Many retirees excitedly open their first Social Security statement expecting a specific deposit, only to discover their actual monthly income is significantly lower than anticipated. This surprising reduction often stems from a few specific federal provisions designed to adjust retirement checks based on your work history, alternate pensions, and current earnings. Understanding the mechanics of your benefit calculation before you claim is crucial for accurate financial planning and avoiding a devastating shortfall in your budget. By navigating the complexities of the Windfall Elimination Provision, the Government Pension Offset, and the annual earnings test, you can accurately project your true federal benefits. This guide breaks down exactly how these rules work so you can secure the monthly check you actually deserve.

Understanding the Foundation of Your Benefit Calculation

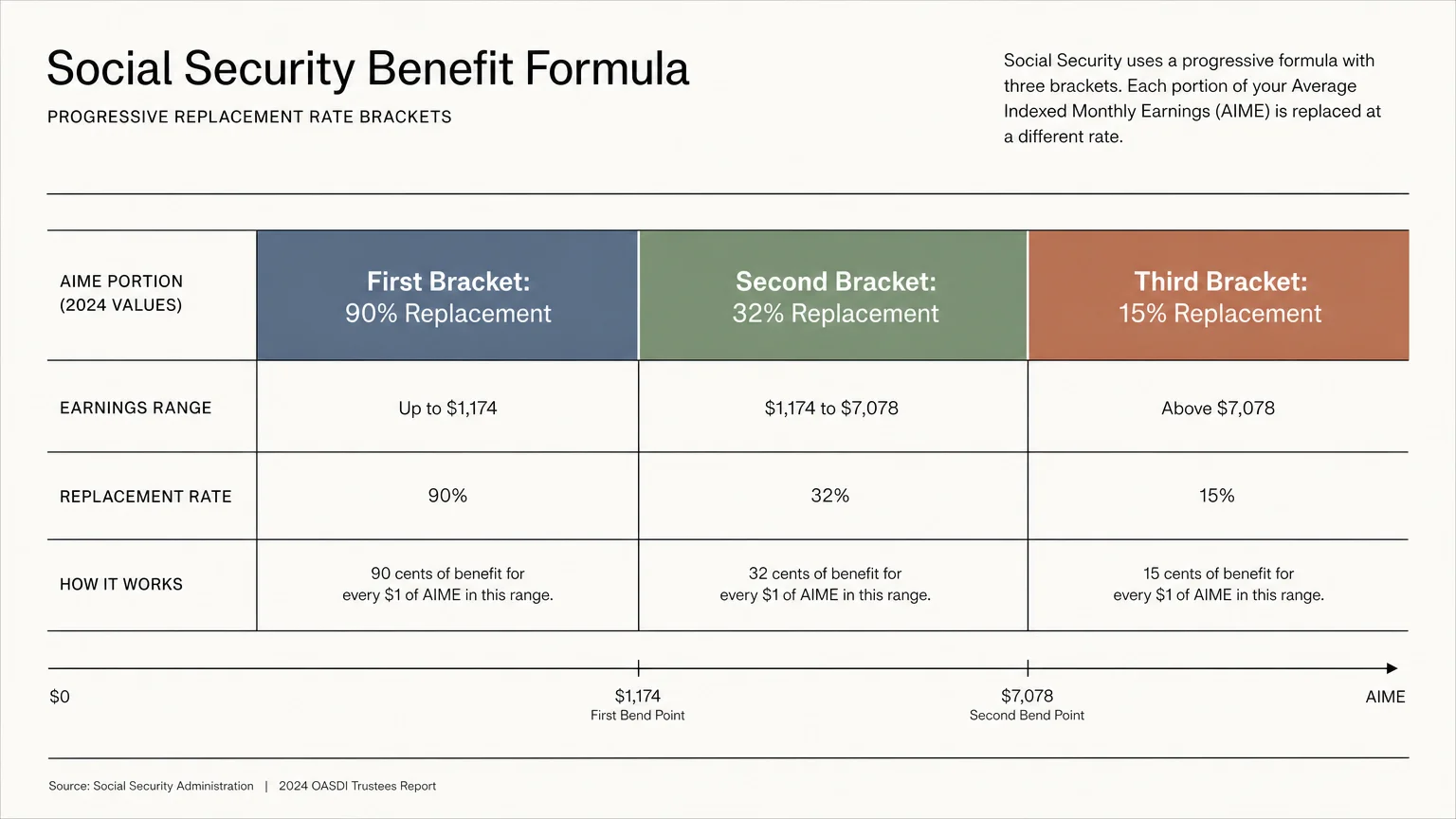

Before diving into the rules that reduce your payments, you must understand how the government determines your baseline amount. The Social Security Administration evaluates your entire work history to find your highest 35 years of earnings. They adjust these historical wages for inflation—a process known as indexing—to ensure that the $15,000 you earned decades ago holds the appropriate modern purchasing power. Once they index your earnings, they average them out to find your Average Indexed Monthly Earnings.

The system applies a progressive formula to this monthly average to determine your Primary Insurance Amount. This progressive design specifically helps lower-income workers replace a larger percentage of their pre-retirement income compared to higher-income workers. The formula uses specific thresholds, known as bend points, to divide your average earnings into three distinct brackets. The government replaces a massive 90 percent of your earnings in the first bracket. The replacement rate drops to 32 percent in the second bracket and plummets to just 15 percent in the final bracket. The progressive nature of this formula operates under the assumption that all your lifetime earnings came from jobs that paid into the federal system. When you step outside that standard framework, specialized rules kick in to alter your final payment.

The Windfall Elimination Provision

The Windfall Elimination Provision exists to level the playing field for workers who split their careers between jobs that paid Social Security taxes and jobs that did not. Congress implemented this rule in the 1980s to close a loophole in the progressive formula. Without this provision, a worker who spent most of their career in a non-covered government job—earning a robust public pension—would appear to the system as a low-wage worker because they only had a few years of taxable earnings from side jobs or earlier employment. The system would unfairly award them the 90 percent replacement rate in the first bracket of their benefit calculation, creating an unintended windfall.

If you earned a pension from an employer who did not withhold federal payroll taxes—such as certain state or local government agencies, public school systems, or foreign employers—and you also qualify for federal retirement checks based on other work, the Windfall Elimination Provision drastically modifies your formula. Instead of receiving 90 percent of the earnings in the first bracket of your calculation, the system reduces that multiplier to as low as 40 percent. This adjustment can slice hundreds of dollars off your expected payments.

You cannot hide your non-covered pension from the federal government. When you apply for your retirement checks, the application explicitly asks if you receive or expect to receive a pension based on earnings not covered by standard payroll taxes. Attempting to obscure this information results in overpayments that the government will inevitably claw back—often by halting your checks entirely until they recover the debt. If you fall into this category, you must use the specialized calculators provided by the Social Security Administration rather than relying on the standard statements mailed to your home, as the standard statements do not account for this specific reduction.

How Substantial Earnings Soften the Impact

The government recognizes that some people truly work full careers in both systems. If you have a significant number of years where you paid substantial payroll taxes, the impact of the Windfall Elimination Provision gradually disappears. The rules define a specific dollar amount for each historical year that constitutes “substantial earnings.” If you meet that threshold for a given year, you earn one year of substantial coverage.

The protection phases in once you hit 21 years of substantial earnings. For every year of substantial earnings beyond 20, the first bracket multiplier increases by five percentage points. If you have 21 years, the multiplier rises from 40 percent to 45 percent. If you hit 25 years, the multiplier climbs to 65 percent. Once you achieve 30 years of substantial earnings, the Windfall Elimination Provision vanishes entirely, and you receive the standard 90 percent multiplier in your first bracket.

You must scrutinize your earnings record to identify how close you are to these thresholds. Sometimes, working just one more year at a job that pays into the federal system can cross a threshold, permanently boosting your monthly income for the rest of your life. Keep in mind that the substantial earnings threshold differs from the standard credits you earn to simply qualify for benefits. You need much higher annual income to clock a year of substantial earnings than you do to earn your standard four quarterly credits.

The Government Pension Offset

While the previous rule targets your own work record, the Government Pension Offset targets spousal and survivor benefits. If you receive a retirement or disability pension from a federal, state, or local government based on your own work for which you did not pay standard payroll taxes, this offset reduces any spousal or survivor benefits you expect to receive on your spouse’s record.

The mathematics behind the Government Pension Offset prove particularly harsh. The government reduces your spousal or survivor payment by two-thirds of the amount of your non-covered government pension. If two-thirds of your government pension exceeds your potential spousal benefit, your spousal benefit drops to zero.

- Scenario A: You receive a $900 monthly pension from your years teaching in a non-covered school district. Two-thirds of $900 equals $600. If you apply for a $1,000 spousal benefit based on your husband’s record, the government deducts the $600 offset. You receive $400 from the federal system, bringing your total monthly income to $1,300.

- Scenario B: You receive a $3,000 monthly public pension. Two-thirds of that pension equals $2,000. If your expected survivor benefit amounts to $1,800, the offset completely wipes out the federal payment. You receive your $3,000 pension, but zero dollars from the survivor claim.

This rule exists because spousal benefits were originally designed for dependent spouses who had little or no income of their own. Congress decided that a spouse with a robust government pension is not financially dependent in the way the original law envisioned. Widows and widowers often discover this rule during the worst time of their lives, expecting to transition to their deceased spouse’s higher benefit amount only to find the door firmly shut. Incorporating this reality into your financial plan long before a spouse passes away ensures the surviving partner maintains adequate monthly income.

The Retirement Earnings Test

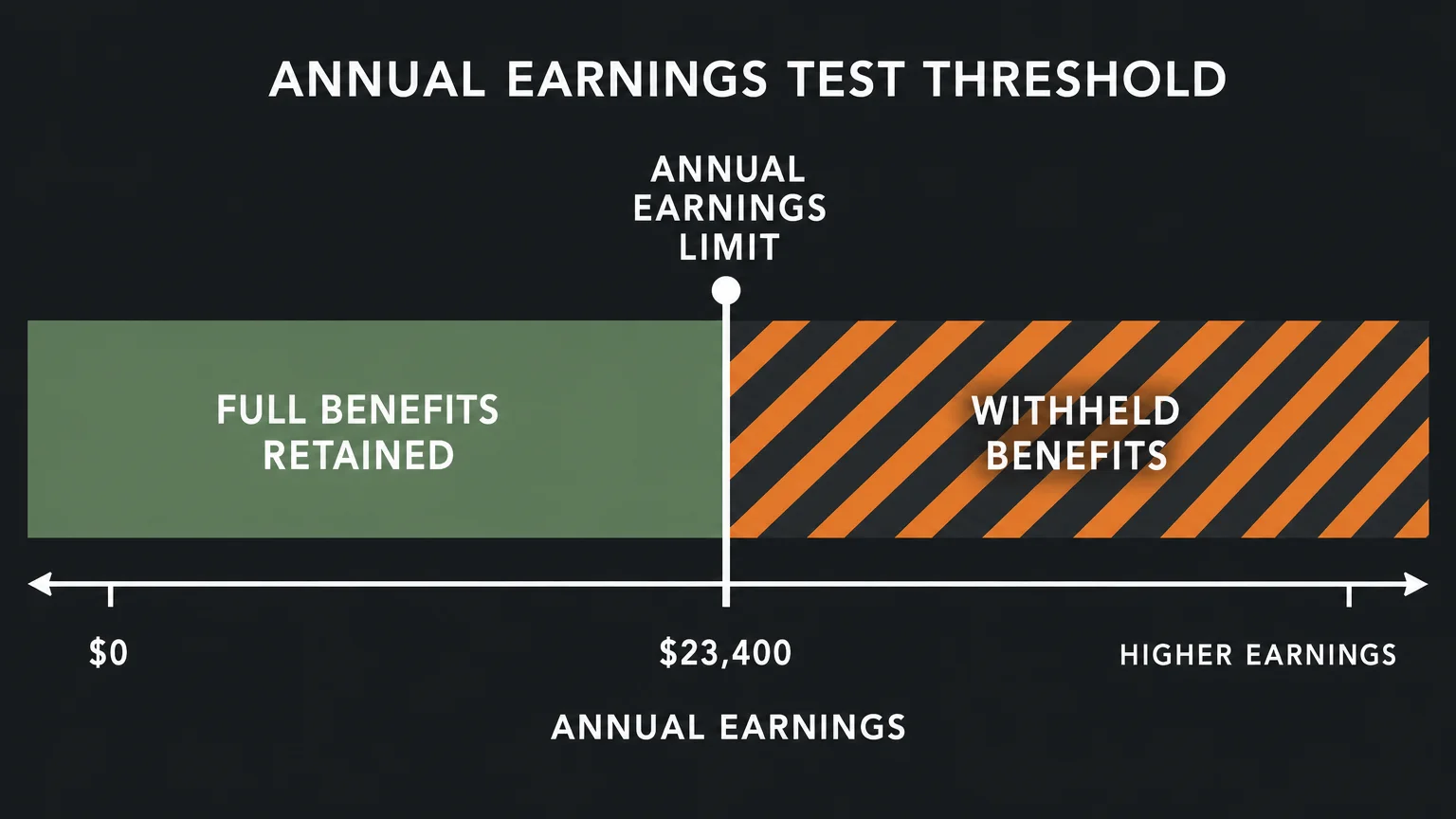

Many individuals prefer to transition into retirement slowly, claiming their benefits early while continuing to work part-time. If you claim your payments before reaching your Full Retirement Age, the annual earnings test becomes the most critical rule in your financial life. The federal government enforces strict income limits for early claimers; if you exceed these limits, they withhold a portion of your monthly checks.

The rules establish a specific earnings threshold that adjusts annually for inflation. If you claim early and your earned income exceeds this lower threshold, the administration withholds $1 in benefits for every $2 you earn above the limit. In the specific calendar year you reach your Full Retirement Age, the rules become more lenient. A higher earnings limit applies for the months leading up to your birthday, and the withholding drops to $1 for every $3 you earn above that higher limit. Once you reach your birth month, the earnings test disappears forever. You can earn a million dollars a year, and the government will not withhold a single dime of your retirement checks.

A massive misconception surrounds the earnings test. Most retirees believe the withheld money operates as a punitive tax, lost forever to the government coffers. In reality, the withholding functions more like a forced deferral. When you reach Full Retirement Age, the administration recalculates your baseline benefit to account for the months you did not receive a check. If you claimed at 62 but had 12 months of checks withheld due to high earnings over the next few years, the system treats you as if you had claimed at 63. They adjust your monthly payment upward permanently, ensuring you recoup the withheld funds over your average life expectancy.

“You have to take the time to learn the rules of retirement. If you do not understand how your benefits are calculated, you are leaving your financial future to chance.” — Suze Orman, Personal Finance Expert

Comparing the Big Three Benefit Adjustments

Understanding which rule applies to your specific situation requires clear differentiation. Review the core differences between these major provisions to accurately assess your exposure.

| Rule Name | Who It Affects | Impact on Benefits | Can You Recover The Money? |

|---|---|---|---|

| Windfall Elimination Provision | Workers with non-covered pensions claiming on their own record. | Reduces the first-bracket multiplier from 90% to as low as 40%. | No, the reduction is permanent unless you accumulate 30 years of substantial covered earnings. |

| Government Pension Offset | Workers with non-covered pensions claiming spousal or survivor benefits. | Reduces the benefit by two-thirds of the government pension amount. | No, this offset applies permanently to spousal and survivor claims. |

| Retirement Earnings Test | Anyone claiming early who continues to work and earn above the annual limit. | Withholds $1 for every $2 (or $3) earned above established thresholds. | Yes, your monthly check increases at Full Retirement Age to account for withheld months. |

The Impact of Provisional Income on Your Net Pay

Even if you avoid the offset rules and wait until Full Retirement Age to sidestep the earnings test, the Internal Revenue Service has its own mechanism for reducing your take-home pay: taxation. Before 1984, federal retirement benefits were entirely tax-free. Today, depending on your total financial picture, you might owe federal income taxes on up to 85 percent of your payments.

The IRS uses a specific formula called Provisional Income to determine your tax liability. To calculate your Provisional Income, you add your Adjusted Gross Income, any nontaxable interest you receive from municipal bonds, and exactly one-half of your annual federal retirement benefits. If this combined total exceeds specific thresholds based on your filing status, taxation begins.

For single filers, Provisional Income between $25,000 and $34,000 means up to 50 percent of your benefits become taxable. If the total exceeds $34,000, up to 85 percent faces taxation. For married couples filing jointly, the 50 percent threshold sits between $32,000 and $44,000, with the 85 percent tier starting above $44,000. Unlike standard tax brackets, Congress never indexed these thresholds for inflation. As normal wages and retirement savings distributions naturally rise over the decades, an increasingly large percentage of retirees find themselves crossing these static lines.

Careful withdrawal strategies can help mitigate this silent reduction. Drawing from Roth accounts does not increase your Adjusted Gross Income, allowing you to generate necessary spending cash without pushing your Provisional Income into the taxable zone. Balancing your withdrawals between pre-tax accounts, taxable brokerage accounts, and tax-free vehicles forms the bedrock of modern retirement income planning. The AARP provides excellent resources on managing these layered tax strategies as you enter your senior years.

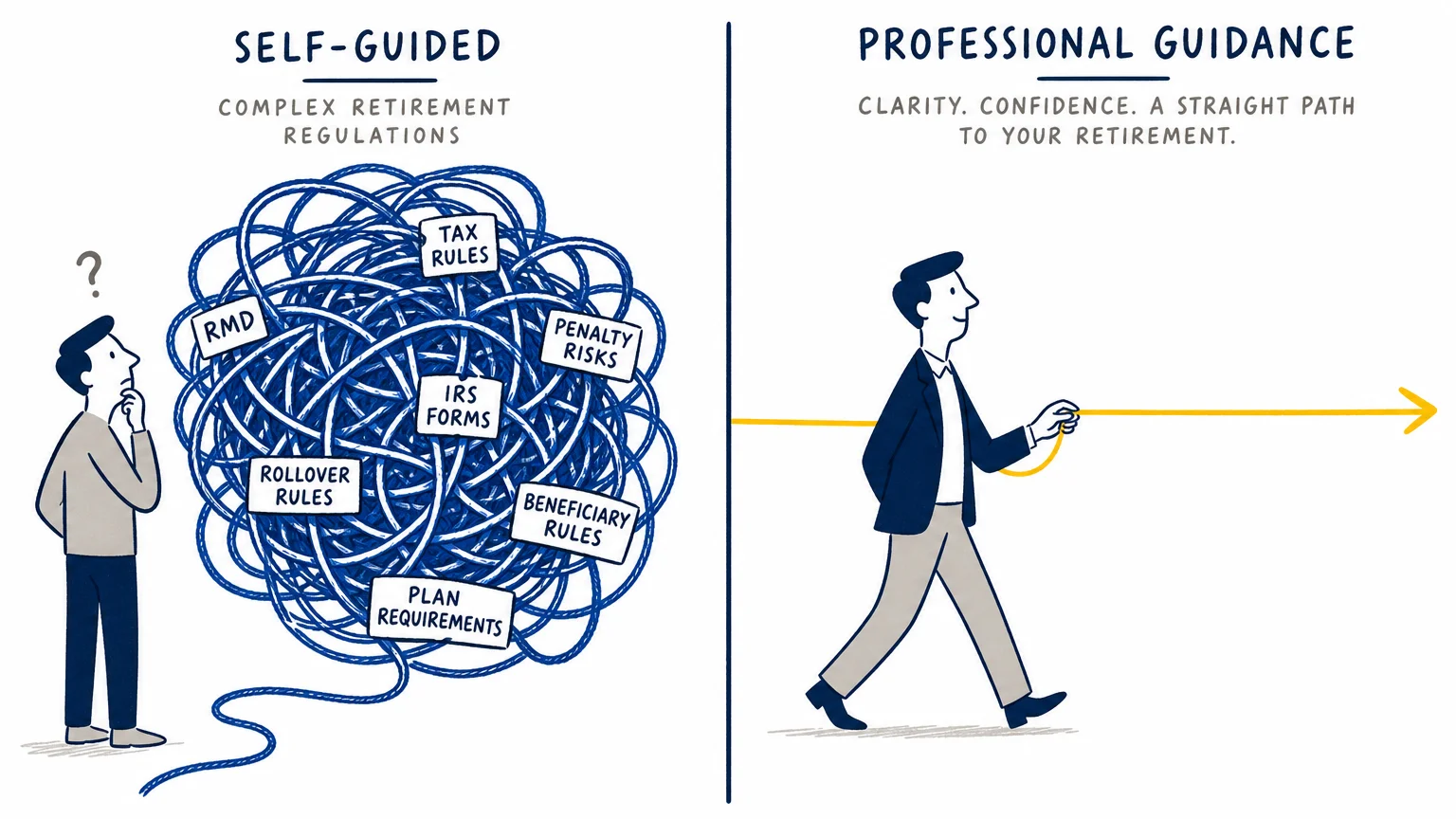

Professional vs. Self-Guided

Navigating benefit rules requires a realistic assessment of your financial complexity. You must decide whether to handle the calculations yourself or hire a fee-only fiduciary advisor to chart your course.

The Self-Guided Approach Works Best When:

- Your entire career took place in the private sector where your employers consistently withheld standard payroll taxes.

- You do not possess a government pension of any kind.

- You plan to stop working entirely before you file your initial claim, rendering the earnings test irrelevant.

- Your primary income sources consist of standard 401(k) withdrawals and federal benefits, making tax projections relatively straightforward.

The Professional Approach Works Best When:

- You spent years working as a teacher, police officer, or municipal worker in a state that utilizes alternate pension systems. A professional uses advanced software to calculate the exact dollar impact of the Windfall Elimination Provision and can advise you on whether acquiring a few more years of substantial earnings makes mathematical sense.

- You own a business and intend to claim early. Business owners often struggle to define what counts as “earned income” under the earnings test rules. An advisor coordinates with your CPA to legally manage your compensation, preventing unexpected benefit withholding.

- You face a complex spousal claiming scenario. If you and your spouse both hold mixed-record careers involving public pensions and private sector work, calculating the interplay between your primary benefits and the Government Pension Offset requires meticulous projections to maximize lifetime household income.

Common Mistakes to Avoid

Misunderstanding the mechanisms that adjust your monthly payments leads to cascading errors throughout your financial plan. Avoid these frequent missteps that trap unsuspecting retirees.

Relying on the Standard Benefit Statement: Millions of public sector workers log into the online portal, see a projected benefit of $2,000 a month, and build their budgets around that number. The standard portal assumes all your earnings history falls under standard rules. If you have a non-covered pension, you must manually use the specialized calculators designed for offset situations. Failing to do so results in a massive income shock on day one of retirement.

Quitting Just Short of the 30-Year Mark: The exemption from the Windfall Elimination Provision requires 30 years of substantial earnings. Many individuals leave the private sector at 28 or 29 years to take an early retirement or pivot to a different lifestyle. Walking away just short of the 30-year threshold leaves you exposed to permanent reductions. Review your earnings record closely; grinding out one or two more years in a covered job can secure thousands of dollars in extra lifetime income.

Misinterpreting the Earnings Test Withholding: Retirees frequently panic when the government halts their checks because they earned too much money while working part-time. They assume the money vanished into a bureaucratic black hole. This panic often drives them to quit lucrative, fulfilling part-time work unnecessarily. Remember that the withheld funds trigger a positive recalculation at Full Retirement Age. Let the math dictate your work choices, not the emotional reaction to a temporary withholding.

Ignoring State Taxation Rules: While federal tax rules apply universally, state rules vary wildly. Some states fully exempt all federal retirement benefits from state income tax; others tax them similarly to the federal government; a few apply completely unique formulas based on age and total income. Relocating across state lines without analyzing the specific tax treatment of your monthly check can neutralize the geographic cost-of-living benefits you sought.

Frequently Asked Questions

Does the Windfall Elimination Provision ever go away?

The provision remains permanently attached to your record unless you eventually accumulate 30 years of substantial earnings from jobs that withhold federal payroll taxes. For individuals who already retired without hitting that 30-year mark, the reduction continues for the remainder of their lives.

How does the earnings test affect me after my Full Retirement Age?

It does not affect you at all. Once you reach your exact birth month for Full Retirement Age, the annual earnings test vanishes. You can earn an unlimited amount of income from a job or business, and the government will never withhold any portion of your monthly check.

Are military pensions subject to these offset rules?

No. Military pensions and standard federal civil service pensions created under the newer FERS system include standard payroll tax withholding. Because you paid the standard taxes while earning the pension, military retirees do not face reductions from the Windfall Elimination Provision or the Government Pension Offset.

Can I voluntarily ask the government to withhold taxes from my check?

Yes. If you anticipate owing taxes due to your Provisional Income levels, you can file a Form W-4V with the federal government. This form allows you to select a flat percentage to withhold automatically, preventing a massive, unexpected tax bill in April.

Accurate retirement planning requires stripping away assumptions and looking purely at the mechanics of the law. Your monthly check serves as the bedrock of your financial independence. By proactively analyzing how your public pensions, current work schedule, and total household income interact with federal rules, you protect yourself from sudden budget shortfalls.

Take the time today to pull your detailed earnings record and run the specific calculators that match your career history. The information in this guide is meant for educational purposes. Your specific circumstances—including income, health needs, tax situation, and goals—may require different approaches. When in doubt, consult a licensed professional.

Last updated: June 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply