A reliable pension provides a strong foundation for your retirement, but rising living costs and shifting lifestyle goals often demand additional cash flow. Securing extra money in retirement does not mean you have to return to the forty-hour workweek or sacrifice the freedom you spent decades building. Instead, strategically leveraging your existing assets, skills, and government benefits can bridge the gap between what your pension covers and the retirement lifestyle you actually want. Whether you need to cover increasing healthcare expenses, fund travel plans, or simply build a more comfortable safety net, exploring these ten distinct strategies will help you supplement your pension income while keeping your financial independence intact.

At a Glance: Expanding Your Financial Foundation

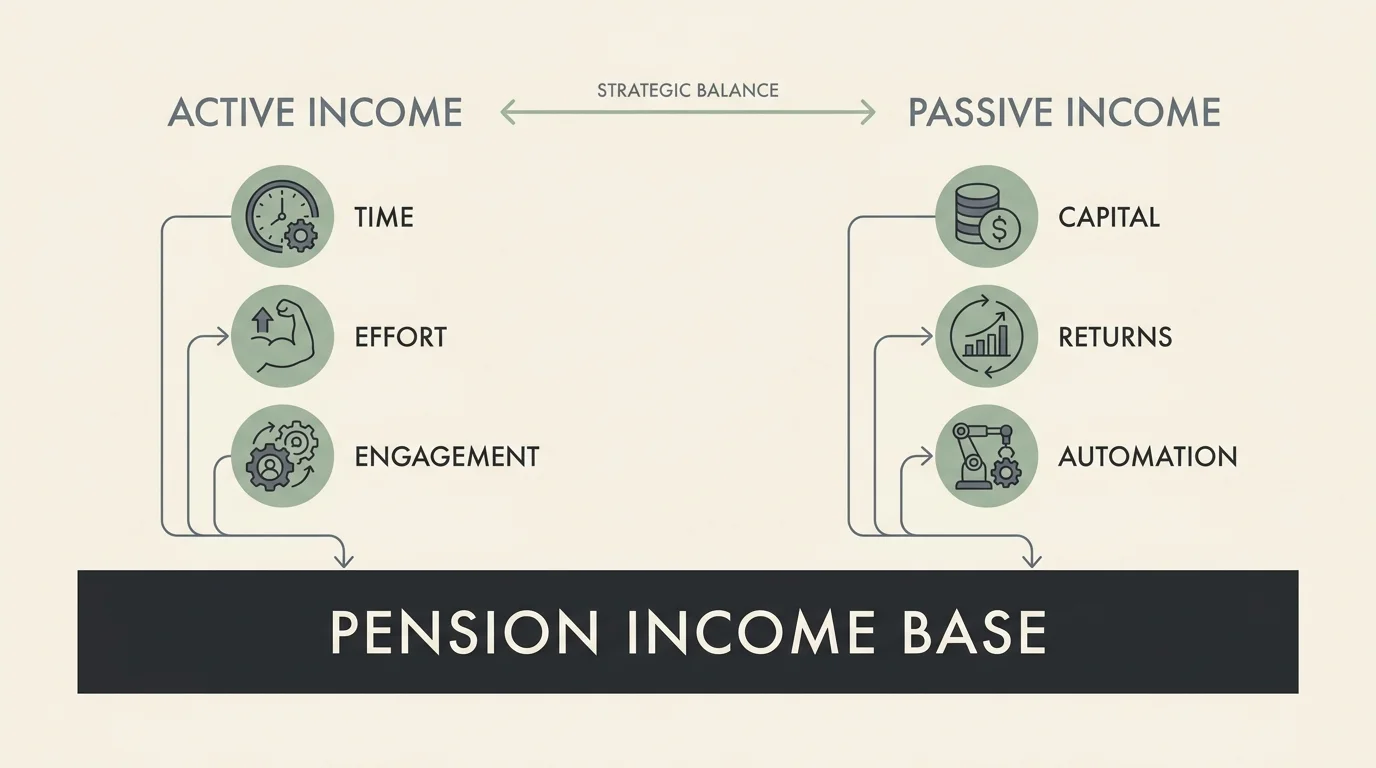

Diversifying your cash flow mitigates risk and provides peace of mind. A pension offers a fixed baseline; the strategies you layer on top of it will determine your flexibility. Retirees generally blend active income streams—which require ongoing time and effort—with passive income vehicles that generate returns automatically. Exploring a combination of both ensures you remain engaged without overwhelming your schedule. The most effective retirement plans utilize multiple avenues to build an income floor that outpaces inflation.

1. Optimize Your Social Security Claiming Strategy

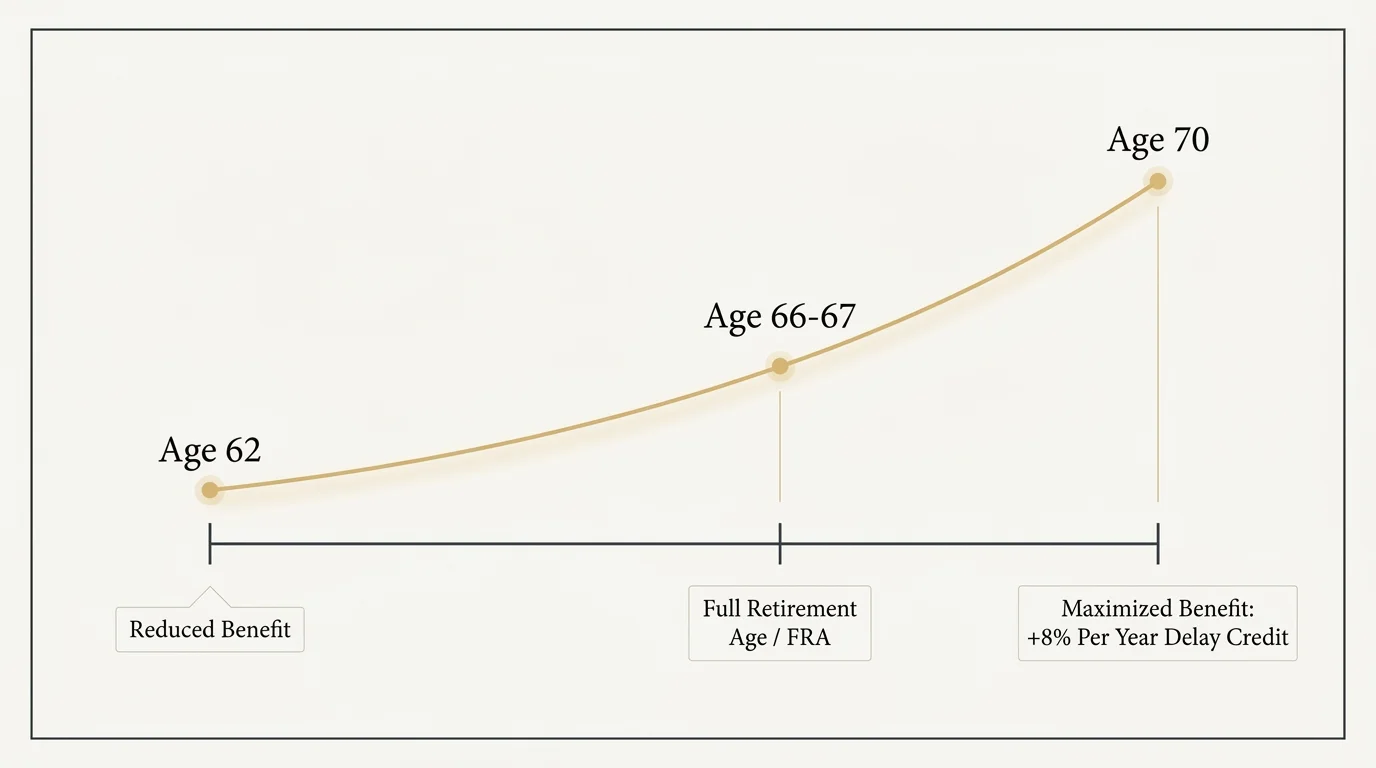

For most retirees, Social Security represents the largest stream of guaranteed, inflation-adjusted income available outside of a pension. Because you already have pension income to rely on, you possess a distinct advantage: the ability to delay your Social Security benefits. Your pension acts as a bridge, covering your living expenses in your early sixties so you can maximize your federal benefits later.

You can claim Social Security as early as age 62, but doing so permanently reduces your monthly payout. Conversely, if you wait until your Full Retirement Age (FRA)—which falls between 66 and 67 for most people currently retiring—you receive your standard benefit amount. The true mathematical power lies in delaying past your FRA. For every year you wait to claim between your FRA and age 70, your benefits increase by a guaranteed 8 percent. This delayed retirement credit provides a substantially larger monthly check for the rest of your life, establishing an unbeatable hedge against longevity risk.

Additionally, coordinated claiming strategies matter deeply for married couples. You must evaluate how your individual benefits interact with spousal benefits and survivor benefits. A higher-earning spouse delaying their claim to age 70 not only maximizes their own income but also ensures the surviving spouse receives the highest possible survivor benefit down the road. You can review your earning history and run personalized estimates directly through the Social Security Administration to map out the exact financial impact of delaying.

2. Build a Dividend-Paying Portfolio

Transitioning from a growth-focused investment strategy to an income-focused one allows you to generate cash without selling off the principal of your portfolio. Dividend-paying stocks distribute a portion of corporate earnings directly to shareholders, typically on a quarterly basis. When you rely on a pension for your fixed expenses, you can direct dividend yields toward discretionary spending like travel, dining, or gifting.

“If you don’t find a way to make money while you sleep, you will work until you die.” — Warren Buffett, Investor and CEO

Retirees often gravitate toward “Dividend Aristocrats”—companies that have consistently increased their dividend payouts for twenty-five consecutive years or more. These established corporations operate in stable sectors such as consumer staples, utilities, and healthcare. Because they prioritize steady dividend growth, they can provide a rising income stream that naturally combats inflation.

If picking individual stocks feels too time-consuming or risky, dividend-focused exchange-traded funds (ETFs) or mutual funds offer instant diversification. These funds pool together dozens or hundreds of dividend-paying companies, lowering your exposure to any single corporate failure. Furthermore, qualified dividends receive favorable tax treatment compared to ordinary income, allowing you to keep more of the money you earn. For objective guidance on evaluating dividend yields and managing investment risk, resources from Investor.gov provide an excellent starting point.

3. Strategically Tap Into Home Equity

Your home likely represents a massive portion of your net worth, yet it sits dormant from an income perspective. Turning home equity into liquid capital provides a powerful way to supplement your pension, particularly if your home is fully paid off.

Downsizing remains the most straightforward method for extracting this wealth. Selling a large family home and moving into a smaller, more accessible property accomplishes two financial goals simultaneously: it liberates a lump sum of cash that you can invest for income, and it drastically reduces your ongoing carrying costs—including property taxes, maintenance, and utility bills. Under current tax law, a married couple filing jointly can exclude up to $500,000 of capital gains on the sale of a primary residence, making this a highly tax-efficient maneuver.

If you prefer to stay in your current home, a Home Equity Conversion Mortgage (HECM), commonly known as a reverse mortgage, allows you to convert equity into cash. You can receive this money as a line of credit, a lump sum, or fixed monthly payouts. While reverse mortgages carry upfront fees and interest, they do not require monthly repayments; the loan is settled when you sell the home, move out permanently, or pass away.

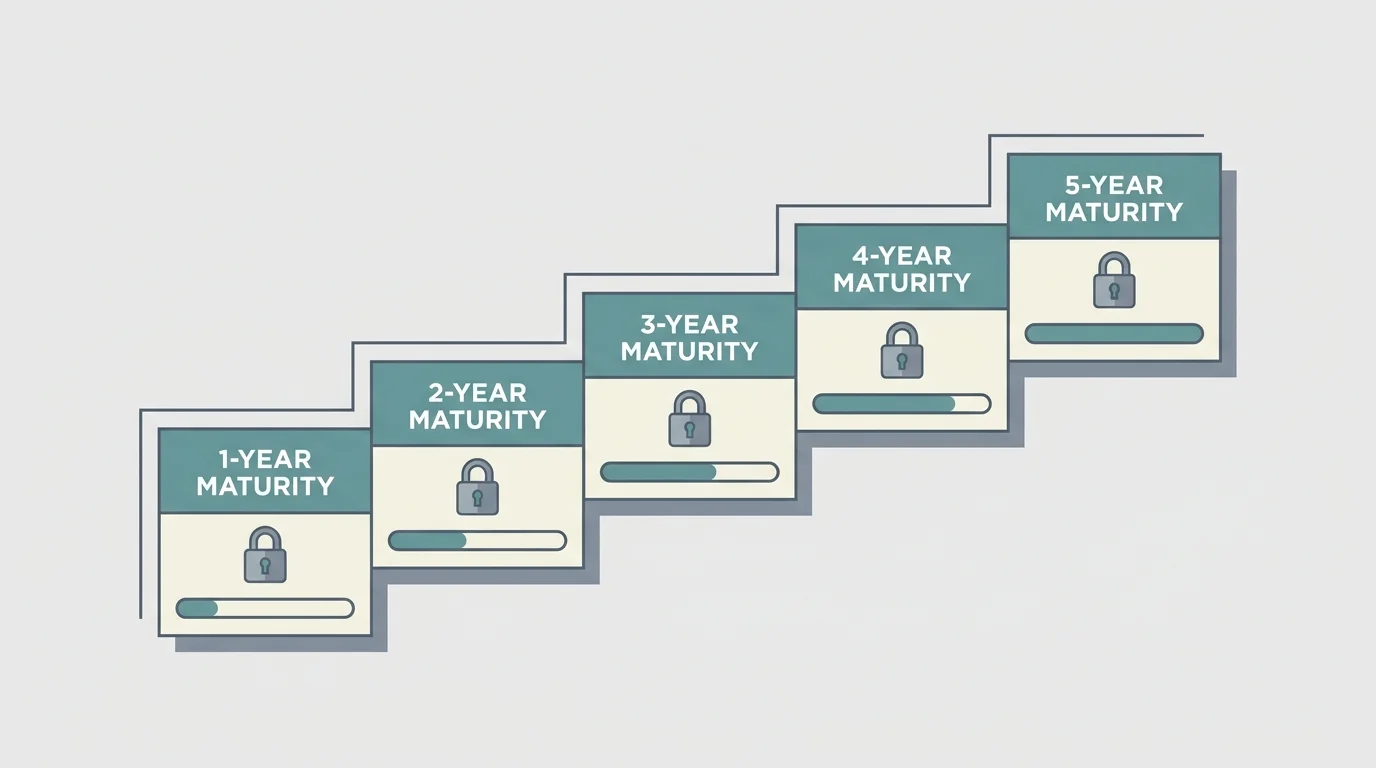

4. Construct a Certificate of Deposit (CD) or Treasury Ladder

When interest rates rise, conservative fixed-income vehicles become incredibly attractive tools for pension supplementation. Rather than locking all your cash into a single term, savvy retirees use a laddering strategy to balance higher yields with ongoing liquidity.

A CD ladder involves dividing your investment capital into equal tranches and purchasing certificates with staggered maturity dates. For example, if you have $50,000, you might place $10,000 each into a 1-year, 2-year, 3-year, 4-year, and 5-year CD. When the 1-year CD matures, you take the interest as supplemental income and reinvest the original $10,000 principal into a new 5-year CD. This continuous rotation ensures you have access to a portion of your cash every year while capturing the higher interest rates typically associated with longer-term deposits.

You can execute the exact same strategy using U.S. Treasury bills and notes. Treasuries are backed by the full faith and credit of the federal government, making them virtually risk-free if held to maturity. Moreover, interest earned on U.S. Treasuries is exempt from state and local taxes, offering a distinct advantage for retirees living in high-tax jurisdictions.

5. Pivot to High-Level Consulting

Leaving behind the daily grind does not mean you must abandon your professional expertise. Decades of industry knowledge hold immense value for businesses that need specialized guidance but cannot afford a full-time executive. Consulting allows you to monetize your intellectual capital on your own terms.

Because you have a pension covering your baseline needs, you possess the ultimate leverage: the ability to say no. You can choose to take on only the projects that genuinely interest you, working ten or fifteen hours a week. Establishing an hourly rate or project fee that reflects your senior-level experience means you can generate substantial supplemental income without committing to a burdensome schedule.

To begin, reach out to your former employer, past vendors, or industry competitors. Let your network know you are available for advisory roles, project management, or staff training. Setting up a simple Limited Liability Company (LLC) allows you to operate professionally and deduct legitimate business expenses—such as your home office, internet, and travel—further optimizing your tax situation.

6. Transform Hobbies into Micro-Businesses

Retirement affords you the time to deeply engage with passions you previously relegated to the weekends. Monetizing a hobby provides a deeply fulfilling way to generate extra cash because it rarely feels like work. The digital economy makes it easier than ever to reach an audience willing to pay for your specific skills or creations.

Consider how your specific interests translate into market value:

- Woodworking or Crafting: Creating custom furniture, birdhouses, or handmade jewelry to sell at local artisan markets or online platforms.

- Gardening: Cultivating specialty plants, propagating rare succulents, or selling organic produce at neighborhood farmers’ markets.

- Writing and Editing: Offering freelance proofreading services, starting a niche blog, or self-publishing specialized instructional guides.

- Photography: Selling landscape prints, offering portrait sessions for local families, or contributing images to stock photography websites.

Keep your expectations grounded; a hobby business may only generate a few hundred dollars a month initially. However, that supplemental cash can perfectly fund your continued participation in the hobby itself, creating a self-sustaining loop that enriches your retirement lifestyle without draining your pension.

7. Maximize Your Health Savings Account (HSA)

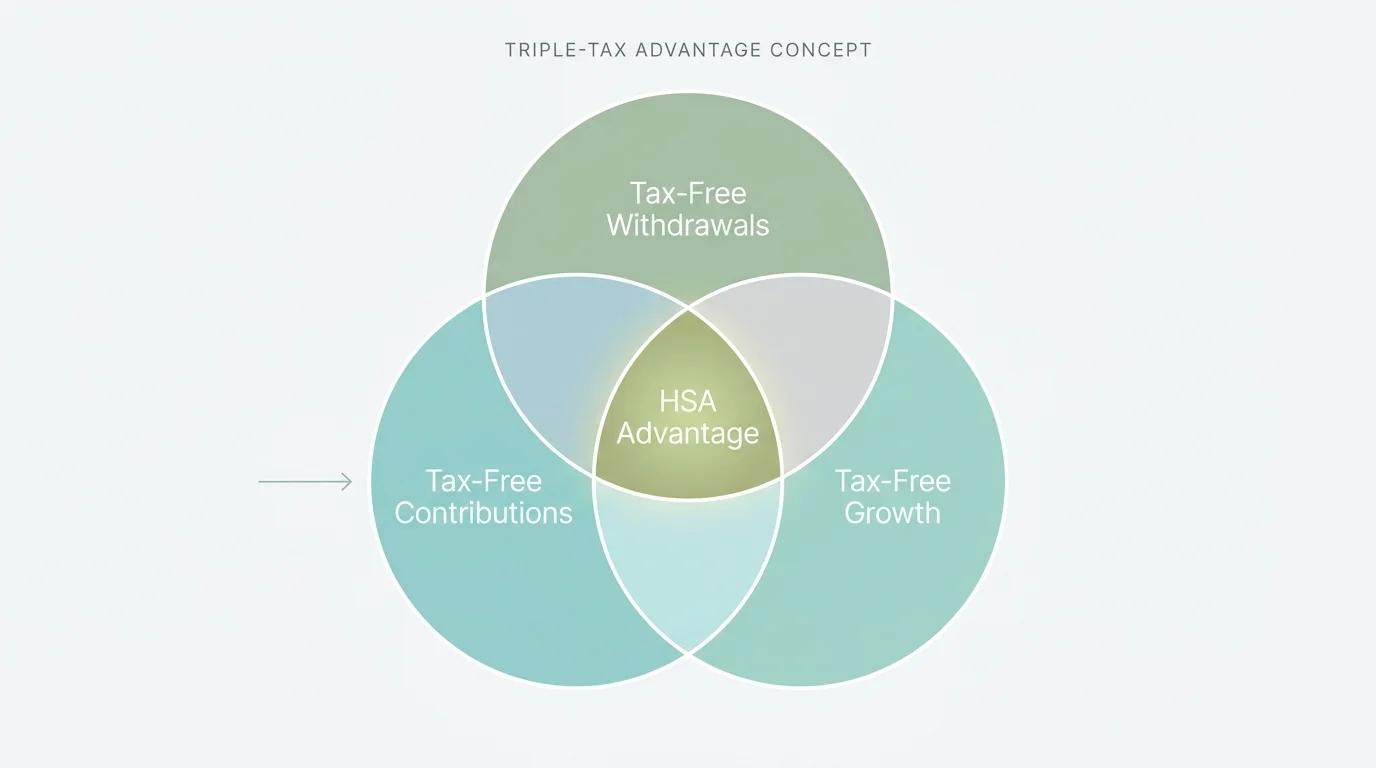

If you utilized a high-deductible health plan during your working years, you might have an HSA sitting in the background. While HSAs are designed to cover medical expenses, they transform into a powerful, stealth retirement account once you reach age 65.

An HSA offers a rare triple-tax advantage: contributions go in tax-free, the money grows tax-free, and withdrawals for qualified medical expenses are entirely tax-free. Considering that healthcare often stands as the highest variable expense in retirement, using HSA funds to cover Medicare premiums, copayments, and prescription costs directly preserves your pension income for other uses.

The true flexibility unlocks at age 65. At this milestone, the 20 percent penalty for non-medical withdrawals completely disappears. If you withdraw HSA funds to pay for a vacation, groceries, or a home renovation, you simply pay standard income tax on the distribution—exactly as you would with a Traditional IRA. For precise guidelines on qualified medical expenses and distribution rules, consult the official documentation provided by the Internal Revenue Service.

8. Purchase Fixed Annuities for Income Certainty

If your pension covers your housing and groceries, but you worry about outliving your assets or facing market downturns, an annuity can build an additional layer of guaranteed income. An annuity is a contract between you and an insurance company where you pay a premium in exchange for regular disbursements.

A Single Premium Immediate Annuity (SPIA) is the most straightforward option for retirees. You hand over a lump sum of cash, and the insurance company begins sending you a monthly check almost immediately, guaranteed for the rest of your life. This effectively allows you to create your own secondary pension.

While annuities provide incredible psychological comfort, they do require you to part with liquidity. Once you purchase an immediate annuity, you generally cannot access that lump sum for emergencies. Therefore, it is critical to purchase annuities only with a portion of your portfolio, leaving ample liquid cash in high-yield savings or brokerage accounts. Furthermore, ensure you select a highly rated insurance provider capable of honoring decades of payments.

9. Rent Out Tangible Assets

The sharing economy has evolved far beyond ride-sharing, offering retirees hands-off methods to generate cash from assets they already own but rarely use. If you have physical property sitting idle, you have untapped income potential.

Renting out extra space in your home or on your property serves as a prime example. If you live in a desirable location, converting a finished basement or an accessory dwelling unit into a short-term vacation rental can yield significant monthly returns. If hosting travelers sounds too intrusive, consider peer-to-peer storage platforms. You can rent out an empty garage bay, a portion of your driveway, or a clean basement to neighbors looking to store boats, RVs, or personal boxes.

Vehicle rentals offer another lucrative avenue. If you own an RV or camper that sits in your driveway for ten months out of the year, specialized rental platforms allow you to lease it out to vetted vacationers, fully covered by platform-provided insurance. Similarly, if your household operates with two cars but you only actively drive one, peer-to-peer car-sharing apps let you monetize the secondary vehicle.

10. Embrace an Encore Career

Sometimes the best way to supplement a pension is to find a completely new, low-stress job that provides both pocket money and deep personal satisfaction. An “encore career” refers to work taken on later in life that prioritizes meaning, community connection, and enjoyment over climbing the corporate ladder.

“Retirement is an artificial finish line. You need a purpose to wake up to, not just a portfolio to retire on.” — Mitch Anthony, Financial Behavior Expert

Working ten to twenty hours a week provides a structured routine and vital social interaction—elements many retirees miss after leaving their primary careers. Popular encore careers include working at local nurseries, taking on part-time roles at golf courses, substituting at local schools, or working front-desk roles at community centers. Nonprofits and museums frequently hire retirees for part-time administrative or coordinating roles, blending paid work with a sense of giving back to the community.

Beyond the paycheck, these roles often come with secondary perks. Working at a hardware store might yield a generous employee discount for your home renovation projects, while working at a state park provides free access to recreational facilities. The supplemental income reduces the pressure on your savings, allowing your investments more time to compound.

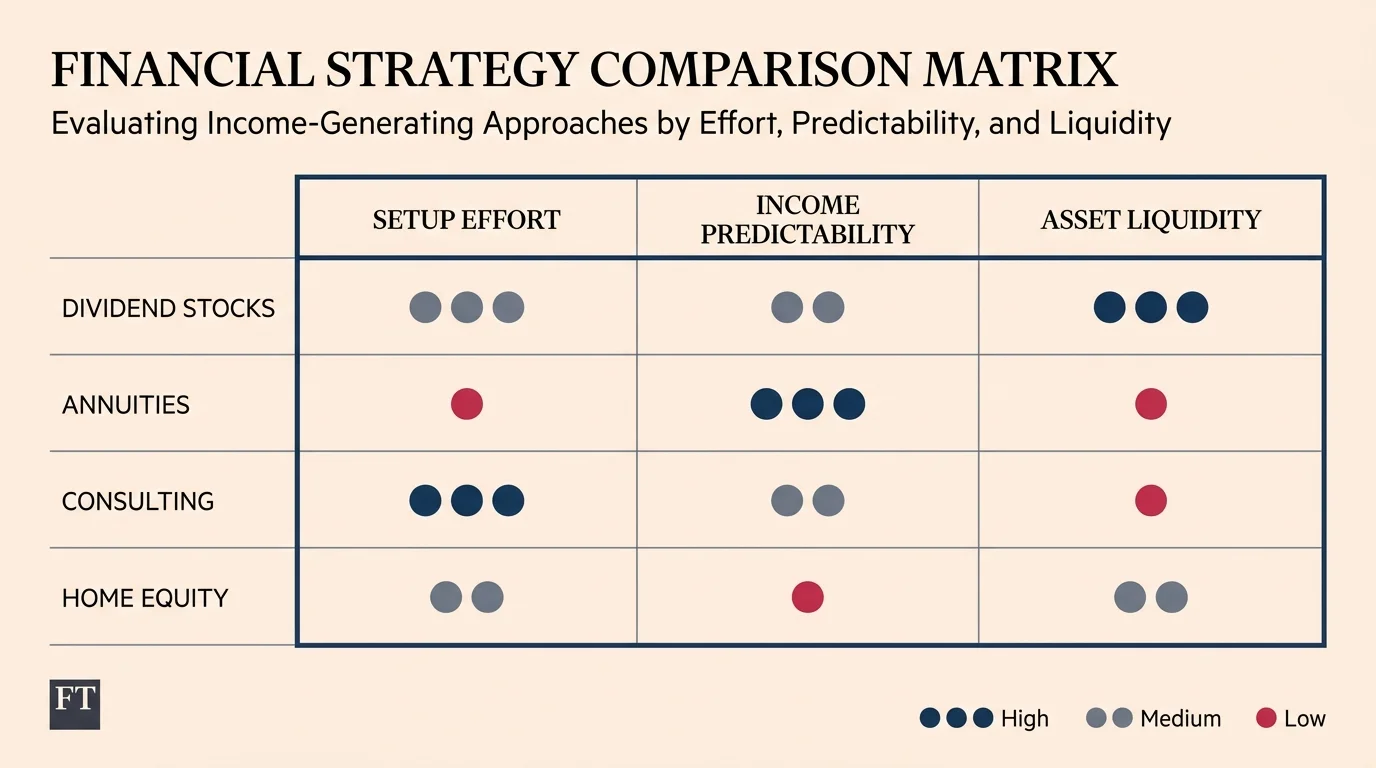

Comparing Your Income Options

Choosing the right supplemental income strategy requires balancing your need for cash against your tolerance for risk and your desire for free time. Use this table to conceptualize how different approaches align with your retirement lifestyle.

| Income Strategy | Time Commitment | Risk Level | Income Predictability |

|---|---|---|---|

| Social Security Delay | None | Zero | High (Guaranteed) |

| Dividend Portfolio | Low (Passive) | Moderate (Market reliant) | Moderate to High |

| CD / Treasury Ladders | Low (Setup required) | Very Low | High (Fixed rate) |

| Consulting / Freelancing | Moderate to High | Low | Variable |

| Fixed Annuities | None | Low (Insurance backed) | High (Guaranteed) |

| Renting Assets | Moderate | Low (Property risk) | Variable |

Avoiding Common Errors

Generating supplemental income requires careful navigation of the tax code and federal benefit rules. Earning extra money can occasionally trigger unintended consequences if you fail to plan appropriately.

First, be intensely aware of the Social Security earnings test. If you claim Social Security before your Full Retirement Age and continue to work (such as consulting or taking an encore career), the government will temporarily withhold a portion of your benefits if your earned income exceeds an annual threshold. While you eventually get this money back in the form of higher payments later, the immediate reduction can shock retirees relying on that specific cash flow.

Second, monitor your Medicare premiums. Medicare Part B and Part D premiums are tied to your Modified Adjusted Gross Income (MAGI). If your supplemental income—whether from large capital gains, Roth conversions, or a successful consulting business—pushes your MAGI over specific thresholds, you will be hit with an Income-Related Monthly Adjustment Amount (IRMAA). This surcharge can significantly increase your healthcare costs for the year.

Finally, avoid confusing yield with safety. Chasing exceptionally high dividend yields or complex alternative investments to generate cash often exposes your principal to extreme volatility. A company offering a massive dividend payout is frequently doing so because its stock price has plummeted, signaling underlying financial distress.

When DIY Isn’t Enough

While many of these strategies can be implemented independently, certain financial maneuvers require an expert’s oversight. A single mistake with tax planning or legal structuring can cost far more than a professional’s fee. Consider hiring a fiduciary advisor or a Certified Public Accountant (CPA) in the following scenarios:

- Executing Large Home Equity Transactions: If you are selling a highly appreciated primary residence or exploring a reverse mortgage, a professional can calculate the precise tax implications and evaluate the long-term impact on your estate.

- Navigating IRMAA and Tax Brackets: When structuring withdrawals from pre-tax accounts, taxable brokerages, and active income streams simultaneously, a CPA can help you optimize distributions to avoid massive tax bumps or Medicare surcharges.

- Purchasing Annuities: Annuity contracts are notoriously complex, laden with hidden fees, surrender charges, and riders. An independent, fee-only planner can evaluate the contract to ensure it genuinely serves your needs without enriching the salesperson at your expense.

- Setting Up a Small Business: If your hobby or consulting work begins generating significant revenue, you need professional guidance on forming an LLC, managing self-employment taxes, and potentially setting up a Solo 401(k) to shield income.

Frequently Asked Questions

Will earning extra money reduce my pension payments?

In the vast majority of cases, earning supplemental income through investments, part-time work, or a business will not impact your private or corporate pension. Your pension is based on your years of service and final salary with your former employer. However, if you receive a disability pension, specific earnings caps may apply. Always review your specific pension plan documents to verify.

Do I have to pay taxes on supplemental retirement income?

Yes, most forms of supplemental income are taxable. Wages from an encore career, consulting fees, rental income, and interest from CDs are generally taxed as ordinary income. Dividends and long-term capital gains often receive preferential, lower tax rates. It is crucial to set aside a portion of your active earnings for quarterly estimated tax payments to avoid penalties.

How much extra income does the average retiree need?

Financial planners typically suggest aiming to replace 70 to 80 percent of your pre-retirement income. If your pension and Social Security cover 60 percent, you need to generate the remaining 20 percent through the strategies listed above. However, the exact amount depends entirely on your location, health status, and lifestyle goals. Track your actual spending for six months to determine your true income gap.

Designing Your Financial Future

Securing a pension is a massive accomplishment that provides you with a baseline of financial security most modern workers will never experience. By viewing that pension not as a rigid boundary, but as a solid foundation, you free yourself to explore diverse, engaging ways to bring extra money into your household. Start small. You might begin by building a simple CD ladder this year, and eventually branch out into part-time consulting or monetizing a hobby next year. The goal is to create a dynamic financial ecosystem that supports a rich, worry-free retirement.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, health needs, tax situation, and goals—may require different approaches. When in doubt, consult a licensed professional to align these strategies with your personalized retirement roadmap.

Last updated: June 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply