Downsizing to a rental property in retirement frees you from property taxes and leaky roofs, but your financial exposure doesn’t disappear when you hand over the security deposit. Your landlord’s insurance policy covers the physical building, leaving everything you own—from your living room furniture to your grandmother’s wedding ring—completely vulnerable to fire, theft, or severe weather. Renters insurance acts as your financial safety net, stepping in to replace your personal property and shield your retirement savings from devastating liability claims. Understanding exactly what a renters insurance policy covers and where its limitations lie allows you to customize your protection, ensuring a burst pipe or a visitor’s slip-and-fall accident won’t derail your carefully planned retirement budget.

The Anatomy of a Standard Renters Insurance Policy

A standard renters insurance policy, known in the insurance industry as an HO-4 policy, provides a comprehensive shield against common domestic disasters. Many renters mistakenly assume this coverage functions as a single, blanket guarantee. In reality, a standard policy divides your protection into four distinct pillars, each serving a specific financial purpose. Managing your financial security for older adults requires understanding how these pillars work together to guard your assets.

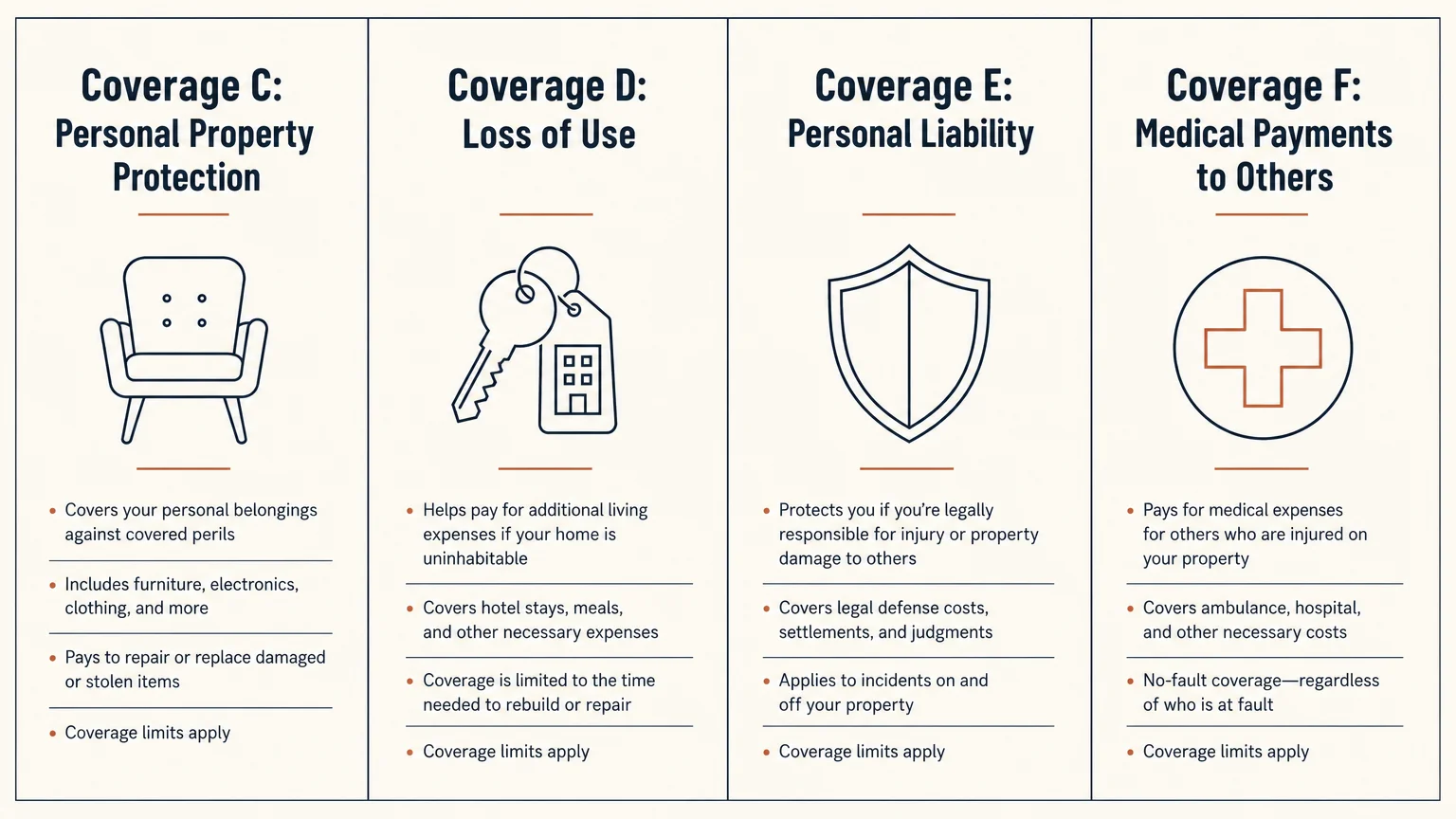

The four primary pillars include:

- Personal Property Protection (Coverage C): Pays to repair or replace your belongings if they are damaged or destroyed by a covered event.

- Loss of Use (Coverage D): Covers additional living expenses if a covered peril makes your rental unit uninhabitable.

- Personal Liability (Coverage E): Protects your financial assets if you are sued for causing bodily injury or property damage to someone else.

- Medical Payments to Others (Coverage F): Pays minor medical bills for guests injured in your home, regardless of who is at fault, helping you avoid costly liability lawsuits.

Personal Property Protection: Valuing Your Lifelong Possessions

Personal property protection forms the core of your renters insurance policy. This coverage reimburses you for the loss of your clothing, furniture, electronics, kitchenware, and other personal items. Renters insurance operates on a “named peril” basis, meaning the policy only pays for damage caused by specific events explicitly listed in your contract.

Standard covered perils typically include fire and lightning, windstorms and hail, explosions, riots, damage from aircraft or vehicles, smoke damage, vandalism, theft, falling objects, the weight of ice and snow, and accidental discharge of water or steam from plumbing systems. If a pipe bursts inside your apartment walls and ruins your antique dining set, your policy covers the damage. If a burglar forces the lock on your front door and steals your television, your policy covers the loss.

“An ounce of prevention is worth a pound of cure.” — Benjamin Franklin

When selecting your coverage limits, you must accurately estimate the cost to replace everything you own. Retirees often underestimate their property’s value because they accumulated their possessions gradually over several decades. Walking through your home and mentally calculating the cost to buy every item brand new reveals the true extent of your financial exposure. Proper calculating coverage limits ensures you do not face a catastrophic out-of-pocket expense after a fire or severe storm.

Actual Cash Value vs. Replacement Cost: A Critical Choice

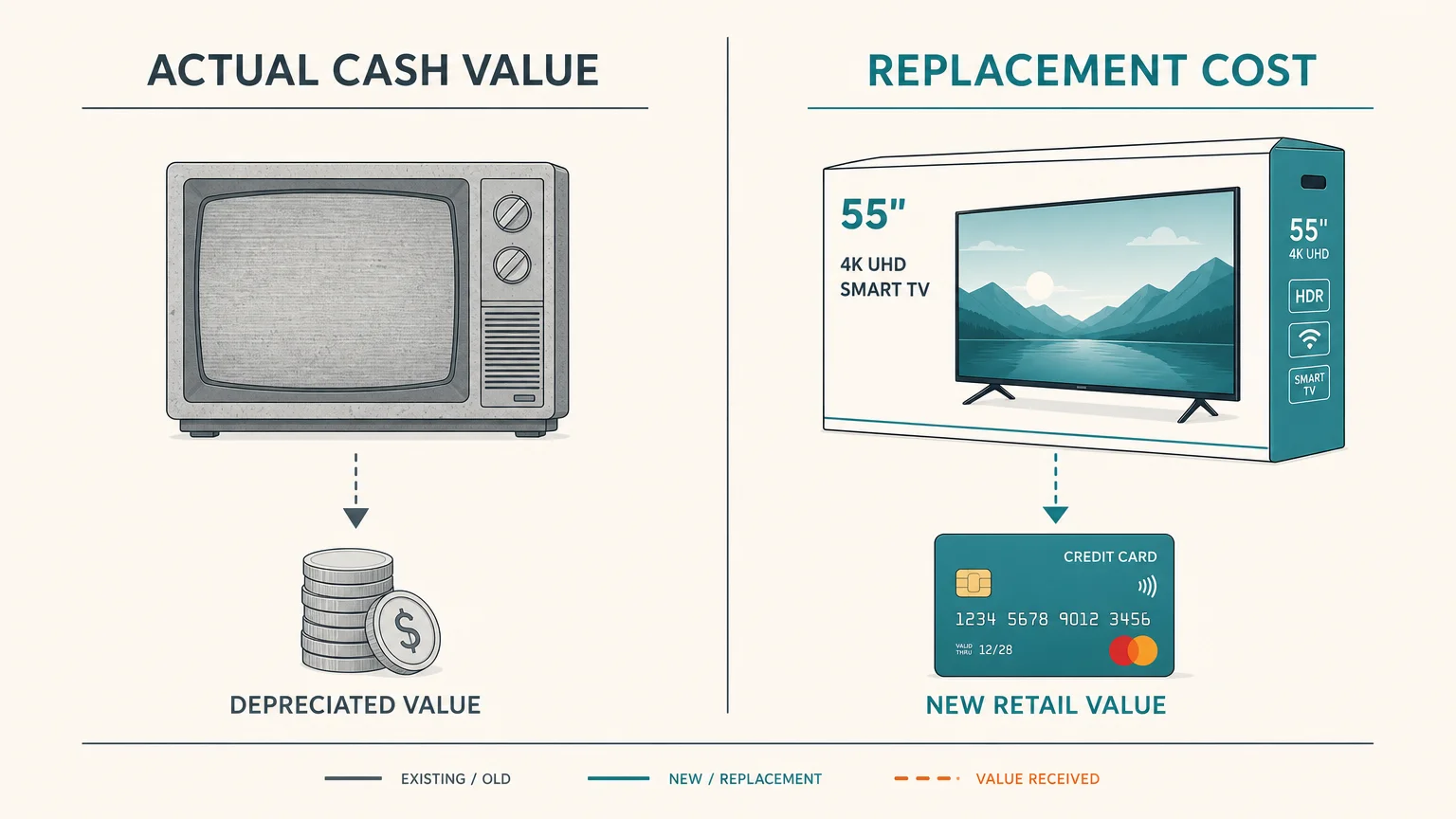

When purchasing a policy, your insurance provider asks you to choose how your claims will be settled: Actual Cash Value (ACV) or Replacement Cost Value (RCV). This single decision drastically impacts your financial recovery after a disaster.

Actual Cash Value factors in depreciation. If your five-year-old television is stolen, the insurance company calculates the lifespan of the television, subtracts five years of depreciation, and issues a check for its current, used market value. You receive a fraction of what you originally paid.

Replacement Cost Value ignores depreciation. The insurance company pays exactly what it costs to purchase a brand-new item of similar make and quality at today’s retail prices. While Replacement Cost policies carry slightly higher monthly premiums, they offer vastly superior financial protection, particularly for retirees on fixed incomes who cannot easily absorb the difference between a depreciated payout and a retail price tag.

| Feature | Actual Cash Value (ACV) | Replacement Cost Value (RCV) |

|---|---|---|

| Payout Calculation | Current market value minus years of depreciation. | The exact cost to buy a brand-new, equivalent item today. |

| Premium Cost | Generally 10% to 15% cheaper. | Slightly higher monthly or annual premium. |

| Out-of-Pocket Risk | High. You must cover the gap to buy new items. | Low. The policy covers the full retail purchase price. |

| Best Suited For | Renters with few assets and strict, minimal budgets. | Retirees seeking full financial recovery without tapping savings. |

Liability Coverage: Shielding Your Retirement Nest Egg

While personal property coverage replaces your belongings, personal liability coverage protects your net worth. For retirees, liability coverage is arguably the most critical component of a renters insurance policy. If a delivery driver slips on a wet spot in your kitchen and breaks their hip, or your dog bites a neighbor in the apartment courtyard, you can be held legally responsible for their medical bills, lost wages, and pain and suffering.

Without liability coverage, a personal injury lawsuit could force you to liquidate your retirement accounts, sell investments, or drain your savings. Renters insurance liability coverage pays for the injured party’s damages up to your policy limit. More importantly, it covers your legal defense costs. Lawyers charge hundreds of dollars per hour; having an insurance company provide your legal defense prevents a lawsuit from bankrupting you before you ever see a courtroom.

“A big part of financial freedom is having your heart and mind free from worry about the what-ifs of life.” — Suze Orman, Personal Finance Expert

Standard renters policies usually default to $100,000 in liability coverage. Financial experts strongly recommend increasing this limit to $300,000 or $500,000, especially since the premium increase for higher liability limits is typically negligible—often just a few dollars a year.

Loss of Use: Surviving Displacement

If a severe kitchen fire renders your apartment unlivable, you cannot simply sleep on the street while the landlord coordinates repairs. You need a place to stay, food to eat, and a way to maintain your standard of living. Loss of Use coverage, also known as Additional Living Expenses (ALE), covers the financial gap when a covered peril displaces you.

Loss of Use pays for hotel bills, temporary rental apartments, restaurant meals, pet boarding, and even laundry services while your home is uninhabitable. The coverage operates on the principle of “incurred additional costs.” If you normally spend $400 a month on groceries, but living in a hotel forces you to spend $1,000 a month at restaurants, the insurance company reimburses you for the $600 difference. Retain all receipts during your displacement, as adjusters require strict documentation before processing ALE claims.

The Hard Truth: What Renters Insurance Does Not Cover

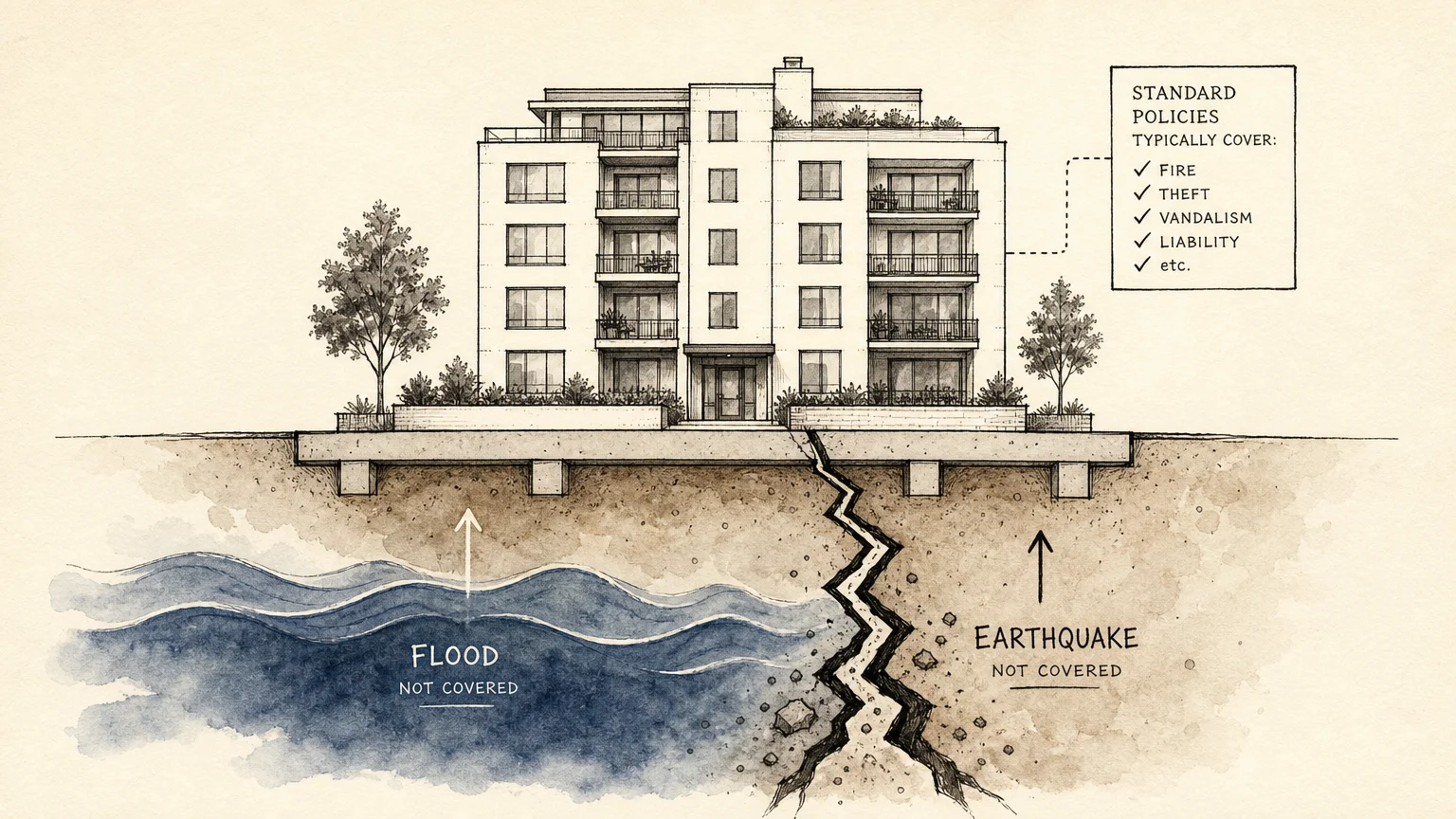

Understanding policy exclusions prevents devastating surprises during the claims process. Standard renters insurance contains strict boundaries regarding what qualifies for reimbursement. Assuming your policy covers every potential disaster leaves massive gaps in your financial plan.

Floods from Outside Water: Standard renters policies never cover damage caused by rising external water. If a nearby river breaches its banks, a storm surge floods your ground-floor apartment, or heavy rain overwhelms street drainage and pushes water under your door, your standard policy will deny the claim. Renters living in low-lying areas or flood zones must purchase a separate flood insurance policy through the National Flood Insurance Program (NFIP) or a private carrier.

Earthquakes and Sinkholes: Earth movement requires specialized coverage. If an earthquake shatters your glassware and topples your furniture, a standard HO-4 policy provides no relief. Renters in seismically active regions need a separate earthquake endorsement or policy.

High-Value Items (Beyond Sub-limits): Renters policies impose strict sub-limits on highly targeted theft items. While your total personal property coverage might be $50,000, the policy likely caps theft payouts for jewelry at $1,500, silverware at $2,500, and firearms at $2,500. If a burglar steals your $8,000 diamond anniversary ring, standard coverage only reimburses you up to the $1,500 sub-limit.

Pest Infestations: Insurance considers pest management a maintenance issue. Damage caused by mice, rats, termites, or bed bugs falls entirely outside the scope of renters insurance. Furthermore, the cost of extermination or replacing mattresses ruined by bed bugs remains your personal financial responsibility.

Roommates’ Belongings: Unless your roommate is related to you by blood or marriage, or legally listed on your specific insurance policy, their belongings lack coverage. If a fire destroys the apartment, your insurance solely reimburses you for your possessions. Unmarried partners should speak directly with their insurance agent about adding both names to the policy as named insureds.

Enhancing Your Safety Net: Endorsements and Floaters

If the standard exclusions leave your most valuable assets unprotected, you can modify your policy using endorsements, riders, or floaters. These add-ons customize your coverage to fit your specific lifestyle and asset profile.

Scheduled Personal Property: To protect high-value items like engagement rings, fine art, coin collections, or expensive medical equipment, you “schedule” them on your policy. This process involves providing the insurer with an appraisal or recent receipt. Scheduled property floats above the standard policy limits, bypasses your deductible, and often broadens coverage to include accidental loss—meaning the insurance pays even if you simply drop your ring down the kitchen drain.

Water Backup Endorsement: While standard policies cover burst pipes, they typically exclude damage caused by water backing up through sewers or drains. If the municipal sewer line clogs and pushes raw sewage into your ground-floor bathroom, you need a water backup endorsement to cover the massive cleanup and replacement costs.

Identity Theft Restoration: Many modern renters policies offer identity theft resolution endorsements for a nominal fee. This coverage reimburses you for legal fees, lost wages, and administrative costs associated with reclaiming your identity after a data breach or stolen wallet.

Common Mistakes to Avoid

Navigating the transition from homeownership to renting requires a mental shift in how you view property insurance. Avoid these frequent missteps when evaluating renters insurance policies.

Assuming the Landlord’s Policy Protects You: The most dangerous myth in renting is that the property owner’s insurance covers the tenant. The landlord’s commercial property policy covers the physical structure of the building and the landlord’s personal liability. It offers absolutely zero protection for your furniture, your clothing, or your legal liability if you cause an accident.

Setting the Deductible Incorrectly: Your deductible represents the amount you pay out of pocket before insurance kicks in. Choosing a $100 deductible results in high monthly premiums. Conversely, choosing a $2,500 deductible lowers your premium but makes the policy useless for smaller, common claims like a stolen laptop. A $500 or $1,000 deductible usually strikes the perfect balance for retirees seeking affordable premiums and accessible coverage.

Failing to Create a Home Inventory: Relying on your memory after a traumatic apartment fire guarantees you will leave money on the table. Adjusters require proof of what you owned. Use your smartphone to walk through your rental, opening drawers and closets, while recording a video of your possessions. Store this video in a cloud service or email it to yourself. Having visual proof drastically speeds up the claims process and ensures maximum reimbursement.

Frequently Asked Questions About Renters Insurance

Does renters insurance cover my belongings in a storage unit?

Yes, standard renters insurance extends coverage to your belongings stored “off-premises,” including items in a self-storage facility. However, insurance companies usually cap off-premises coverage at 10% of your total personal property limit. If you have $50,000 in personal property coverage, you have $5,000 in coverage for items in storage. The same covered perils (fire, theft, vandalism) apply.

Is my e-bike or mobility scooter covered?

Coverage depends entirely on the vehicle’s classification and motor size. Standard pedal bicycles enjoy full protection under a renters policy. Motorized mobility scooters used to assist a person with a disability are also generally covered. However, high-speed e-bikes and electric scooters used for recreation or commuting are frequently excluded under the “motor vehicle” exclusion. You must consult your agent to determine if your specific e-bike requires a specialized policy.

Do I need coverage if I move into an independent or assisted living facility?

Yes. Independent living apartments function exactly like traditional rentals, requiring standard renters insurance. In assisted living, some facilities provide minimal coverage for residents’ belongings, but it is rarely enough to replace a lifetime of possessions. A specialized renters policy or an endorsement on a family member’s homeowners policy ensures your assets remain protected in senior living communities.

Will a renters policy cover my dog if it bites someone?

Liability coverage generally extends to incidents involving your pets. If your dog bites a guest or another dog at the park, your renters insurance liability coverage pays for the medical bills and legal defense. However, many insurance companies exclude specific breeds deemed “high-risk,” such as Pit Bulls, Rottweilers, or Akitas. If you own an excluded breed, your policy will deny the claim, and you will need to purchase standalone canine liability insurance.

Maintaining proper insurance coverage serves as the bedrock of a stable, stress-free retirement. Renters insurance provides exceptional value, offering hundreds of thousands of dollars in asset protection for roughly the cost of a few cups of coffee each month. Take the time to inventory your belongings, assess your liability risks, and select a policy with robust replacement cost coverage. By understanding your specific risks and customizing your policy accordingly, you safeguard the wealth you spent a lifetime building.

This article provides general retirement education and information only. Every retiree’s situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: March 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply