The taxation of Social Security benefits catches millions of retirees off guard, turning a reliable income stream into an unexpected tax liability. Understanding whether these taxes could change again requires examining the legislative landscape facing the program’s trust funds. Originally tax-free, benefits first faced taxation in 1984; notoriously, the income thresholds determining those taxes have remained unadjusted for inflation ever since. As lawmakers debate the future solvency of the program ahead of the projected trust fund depletion in the 2030s, adjusting how benefits are taxed remains a prime target for reform. Staying ahead of these potential legislative shifts allows you to structure your retirement income defensively and keep much more of your hard-earned money over the long term.

The Historical Precedent for Social Security Taxation

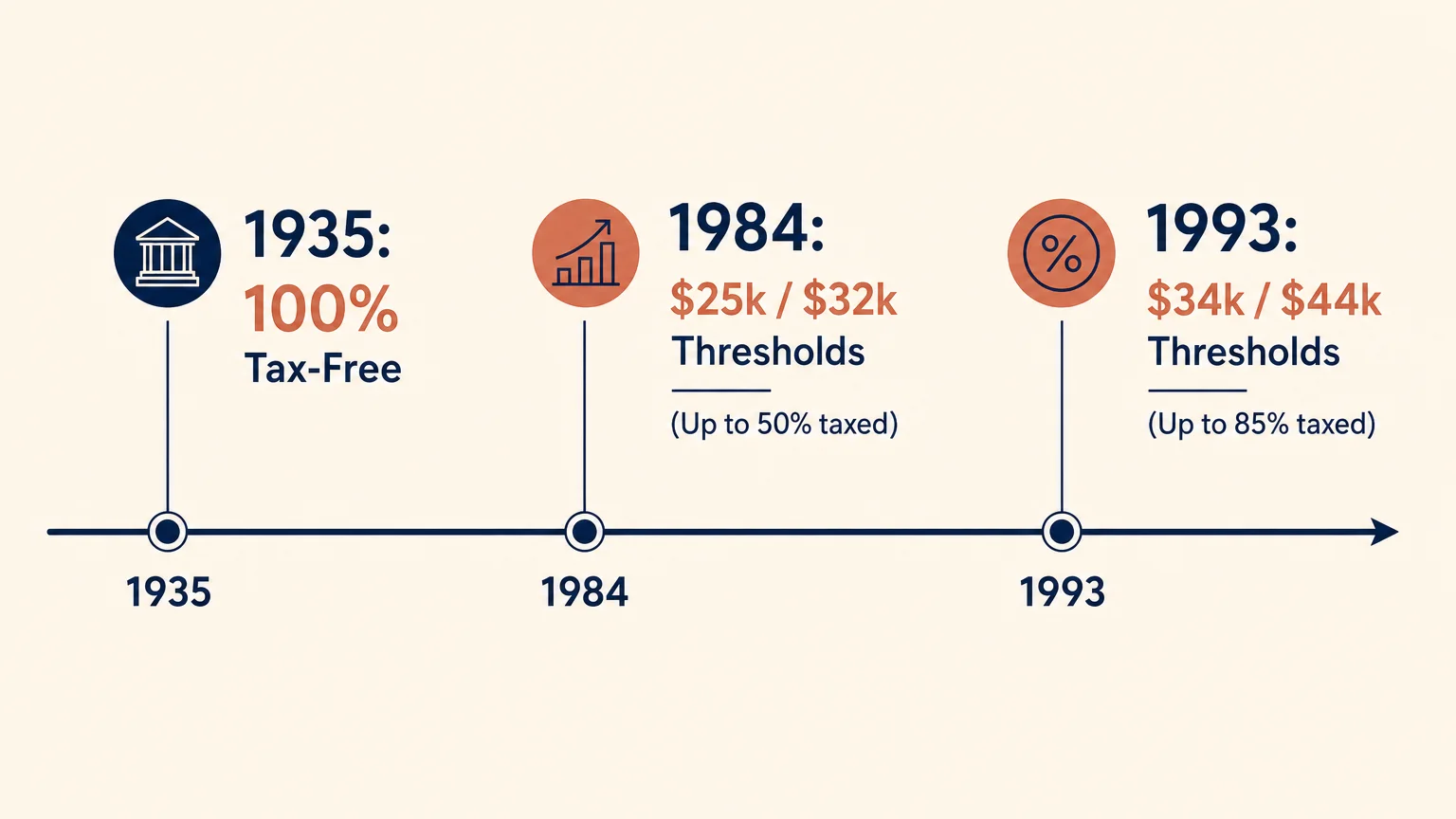

To understand where Social Security taxes might be heading, it is necessary to look at how we arrived at the current system. When the Social Security Act was signed into law in 1935, and for decades following the first monthly check issued in 1940, benefits were entirely exempt from federal income tax. The program was viewed strictly as a social insurance safety net, and taxing the benefits was considered contrary to its purpose of keeping older Americans out of poverty.

That paradigm shifted dramatically in the early 1980s. Facing a severe, immediate funding crisis where the program was mere months away from being unable to pay full benefits, the federal government formed the bipartisan National Commission on Social Security Reform, commonly known as the Greenspan Commission. Among the sweeping changes signed into law in 1983 was the introduction of a tax on the benefits of higher-income retirees.

Beginning in 1984, retirees whose “combined income” exceeded $25,000 for individuals or $32,000 for married couples filing jointly had to pay income tax on up to 50% of their Social Security benefits. At the time, these thresholds were considered high. The legislation was intentionally designed to only impact roughly the top 10% of wealthiest retirees. The revenue generated from this new tax was funneled directly back into the Social Security Trust Funds to help stabilize the program.

A decade later, the system underwent another major revision. The Omnibus Budget Reconciliation Act of 1993, driven by a desire to reduce the federal deficit and further shore up entitlement programs, added a second tier to the taxation formula. For individuals with combined income over $34,000 and couples over $44,000, up to 85% of their benefits became subject to federal income tax. The revenue from this second tier was directed into the Medicare Hospital Insurance Trust Fund.

The most critical historical detail—and the primary reason millions of middle-class retirees now pay these taxes today—is that Congress never indexed these income thresholds for inflation. Because the $25,000 and $32,000 base limits remain exactly the same today as they were in 1984, the natural rise in wages and living costs over four decades has resulted in profound “bracket creep.” What was once a tax exclusively on the wealthy now affects roughly half of all households receiving Social Security benefits.

How Your Benefits Are Taxed Today

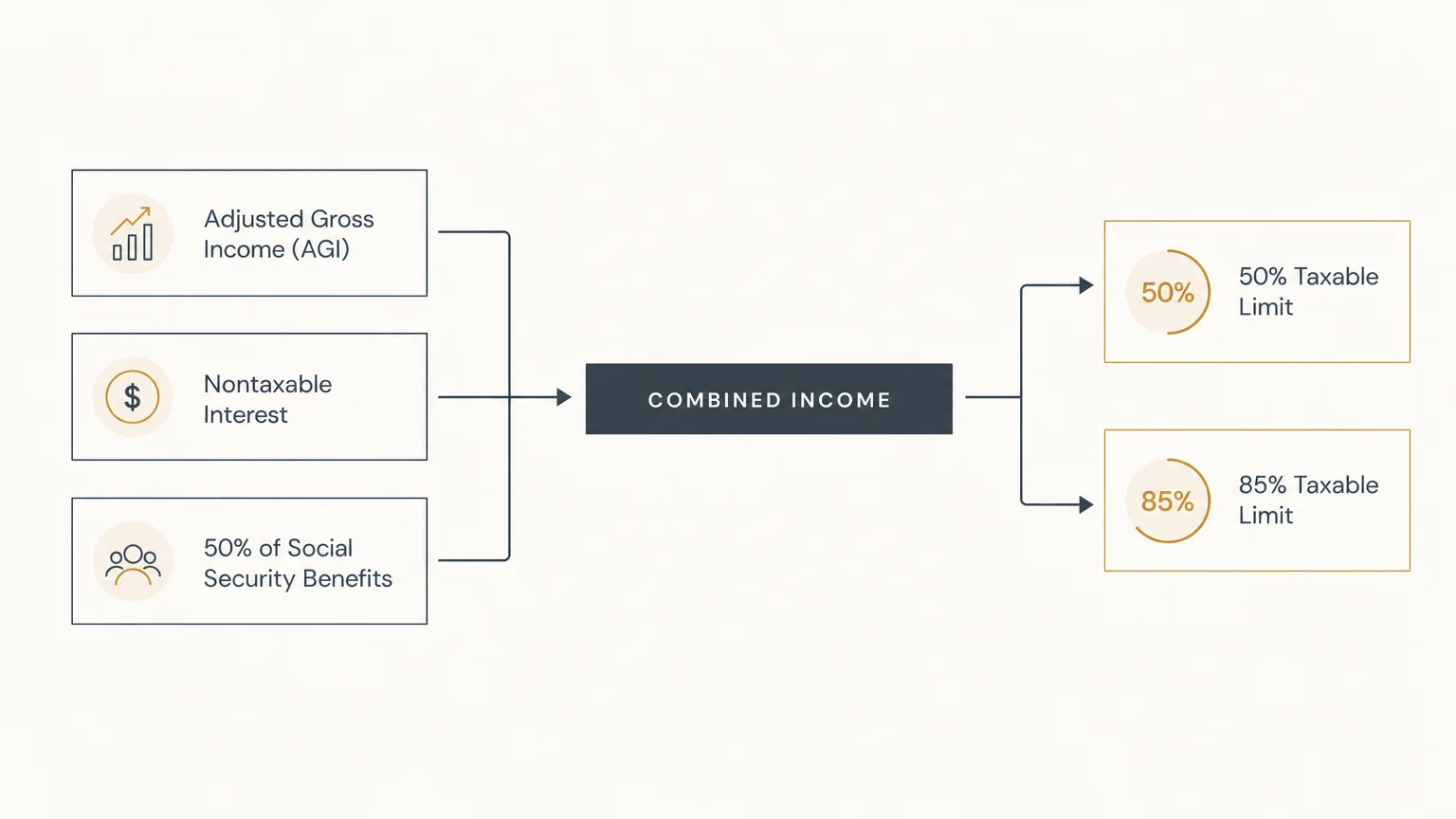

Before exploring how taxes might change, you must grasp the mechanics of how they are calculated right now. The Internal Revenue Service uses a specific metric called “Provisional Income” (sometimes referred to as combined income) to determine what portion of your Social Security benefits is subject to taxation.

Your Provisional Income is calculated using three components:

- Your Adjusted Gross Income (AGI): This includes your wages, pensions, traditional IRA withdrawals, 401(k) distributions, dividends, and taxable interest.

- Nontaxable Interest: Any interest you earn from municipal bonds, even though it is exempt from standard federal income tax, must be added back into this specific calculation.

- 50% of Your Social Security Benefits: Exactly half of the total benefits you and your spouse received during the tax year.

Once you calculate your Provisional Income, the IRS applies it to the unadjusted base limits established in 1984 and 1993. If you file as a single individual:

- Under $25,000: You pay zero federal income tax on your Social Security benefits.

- Between $25,000 and $34,000: Up to 50% of your benefits may be taxable.

- Over $34,000: Up to 85% of your benefits may be taxable.

If you are married and file a joint return:

- Under $32,000: You pay zero federal income tax on your Social Security benefits.

- Between $32,000 and $44,000: Up to 50% of your benefits may be taxable.

- Over $44,000: Up to 85% of your benefits may be taxable.

It is vital to recognize a common point of confusion: falling into the 85% tier does not mean you lose 85% of your Social Security check to taxes. It means that up to 85% of your total benefit amount is added to your taxable income for the year, which is then taxed at your standard marginal income tax rate.

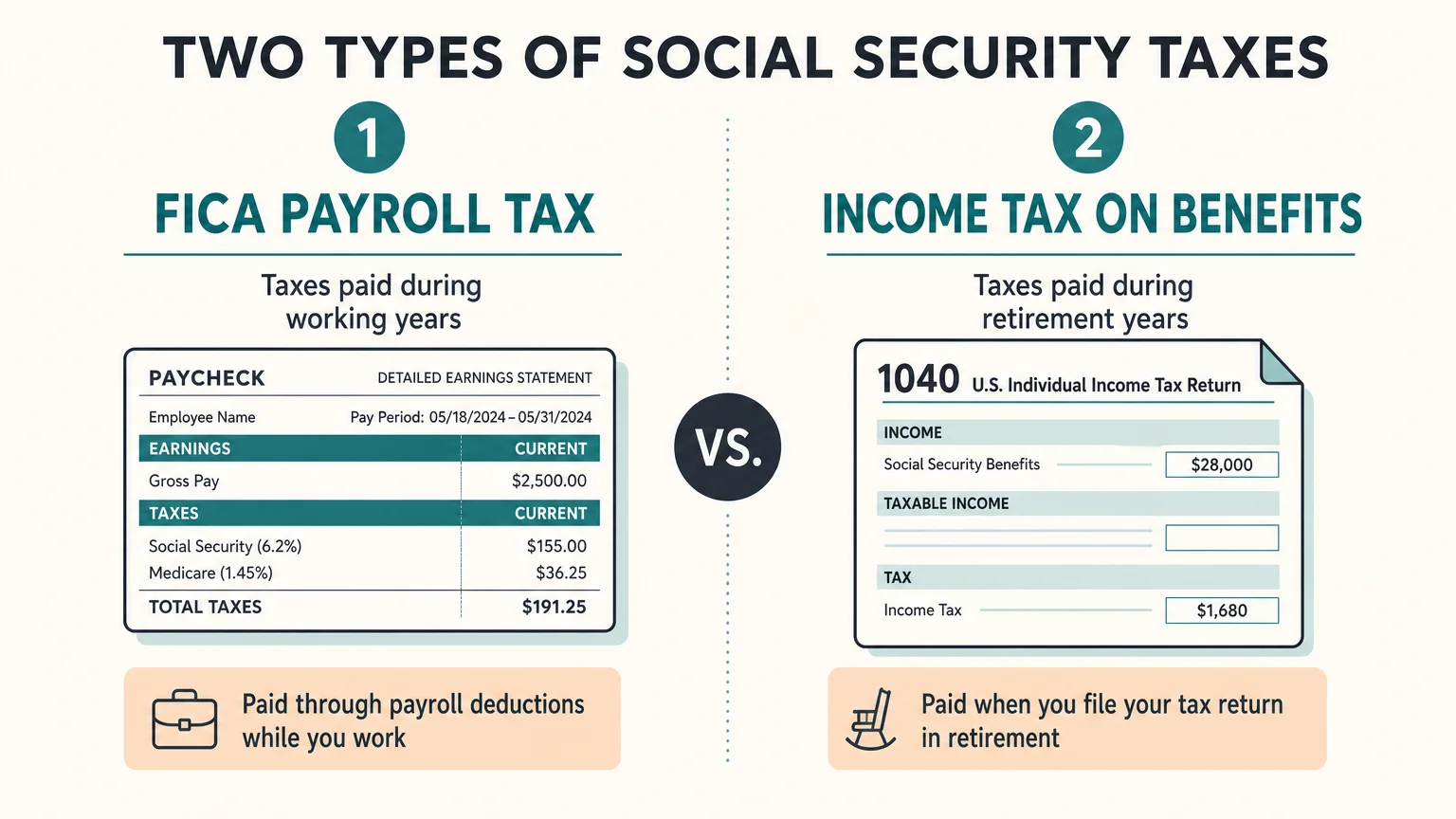

The Two Types of Social Security Taxes

When policymakers and financial analysts discuss “changes to Social Security taxes,” they are actually talking about two entirely different sides of the same coin. Understanding this distinction is crucial for your long-term retirement planning.

1. Taxation of Benefits (The Output Tax)

This refers to the federal income taxes you pay on the checks you receive during retirement, governed by the Provisional Income thresholds detailed above. Proposals to change this tax usually revolve around providing relief to current retirees by adjusting or eliminating the tax brackets.

2. Payroll Taxes (The Input Tax)

This refers to the Federal Insurance Contributions Act (FICA) taxes withdrawn from your paycheck while you are working. Currently, employees pay 6.2% of their earnings into the Social Security system, and employers match that 6.2%, for a total of 12.4%. However, this tax only applies up to a specific wage cap, known as the taxable maximum. In 2024, that cap was $168,600, and it adjusts annually based on average wage growth. Earnings above that cap are entirely exempt from the Social Security payroll tax. Self-employed individuals pay the full 12.4% via the self-employment tax.

When asking if Social Security taxes could change again, the answer involves legislative proposals targeting both the output taxes paid by retirees and the input taxes paid by current workers. Changes to either mechanism have profound ripple effects on the economy and your personal wealth.

The Looming Trust Fund Deadline

The primary catalyst driving the conversation about tax changes is the impending financial shortfall facing the Social Security program. The system operates through two primary trust funds: the Old-Age and Survivors Insurance (OASI) Trust Fund, which pays retirement and survivor benefits, and the Disability Insurance (DI) Trust Fund.

For decades, Social Security collected more in payroll taxes than it paid out in benefits, building up nearly $3 trillion in reserves. However, changing demographics—specifically the massive wave of Baby Boomers entering retirement, coupled with lower birth rates and longer life expectancies—have flipped that dynamic. The program is now paying out more than it takes in, requiring it to draw down its reserves to make full benefit payments.

According to the annual reports from the Social Security Administration Board of Trustees, the combined trust funds are projected to be depleted in the mid-2030s (typically estimated around 2033 to 2035). It is crucial to understand that “depletion” does not mean bankruptcy. Once the reserves are exhausted, ongoing tax revenues will still cover the majority of obligations. However, if Congress takes no legislative action before that depletion date, the law requires an automatic across-the-board benefit cut—projected to be roughly 21%—to align outgoing payments with incoming tax revenues.

Because allowing a 21% benefit cut for tens of millions of elderly Americans is widely considered political suicide, Congress will almost certainly be forced to act. Historically, closing a shortfall of this magnitude requires a combination of reducing future benefits (such as raising the full retirement age) and increasing revenue (raising taxes). Therefore, changes to Social Security taxes are not just possible; they are highly probable as the deadline approaches.

Proposed Legislative Changes on the Table

Lawmakers have introduced dozens of bills over the past decade aimed at restructuring Social Security taxes to avert the trust fund depletion and adjust retiree tax burdens. While none have yet passed both chambers of Congress, they provide a clear roadmap of the options being debated on Capitol Hill.

Eliminating the Tax on Benefits

Several popular legislative proposals, such as the repeatedly introduced “You Earned It, You Keep It Act,” aim to entirely repeal the federal income tax on Social Security benefits. Proponents argue that since workers already paid taxes on the wages that funded the system, taxing the benefits amounts to double taxation. While immensely popular with voters, the mathematical hurdle is severe. The taxes collected on benefits provide critical funding to both the Social Security and Medicare trust funds. Eliminating this tax without replacing the revenue would accelerate the trust fund depletion dates by several years. To offset this, these bills often propose raising payroll taxes on high earners.

Raising or Eliminating the Payroll Tax Cap

Currently, any earned income above the annual wage cap is exempt from Social Security payroll taxes. A dominant proposal among progressive lawmakers is to eliminate this cap entirely, subjecting all earned income to the 12.4% FICA tax, or to create a “donut hole” approach. Under a donut hole structure, earnings up to the current cap are taxed, earnings between the cap and a high threshold (such as $400,000) are exempt, and earnings above $400,000 are taxed again. This strategy would generate massive new revenues for the trust funds, significantly extending their solvency without raising taxes on middle-class workers.

Increasing the Payroll Tax Rate

Another straightforward mathematical fix is to gradually increase the FICA tax rate itself. Instead of the current 6.2% paid by employees and employers, proposals suggest inching the rate up slowly over a decade—for instance, to 7.2% each. While this spreads the burden across the entire workforce and generates immense revenue, it directly reduces the take-home pay of lower- and middle-income workers, making it a difficult political sell.

Indexing the Benefit Tax Thresholds to Inflation

A moderate proposal targets the bracket creep affecting current retirees. This legislation would retroactively adjust the $25,000 and $32,000 Provisional Income thresholds to reflect inflation since 1984, pushing the new thresholds to well over $70,000 for individuals and $90,000 for couples. Moving forward, these limits would be indexed to the Consumer Price Index (CPI), ensuring that middle-class retirees are not penalized simply due to the rising cost of living. This would drastically reduce the number of retirees paying taxes on their benefits, but it also creates a revenue shortfall that would need to be addressed elsewhere.

| Proposal Strategy | Mechanism | Primary Benefit | Primary Drawback |

|---|---|---|---|

| Eliminate Taxation on Benefits | Repeals federal income tax on Social Security checks. | Increases net income for millions of current retirees. | Removes vital revenue from trust funds; worsens solvency unless offset. |

| Index Thresholds to Inflation | Adjusts the 1984 Provisional Income base limits upward annually. | Stops bracket creep; protects middle-class retirees from tax traps. | Reduces incoming revenue to Medicare and Social Security trust funds. |

| Raise Payroll Tax Cap | Subjects wages above the current cap (or over $400k) to FICA taxes. | Generates massive revenue to fix trust fund shortfall. | Significantly increases tax burden on high-income workers. |

| Increase FICA Rate | Gradually raises the 6.2% worker/employer tax rate. | Shares the funding burden across the entire workforce equally. | Reduces immediate take-home pay for lower and middle-income workers. |

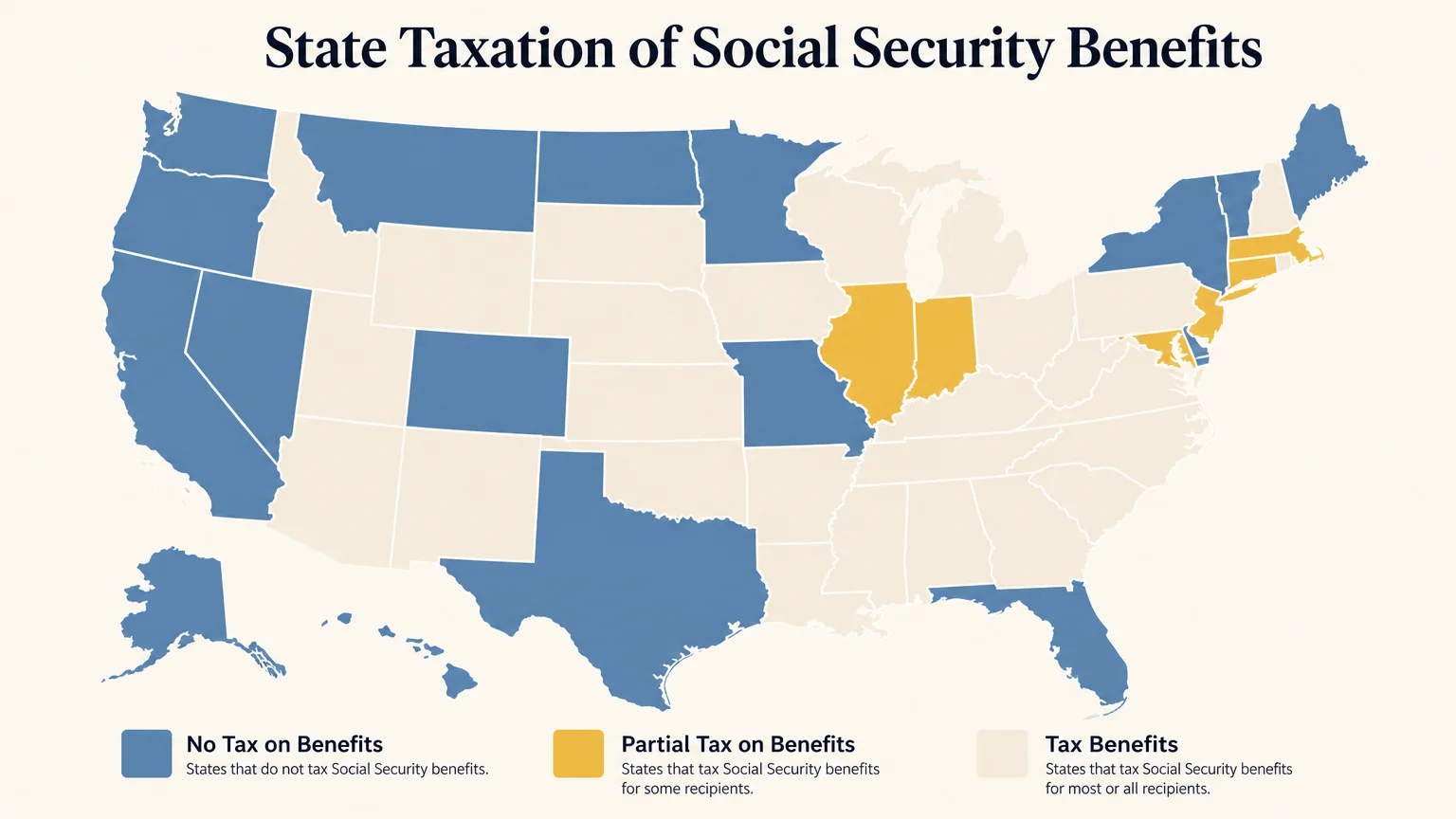

The Shift in State-Level Benefit Taxation

While the federal government remains locked in a stalemate over how to adjust Social Security taxes, state governments have been moving decisively in the opposite direction. Historically, many states mirrored the federal tax code and levied state income taxes on Social Security benefits. However, the trend over the last decade has been a rapid retreat from this practice.

States recognize that retirees are highly mobile and heavily weigh tax burdens when deciding where to live out their golden years. To remain competitive and retain the economic stimulus that retirees provide, numerous state legislatures have phased out their taxes on Social Security.

As recently as the early 2020s, more than a dozen states taxed benefits. Today, that number has shrunk dramatically. States like Missouri and Nebraska have recently enacted legislation to fully exempt Social Security benefits from state income taxes. Currently, only a handful of states still tax these benefits, and among those that do, most offer generous age or income-based exemptions that shield the majority of middle-class retirees. If you live in a state that still taxes benefits, such as Colorado, Connecticut, Minnesota, Montana, New Mexico, Rhode Island, Utah, or Vermont, it is highly advisable to consult resources like Kiplinger to understand your specific state-level exemptions and stay updated on local legislative changes.

Strategic Moves to Protect Your Retirement Income

Given the uncertainty surrounding federal tax changes, the most prudent approach is to manage the variables you can control. By manipulating the timing and sources of your retirement income, you can exert significant control over your Provisional Income, potentially shielding your Social Security benefits from high federal tax rates.

Executing Roth Conversions

One of the most powerful strategies to defuse future Social Security taxes is utilizing a Roth IRA. Withdrawals from a traditional IRA or 401(k) count dollar-for-dollar toward your Adjusted Gross Income, directly inflating your Provisional Income and triggering taxes on your benefits. Conversely, qualified withdrawals from a Roth IRA do not count toward your AGI. They are entirely invisible to the Provisional Income calculation.

Many retirees utilize the “tax valley”—the low-income years between when they retire and when they claim Social Security or face Required Minimum Distributions (RMDs)—to execute Roth conversions. By voluntarily shifting money from tax-deferred accounts to a Roth IRA and paying the taxes during these lower-income years, you permanently remove those assets from future Provisional Income calculations. When you eventually draw on the Roth account later in retirement, the income will not cause your Social Security benefits to become taxable.

Optimizing Withdrawal Sequencing

How you sequence your withdrawals across different types of accounts dictates your tax burden. A common mistake is draining standard taxable brokerage accounts first, then shifting entirely to traditional IRAs. Because traditional IRA withdrawals are fully taxable, relying on them exclusively later in retirement almost guarantees your Social Security will be pushed into the 85% taxable tier.

Instead, coordinate your withdrawals proportionally. By blending distributions from tax-deferred accounts (Traditional IRAs), tax-free accounts (Roth IRAs), and taxable brokerage accounts (where only the capital gains are taxed, not the principal), you can intentionally suppress your Provisional Income to stay just below the $34,000 or $44,000 thresholds.

Utilizing Qualified Charitable Distributions (QCDs)

If you are charitably inclined and over age 70½, Qualified Charitable Distributions are a vital tool. Once you reach RMD age, the IRS forces you to withdraw a certain amount from your tax-deferred accounts each year, whether you need the money or not. This forced income frequently pushes retirees over the Provisional Income thresholds, subjecting their Social Security to heavy taxation.

A QCD allows you to transfer funds directly from your traditional IRA to a qualified charity. This distribution satisfies your RMD requirement but is completely excluded from your Adjusted Gross Income. Because it bypasses your AGI entirely, it does not inflate your Provisional Income, allowing you to support causes you care about while simultaneously protecting your Social Security checks from the IRS.

Delaying Social Security Claims

Delaying your Social Security benefits until age 70 offers a dual advantage. First, it guarantees an 8% increase in your benefit amount for every year you delay past your full retirement age. Second, it reduces the number of years your benefits are subjected to taxation. By spending down your traditional IRA balances in your early 60s while delaying Social Security, you effectively reduce the future RMDs that would later trigger taxes on your benefits.

Financial expert Suze Orman emphasizes the importance of this timing:

“The biggest mistake you can make is to treat your Social Security as an afterthought. It is the foundation of your retirement house. Delaying until 70 is the best investment you can make.” — Suze Orman, Personal Finance Expert

Navigating the Social Security Tax Torpedo

Perhaps the most insidious element of the current tax structure is a phenomenon financial planners refer to as the “Social Security Tax Torpedo.” This occurs when a retiree needs to generate just a little bit of extra cash—perhaps taking an extra $1,000 from an IRA to pay for a minor home repair—but experiences a massive, disproportionate spike in their marginal tax rate.

Here is how the math traps retirees: Because of how Provisional Income is structured, pulling an extra $1,000 out of a traditional IRA increases your AGI by $1,000. If your Provisional Income is already sitting inside the 85% phase-in tier, that $1,000 withdrawal forces an additional $850 of your Social Security benefits to become taxable.

Consequently, your taxable income for the year didn’t just increase by the $1,000 you withdrew; it increased by $1,850. If you are in the 22% federal tax bracket, you must pay 22% tax on that entire $1,850. This means the actual tax bill on your $1,000 withdrawal is $407—creating an effective marginal tax rate of 40.7%, higher than the top tax bracket paid by billionaires.

Navigating the tax torpedo requires hyper-vigilant income management. If you know you are approaching the threshold where the 85% rule triggers, generating extra cash from a Roth IRA, a home equity line of credit, or by selling assets with zero capital gains in a standard brokerage account is infinitely preferable to pulling from a tax-deferred IRA.

Avoiding Common Errors

The complexity of retirement taxation leads to several pervasive myths and costly mistakes. Recognizing these pitfalls is half the battle in preserving your income.

- Misunderstanding the 85% Rule: As previously noted, the most common error is believing the IRS seizes 85% of your Social Security check. Never make financial decisions based on this fear. The rule dictates that up to 85% of the benefit is added to your income, where it is then taxed at your standard bracket rate (typically 10%, 12%, or 22%).

- Ignoring Municipal Bond Interest: Retirees frequently heavily invest in municipal bonds under the assumption they provide “tax-free income.” While exempt from standard federal taxes, municipal bond interest must be added back into the Provisional Income formula. A portfolio heavy in municipal bonds can easily cause your Social Security benefits to become fully taxable.

- Spiking Income in a Single Year: Large, one-time financial events can wreak havoc on your benefit taxation. Selling a highly appreciated secondary property, executing a massive one-time Roth conversion, or realizing large capital gains all spike your AGI for that year. If possible, spread large liquidations over multiple tax years to avoid pushing a single year’s Provisional Income into the maximum taxation tier.

- Forgetting the Widow’s Penalty: When one spouse passes away, the surviving spouse experiences a sharp drop in their Provisional Income thresholds (from $32,000 down to $25,000) because they must now file as a single taxpayer. Even though household income has dropped because the smaller of the two Social Security checks ceases, the surviving spouse often finds themselves pushed into a higher tax bracket, paying more taxes on less total income.

When DIY Isn’t Enough

While basic income management is manageable for many, certain financial situations introduce a level of complexity where relying strictly on self-education can result in severe financial penalties. The tax code is unforgiving, and restructuring your income retroactively is rarely possible.

You should strongly consider consulting a Certified Public Accountant (CPA) or a Certified Financial Planner (CFP) if you face any of the following scenarios:

- You Are Approaching RMD Age with Massive Pre-Tax Balances: If you have accumulated $1 million or more in traditional IRAs or 401(k)s, your Required Minimum Distributions will be substantial. A professional can help you execute a multi-year Roth conversion strategy to draw down those balances before RMDs begin, smoothing your tax liability over time and protecting your future Social Security checks.

- You Own a Business or Farm: Retirees who continue to receive K-1 income, royalties, or business distributions face highly variable AGIs. This unpredictable income makes managing Provisional Income incredibly difficult without advanced tax projection software and professional guidance.

- You Are Navigating the Widow’s Penalty: Transitioning from “Married Filing Jointly” to “Single” alters your entire tax landscape. A professional can help sequence which accounts the surviving spouse should draw from first to minimize the abrupt tax increase on their remaining benefits.

- You Plan to Relocate Across State Lines: Moving introduces new variables, including changes in state income tax, property tax, and estate tax laws. A professional can analyze whether the tax savings of moving to a state that doesn’t tax Social Security are offset by higher property or sales taxes.

Frequently Asked Questions

At what age does Social Security stop being taxed?

Age has no bearing on the federal taxation of your Social Security benefits. Whether you claim at 62, reach full retirement age, or live past 100, the IRS applies the exact same Provisional Income rules. The tax never expires based on your age.

Does my spouse’s income affect the tax on my Social Security?

Yes, if you file your taxes as “Married Filing Jointly.” The IRS looks at the combined Adjusted Gross Income of both spouses, plus 50% of your combined Social Security benefits, to determine your Provisional Income. If your spouse continues to work and earns a high salary, it is highly likely that up to 85% of your combined Social Security benefits will be subject to taxation.

Can I have taxes withheld directly from my Social Security check?

Yes. If you anticipate that your benefits will be taxable and want to avoid a large bill at tax time or potential underpayment penalties, you can file IRS Form W-4V (Voluntary Withholding Request). You can choose to have the government withhold 7%, 10%, 12%, or 22% of your monthly benefit for taxes.

Will Congress fix the unadjusted income thresholds?

While there is bipartisan acknowledgment that the 1984 limits unfairly punish middle-class retirees due to inflation, adjusting them requires replacing the lost revenue. Because the taxes collected on benefits flow directly into the Medicare and Social Security trust funds, lawmakers are hesitant to adjust the thresholds without passing broader tax increases elsewhere to compensate.

Anticipating changes to Social Security taxes requires vigilance. The mathematical realities of the looming trust fund depletion guarantee that the status quo cannot persist indefinitely. Congress will have to pull one or several levers—raising payroll caps, adjusting tax rates, or altering benefit taxation—within the next decade. Rather than waiting passively for legislation to pass, the most effective approach is to build flexibility into your retirement portfolio now. Cultivating a mix of tax-deferred, tax-free, and taxable accounts ensures that regardless of how the IRS changes the rules, you retain the ability to maneuver and minimize your tax burden.

This article provides general retirement education and information only. Every retiree’s situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: June 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply