If you are 68 years old, your average monthly Social Security check in 2026 is approximately $2,059. Knowing exactly where you stand against this national average helps you evaluate your retirement income strategy and make informed decisions about your financial future. While many Americans begin collecting benefits at age 62, waiting until age 68 provides an eight percent boost over your Full Retirement Age amount if your FRA is 67. The difference between claiming early and delaying can mean hundreds of extra dollars in your pocket every single month. By comparing your own benefit to the typical 68-year-old’s payout, you gain critical insight into how well your current savings plan complements your guaranteed government income.

Decoding the 68-Year-Old Average Benefit

The $2,059 figure represents a national average across millions of retirees, smoothing out the differences between high earners and those with modest incomes. The Social Security Administration determines your specific benefit using a formula based on your Average Indexed Monthly Earnings (AIME). The government reviews your entire work history, indexes your past wages to account for inflation, and selects your highest 35 years of earnings. They run this average through a specialized calculation to find your Primary Insurance Amount (PIA)—the exact baseline benefit you earn at your Full Retirement Age.

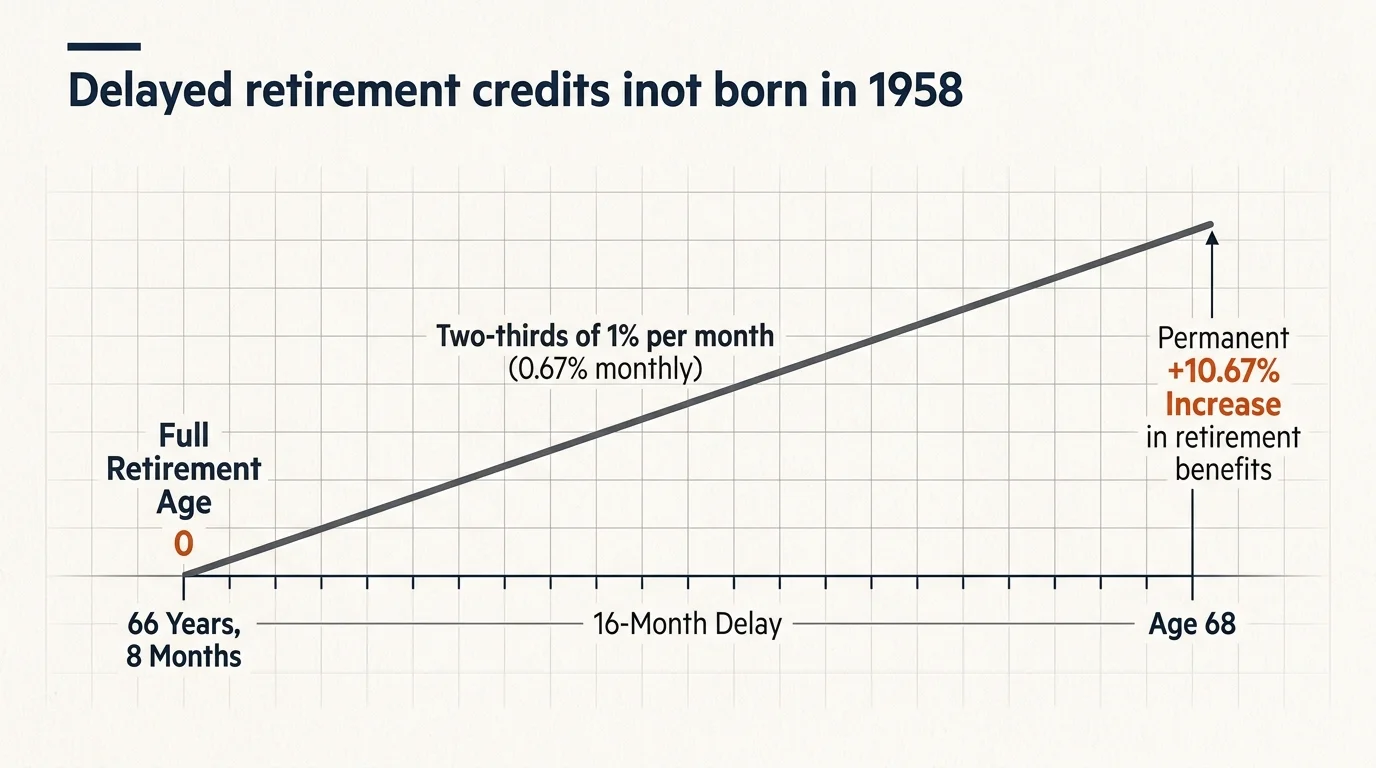

Your birth year heavily influences how the government calculates your claiming age adjustments. If you turn 68 in 2026, you were born in 1958. For your specific birth cohort, the government defines your Full Retirement Age as 66 and 8 months. By waiting until your 68th birthday to claim benefits, you delayed your application by exactly 16 months past your FRA. The system rewards this patience with delayed retirement credits, adding two-thirds of one percent to your baseline benefit for every single month you wait.

Those 16 months of earned credits give you an approximate 10.67 percent permanent increase over your baseline payout. If you were born in 1960 or later, your Full Retirement Age shifts to 67. In that scenario, claiming at age 68 provides an exact 8 percent boost. Understanding the mechanics behind these numbers explains why the average 68-year-old receives a significantly higher check than someone who claimed at the earliest possible age.

How Age 68 Compares to Other Claiming Milestones

Timing your Social Security claim remains one of the most consequential financial decisions you make in retirement. You maintain complete control over when you file between ages 62 and 70. Reviewing the average benefits across different ages illustrates the severe financial penalty of claiming early and the substantial reward of waiting.

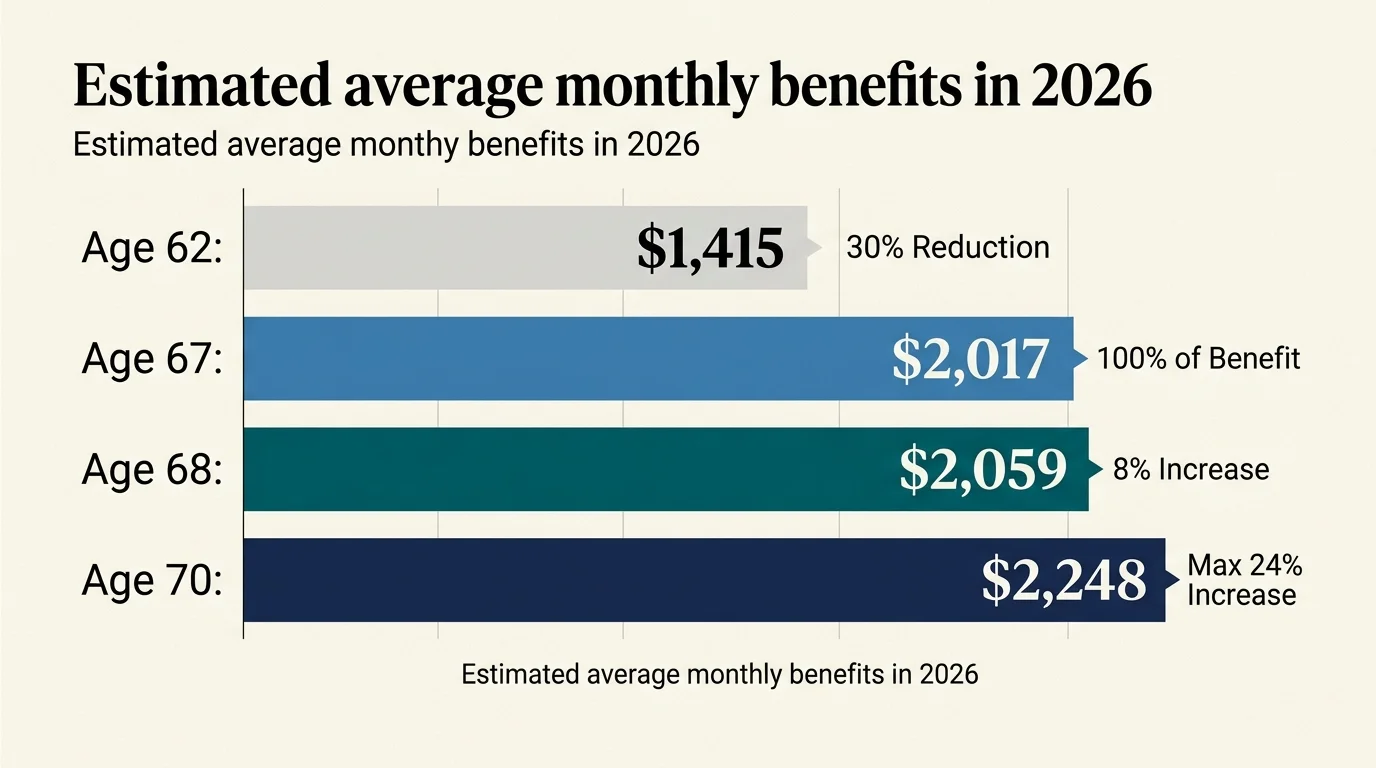

The table below demonstrates the estimated average monthly benefits for retirees at various claiming ages in 2026, highlighting the direct financial impact of your claiming timeline.

| Claiming Age | Estimated Average Monthly Benefit (2026) | Impact on Standard Benefit |

|---|---|---|

| Age 62 | $1,415 | Permanent 30% reduction from FRA |

| Age 67 (FRA for 1960+) | $2,017 | 100% of earned benefit |

| Age 68 | $2,059 | 8% increase via delayed credits |

| Age 70 | $2,248 | Maximum 24% increase |

A 68-year-old taking home roughly $2,059 per month secures over $600 more than a typical 62-year-old. Over a 20-year retirement, that monthly difference compounds into more than $144,000 in additional guaranteed income. Delaying your claim requires relying on your personal savings or continuing to work during your mid-sixties, but the resulting boost to your lifelong government benefit provides an exceptional hedge against longevity risk.

Factors That Pull Your Benefit Above or Below Average

If your current monthly deposit looks dramatically different than the $2,059 national average, your personal work history and family structure hold the answers. High earners who consistently maxed out the Social Security wage base for 35 years can see monthly checks exceeding $3,800 at age 68. Conversely, those with gaps in their employment history or lower lifetime wages receive smaller distributions.

The 35-year rule dictates a massive portion of your final calculation. If you worked for only 28 years to stay home and raise children, the government inserts seven zeroes into your earnings average. Those zeroes severely depress your Primary Insurance Amount. Working a few extra years in your sixties—even part-time—allows you to replace those zeroes with actual income, steadily driving your lifetime average upward.

Spousal benefits also shift the data. If you lack the required 40 work credits to qualify for your own benefit, you may receive a spousal benefit based entirely on your partner’s earnings record. A spousal benefit maxes out at 50 percent of the primary earner’s Full Retirement Age amount. It is vital to note that spousal benefits do not earn delayed retirement credits; they plateau at your FRA. If you delay a pure spousal benefit until age 68, you leave money on the table without generating any future financial upside.

The Hidden Impact of Medicare on Your Net Check

You must differentiate between your gross benefit and your net benefit. The $2,059 average represents a gross figure. However, most 68-year-olds participate in Medicare, and the government streamlines the premium collection process by deducting Part B costs directly from your Social Security payment.

When you review your monthly bank statement, the deposit you see reflects your gross benefit minus your standard Part B premium. Medicare.gov outlines the baseline costs, but higher-income retirees face an additional surcharge known as the Income-Related Monthly Adjustment Amount (IRMAA). If your modified adjusted gross income from two years prior exceeded specific thresholds, the government subtracts a much larger premium from your Social Security check.

This dynamic creates a cash-flow shock for many new retirees. A single retiree with substantial capital gains or aggressive IRA withdrawals might trigger IRMAA, watching their net Social Security check shrink unexpectedly. Proactive tax management keeps your taxable income below these thresholds, preserving more of your hard-earned Social Security money.

Avoiding Common Errors

Many 68-year-olds stumble into easily preventable financial traps because they misunderstand the complex rules governing retirement income. The most widespread error involves the taxation of Social Security benefits. Your age does not exempt you from federal income taxes. The Internal Revenue Service uses a metric called “combined income” to determine your tax liability. You calculate combined income by adding your adjusted gross income, your nontaxable interest, and half of your annual Social Security benefits.

If your combined income lands between $25,000 and $34,000 as a single filer, up to 50 percent of your benefit becomes taxable. If your combined income exceeds $34,000, up to 85 percent of your benefit faces federal income tax. Married couples filing jointly face similar thresholds at $32,000 and $44,000. Failing to plan for this tax liability often leads to frustrating tax bills in April.

“Every year you wait to claim Social Security between your full retirement age and 70, your benefit guarantees an 8 percent return. You cannot get that guaranteed return anywhere else.” — Suze Orman, Personal Finance Expert

Another common mistake involves suspending benefits incorrectly. If you claimed at 62 but now realize you want a higher payout, you possess the right to voluntarily suspend your benefits once you reach your Full Retirement Age. A 68-year-old can suspend payments today, allowing the benefit to earn delayed retirement credits until age 70. However, many retirees forget that suspending your benefit also suspends any spousal or dependent benefits tied to your record.

When DIY Isn’t Enough

Managing standard retirement accounts and Social Security claims seems straightforward until you encounter specialized life circumstances. You should seek professional guidance when your financial picture involves moving parts that trigger obscure government rules.

Consider bringing in a professional if you worked as a teacher, firefighter, or government employee in a role that did not withhold Social Security taxes. You will likely face the Windfall Elimination Provision (WEP) or the Government Pension Offset (GPO). These provisions aggressively reduce your Social Security benefits, completely changing your retirement income projections. Standard online calculators frequently fail to account for the WEP, leading retirees to overestimate their future checks.

Divorced retirees also require careful planning. If your marriage lasted at least ten years and you remain unmarried, you can claim benefits on your ex-spouse’s earnings record. Coordinating this strategy without alerting your former spouse involves navigating strict filing rules. Utilizing resources from Investor.gov or hiring a fee-only fiduciary planner ensures you maximize these obscure claiming strategies without triggering a penalty.

Actionable Steps to Manage Your Social Security Income

You hold the power to optimize your retirement cash flow right now. Taking immediate, concrete actions protects your guaranteed income and ensures you keep more money in your pocket.

- Review your earnings record annually: Log into your official Social Security account and verify that your annual wages match your past tax returns. A missing year of income drastically reduces your lifetime average.

- Coordinate claims with your spouse: If you are married, sit down and map out a joint claiming timeline. Often, the lower-earning spouse claims early to generate cash flow, while the higher-earning spouse delays until age 70 to maximize the permanent survivor benefit.

- Submit a W-4V for voluntary tax withholding: Avoid massive tax bills at the end of the year by asking the government to withhold a set percentage of your Social Security check for federal taxes. You can withhold 7, 10, 12, or 22 percent.

- Manage your IRA withdrawal sequence: Work strategically with your savings to stay below IRMAA thresholds. Mixing Roth IRA withdrawals (which do not count toward combined income) with traditional IRA withdrawals helps you navigate your tax brackets safely.

“Retirement is not the end of your financial life; it is the beginning of a new phase where you transition from accumulating assets to managing income.” — Jean Chatzky, Financial Editor

Frequently Asked Questions

Are Social Security benefits taxable at age 68?

Yes. Your age provides no special exemption from federal income taxes regarding Social Security. If your combined income exceeds the strict IRS thresholds, the federal government taxes up to 85 percent of your benefit. Additionally, depending on where you live, you might owe state income taxes on your monthly check.

Can I still work if I collect Social Security at 68?

Absolutely. Because you surpassed your Full Retirement Age, the restrictive Social Security earnings test no longer applies to your situation. You can earn an unlimited amount of income from a job or business without the government withholding a single dime of your monthly retirement benefit.

What happens if I suspend my benefits at 68?

If you already receive monthly payments, you can voluntarily contact the government and suspend your benefits. During the suspension period, your baseline benefit earns an 8 percent annual return via delayed retirement credits. Your payments will automatically resume at a much higher monthly rate when you reach age 70.

Will Medicare premiums continue to increase and reduce my net check?

Yes. Medicare Part B premiums generally rise over time to keep pace with healthcare inflation. While the annual Social Security Cost-of-Living Adjustment (COLA) usually increases your gross check enough to cover the higher Medicare premium, a “hold harmless” provision ensures that standard Medicare premium increases cannot mathematically reduce your net Social Security check below the previous year’s amount.

You worked hard for decades to earn your Social Security benefit. By understanding how your 68-year-old payout compares to the national average, you equip yourself with the knowledge needed to handle taxes, manage Medicare costs, and stretch your savings further. Take a moment this week to review your official earnings record and evaluate your upcoming withdrawal strategy. Small adjustments made today create massive financial security for the rest of your life.

This article provides general retirement education and information only. Every retiree’s situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: March 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply