Balancing a desire for extra income with the strict rules of the Social Security retirement earnings test requires careful planning. Once you claim benefits before reaching your full retirement age, the government limits how much you can earn before they start withholding your monthly checks. For those navigating this phase, earning even one dollar over the threshold means facing potential benefit reductions, making the right choice of employment crucial. Fortunately, the modern gig economy and shifting workplace demographics offer excellent opportunities for older adults looking to stay active without triggering financial penalties. By selecting flexible roles that allow you to precisely control your hours and income, you can secure valuable retiree income while keeping your hard-earned benefits entirely intact.

How the Social Security Earnings Test Dictates Your Choices

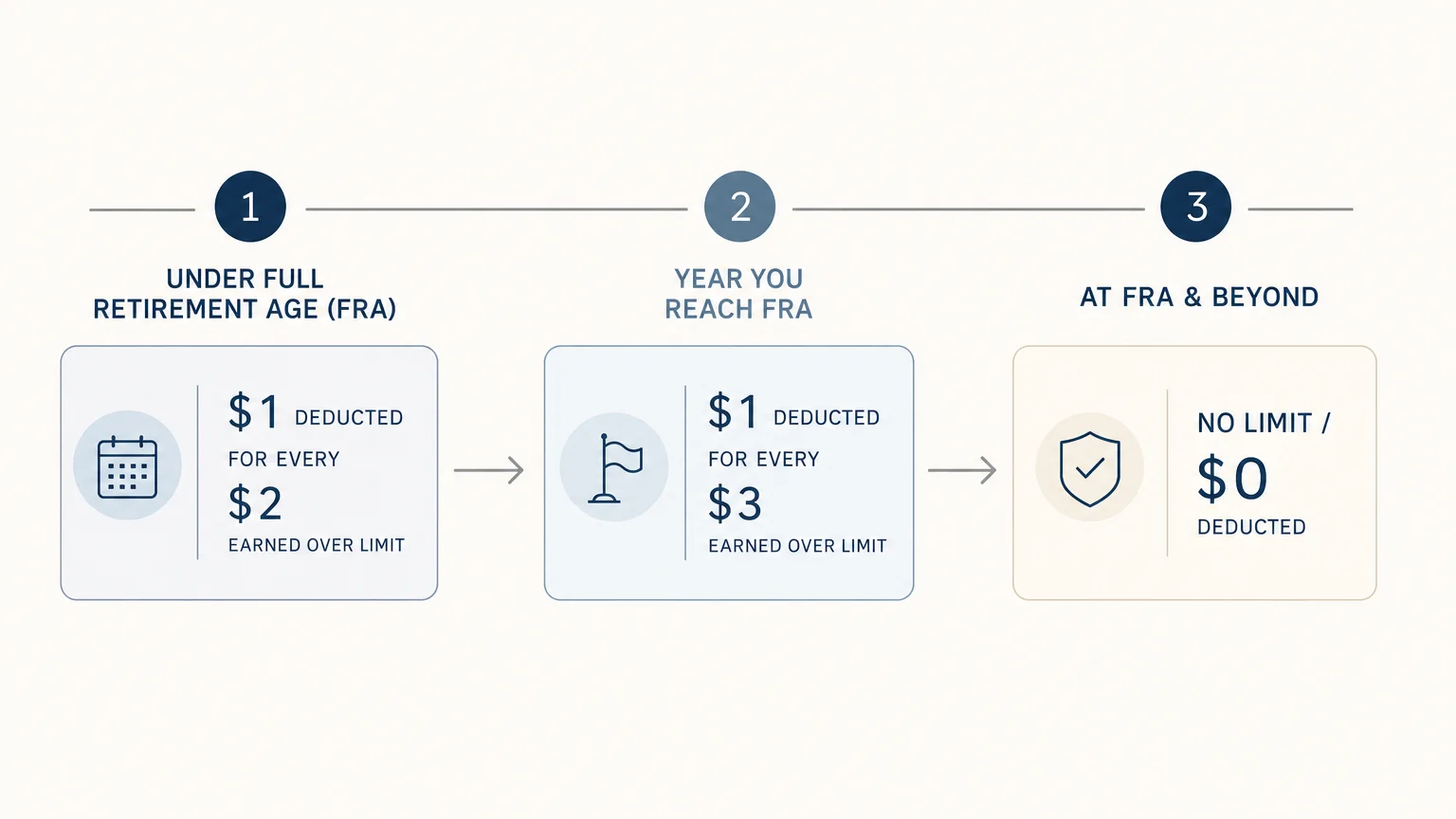

Before diving into specific job opportunities, you must understand exactly how the earnings test works. If you claim Social Security before your Full Retirement Age (FRA)—which falls between 66 and 67 for most people retiring today—the Social Security Administration (SSA) closely monitors your earned income. If your earnings exceed the annual limit, the SSA deducts $1 from your benefit payments for every $2 you earn above that threshold. In the specific year you reach your FRA, the rules soften slightly; the SSA deducts $1 for every $3 you earn above a significantly higher limit, and they only count earnings from the months prior to your birthday month.

Once you reach your FRA, the earnings test disappears entirely. You can earn an unlimited amount of money without facing any benefit reductions. However, if you are currently navigating the years prior to your FRA, selecting part-time jobs for retirees that offer total control over your schedule is the single most effective strategy for avoiding these penalties. You need roles where you can confidently project your annual income and stop taking on work the moment you approach the earnings threshold.

The Independent Contractor Advantage

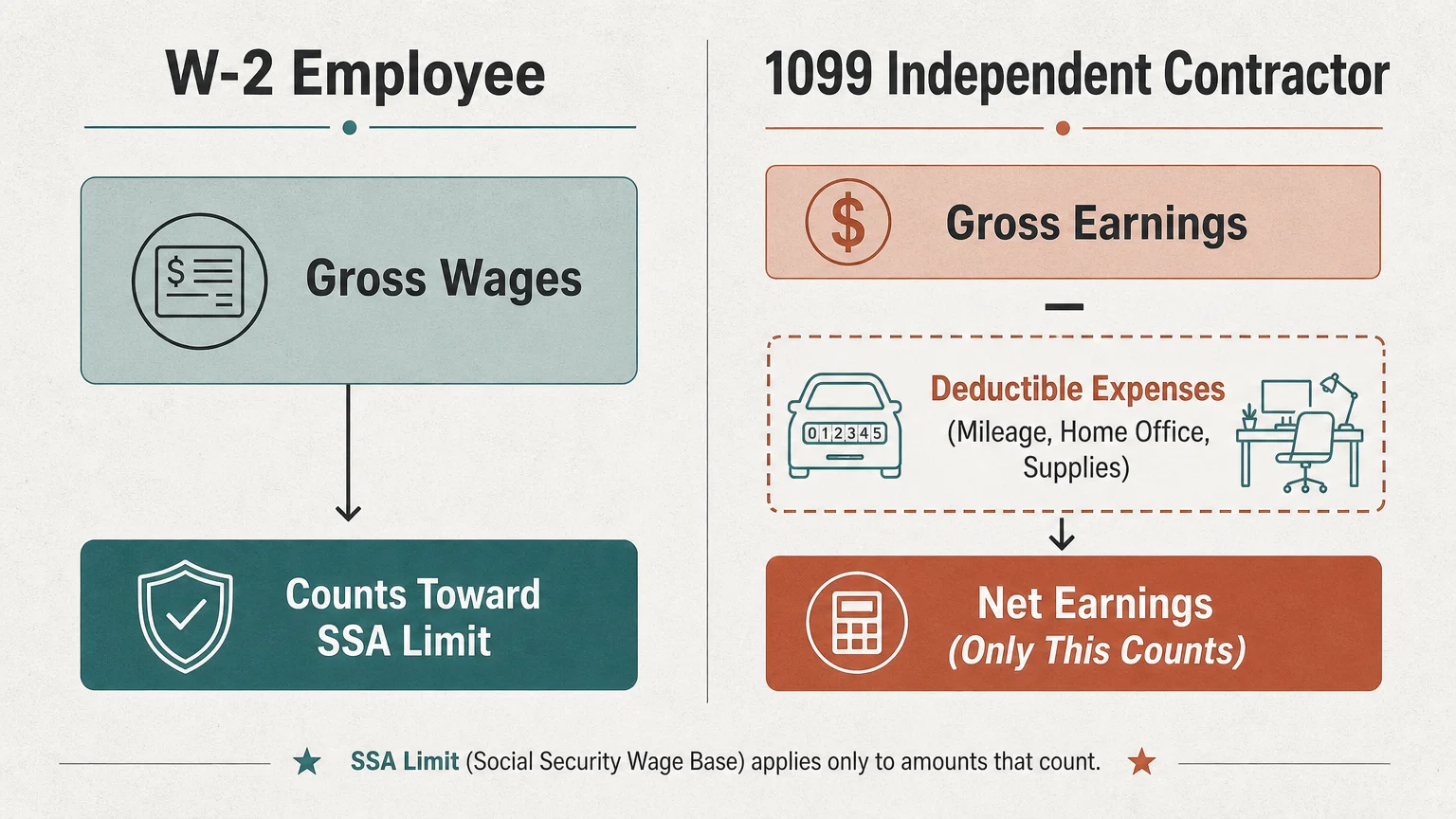

Many of the most flexible retirement jobs classify you as an independent contractor (a 1099 worker) rather than a traditional employee (a W-2 worker). This distinction provides a massive advantage when managing your Social Security earnings limit. When you work as an employee, the SSA counts your gross wages toward the earnings test. When you operate as an independent contractor, the SSA only counts your net earnings from self-employment.

This means you can deduct legitimate business expenses—such as mileage, home office costs, internet bills, and professional supplies—before reporting your final income figure. By legally reducing your net earnings through standard deductions permitted by the Internal Revenue Service (IRS), you can technically take home more money while keeping your official earnings below the Social Security limit. Always keep meticulous records of your expenses to maximize this advantage safely.

8 Flexible Retirement Jobs to Control Your Income

1. High-Value Consulting in Your Previous Industry

Your decades of professional experience carry immense market value. Instead of working a low-wage job that requires dozens of hours a week to generate meaningful income, consider consulting in your former field. Because consultants charge premium hourly or project rates, you can reach your target income by working only a fraction of the time.

For example, if you aim to earn $20,000 a year without crossing the earnings threshold, a $100-per-hour consulting rate means you only need to work 200 hours annually. That breaks down to fewer than four hours a week. Consulting allows you to remain engaged with your professional network, keep your mind sharp, and maintain absolute authority over which contracts you accept and when you complete the work.

2. Freelance Virtual Administration and Support

Small businesses and busy entrepreneurs increasingly rely on virtual assistants to manage their day-to-day operations. If you have a background in administration, project management, or basic accounting, you can easily transition these skills into a remote, part-time role. Virtual assistants handle tasks ranging from email management and scheduling to customer service and basic website maintenance.

The primary benefit of virtual administration is schedule autonomy. You dictate how many clients you take on and establish clear boundaries around your availability. When you calculate that your earnings are approaching the Social Security limit for the year, you can simply pause taking new clients or scale back your hours with existing ones.

3. Professional Pet Care and Dog Walking

For retirees seeking physical activity and a low-stress environment, pet sitting and dog walking offer an ideal blend of income and wellness. Platforms like Rover and Care.com make it incredibly simple to connect with local pet owners who need daily walks, drop-in visits, or overnight boarding.

- Physical Health Benefits: Regular dog walking ensures you meet daily cardiovascular exercise goals.

- Total Schedule Control: You set your exact availability on the apps. You can block out dates for vacations or turn off your profile entirely if you reach your income cap.

- Rate Autonomy: You determine your own pricing based on your local market and the specific services you provide.

4. Seasonal Tax Preparation or Bookkeeping

If you possess a strong aptitude for numbers, seasonal bookkeeping or tax preparation provides predictable, condensed income bursts. Many local accounting firms hire extra help between January and April to manage the influx of tax season. Alternatively, you can offer independent bookkeeping services to local small businesses.

This role fits perfectly into a retiree lifestyle because the heavy workload is confined to a few months of the year. You can earn a substantial portion of your allowed Social Security limit during the winter and early spring, leaving the rest of your year entirely free for travel, hobbies, and family.

5. Academic Tutoring or Adjunct Teaching

Sharing your knowledge with the next generation provides deep personal satisfaction alongside financial reward. Tutoring can take many forms: helping high school students prepare for college entrance exams, assisting elementary students with reading comprehension, or teaching English to international students online.

The academic calendar naturally limits your working hours. Work scales down during summer and holiday breaks, providing built-in downtime. Online platforms allow you to tutor from the comfort of your home, eliminating commute times and providing the flexibility to schedule sessions strictly around your lifestyle preferences.

6. App-Based Ride-Share or Delivery Driving

Few roles offer the immediate, on-demand flexibility of app-based driving. Whether you choose to transport passengers via Uber and Lyft or deliver groceries and meals through Instacart and DoorDash, you function as your own boss. You never have to ask for time off; you simply choose not to log into the application.

This level of control makes app-based driving one of the safest bets for retirees managing the earnings test. If you realize in November that you are only $500 away from hitting the annual limit, you just delete the app from your phone until January. Furthermore, the IRS standard mileage deduction significantly reduces your net taxable income, helping you keep more of what you earn without affecting your benefits.

7. Local Tour Guiding or Museum Docent

If you love your city and enjoy public speaking, working as a local tour guide or paid museum docent offers a fantastic way to generate retiree income while staying socially active. Many historical societies, ghost tour companies, and food tour operators look for reliable, articulate individuals to lead groups.

These roles are highly seasonal, often peaking during summer months or specific local festivals. You can commit to leading just one or two tours a week. The physical demands vary—some tours require extensive walking, while others operate on buses or boats—so you can select an option that matches your mobility and fitness level.

8. Paid Market Research and Focus Group Participant

Companies constantly seek consumer opinions to refine their products, marketing campaigns, and legal strategies. Participating in paid market research, online surveys, or professional mock juries requires zero long-term commitment. You act as an independent contractor, offering your demographic insights on a per-project basis.

While this income stream is the most sporadic on our list, it is also the easiest to manage. Focus groups often pay between $50 and $200 for a few hours of your time. Because you only participate when invited and when it suits your schedule, you run almost no risk of accidentally over-earning and triggering a Social Security penalty.

Comparing Your Part-Time Options

To help you decide which path aligns with your lifestyle, review this comparison of the most common flexible retirement jobs.

| Job Type | Income Structure | Flexibility Level | Typical Physical Demand |

|---|---|---|---|

| High-Value Consulting | 1099 (Net Income) | High | Low |

| Virtual Administration | 1099 (Net Income) | High | Low |

| Pet Care / Dog Walking | 1099 (Net Income) | Very High | Moderate to High |

| Seasonal Tax Prep | W-2 or 1099 | Moderate (Seasonal) | Low |

| Tutoring / Teaching | W-2 or 1099 | Moderate (Scheduled) | Low |

| Ride-Share / Delivery | 1099 (Net Income) | Maximum | Low to Moderate |

| Tour Guiding | W-2 or 1099 | Moderate | Moderate to High |

| Market Research | 1099 (Net Income) | Maximum | Low |

“A big part of financial freedom is having your heart and mind free from worry about the what-ifs of life.” — Suze Orman, Personal Finance Expert

Pitfalls to Watch For: Navigating Earnings Limits

Even with a highly flexible job, mistakes happen when retirees misunderstand what the SSA counts as “income.” The most common pitfall involves confusing earned income with passive income. The earnings limit only applies to wages from a job or net earnings from self-employment. It does not apply to pensions, annuities, investment dividends, interest, capital gains, or withdrawals from your IRA or 401(k). You can generate $100,000 a year in investment dividends, and the SSA will not deduct a single penny from your benefits.

Another dangerous pitfall involves the Special Earnings Limit Rule, which applies during your first year of retirement. If you retire mid-year, the SSA uses a monthly earnings test rather than the annual one for the remainder of that calendar year. This prevents you from being penalized for the high wages you earned before you officially retired. However, if you take a part-time job during that first year and exceed the strict monthly limit, you will face deductions even if your overall post-retirement annual earnings seem low. Always consult the SSA guidelines specifically for your first year of retirement to avoid accidental over-earning.

Finally, remember that while independent contractor status helps manage your Social Security earnings test through business deductions, it also makes you responsible for both the employer and employee portions of Medicare and Social Security taxes (known as SECA taxes). You must set aside roughly 15.3% of your net self-employment income to cover these tax obligations. The National Council on Aging (NCOA) frequently advises retirees to work with a tax professional during their first year of gig work to ensure they correctly balance their deductions and tax liabilities.

Frequently Asked Questions About Retiree Income

Does passive income affect my Social Security benefits?

No. The Social Security earnings test only applies to earned income—money you make from actively working a job or running a business. Passive income streams like real estate rentals, investment dividends, pensions, and retirement account withdrawals do not count toward the earnings limit and will not trigger a reduction in your monthly benefit check.

What happens to the money withheld by the SSA if I earn too much?

Many retirees mistakenly believe that money withheld by the earnings test is lost forever. It is not a permanent tax. When you reach your Full Retirement Age, the SSA will recalculate your monthly benefit amount to give you credit for the months they withheld your payments. Your monthly check will permanently increase, allowing you to gradually recoup the withheld funds over your remaining lifetime.

Will my Medicare premiums increase if I work part-time?

Medicare Part B and Part D premiums are based on your Modified Adjusted Gross Income (MAGI) from two years prior. If your part-time income, combined with your other retirement income, pushes you above certain high-income thresholds, you could face an Income-Related Monthly Adjustment Amount (IRMAA). However, because part-time retirement jobs generally cap out below the Social Security earnings limit, this modest extra income rarely pushes an average retiree into an IRMAA surcharge bracket.

Do I still pay Social Security taxes on my part-time income?

Yes. Regardless of your age or whether you are already collecting benefits, you must pay Social Security and Medicare taxes on your earned income. If you work a W-2 job, your employer will automatically deduct these from your paycheck. If you work as an independent contractor, you will pay them via your self-employment taxes when you file your annual return.

Maximizing Your Next Chapter

Staying active in the workforce during retirement provides undeniable mental, physical, and financial benefits. By strategically choosing flexible work—whether that means taking dogs for morning walks, consulting on your own terms, or delivering groceries for a few hours a week—you dictate the pace of your life. Track your net earnings carefully throughout the year, leverage the tax advantages of self-employment where applicable, and never hesitate to press pause on your work schedule when you approach the earnings threshold.

This is educational content based on general retirement and financial principles. Individual results vary based on your situation. Always verify current benefit rules, tax laws, and eligibility requirements with official sources like SSA, Medicare.gov, or the IRS.

Last updated: March 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply