Navigating the maze of Social Security rules determines whether you leave thousands of dollars on the table or secure the retirement you earned. The decisions you make about when to claim, how to handle taxes, and how benefits coordinate with a spouse are permanent choices that dictate your financial foundation for decades. As retirement approaches, complex scenarios emerge regarding working while claiming, maximizing survivor benefits, and understanding Medicare deductions. This guide strips away the bureaucratic jargon to answer the specific, high-stakes questions retirees constantly face. By understanding the mechanics behind the math, you position yourself to optimize your monthly checks, avoid irreversible claiming mistakes, and build a resilient retirement income strategy.

How Does the Timing of My Claim Affect My Monthly Check?

The single most important decision you make regarding Social Security is when to file your claim. The Social Security Administration anchors all calculations to your Full Retirement Age (FRA). Depending on your birth year, your FRA falls somewhere between 66 and 67. Claiming before or after this specific milestone alters your monthly payout permanently.

If you claim benefits as early as possible—age 62—your monthly check faces a severe reduction. For those with a Full Retirement Age of 67, claiming at 62 results in a permanent 30% cut to the base benefit amount. This reduction accounts for the fact that you will receive checks for a longer period over your lifetime.

Conversely, delaying your claim past your FRA triggers delayed retirement credits. For every year you wait between your FRA and age 70, your benefit increases by a guaranteed 8%. This is one of the most powerful risk-free returns available in the financial world. Once you reach age 70, these credits stop accumulating, making it the absolute latest you should ever file.

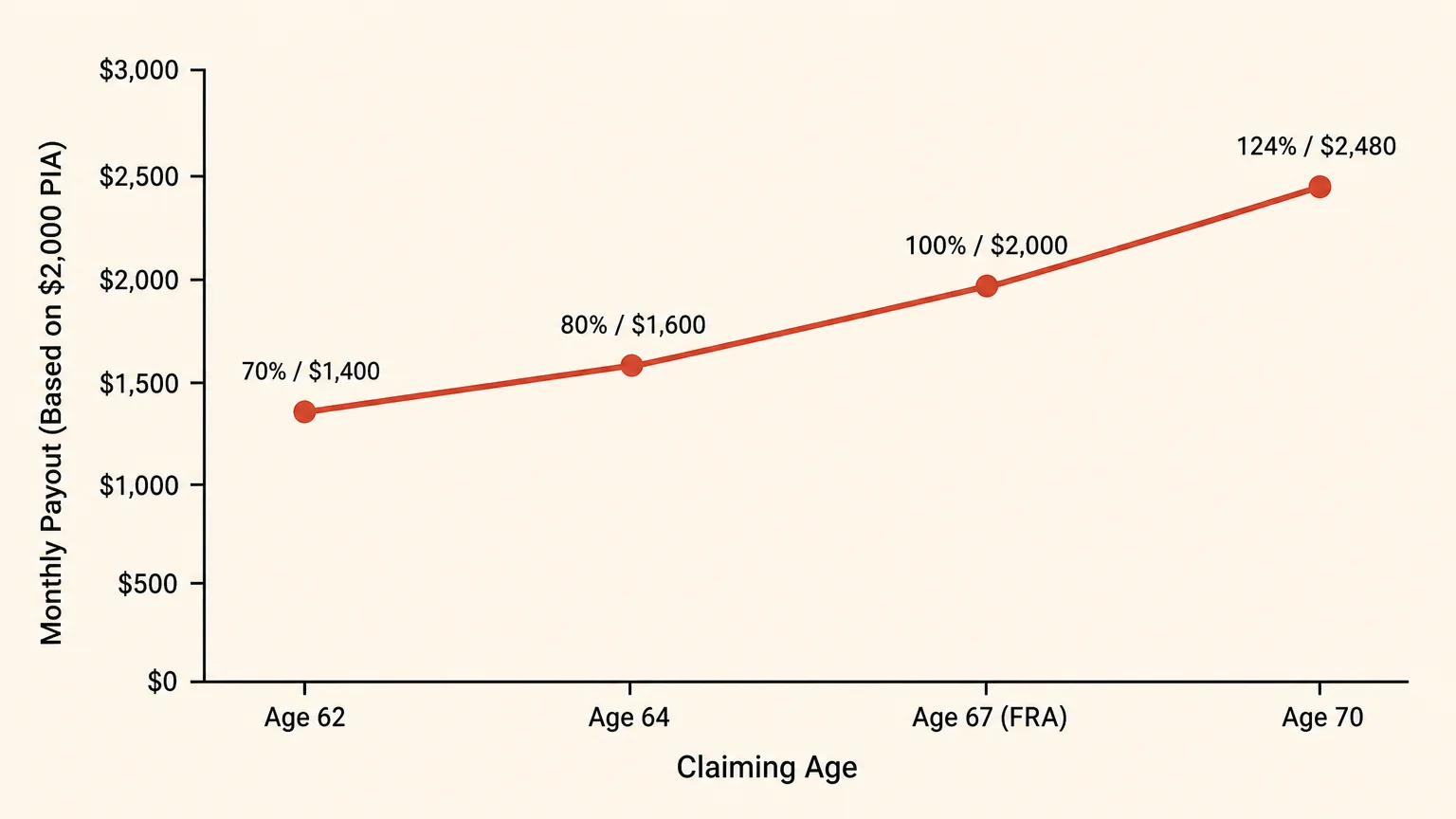

Consider a hypothetical retiree with a Full Retirement Age of 67 and a base benefit (Primary Insurance Amount) of $2,000 per month. The table below illustrates how drastically timing alters the payout.

| Claiming Age | Percentage of Base Benefit | Monthly Payout (Based on $2,000 PIA) |

|---|---|---|

| Age 62 (Earliest) | 70% | $1,400 |

| Age 64 | 80% | $1,600 |

| Age 67 (FRA) | 100% | $2,000 |

| Age 70 (Maximum) | 124% | $2,480 |

Choosing when to claim requires a detailed break-even analysis. A break-even calculation compares the lower amount received earlier versus the higher amount received later to determine the age at which the total lifetime payouts equalize. Typically, if you live past your early 80s, delaying until age 70 provides the greatest lifetime payout. However, single individuals in poor health might find that claiming at 62 makes the most mathematical sense.

Can I Work While Receiving Social Security Benefits?

Many retirees envision a gradual transition into retirement, choosing to work part-time while collecting Social Security. You absolutely can work and receive benefits simultaneously, but doing so before you reach your Full Retirement Age triggers the Retirement Earnings Test (RET).

The RET temporarily withholds a portion of your Social Security checks if your earned income exceeds a specific annual limit set by the government. The rules change depending on how close you are to your FRA:

- Years prior to FRA: If you are under your FRA for the entire calendar year, the government deducts $1 from your benefit payments for every $2 you earn above the annual limit.

- The year you reach FRA: In the months leading up to your birthday, the limit is significantly higher, and the penalty is reduced. The government deducts $1 for every $3 you earn above this higher threshold.

- After reaching FRA: The earnings test disappears completely. You can earn a million dollars a year, and your Social Security check will not be reduced by a single cent.

It is crucial to understand that the earnings test only applies to earned income—meaning W-2 wages or net earnings from self-employment. Passive income streams do not count. Pensions, annuities, investment dividends, interest, and capital gains have zero impact on the Retirement Earnings Test.

Furthermore, money withheld by the RET is not lost forever. Once you reach your Full Retirement Age, the Social Security Administration recalculates your benefit upward to account for the months your checks were partially or fully withheld. You eventually get the money back in the form of a higher monthly check for the rest of your life.

How Do Spousal Benefits Actually Work?

Social Security includes provisions to protect spouses who stayed home to raise children or earned significantly less than their partners over their lifetimes. A spousal benefit allows you to claim up to 50% of your partner’s primary insurance amount (their benefit at FRA), rather than relying solely on your own work record.

The mechanics of spousal benefits confuse many planners. The government uses a concept called “dual entitlement.” When you file for benefits, the Social Security Administration first calculates the benefit based on your own work history. If your personal benefit is higher than the spousal benefit, you receive your own money. If the spousal benefit is higher, the government pays your benefit first, then adds a supplemental amount to bring your total check up to the spousal maximum.

To receive the full 50% spousal benefit, you must wait until your own Full Retirement Age to file. If you claim a spousal benefit early—say, at age 62—that 50% maximum is reduced to as little as 32.5%. Additionally, you cannot claim a spousal benefit until your partner has officially filed for their own retirement benefits.

These rules extend to divorced spouses as well. If your marriage lasted for at least 10 consecutive years and you are currently unmarried, you can claim a benefit based on your ex-spouse’s earnings record. Crucially, claiming on an ex-spouse’s record does not impact their benefit, nor does it impact the benefit of their current spouse. They will not even be notified that you filed the claim.

What Happens to Benefits When a Spouse Passes Away?

The death of a spouse is emotionally devastating, and the financial transition requires careful navigation. Social Security survivor benefits differ entirely from spousal benefits and serve as a vital safety net for widows and widowers.

When one spouse passes away, the household loses one of its Social Security checks. The surviving spouse keeps the higher of the two benefits that were coming into the household, and the smaller benefit disappears forever. This makes the primary earner’s claiming strategy incredibly important. If the higher earner delays their claim to age 70, they not only increase their own lifetime income, but they also leave behind a significantly larger survivor benefit for their spouse.

Survivor benefits have unique timing rules that provide strategic flexibility. Unlike retirement benefits, survivor benefits can be claimed as early as age 60 (or age 50 if the survivor has a qualifying disability). Furthermore, survivors have the option to decouple their benefits. You can claim a reduced survivor benefit early while allowing your own personal retirement benefit to grow until age 70, at which point you switch to your own higher amount.

“When it comes to Social Security, the most critical mistake people make is letting fear dictate their claiming strategy rather than relying on the math. Delaying benefits is often the best insurance policy against outliving your money.” — Suze Orman, Personal Finance Expert

Will My Social Security Benefits Be Taxed?

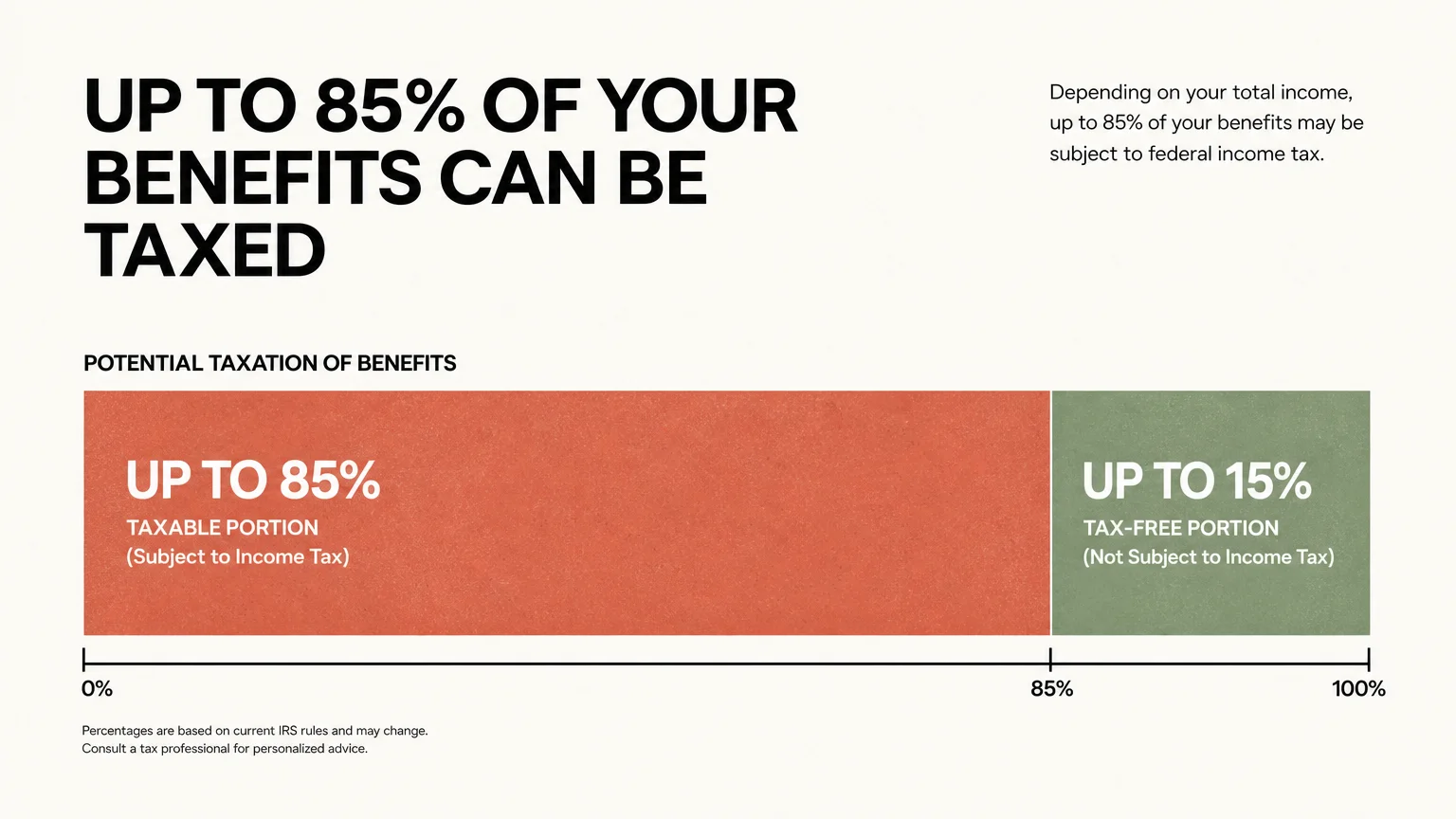

A common and unpleasant surprise for new retirees is discovering that the Internal Revenue Service taxes Social Security benefits. Whether or not you pay taxes on your checks depends on a specific calculation known as “combined income” (sometimes called provisional income).

Your combined income is calculated using a strict formula: Adjusted Gross Income (AGI) + Nontaxable Interest + 50% of your Social Security benefits.

Once you calculate this number, the IRS measures it against static thresholds that were established decades ago and have never been indexed for inflation. As a result, more retirees fall into these tax brackets every year.

- Individual Filers: If your combined income is between $25,000 and $34,000, up to 50% of your benefits may be taxable. If it exceeds $34,000, up to 85% of your benefits become taxable.

- Married Filing Jointly: If your combined income is between $32,000 and $44,000, up to 50% of your benefits are taxable. If it exceeds $44,000, up to 85% of your benefits are taxable.

It is critical to note that “85% taxable” does not mean you pay an 85% tax rate. It simply means that 85% of your benefit amount is added to your total taxable income and taxed at your ordinary marginal income tax rate.

Managing these taxes requires proactive strategy. Retirees often utilize Roth IRAs, which provide tax-free withdrawals that do not count toward the combined income calculation. Executing Roth conversions before filing for Social Security can permanently lower your combined income in later years, protecting your benefits from federal taxation.

How Does Medicare Tie Into My Social Security Check?

Social Security and Medicare operate as distinct programs, but they are financially intertwined. If you are already collecting Social Security when you turn 65, you will be automatically enrolled in Medicare Parts A and B. If you delay Social Security past age 65, you must manually enroll in Medicare to avoid permanent late penalties.

Once you are enrolled in both programs, the government requires your Medicare Part B premiums to be deducted directly from your Social Security checks. You will not receive a separate bill; your monthly Social Security deposit will simply be reduced by the cost of your healthcare premium.

This deduction introduces two complex rules every retiree must understand:

The Hold Harmless Provision: By law, a Medicare Part B premium increase cannot reduce the net amount of your Social Security check from one year to the next. If the annual Cost of Living Adjustment (COLA) for Social Security is very low, but Medicare premiums rise sharply, the government caps the premium increase so your check does not shrink. However, this protection only applies if you have your premiums deducted directly from your benefit check.

IRMAA (Income-Related Monthly Adjustment Amount): If you have a high income in retirement, you will pay a surcharge on your Medicare Part B and Part D premiums. The government looks at your tax return from two years prior to determine your IRMAA bracket. A large one-time financial event—such as selling a business or executing a massive Roth conversion at age 63—can artificially inflate your income and trigger massive Medicare surcharges when you turn 65.

Does a Pension Affect My Social Security?

If you worked in the private sector and earned a traditional pension, it will not affect your Social Security. However, if you worked a government job where you did not pay Social Security payroll taxes (such as teaching in certain states, working for the postal service, or serving as a municipal firefighter), two obscure provisions can drastically reduce your benefits.

The Windfall Elimination Provision (WEP): The WEP impacts how your personal retirement benefit is calculated. The Social Security formula is designed to replace a higher percentage of income for low-wage workers. If you have a pension from “non-covered” employment, the WEP alters the formula, assuming your missing Social Security earnings years were due to high-paying government work rather than low-wage labor. This can reduce your base benefit by roughly half, up to a specific statutory maximum.

The Government Pension Offset (GPO): The GPO is far more punitive, as it targets spousal and survivor benefits. Under the GPO, your spousal or survivor benefit is reduced by two-thirds of the amount of your non-covered government pension. For example, if you receive a $3,000 monthly teacher’s pension from a state that does not participate in Social Security, the GPO deducts $2,000 from any spousal or survivor benefit you might claim. In many cases, the GPO completely wipes out spousal and survivor benefits.

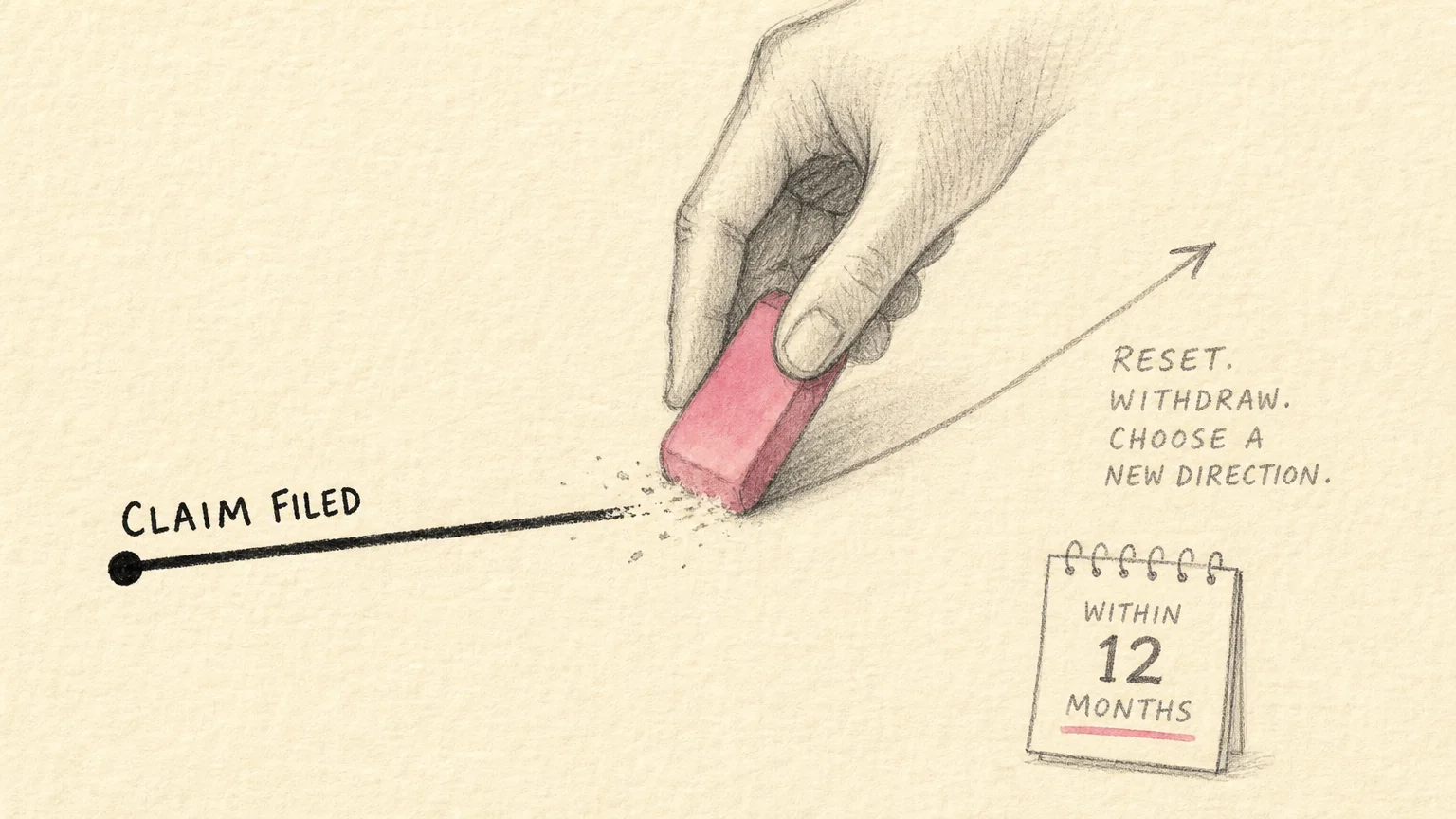

What if I Make a Mistake? Can I Undo My Claim?

Retirement planning happens in the real world, where unexpected events occur. You might claim early, only to be offered an incredible consulting contract a few months later. You might file at 62, suddenly inherit a significant sum of money, and wish you had delayed to maximize your checks.

The government provides a one-time “do-over” option. If you change your mind within 12 months of claiming benefits, you can file SSA Form 521 to withdraw your application. The catch? You must repay every single penny that you and your family members received based on your record, including any Medicare premiums that were deducted from your checks. Once you repay the funds, it is as if you never filed, allowing your future benefits to grow with delayed retirement credits.

If you pass the 12-month window, you cannot withdraw your claim. However, you gain another option once you reach your Full Retirement Age. At FRA, you can voluntarily suspend your benefits. This stops your monthly checks temporarily, allowing your benefit to earn the 8% delayed retirement credits until age 70. This strategy is highly effective for retirees who filed early out of necessity but subsequently improved their financial standing.

Will Social Security Run Out Before I Die?

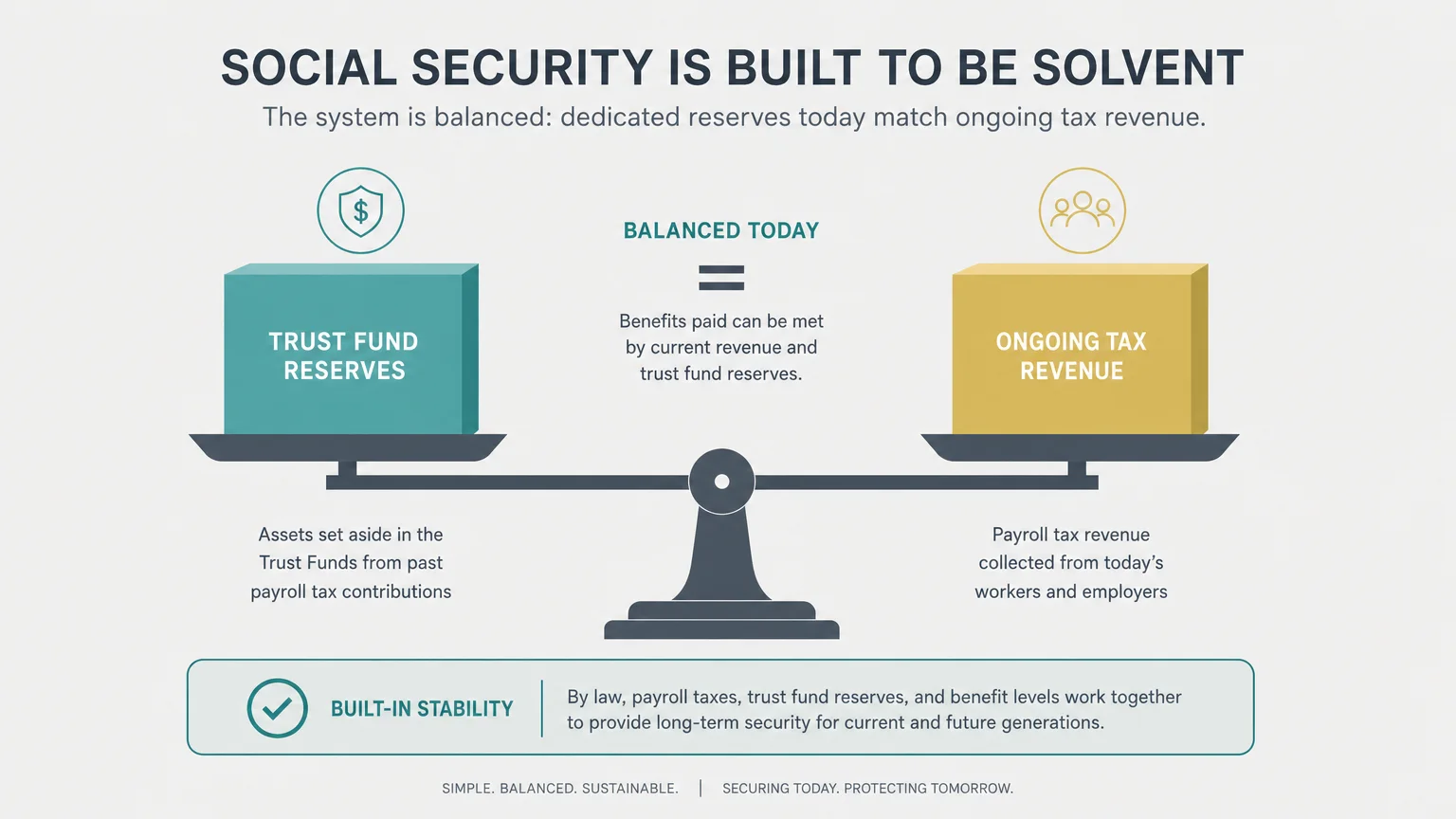

Every year, headlines proclaim that Social Security is going bankrupt. These alarmist statements cause massive anxiety and drive retirees to claim benefits at 62 out of sheer panic, permanently damaging their lifetime income. Understanding how the trust funds operate dispels this fear.

Social Security is funded through payroll taxes. As long as Americans are working and paying taxes, money enters the system. Currently, the system pays out more to retirees than it takes in from workers. To cover the shortfall, the Social Security Administration draws from the Old-Age and Survivors Insurance (OASI) Trust Fund—a massive reserve built up over decades of surplus.

According to the annual Trustees Report, this surplus trust fund will likely be depleted in the mid-2030s. Depletion does not mean bankruptcy. It simply means the reserve account is empty. If Congress takes absolutely no action to reform the system before that date, the ongoing payroll taxes collected from active workers would still cover roughly 75% to 80% of promised benefits.

History suggests that Congress will act before a 20% benefit cut occurs, as older Americans represent the most reliable voting demographic in the country. Solutions range from increasing the FRA, raising the cap on wages subject to payroll taxes, tweaking the inflation calculation, or increasing the payroll tax rate. Basing a lifelong financial decision on the fear of a system collapse almost always results in a mathematically poor outcome.

Pitfalls to Watch For

Even with access to accurate information, retirees frequently stumble into irreversible traps. Be hyper-vigilant regarding these common mistakes:

- Ignoring Life Expectancy: Many individuals calculate their break-even point using an average life expectancy of 78. If you reach age 65 in good health, your statistical likelihood of living into your late 80s or 90s is incredibly high. Claiming early under the assumption that you will pass away young leaves you vulnerable to extreme poverty in your final decades.

- Failing to Coordinate with a Spouse: Married couples often view their claiming strategies in isolation. The lower-earning spouse might file at 62, while the higher-earning spouse files at 64. This lack of coordination destroys survivor benefits. The highest earner in a household should exhaust every other financial asset before claiming Social Security, ensuring the maximum possible check is passed on to the surviving spouse.

- Misunderstanding the Earnings Test: Continuing to work while claiming benefits at age 62 without understanding the Retirement Earnings Test leads to massive cash flow disruptions. Retirees often spend their initial checks, only to receive a letter from the SSA demanding thousands of dollars in repayment because they exceeded the earned income limits.

- Forgetting About Taxation: Failing to plan for the “tax torpedo” caused by combined income thresholds can severely impact your net cash flow. Pulling heavily from traditional 401(k)s while receiving Social Security can force up to 85% of your benefits into taxable status, drastically shrinking your usable income.

Getting Expert Help

While the basic rules of Social Security are accessible, certain scenarios introduce mathematical complexities that demand professional analysis. You should consult a fee-only fiduciary financial planner or a certified Social Security claiming expert if you fall into any of these categories:

You have a complex marital history. If you have been married multiple times, divorced, or widowed, the rules regarding dual entitlement, survivor benefits, and ex-spouse records become incredibly intricate. A professional can identify which specific record yields the highest lifetime payout.

You are a business owner controlling your income. If you own a business, you have leverage over how much W-2 income you draw versus how much you retain in the company or take as distributions. An advisor can structure your compensation to respect the Retirement Earnings Test and minimize IRMAA surcharges.

You are subject to the WEP or GPO. The calculations surrounding non-covered pensions are notoriously difficult to predict. Software utilized by financial planners can precisely project how your government pension will erode your Social Security benefits, allowing you to plan your cash flow accurately.

You have massive pre-tax retirement accounts. If you hold millions in traditional IRAs or 401(k)s, Required Minimum Distributions (RMDs) will eventually force you into high tax brackets, pushing 85% of your Social Security into taxable status and triggering top-tier Medicare surcharges. An expert can design a multi-year Roth conversion strategy to mitigate this damage before you begin claiming benefits.

Frequently Asked Questions

Are Social Security benefits adjusted for inflation?

Yes. Every October, the government announces the Cost of Living Adjustment (COLA) for the upcoming year. This adjustment is based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). When inflation rises, your monthly benefit increases to help preserve your purchasing power. Even if you delay claiming until age 70, the COLAs announced during your 60s are automatically added to your base calculation.

Can I collect my benefits if I move out of the United States?

In most cases, yes. If you are a United States citizen, you can receive your Social Security payments in nearly any country in the world. The SSA will deposit funds directly into an international bank account or a U.S. bank account. However, there are a handful of countries (such as Cuba and North Korea) where the United States Treasury prohibits sending payments. If you move to one of these restricted nations, your benefits are held until you move to a permissible location.

Will my dependent children receive benefits when I retire?

If you claim your retirement benefits and have unmarried children under the age of 18 (or up to age 19 if they are still attending high school full-time), they can receive a dependent benefit. This payment can be up to 50% of your full retirement benefit. Children who were disabled before the age of 22 can also receive this benefit indefinitely. However, there is a strict Family Maximum Benefit limit that caps the total amount your household can receive on a single earnings record.

How does the government calculate my initial benefit amount?

The SSA looks at your entire lifetime of earnings and indexes your past wages for inflation to bring them up to modern values. They then select your 35 highest-earning years. If you worked fewer than 35 years, the missing years are entered as zeros. The average of those 35 indexed years becomes your Average Indexed Monthly Earnings (AIME). The government then applies a progressive formula containing distinct “bend points” to determine your primary benefit amount, designed to replace a higher percentage of income for lower-wage earners.

Mastering Social Security requires stepping back from the fear of changing regulations and focusing on the concrete math of your unique situation. Whether you are coordinating with a spouse, managing taxation, or deciding the exact month to file, your objective is to build an income floor that protects you against outliving your assets. Take the time to run the calculations, review your annual statements from the SSA, and integrate your claiming strategy with your broader investment portfolio.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, health needs, tax situation, and goals—may require different approaches. When in doubt, consult a licensed professional.

Last updated: March 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply