate significant regional payrolls. Additionally, Delaware is highly favored by affluent retirees due to its lack of sales tax and low property taxes. Many high-earning out-of-state workers retire here, directly pulling the state’s median benefit numbers up.

6. Massachusetts

Massachusetts operates as a global powerhouse in higher education, biotechnology, and healthcare. The Boston and Cambridge metropolitan areas act as massive engines of economic growth, employing hundreds of thousands of highly paid specialists and researchers. Workers who spend their 35-year benchmark careers in these advanced sectors build an optimal earnings record, leading to outsized monthly checks upon retirement.

7. Minnesota

The only Midwestern state to consistently breach the absolute top tier, Minnesota thrives on a highly diversified economy. The Minneapolis-St. Paul region is home to numerous Fortune 500 companies across retail, medical technology, banking, and agribusiness. Minnesota also boasts exceptional labor force participation rates and consistent wage growth, ensuring that its residents build solid, uninterrupted earning histories—a critical factor in the Social Security calculation formula.

8. Washington

The Pacific Northwest economic engine is fueled by massive aerospace and technology sectors. With companies pulling global talent to the Seattle region, Washington has experienced decades of explosive wage growth. Because technology compensation packages frequently push base salaries beyond the Social Security taxable maximum, retirees who built their careers here naturally collect top-tier federal benefits.

9. Rhode Island

Despite its small size, Rhode Island benefits from a dense, highly developed economy heavily reliant on healthcare, education, and specialized financial services. Its immediate proximity to both the Boston and New York economies keeps regional wages highly competitive. Retirees here reflect a legacy of steady professional sector salaries that characterized the region over the last several decades.

10. Virginia

Driven almost entirely by the economic force of Northern Virginia, the state rounds out the top ten. The Dulles technology corridor, combined with the massive presence of the Department of Defense, Pentagon staff, and global security contractors, creates a dense population of high earners. The steady, high-paying nature of government contracting ensures that these workers maximize their Social Security credits with remarkable consistency.

The Wealth Gap: Why Cost-of-Living Adjustments Compound the Divide

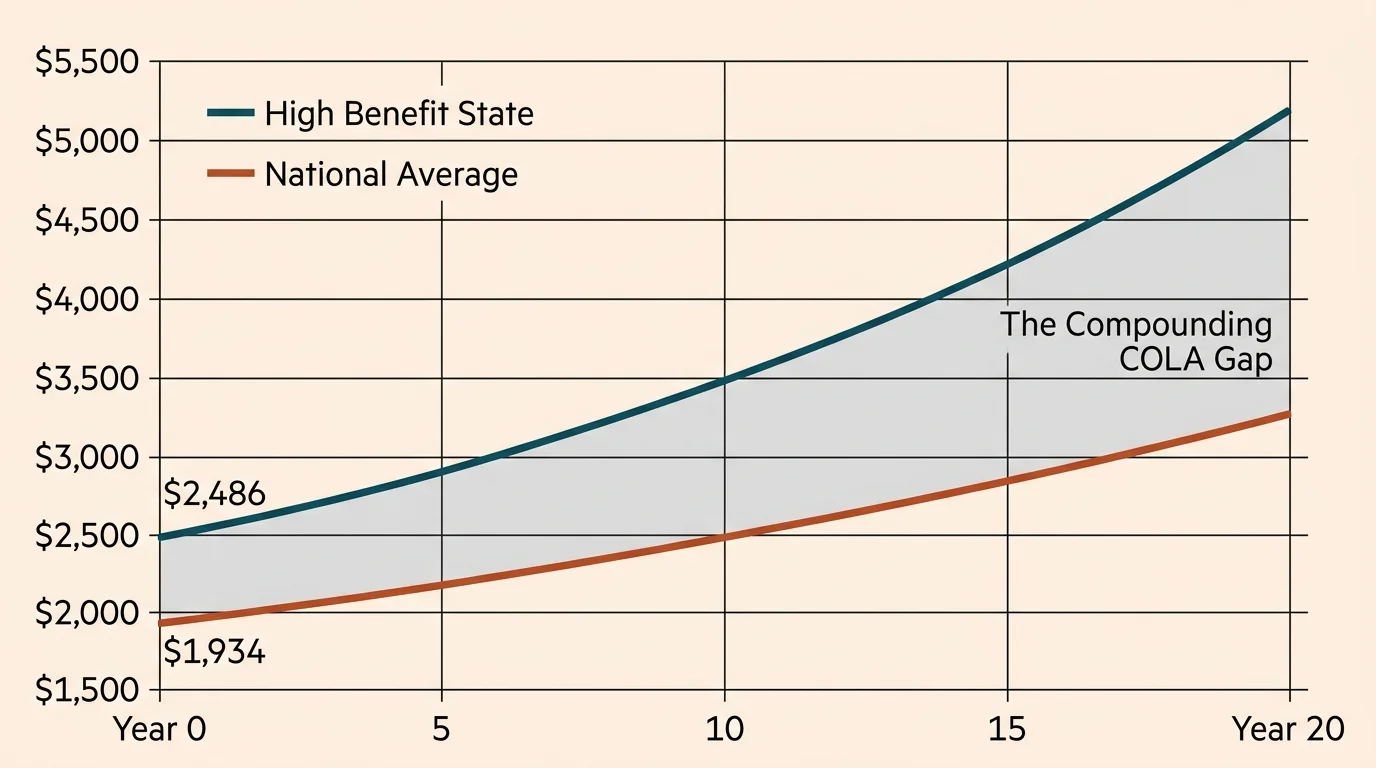

Understanding how the annual Cost-of-Living Adjustment (COLA) works provides crucial insight into why these ten states consistently pull away from the rest of the country. When inflation adjustments are announced, they are always delivered as a percentage multiplier, not a flat dollar amount.

If the government announces a 2.8 percent COLA, a retiree living in Mississippi receiving $1,700 a month will see an increase of roughly $47. However, a retiree in New Hampshire receiving $2,400 a month will see an increase of roughly $67. Over a twenty-year retirement, these percentage-based adjustments compound dramatically. The math fundamentally guarantees that high-benefit states will continue to widen the dollar gap over low-benefit states over time.

What Can Go Wrong: Misinterpreting Benefit Statistics

Reading lists of top-performing states can accidentally lead to poor retirement decisions if you misinterpret what the data actually represents. Watch out for these common traps.

Mistake 1: Moving for the Wrong Reasons

A surprising number of people mistakenly believe that relocating to a state like New Hampshire or Connecticut will increase their Social Security check. This is entirely false. Your benefit is determined strictly by your personal earnings history and your claiming age. A high-earning state average simply means the people who already live there made higher wages during their working years. Moving there in retirement will not alter your historical W-2s.

Mistake 2: Ignoring State Taxation on Benefits

A high gross monthly check does not always equal high net income. Several of the states on the top 10 list—including Connecticut, Minnesota, and Rhode Island—tax Social Security benefits at the state level under certain income conditions. If you blindly move to a state boasting high average benefits without consulting a resource like AARP to understand the local tax code, you could end up surrendering a portion of your income to the state department of revenue.

Mistake 3: Overlooking the Cost of Living Reality

States with the highest Social Security checks almost universally feature the highest costs of living. A $2,400 monthly benefit does not stretch very far in New Jersey or Massachusetts when property taxes, healthcare costs, and housing are factored in. Often, a retiree collecting $1,800 a month in a tax-friendly, low-cost state will experience more monthly cash flow than someone collecting $2,400 in a premium coastal market.

Strategies to Increase Your Own Social Security Benefit

You cannot change the past, but you maintain immense control over how you handle the final years before retirement. If you want to push your own monthly check toward the numbers seen in the top 10 states, focus on the variables you can actually control.

- Work a Full 35 Years: The formula averages your 35 highest-earning years. If you only work 30 years, the government inserts five “zeros” into your calculation. Replacing those zero-income years with even modest earnings will noticeably lift your baseline benefit.

- Maximize Earnings Now: Because your benefit scales with your income up to the taxable maximum, late-career salary negotiations, promotions, or side businesses directly pad your future retirement checks.

- Delay Your Claim: The most powerful lever you have is patience. Claiming at age 62 permanently locks in a reduced benefit. Waiting until your full retirement age ensures you get 100 percent of your earned amount. Waiting until age 70 maxes out the delayed retirement credits.

“Every year you delay claiming Social Security past your full retirement age, your benefit grows by a guaranteed 8 percent. There is no other investment that gives you a risk-free 8 percent return.” — Suze Orman, Personal Finance Expert

When to Consult a Professional

Navigating the transition from active income to fixed income involves complex math and permanent decisions. You should seek guidance from a fee-only fiduciary planner or a Social Security optimization expert in the following scenarios:

- You are coordinating spousal or survivor benefits: Dual-income households face complex filing decisions. A professional can run software models to determine the exact month each spouse should claim to maximize lifetime household income.

- You own a small business: Business owners must balance the tax advantages of taking lower W-2 salaries against the long-term cost of reducing their future Social Security benefits.

- You are planning a cross-country relocation: If you are moving to a new state, you need a professional to assess state income taxes, estate taxes, and how regional Medicare supplement premiums will impact your bottom line.

- You have a government pension: If you spent time working in a local, state, or federal job that did not withhold Social Security taxes, you need an expert to navigate the Windfall Elimination Provision (WEP) or the Government Pension Offset (GPO).

Frequently Asked Questions

Does my Social Security check decrease if I move to a cheaper state?

No. The Social Security Administration bases your monthly benefit entirely on your lifetime earnings record and the exact age at which you file your claim. Relocating to a state with a lower cost of living does not reduce your federal benefit. This makes geographic arbitrage—earning a high salary in an expensive state and retiring in a cheaper state—a highly effective wealth strategy.

Do the states with the highest Social Security benefits also tax those benefits?

Some do, but not all. Connecticut, Minnesota, and Rhode Island currently tax Social Security benefits at the state level, though they offer exemptions based on adjusted gross income. Conversely, high-benefit states like New Hampshire, New Jersey, and Washington do not tax Social Security at the state level.

What is the absolute maximum Social Security benefit?

To receive the absolute maximum benefit, you must earn at or above the Social Security taxable maximum for at least 35 years and delay claiming your benefits until age 70. Very few workers meet all of these criteria, which is why state averages sit thousands of dollars below the theoretical absolute maximum.

How do cost-of-living adjustments (COLAs) impact high-benefit states differently?

Because COLAs are calculated as a percentage increase rather than a flat dollar increase, retirees with larger baseline benefits receive larger actual dollar increases. Consequently, retirees living in the 10 states with the highest median checks receive the largest aggregate dollar raises every time inflation triggers an adjustment.

Protecting Your Retirement Income

Reviewing state-by-state data provides fascinating insight into the geographic distribution of wealth in America, but your retirement requires a personalized roadmap. Whether you spent your career in the tech hubs of Washington or the financial centers of Connecticut, your ultimate financial security relies on proper planning, disciplined saving, and a calculated claiming strategy. Take the time to create a personalized “my Social Security” account online to verify your earnings record and run estimates based on your actual data. Armed with accurate projections, you can make the precise, informed decisions necessary to protect your lifestyle.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, health needs, tax situation, and goals—may require different approaches. When in doubt, consult a licensed professional.

Last updated: July 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply