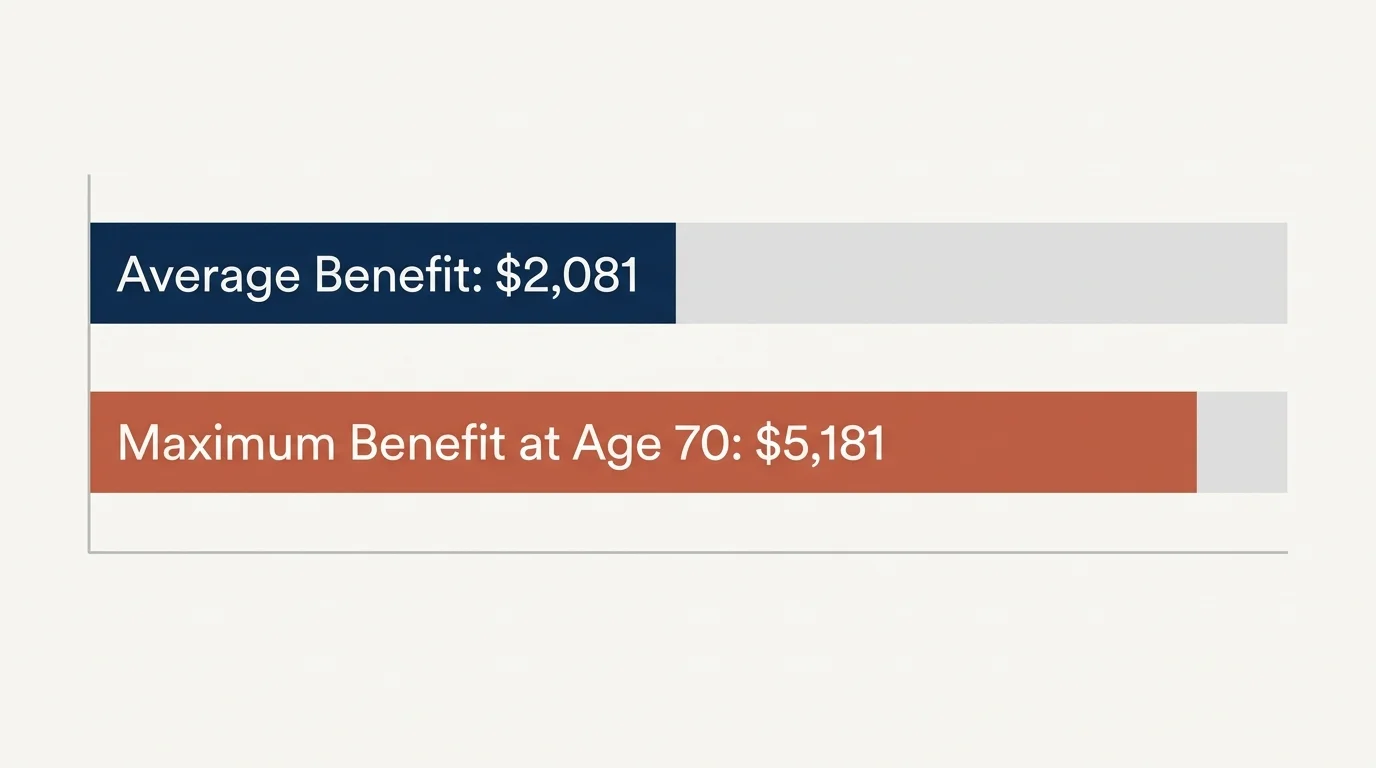

If you are wondering how your retirement income stacks up this summer, the average Social Security check for a retired worker in August 2026 is approximately $2,081. While hitting the average might feel reassuring, the reality is that a $24,972 annual baseline is rarely enough to comfortably cover housing, healthcare, and daily living expenses on its own. Your exact payment depends heavily on your 35 highest-earning years and the precise month you claim your benefits. Understanding where you fall on the spectrum—from the absolute minimums to the maximum possible payout of $5,181 at age 70—gives you the clarity needed to adjust your withdrawal strategies and maximize the retirement nest egg you have worked decades to build.

The Average Social Security Check in August 2026

When you look at the monthly data released by the Social Security Administration, the numbers tell a fascinating story about how Americans fund their later years. As of mid-2026, the average monthly benefit for a retired worker sits right around $2,081. This figure is the result of years of steady wage growth combined with recent cost-of-living adjustments (COLAs) designed to help seniors keep pace with inflation.

However, averages can be deceiving. The $2,081 figure specifically reflects the benefits paid to retired workers. If you look at the broader Social Security system, the averages shift dramatically depending on the type of beneficiary. For instance, disabled workers generally receive a lower average monthly payment, while widowers and surviving spouses see different baselines entirely. Furthermore, geographic location plays a silent but significant role in these statistics. Retirees living in states with higher median incomes—such as New Jersey, Maryland, or Connecticut—often pull higher average Social Security checks simply because their lifetime wages were higher, thus feeding more money into the system’s calculation engine.

Comparing your check to the national average is a great starting point, but it should not dictate your financial confidence. A $2,081 monthly payment might stretch beautifully in a paid-off home in the rural Midwest, yet fall entirely flat for a renter facing property tax pass-throughs in a coastal city. The real value of knowing the average is recognizing that Social Security was never designed to be your sole source of income; it was built to replace roughly 40 percent of a median earner’s pre-retirement wages. If you are earning well above the median, that replacement rate drops even lower, placing the burden of your lifestyle squarely on your personal savings, pensions, and investment accounts.

Summary: The Essentials at a Glance

If you need the most critical facts before diving into the mathematical details of your retirement benefits, here are the core concepts driving your August 2026 payout:

- The Baseline Average: The typical retired worker is receiving approximately $2,081 this month.

- The Absolute Maximum: High earners who wait until age 70 to claim can capture a maximum monthly payout of $5,181.

- The 35-Year Rule: Your benefit is calculated using your 35 highest-earning years; working fewer than 35 years means zeroes will drag your average down.

- The Medicare Deduction: The published average of $2,081 is a gross figure. Your actual bank deposit will be lower after mandatory Medicare Part B premiums are deducted.

- The Timing Penalty: Claiming at age 62 permanently reduces your monthly check by up to 30 percent compared to your full retirement age amount.

Maximum Benefits vs. Average Benefits (Where Do You Stand?)

Understanding the vast gap between the average check and the maximum possible check reveals exactly how the system rewards patience and high lifetime earnings. Many pre-retirees assume that simply earning a good salary guarantees them the maximum benefit. In reality, hitting the absolute peak requires threading a very specific financial needle over several decades.

To secure the maximum Social Security payout, you must meet three stringent requirements. First, you must work for at least 35 years. Second, in every single one of those 35 years, your earnings must hit or exceed the Social Security taxable maximum—the cap on which you pay payroll taxes. In 2026, that taxable maximum sits deep into the six figures. Third, you must delay claiming your benefit until age 70, capturing every possible delayed retirement credit.

Here is how the maximum monthly benefits break down for new claimants in 2026 based on the age they file:

| Filing Age | Maximum Monthly Benefit (2026) | Annualized Maximum Income |

|---|---|---|

| Age 62 (Earliest Eligibility) | $2,969 | $35,628 |

| Full Retirement Age (Age 67) | $4,152 | $49,824 |

| Age 70 (Maximum Delay) | $5,181 | $62,172 |

When you contrast these maximums with the $2,081 average, the impact of claiming age becomes undeniable. A worker qualifying for the maximum benefit who chooses to file at 62 leaves more than $2,200 on the table every single month compared to what they would receive at age 70. Over a 20-year retirement, that differential translates to hundreds of thousands of dollars in lost guaranteed, inflation-adjusted income.

“Every year you wait to claim Social Security between your full retirement age and 70, you get a guaranteed 8 percent return on your money. Where else can you find a guaranteed 8 percent today?” — Suze Orman, Personal Finance Expert

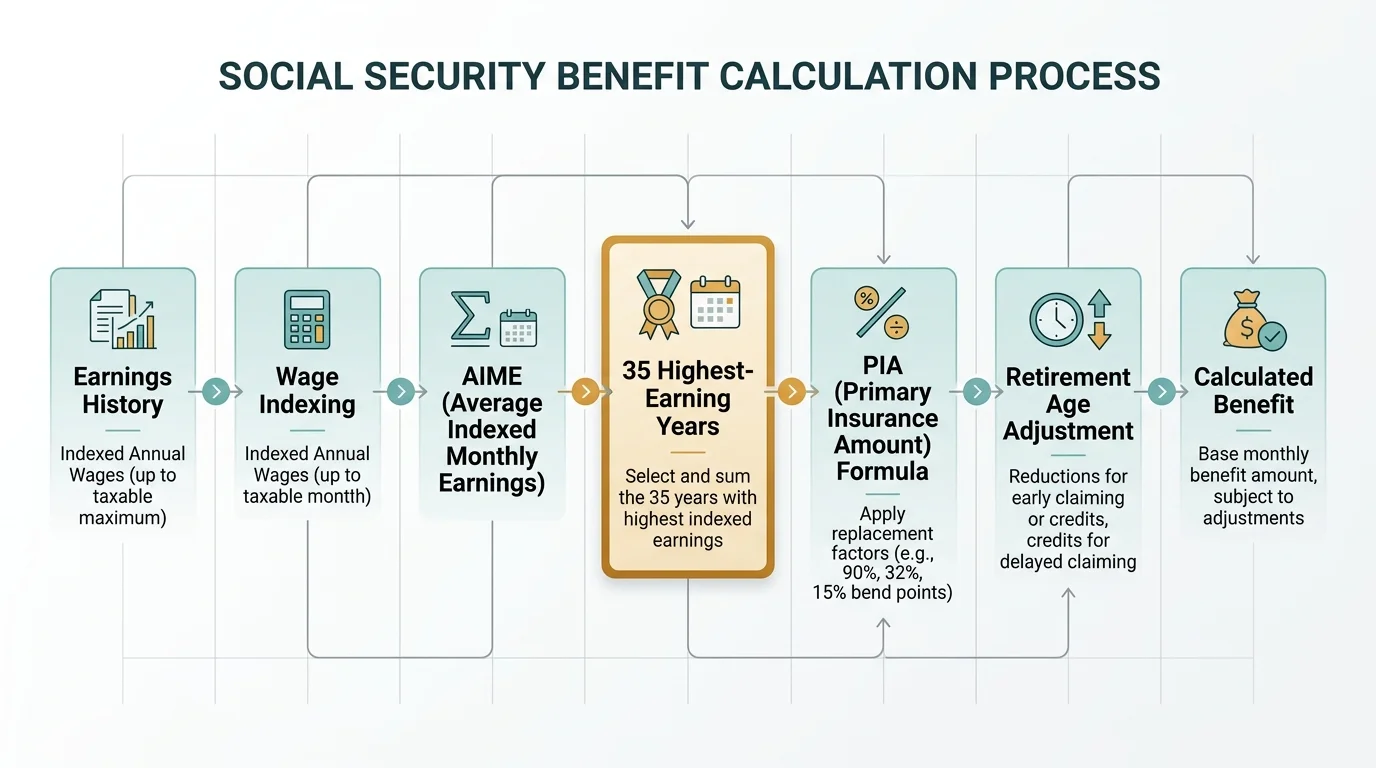

How the Social Security Administration Calculates Your Check

Your monthly payment is not pulled out of a hat, nor is it based solely on the last few years of your career. The Social Security calculation engine is highly structured, deeply historical, and intentionally designed to provide a stronger safety net for lower-income workers while still rewarding high earners.

The process begins with your earnings history. The SSA reviews your entire working life and adjusts your past wages for inflation, a process known as indexing. This ensures that the $25,000 you earned in 1990 is valued appropriately in today’s economic environment. Once your entire history is indexed, the system isolates your 35 highest-earning years. If you worked for 40 years, your lowest five earning years are entirely dropped from the equation. Conversely, if you stepped away from the workforce to raise children or care for aging parents and only accumulated 28 years of earnings, the system inserts seven zeroes into your calculation, which significantly dilutes your average.

These 35 years are then divided by 420 (the total number of months in 35 years) to establish your Average Indexed Monthly Earnings, commonly referred to as your AIME. But the SSA does not just cut you a check for your AIME. They run that figure through a progressive formula to determine your Primary Insurance Amount (PIA)—the exact baseline benefit you are entitled to at your full retirement age.

This progressive formula uses specific thresholds called “bend points.” A very high percentage of your lowest earnings is replaced by Social Security, while a much smaller percentage of your higher earnings is replaced. This is why a worker who earned $50,000 a year might see Social Security replace half their pre-retirement income, while an executive earning $200,000 a year will only see the system replace a small fraction of their former lifestyle. The design is intentional; it prevents seniors on the lowest end of the economic spectrum from falling into poverty, while expecting wealthier retirees to rely heavily on private investments.

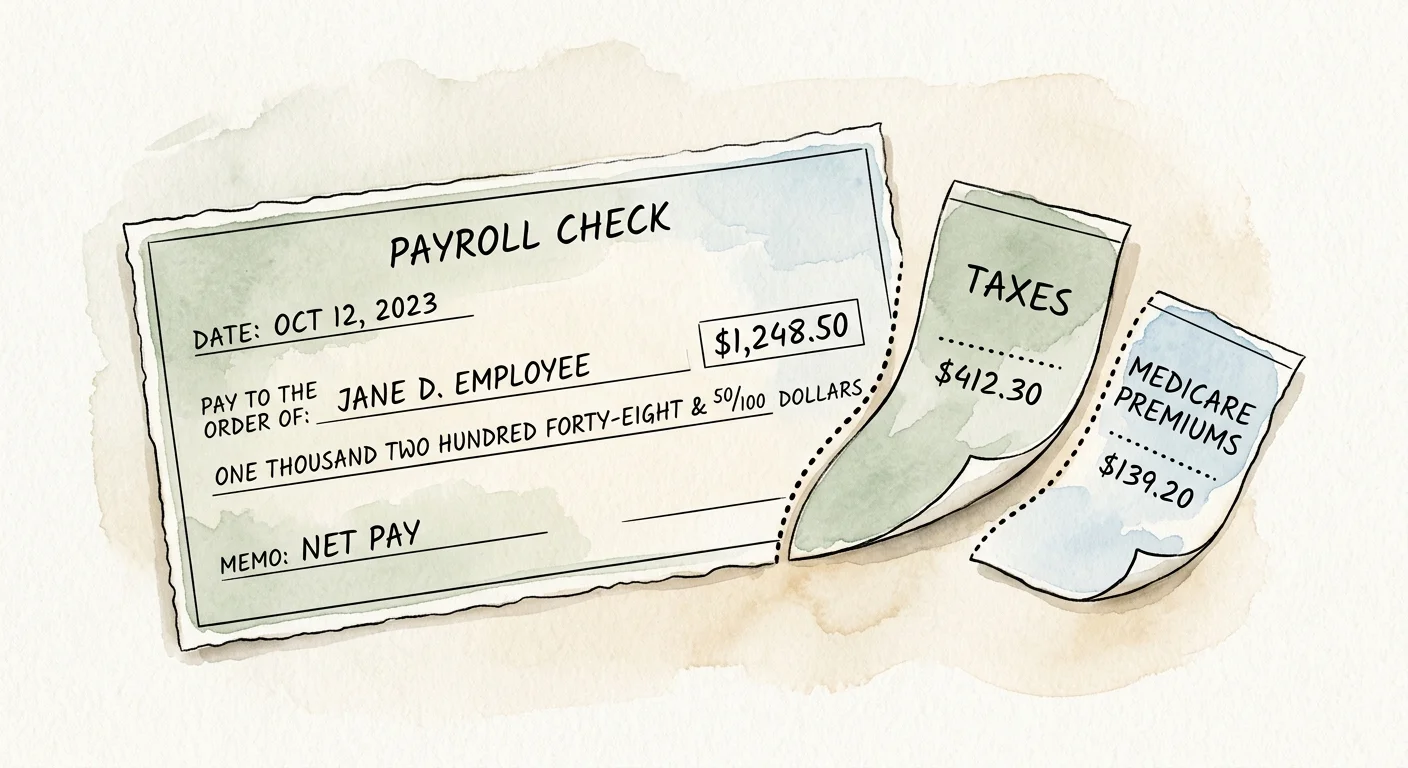

How Taxes and Medicare Premiums Shrink Your Net Payout

One of the most frustrating surprises for new retirees is discovering that the figure listed on their Social Security statement is not the amount that actually lands in their checking account. The $2,081 average check we see in August is a gross figure. Before that money reaches you, the federal government—and sometimes your state government—will likely take a slice.

The most immediate reduction comes from healthcare. If you are 65 or older and enrolled in Medicare, your Part B premiums are automatically deducted from your Social Security check. The standard Medicare Part B premium adjustments happen annually, and this deduction alone knocks a substantial chunk off your gross benefit. If you had a highly successful career and your current retirement income is robust, you might also face the Income-Related Monthly Adjustment Amount (IRMAA). This surcharge requires higher-income retirees to pay significantly more for their Medicare Part B and Part D coverage, effectively shrinking their net Social Security check even further. You can review current premium brackets directly through Medicare.gov to project your exact deductions.

Then comes the tax torpedo. Up to 85 percent of your Social Security benefits can be subject to federal income tax, depending on your “provisional income.” To find this number, the Internal Revenue Service requires you to calculate your adjusted gross income, add any nontaxable interest (like municipal bond yields), and then add half of your Social Security benefit. For a married couple filing jointly, if this combined total exceeds $32,000, up to 50 percent of their benefits may be taxable. If it exceeds $44,000, up to 85 percent becomes taxable. Because these thresholds were established decades ago and were never indexed for inflation, a massive percentage of middle-class retirees now find themselves paying federal taxes on the very benefits they were taxed to fund during their working years.

Finally, your geographic location dictates whether you face a third layer of taxation. While the vast majority of states leave Social Security benefits alone, a handful of states still levy state income taxes on this money. Staying informed about your state’s specific tax code is crucial for accurate retirement budgeting.

Spousal and Survivor Benefits: The Hidden Income Levers

You do not need to rely entirely on your own work record to generate a reliable monthly check. The system contains powerful provisions for spouses, ex-spouses, and widows that can significantly alter your baseline income.

The spousal benefit rule guarantees that you are entitled to up to 50 percent of your spouse’s Primary Insurance Amount (the benefit they are owed at their full retirement age), provided that 50 percent is higher than what you would receive on your own work record. Consider a household where one partner was the primary breadwinner earning a robust salary, while the other managed the home and worked part-time, generating a modest personal benefit of $800. If the breadwinner’s primary benefit is $2,800, the lower-earning spouse can step up to a $1,400 monthly benefit once both reach full retirement age. The SSA automatically checks both records when you apply and awards you the higher amount through a process called “deemed filing.”

However, the most critical planning aspect for couples revolves around survivor benefits. When one spouse passes away, the smaller of the two Social Security checks disappears entirely, and the surviving spouse inherits the larger check. This reality makes the claiming strategy of the higher earner an issue of household survival. When the higher earner delays claiming until age 70, they are not just maximizing their own income—they are building permanent, maximized longevity insurance for their widow or widower. Rushing to claim the higher earner’s benefit at 62 permanently locks in a reduced safety net for the surviving spouse.

“Retirement is not a fixed destination; it is a long transition. Securing a reliable baseline of guaranteed income gives you the freedom to navigate that transition on your own terms.” — Jean Chatzky, Financial Editor and Author

Working While Claiming: Understanding the Earnings Test

Many Americans ease into retirement by working part-time, consulting, or starting small businesses. If you choose to work while collecting Social Security, and you have not yet reached your full retirement age, you will collide with the Retirement Earnings Test. This rule is widely misunderstood and often prevents perfectly capable seniors from earning additional income out of a misplaced fear that the government will “steal” their benefits.

If you claim benefits early and continue to work, the SSA places a cap on how much you can earn from active wages. In 2026, if you earn above the established limit (which is adjusted annually for inflation), the SSA will withhold $1 in benefits for every $2 you earn over the threshold. In the specific calendar year you reach your full retirement age, the rules loosen; the earnings limit jumps significantly higher, and the penalty drops to $1 withheld for every $3 earned over the limit. The moment you reach the exact month of your full retirement age, the earnings test disappears entirely. You can earn a million dollars a year, and your Social Security check will not be reduced by a single penny.

The most important insight here is that the money withheld due to the earnings test is not lost forever. Once you reach your full retirement age, the SSA recalculates your monthly payment, increasing your ongoing benefit to account for the months they withheld payments. Essentially, working while claiming early forces you into a mandatory deferral program, which ultimately results in a slightly higher permanent check later in life.

What Can Go Wrong (Common Claiming Mistakes)

Retirement is an unforgiving landscape when it comes to financial errors. Once you lock in your Social Security strategy, undoing it is remarkably difficult. Avoiding these common pitfalls can save your portfolio from premature depletion.

Filing Out of Fear: The most destructive mistake pre-retirees make is claiming at 62 simply because they read headlines about the Social Security trust funds running dry. While the system faces genuine funding challenges in the 2030s, depletion of the surplus trust funds does not mean benefits drop to zero. It means ongoing tax revenues would cover roughly 80 percent of promised benefits. Locking in a permanent 30 percent reduction at age 62 to avoid a potential future reduction is mathematically counterproductive. You are guaranteeing a loss today to avoid a hypothetical loss tomorrow.

Ignoring the Tax Torpedo: Many retirees build elaborate withdrawal strategies for their 401(k) and IRA accounts without realizing how those withdrawals interact with their Social Security benefits. Pulling a large lump sum out of a traditional IRA to buy a boat or renovate a kitchen will spike your adjusted gross income for that year. This spike can instantly push your provisional income over the IRS thresholds, suddenly causing 85 percent of your Social Security check to become taxable. Failing to sequence your withdrawals correctly results in unnecessary tax leakage.

Failing to Coordinate with Your Spouse: Treating Social Security as an individual decision rather than a household asset optimization problem leaves vast sums of money unclaimed. Couples who fail to stagger their claims, or who both file at 62 without analyzing survivor scenarios, frequently damage the financial security of the partner who outlives the other. Coordination is essential.

When to Consult a Professional

While the average retiree with a straightforward employment history can often navigate the SSA website independently, certain financial realities demand the intervention of a fiduciary financial planner or a certified public accountant. Your retirement security is too vital to risk on a misinterpretation of complex federal rules.

Consider seeking professional guidance if you fall into any of the following categories:

- You Have Non-Covered Pension Income: If you worked as a teacher, police officer, or government employee in a system that did not pay into Social Security, you will likely be subject to the Windfall Elimination Provision (WEP) or the Government Pension Offset (GPO). These rules dramatically reduce your expected Social Security benefits, and professional modeling is required to understand your actual net income.

- You Are Navigating a Complex Divorce: If you were married for at least 10 years and are currently unmarried, you may be entitled to claim benefits on your ex-spouse’s earnings record. A professional can help you coordinate this without alerting your ex-spouse, as their permission is not required.

- You Have a High Net Worth: For affluent retirees, managing required minimum distributions (RMDs), Roth conversions, and capital gains requires precise tax bracketing to minimize the taxation of your Social Security benefits and avoid triggering massive IRMAA surcharges on your Medicare premiums.

If you need reliable guidance on finding trusted financial professionals or understanding your consumer rights regarding retirement products, the Consumer Financial Protection Bureau provides excellent, unbiased resources to help you protect your assets.

Frequently Asked Questions

Will the average Social Security check increase next year?

Yes, Social Security benefits typically increase annually due to the Cost-of-Living Adjustment (COLA). The exact percentage is announced every October based on third-quarter inflation data and takes effect the following January. If inflation remains present in the economy, your baseline benefit will rise accordingly to help protect your purchasing power.

Can I live comfortably on just the average Social Security check?

Living comfortably on $2,081 a month is exceptionally difficult in most parts of the United States unless you carry zero debt, own your home outright, and have remarkably low healthcare costs. Social Security is intended to replace only a portion of your working income. A comfortable retirement almost always requires supplementary income from personal savings, investments, or part-time work.

How do I find out what my specific benefit will be?

The most accurate way to project your future income is to create a secure account on the official SSA website. By logging in, you can view your real-time earnings record, verify that your past wages were recorded correctly, and see exact projections for your benefits at age 62, full retirement age, and age 70.

What happens if I claim at 62 but change my mind?

The Social Security Administration offers a one-time “do-over” provision. If you claim your benefits early and realize it was a mistake, you have exactly 12 months from your initial filing date to withdraw your application. However, you must repay every cent you and your family received during that period. Once you repay the funds, your record is wiped clean, allowing you to claim a higher benefit at a later age.

Do my Medicare Part B premiums go up if my Social Security check increases?

Generally, no. A provision known as the “hold harmless” rule ensures that for the vast majority of retirees, your Medicare Part B premium increase cannot exceed the dollar amount of your Social Security COLA increase. This prevents a scenario where an inflation adjustment actually causes your net monthly check to decrease. However, high-income earners subject to IRMAA are not protected by the hold harmless rule.

Your transition into retirement marks the shift from accumulating wealth to intelligently distributing it. Knowing that the average Social Security check in August 2026 sits around $2,081 gives you a solid benchmark, but your ultimate goal should be optimizing your specific household filing strategy. Pull your latest earnings statement, map out your anticipated living expenses, and strongly consider the long-term mathematical advantage of delaying your claim if your health and savings allow it.

This is educational content based on general retirement and financial principles. Individual results vary based on your situation. Always verify current benefit rules, tax laws, and eligibility requirements with official sources like SSA, Medicare.gov, or the IRS.

Last updated: July 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply