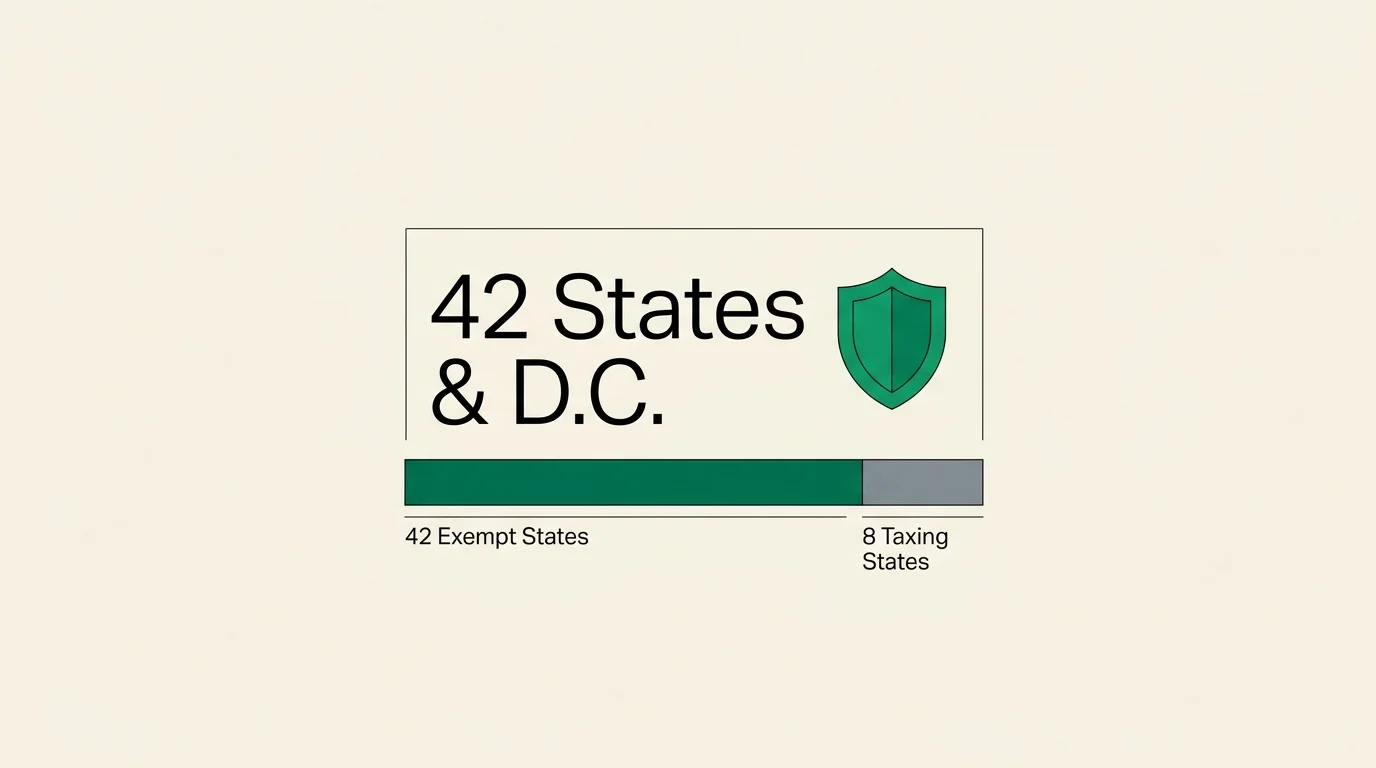

Deciding where to spend retirement involves more than just finding favorable weather and affordable housing. State taxes play a massive role in your financial security, particularly regarding your benefits. By 2027, the map of states without Social Security tax has shifted significantly in favor of retirees. Forty two states and the District of Columbia now allow you to keep every penny of your benefits at the state level. As legislative trends continue to eliminate retirement taxes, understanding local tax laws ensures you avoid leaving money on the table. Knowing exactly where your retiree finances are protected helps you build a more accurate and resilient budget for your future.

The 2027 Landscape of Retirement Taxes

State legislatures have recognized a fundamental demographic truth: retirees represent a highly mobile, financially stable population that brings immense economic value to local economies. When older adults relocate, they bring their consumer spending, charitable giving, and stable property tax payments with them. Recognizing this economic power, lawmakers across the country have aggressively slashed retirement taxes over the past five years to attract and retain seniors.

Just a few years ago, more than a dozen states levied taxes on Social Security income. However, a wave of bi-partisan legislation drastically altered the map. Missouri, Nebraska, and Kansas phased out their benefit taxes entirely by 2024. West Virginia successfully completed its phased reduction, joining the ranks of tax-free benefit states for the 2026 tax year—which you reconcile on your 2027 tax returns. Because of this legislative momentum, 42 states and Washington D.C. now completely exempt your Social Security checks from state-level income taxation.

This massive shift fundamentally changes how you should approach retirement relocation. You no longer need to restrict your home search to traditional sunbelt havens to protect your benefits. You can now choose from a vast majority of the country—from the coastal communities of Maine to the mountainous regions of Idaho—without surrendering a portion of your guaranteed monthly income to the state capital.

However, this favorable tax treatment of Social Security does not mean state revenue departments have stopped collecting taxes altogether. States must fund public schools, infrastructure, and emergency services. When a state gives up income tax revenue, it inevitably compensates through other channels. As you evaluate the 42 states that protect your benefits, you must widen your lens to view the complete tax picture, including sales taxes, property taxes, and the taxation of your other retirement accounts.

States With No Income Tax At All

The most straightforward way a state protects your Social Security benefits is by simply not having a personal income tax code. Nine states fall into this category. If you establish legal domicile in one of these locations, you will not file a state income tax return, and your benefits—along with your pension, IRA withdrawals, and capital gains—are entirely shielded from state taxation.

The nine states with no broad personal income tax in 2027 are:

- Alaska: Not only does Alaska lack an income tax, but it also pays residents an annual dividend from its Permanent Fund. However, the extreme climate, geographic isolation, and high cost of everyday goods often offset the tax savings for many retirees.

- Florida: The ultimate traditional retirement destination offers no income tax and robust asset protection laws. The financial tradeoff here usually appears in the form of elevated property insurance premiums and higher property taxes.

- Nevada: A popular choice for West Coast retirees fleeing California’s high tax brackets. Nevada funds its government largely through tourism and sales taxes, meaning your daily purchases will carry a higher premium.

- New Hampshire: Known for its “Live Free or Die” motto, New Hampshire completely phased out its narrow tax on interest and dividends by 2025. It now operates as a true no-income-tax state, though residents face some of the highest property tax rates in the nation.

- South Dakota: Offering an incredibly low overall tax burden, South Dakota has become a haven for RV retirees and those seeking a quiet, affordable lifestyle—provided you can tolerate harsh winters.

- Tennessee: This Southern state combines zero income tax with mild weather and a low cost of living. To compensate, Tennessee relies on a combined state and local sales tax rate that often nears 10 percent.

- Texas: You will keep every dime of your Social Security and 401(k) withdrawals here. But prepare your budget for property taxes; Texas counties heavily rely on real estate assessments to fund local municipalities and schools.

- Washington: While Washington does not levy a traditional income tax on Social Security or retirement account withdrawals, high-net-worth retirees should note its capital gains tax on profits exceeding specific high thresholds, which primarily affects wealthy investors selling substantial assets.

- Wyoming: With a tiny population and vast natural beauty, Wyoming offers an incredibly tax-friendly environment, bolstered by revenue from the state’s energy sector.

Choosing one of these nine states guarantees that your state tax liability on your benefits remains zero. However, you must carefully calculate whether the corresponding property and sales taxes will consume the money you saved on income taxes. A comprehensive retirement plan accounts for total cash flow, not just a single missing tax bracket.

States That Collect Income Tax But Exempt Social Security

The largest group of states—33 in total, plus the District of Columbia—operate with a more nuanced tax code. These jurisdictions levy a traditional state income tax on wages, business income, and often standard retirement accounts, but they specifically carve out an absolute exemption for Social Security benefits.

This category is incredibly diverse. It includes states notorious for high taxes alongside those praised for affordability. Understanding how these states treat your broader financial picture is crucial because your Social Security is rarely your only source of income. We can break these 33 states down into three distinct operational categories based on how they treat the rest of your money.

The “Total Retirement Exemption” States

A select few states in this group go above and beyond exempting just your Social Security. Illinois, Mississippi, and Pennsylvania stand out as exceptionally generous to retirees. In these states, almost all forms of retirement income—including 401(k) distributions, traditional IRA withdrawals, and both public and private pensions—are completely exempt from state income tax. Furthermore, Iowa joined this elite tier recently, making retirement income entirely tax-free for residents aged 55 and older. If you build a diversified portfolio heavily reliant on tax-deferred accounts, these specific states offer an environment functionally identical to Florida or Texas, but often with lower property insurance risks.

The “Generous Deduction” States

Many states exempt your benefits but set limits on how much of your other retirement income is protected. For instance, Georgia completely exempts Social Security and offers an additional retirement income exclusion of up to $65,000 per person for residents aged 65 and older. This means a married couple could potentially shield $130,000 of IRA withdrawals and pensions, plus all of their Social Security, from state taxes. South Carolina and Michigan offer similarly structured, age-based deductions that effectively wipe out state income taxes for the middle class, while still collecting revenue from the wealthiest retirees.

The “Social Security Only” Exemption States

States like California, New York, and Oregon represent the opposite end of the spectrum. They absolutely protect your Social Security benefits—you will pay zero state tax on those checks. However, they aggressively tax your 401(k) distributions, IRA withdrawals, and capital gains at standard, often high, state income tax rates. If your retirement strategy relies on large conversions to Roth IRAs or heavy withdrawals from traditional brokerage accounts, these states will take a significant slice of your wealth, even though your Social Security remains untouched.

The complete list of states that fall into this 33-state category includes Alabama, Arizona, Arkansas, California, Delaware, Georgia, Hawaii, Idaho, Illinois, Indiana, Iowa, Kansas, Kentucky, Louisiana, Maine, Maryland, Massachusetts, Michigan, Mississippi, Missouri, Nebraska, New Jersey, New York, North Carolina, North Dakota, Ohio, Oklahoma, Oregon, Pennsylvania, South Carolina, Virginia, West Virginia, and Wisconsin.

The Eight States That Still Tax Benefits

If 42 states exempt your benefits, simple subtraction leaves exactly eight states that still enforce state tax laws on Social Security in 2027. If you plan to retire in the Rocky Mountains, the Northeast, or the Upper Midwest, you must pay close attention to this list.

However, the phrase “taxes Social Security” is somewhat misleading. None of these eight states universally tax every retiree. They all offer substantial deductions, exemptions, and age-based credits that protect low- and middle-income seniors. In reality, these states specifically target high-income retirees who have substantial wealth outside of the Social Security system.

| State | 2027 Social Security Tax Rules & Exemptions |

|---|---|

| Colorado | Fully exempt for residents aged 65 and older. If you retire early between ages 55 and 64, you can exempt up to $20,000 of total retirement income, which includes your Social Security benefits. |

| Connecticut | Your benefits are completely tax-free if your Adjusted Gross Income (AGI) is below $75,000 as a single filer, or below $100,000 as a married couple filing jointly. Above those limits, partial taxation applies. |

| Minnesota | Utilizes a sliding scale. Most middle-income retirees pay no tax, but the exemption phases out as your income rises. Singles with income roughly above $85,000 and couples above $110,000 will see portions of their benefits taxed. |

| Montana | Aligns closely with federal tax rules but applies a state-level exemption that phases out for higher earners. Lower-income retirees are entirely protected. |

| New Mexico | Exempts benefits entirely for singles with an AGI under $100,000 and married couples with an AGI under $150,000. Only the most affluent retirees face state taxation here. |

| Rhode Island | Provides a full exemption for residents who have reached full retirement age, provided their AGI falls below roughly $101,000 for singles or $126,250 for joint filers (figures adjust annually for inflation). |

| Utah | Does not offer a direct deduction; instead, it provides a non-refundable tax credit for Social Security benefits. This credit phases out by 2.5 cents for every dollar of AGI over specific thresholds ($45,000 single / $75,000 married). |

| Vermont | Completely exempts benefits if your AGI is under $50,000 (single) or $65,000 (married). The exemption phases out gradually, disappearing completely once joint income exceeds $75,000. |

As you can see from the data, living in one of these eight states does not automatically trigger a tax bill. If you maintain a moderate lifestyle and pull carefully from a balanced mix of Roth and Traditional accounts, you can easily slide under the income thresholds and pay nothing to the state.

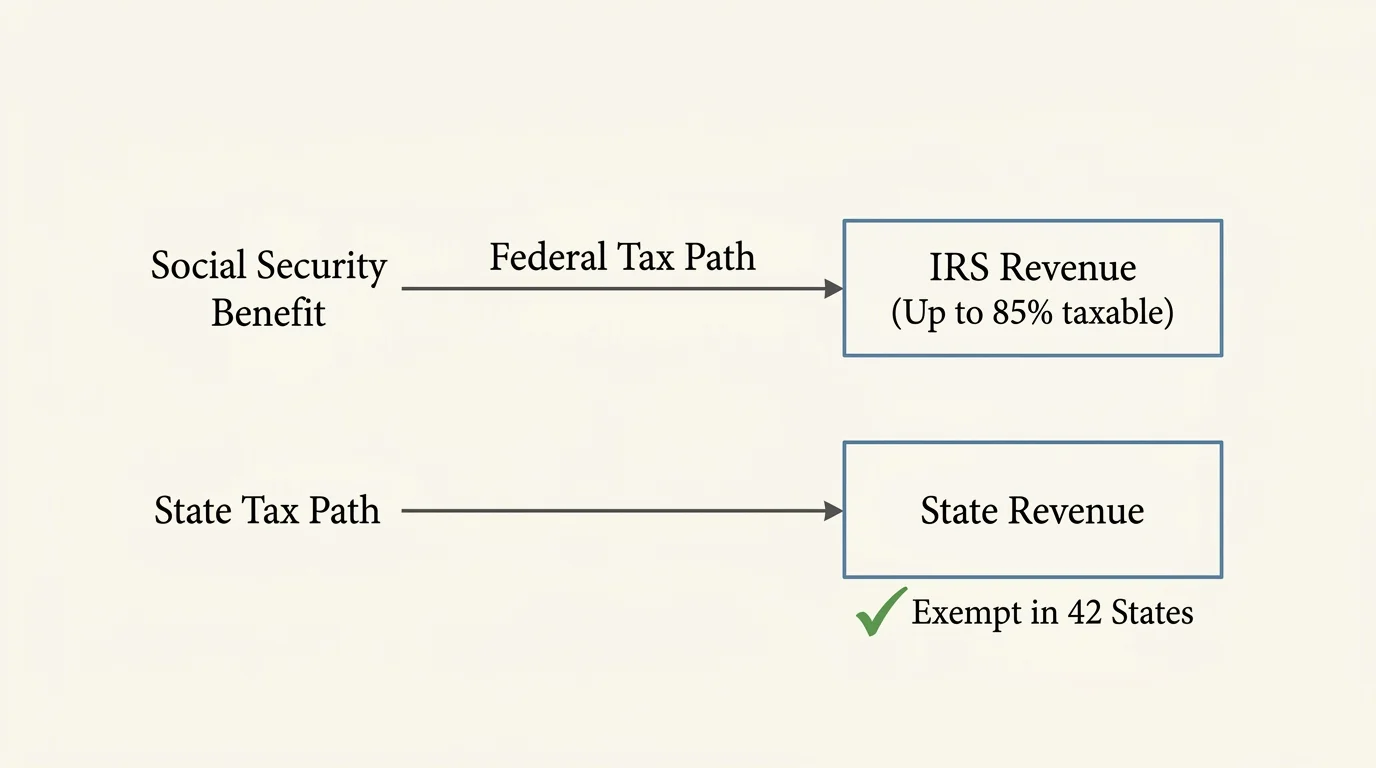

Federal vs. State Taxes: The Double Taxation Confusion

A dangerous misconception plagues many future retirees: they assume that moving to a state without Social Security tax protects them from all taxes on their benefits. This is entirely false. State laws have absolutely no bearing on the Internal Revenue Service. Regardless of where you park your RV or buy your retirement condo, you are still subject to federal tax laws.

The federal government taxes Social Security based on a formula called “Provisional Income.” You must calculate this specific metric to determine how much of your benefit falls into your taxable federal bucket. Provisional Income equals your Adjusted Gross Income (excluding Social Security) plus any non-taxable interest (like municipal bonds) plus exactly 50 percent of your total Social Security benefits.

Once you calculate that number, the IRS applies the following thresholds:

- For Single Filers: If your Provisional Income is between $25,000 and $34,000, up to 50% of your benefits may be taxable. If it exceeds $34,000, up to 85% of your benefits become subject to federal income tax.

- For Married Filing Jointly: If your Provisional Income is between $32,000 and $44,000, up to 50% of your benefits may be taxable. If it exceeds $44,000, up to 85% of your benefits become subject to federal income tax.

Notice that these federal thresholds are incredibly low and have never been adjusted for inflation since they were introduced decades ago. Consequently, a vast majority of middle-class retirees find that 85% of their benefits are federally taxable. You can find the official worksheets and IRS guidelines on provisional income directly through the Internal Revenue Service website.

Here is how the double-taxation dynamic works in practice: Imagine a married couple receiving $40,000 in Social Security and pulling $60,000 from traditional IRAs. Their Provisional Income easily exceeds the $44,000 federal limit. Therefore, they will pay federal income taxes on 85% of their benefits. If they live in Texas, their tax journey ends there. But if they live in Utah—one of the eight taxing states—they will calculate their federal tax bill, and then they will also calculate a state tax bill based on Utah’s specific formulas. Understanding this two-tiered system prevents massive budget shocks during your first year of retirement.

Strategic Moves for Retiree Finances

You possess considerable control over how much tax you ultimately pay in retirement. Tax planning is not a passive activity; it requires proactive management of your income streams. Your goal is to maximize what you keep, minimizing the drag that taxes place on your investment portfolio.

“Retirement is not an endpoint. It is a transition. You are moving from accumulating assets to distributing them, and the tax implications of that shift are profound.” — Jean Chatzky, Financial Editor and Author

One highly effective strategy involves controlling the timing of your Social Security claim. Because the federal government taxes up to 85% of your benefits based on your other income, many retirees choose to delay their claim until age 70. During your 60s, you can live off your traditional IRAs and 401(k)s. By spending down these pre-tax accounts early, you reduce the Required Minimum Distributions (RMDs) you will face later in life. When you finally claim a maximized Social Security benefit at age 70, your IRA balances are lower, meaning your taxable withdrawals are smaller, which helps keep your Provisional Income low enough to protect your benefits from the IRS. You can run customized claiming scenarios using the calculators at the Social Security Administration.

Asset location provides another powerful lever. If you live in a state that exempts Social Security but taxes IRA withdrawals heavily, you must think carefully about which accounts hold your highest-yielding assets. Keep your tax-inefficient assets (like high-yield bonds and REITs) inside your tax-advantaged accounts. Keep your highly tax-efficient assets (like municipal bonds from your home state or low-turnover index funds) in your standard taxable brokerage accounts. When you need cash, pulling from the taxable brokerage generates long-term capital gains, which states often tax at lower, preferential rates compared to standard income.

Common Mistakes to Avoid

Navigating the complex web of retirement taxes requires vigilance. Many retirees make costly unforced errors simply by overlooking the broader financial ecosystem. Protect your nest egg by avoiding these specific blunders:

- Moving Purely for the Income Tax Exemption: Never let the “tax tail” wag the “lifestyle dog.” Moving away from your grandchildren and support network to a state like Wyoming simply to save 4% on your income taxes often leads to an isolating, unhappy retirement. Furthermore, the cost of flying back home to visit family multiple times a year will quickly erase your tax savings.

- Ignoring Estate and Inheritance Taxes: Some states generously exempt your Social Security while you are alive, but aggressively tax your assets when you pass away. States like Massachusetts and Oregon enforce estate taxes on assets exceeding just $1 million to $2 million. If you own a modest home and a decent retirement account, your heirs could face a massive “death tax” bill.

- Failing to Account for IRMAA: When you execute large Roth conversions or take massive IRA withdrawals to fund a lifestyle purchase, you spike your Adjusted Gross Income. This does more than just increase your income tax—it can trigger the Income-Related Monthly Adjustment Amount (IRMAA). IRMAA is a federal surcharge that drastically increases your Medicare Part B and Part D premiums. You can review current premium brackets at Medicare.gov.

- Misunderstanding the Domicile Rules: You cannot simply buy a cheap condo in Florida, register your car there, and claim tax-free status while spending nine months a year in your primary home in New York. High-tax states aggressively audit retirees claiming to have moved. You must generally spend more than 183 days a year in your new state and sever meaningful financial ties with your old state to successfully shift your tax domicile.

Professional vs. Self-Guided Planning

Determining whether you need to hire an expert to manage your retirement taxes depends entirely on the complexity of your income streams and your future lifestyle plans. No single approach works for everyone. Consider these common scenarios to gauge your need for professional intervention.

Scenario 1: The Single-State, Fixed-Income Retiree (Self-Guided)

If you plan to age in place in a state that completely exempts Social Security, and your income consists purely of your monthly benefits and modest, predictable withdrawals from a traditional IRA, you likely do not need a CPA on retainer. High-quality commercial tax software is perfectly capable of handling the standard deduction and ensuring your benefits remain untaxed.

Scenario 2: The Interstate Snowbird (Professional)

If you split your year between two states—for example, spending winters in tax-free Nevada and summers in high-tax California—the residency and taxation rules become incredibly complex. You risk being taxed as a part-year resident in both locations. A qualified tax professional is vital to track your days, manage your domicile audits, and file the appropriate multi-state returns.

Scenario 3: The Business Owner or Real Estate Investor (Professional)

If your retirement involves selling a business, liquidating commercial real estate, or executing aggressive Roth IRA conversions, do not attempt this alone. The interaction between capital gains, state depreciation recapture, and federal provisional income requires sophisticated projection software. A certified planner can build a multi-year tax optimization strategy. You can locate vetted fiduciaries through the Certified Financial Planner Board.

Frequently Asked Questions

Do I still owe federal taxes if my state exempts Social Security?

Yes. State tax laws operate entirely independently of federal tax laws. Even if you live in a state with absolutely no income tax, like Texas or Florida, you must still calculate your Provisional Income. If your income exceeds federal thresholds, you will pay federal income tax on up to 85% of your Social Security benefits.

Will my state tax my 401(k) withdrawals even if it exempts Social Security?

It depends heavily on the state. While 42 states completely exempt Social Security, only a handful (such as Illinois, Mississippi, and Pennsylvania) completely exempt 401(k) and IRA withdrawals. Many states that protect your benefits will fully tax your traditional retirement account distributions at standard income rates.

Do I need to report exempt Social Security on my state return?

Generally, yes. Most state tax returns begin by asking for your Federal Adjusted Gross Income (AGI), which already includes the taxable portion of your Social Security. You will then use a specific line on the state tax form to “subtract” or “deduct” your federally taxable benefits out of the equation, bringing your state-level tax liability for those benefits down to zero.

Are pensions taxed the same way as Social Security?

Rarely. State governments usually treat pensions differently than Social Security. Furthermore, many states distinguish between public pensions (like those for teachers and firefighters) and private corporate pensions. A state might exempt military and civil service pensions entirely while aggressively taxing a private corporate pension. Always verify your specific state’s rules regarding your exact pension type.

Retirement presents a massive financial shift, moving you from decades of saving into a new era of strategic spending. By understanding how the 42 tax-exempt states treat your hard-earned benefits, you can make an informed, confident decision about where to plant your roots. Whether you choose the rugged independence of Wyoming, the coastal warmth of Florida, or the protective tax codes of Illinois, the right location aligns your financial reality with your lifestyle goals.

This is educational content based on general retirement and financial principles. Individual results vary based on your situation. Always verify current benefit rules, tax laws, and eligibility requirements with official sources like SSA, Medicare.gov, or the IRS.

Leave a Reply