As inflation metrics shift through the first half of 2026, the trajectory of your 2027 Social Security Cost of Living Adjustment (COLA) is already coming into focus. The Consumer Price Index numbers reported over the coming months will directly determine how much your monthly benefits increase next year. While the official announcement will not arrive until October, current economic data suggests retirees should prepare for a potentially different adjustment compared to recent years. Understanding how these numbers work allows you to adjust your household budget proactively. Tracking this data now gives you a crucial head start on managing your fixed income, ensuring your purchasing power remains protected against the rising costs of healthcare, housing, and everyday necessities.

At a Glance: The 2027 COLA Timeline

Before diving into the complexities of inflation data and tax brackets, it helps to understand exactly when and how the Social Security Administration (SSA) makes its decisions. The 2027 COLA is not based on inflation for the entire calendar year. Instead, it relies on a highly specific window of time.

- July 2026: The crucial third-quarter measurement period begins. The inflation data for this month represents the first piece of the 2027 COLA puzzle.

- August 2026: The second month of the measurement period. Economists and advocacy groups begin releasing highly accurate projections based on the emerging trend.

- September 2026: The final month of the measurement period. This data point locks in the average index required for the calculation.

- October 2026: The SSA officially announces the 2027 COLA percentage. Shortly after, the Centers for Medicare & Medicaid Services (CMS) typically announces the upcoming Medicare Part B premiums.

- December 2026: You will receive a personalized notice from the SSA detailing your exact new benefit amount, net of any Medicare deductions.

- January 2027: Your first payment reflecting the new 2027 COLA is deposited into your bank account.

How the CPI Dictates Your Social Security COLA

When news outlets discuss inflation, they usually reference the Consumer Price Index for All Urban Consumers (CPI-U). However, the Social Security Administration uses a different metric: the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). Understanding the distinction is vital for recognizing why your benefit increase might feel out of sync with your actual living expenses.

The CPI-W tracks the monthly change in prices paid by households that derive more than half their income from clerical or wage occupations. The Bureau of Labor Statistics (BLS) collects price data on a “basket of goods and services” that includes food, housing, apparel, transportation, medical care, recreation, and education. To calculate the annual COLA, the SSA takes the average CPI-W reading from the third quarter (July, August, and September) of the current year and compares it to the average CPI-W from the third quarter of the last year a COLA was triggered.

If the current year’s third-quarter average is higher, the percentage difference becomes the COLA for the following year. If prices have dropped and the average is lower, Social Security benefits remain flat; they are never reduced due to deflation. You can review the exact mathematical history of these adjustments directly through the Social Security Administration.

The Gap Between Official Inflation and Retiree Reality

A growing point of friction for retirees is the disconnect between the CPI-W and the realities of a senior citizen’s budget. Because the CPI-W measures the spending habits of working-age Americans, it heavily weights categories like transportation to work, apparel, and education. It places less emphasis on healthcare and housing—the two areas where retirees spend the overwhelming majority of their income.

This structural mismatch means that even when the CPI-W generates a seemingly healthy COLA, it often fails to cover the surging costs of prescription drugs, supplemental insurance premiums, and property taxes. For years, advocates have lobbied Congress to switch the COLA calculation to the Consumer Price Index for the Elderly (CPI-E), an experimental index maintained by the BLS that specifically tracks the spending habits of Americans aged 62 and older. The CPI-E typically shows a higher inflation rate than the CPI-W precisely because it gives more weight to medical care and housing.

“Arithmetic makes it plain that inflation is a far more devastating tax than anything that has been enacted by our legislatures. The inflation tax has a fantastic ability to simply consume capital.” — Warren Buffett, Investor and Philanthropist

Until a legislative change occurs, you must operate within the confines of the CPI-W. This makes proactive financial planning essential, as you cannot rely solely on the annual COLA to maintain your standard of living.

Why the Latest 2026 Inflation Numbers Matter Now

As we navigate the middle of 2026, the specific inflation categories driving the economy are uniquely impactful for retirees. While broad inflation may show signs of cooling compared to the historic spikes seen in 2022 and 2023, “core inflation”—which excludes volatile food and energy sectors—often remains stubbornly entrenched in areas that disproportionately affect older adults.

For example, property insurance and auto insurance rates have seen significant upward pressure, directly impacting the fixed costs of homeownership and driving. Medical services and prescription drug costs also continue to outpace general inflation. If the CPI-W data in July, August, and September is pulled downward by falling gasoline prices or cheaper consumer electronics, the resulting 2027 COLA could be modest. However, a modest COLA provides little comfort if your personal expenses—driven by insurance and healthcare—are rising at a much faster pace.

Historical Context: Comparing Recent COLA Trends

To understand the significance of the upcoming 2027 COLA, it is helpful to look at how inflation has shaped benefits over recent years. The economic volatility of the 2020s has resulted in some of the most dramatic adjustments in the history of the Social Security program.

| Year (Effective Jan) | COLA Percentage | Economic Context |

|---|---|---|

| 2021 | 1.3% | Historically low inflation during the height of pandemic lockdowns. |

| 2022 | 5.9% | The highest increase in decades as post-pandemic demand outpaced supply. |

| 2023 | 8.7% | A historic 40-year high adjustment driven by energy and food costs. |

| 2024 | 3.2% | Inflation began cooling, though cumulative price levels remained high. |

| 2025 | 2.5% | A return to more normalized, historical average adjustments. |

| 2026 | 2.8% | Persistent service-sector inflation keeping the adjustment steady. |

This table illustrates the pendulum swing of inflation. Retirees who anchored their expectations to the massive 8.7% bump in 2023 quickly learned that as inflation normalizes, COLAs shrink back to the 2% to 3% range. If the CPI data for late 2026 remains moderate, you should plan for a 2027 COLA that aligns closer to historical averages rather than pandemic-era extremes.

The Medicare Part B Premium Interaction

You cannot discuss the Social Security COLA without examining Medicare Part B premiums. For the vast majority of beneficiaries, Medicare Part B premiums are deducted directly from their Social Security checks. Because of this interaction, your “gross” COLA increase is rarely the amount that actually lands in your bank account.

Each year, CMS evaluates the projected costs of the Medicare program and sets the standard Part B premium. If the dollar amount of your Part B premium increase is larger than the dollar amount of your Social Security COLA, a special rule known as the “hold harmless” provision kicks in. This rule ensures that your net Social Security check will not decrease from one year to the next due to a standard Part B premium hike.

However, the hold harmless provision does not apply to everyone. It does not protect you if you are new to Medicare, if you do not have your premiums deducted from Social Security, or if you are subject to the Income-Related Monthly Adjustment Amount (IRMAA). To understand how your specific premiums are calculated, you can utilize the resources available at Medicare.gov.

The Stealth Tax: How COLA Increases Impact Your Tax Bracket

One of the most frustrating aspects of a higher COLA is its potential to push you into a higher tax bracket. This phenomenon is often referred to as a “stealth tax” on retirees. Up to 85% of your Social Security benefits can be subject to federal income taxes, depending on your “provisional income.”

The Internal Revenue Service calculates your provisional income by combining your Adjusted Gross Income (AGI), any nontaxable interest (such as municipal bond interest), and half of your Social Security benefits. The thresholds for taxing benefits are remarkably low and, crucially, they are not indexed to inflation:

- Individual Filers: If your provisional income is between $25,000 and $34,000, up to 50% of your benefits may be taxable. If it exceeds $34,000, up to 85% may be taxable.

- Joint Filers: If your provisional income is between $32,000 and $44,000, up to 50% of your benefits may be taxable. If it exceeds $44,000, up to 85% may be taxable.

Because these thresholds were established in the 1980s and 1990s and have never been updated for inflation, every time you receive a COLA, your provisional income rises. A modest 2027 COLA could be the exact amount that pushes your income over the $34,000 or $44,000 threshold, resulting in a larger portion of your benefits becoming subject to federal taxes. You can verify the latest tax brackets and rules regarding retirement income on the Internal Revenue Service website.

The IRMAA Effect: Delayed Consequences of Higher Income

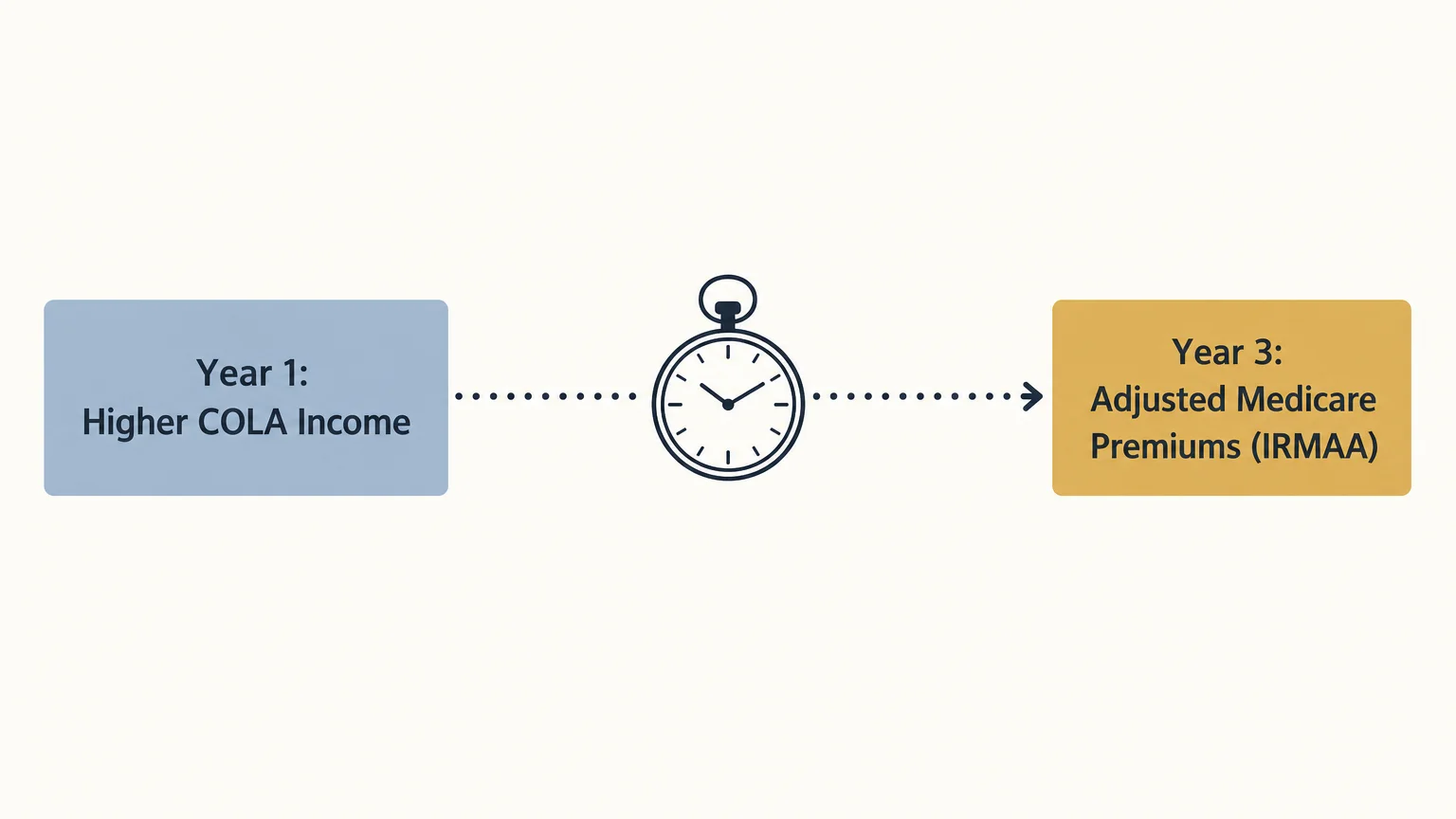

The tax implications of a higher COLA do not stop at standard income taxes. If you rely on taxable withdrawals from traditional IRAs or 401(k)s to supplement your Social Security, you must carefully monitor your Modified Adjusted Gross Income (MAGI) to avoid triggering IRMAA surcharges.

IRMAA is a surcharge added to your Medicare Part B and Part D premiums if your income exceeds certain thresholds. What makes IRMAA particularly tricky is the two-year lookback period. Your 2027 Medicare premiums are based on your 2025 tax return. If a previous COLA combined with Required Minimum Distributions (RMDs) artificially inflated your income, you might face significantly higher Medicare costs down the road. Managing this requires precise tax planning, often involving strategies like Qualified Charitable Distributions (QCDs) or Roth conversions to keep your taxable income below the IRMAA cliffs.

What Can Go Wrong: Relying Too Heavily on COLA Estimates

Financial planning requires precision, but banking on early COLA estimates can introduce risk into your retirement strategy. Here are the most common pitfalls retirees face when anticipating their adjustment:

- Spending the Increase Before It Arrives: Hearing news about high inflation in early 2026 might tempt you to loosen your budget in anticipation of a big 2027 bump. However, if third-quarter inflation cools unexpectedly, the actual COLA will be lower than summer estimates, leaving you with a budget shortfall.

- Ignoring Localized Inflation: The CPI-W is a national average. If you live in a rapidly growing area with skyrocketing property taxes, or a rural area with high utility and transportation costs, your personal inflation rate may far exceed the national COLA. Relying solely on Social Security to bridge this localized gap will slowly erode your wealth.

- Forgetting the Net vs. Gross Difference: Never base your budgeting on the gross percentage announced in October. Until you receive your December notice showing your net benefit after Medicare deductions, you do not truly know how much your monthly cash flow will improve.

Actionable Steps to Protect Your Purchasing Power

Rather than waiting passively for the SSA to announce the 2027 COLA, you can take concrete steps today to fortify your retirement income against inflation.

Calculate Your Personal Inflation Rate

Track your spending meticulously for three months. Categorize your expenses into essential fixed costs (housing, groceries, healthcare, insurance) and discretionary costs (travel, dining, entertainment). Compare your year-over-year spending in these categories. Understanding your personal inflation rate allows you to see exactly how much extra income you need to generate, regardless of what the official CPI-W dictates.

Optimize Your Cash Buffer

Maintaining a healthy cash reserve prevents you from having to sell investments at a loss during market downturns. Ensure you have 12 to 18 months of living expenses held in high-yield savings accounts, Certificates of Deposit (CDs), or money market funds. As interest rates fluctuate, proactively seek out the best yields to ensure your idle cash is at least partially keeping pace with inflation.

Review Your Investment Allocation

Social Security provides a baseline of inflation-protected income, but your investment portfolio must carry the rest of the weight. Consider allocating a portion of your portfolio to assets that historically weather inflation well, such as dividend-paying stocks or Treasury Inflation-Protected Securities (TIPS). You can learn more about how TIPS and other fixed-income instruments work through educational resources provided by Investor.gov.

Max Out Medicare Open Enrollment

Because healthcare inflation outpaces general inflation, your annual Medicare Open Enrollment period (October 15 through December 7) is one of your best financial defense mechanisms. Do not allow your Part D prescription drug plan or Medicare Advantage plan to auto-renew without reviewing the upcoming year’s formulary and copays. Switching to a more cost-effective plan can easily save you more money than the entire value of your annual COLA.

When to Consult a Professional

While many retirees manage their finances independently, specific situations related to inflation, taxes, and Social Security warrant professional intervention.

- Approaching the Tax Torpedo Threshold: If your provisional income is hovering just below the $34,000 (individual) or $44,000 (joint) mark, a Certified Financial Planner (CFP) or CPA can help you structure your withdrawals to minimize the taxation of your benefits.

- Navigating the IRMAA Cliff: Because exceeding an IRMAA bracket by even one dollar triggers the full surcharge, professional tax planning is crucial if you have large RMDs or are planning the sale of a highly appreciated asset.

- Delaying Social Security Claims: If you have not yet claimed your benefits, you still receive the annual COLA—it is applied to your primary insurance amount behind the scenes. An advisor can run break-even analyses to help you determine if delaying until age 70 is the best mathematical strategy for maximizing this inflation-adjusted income.

“Social Security was never meant to be your only source of income in retirement. It is a safety net, and you must build your own financial foundation to withstand the pressures of rising costs over a 20- or 30-year retirement.” — Suze Orman, Personal Finance Expert

Frequently Asked Questions About the 2027 COLA

When will the 2027 Social Security COLA be officially announced?

The Social Security Administration will officially announce the 2027 COLA in mid-October 2026. This announcement follows the release of the September CPI-W data by the Bureau of Labor Statistics, which provides the final data point needed to calculate the third-quarter average.

Will my 2027 COLA be enough to cover rising Medicare premiums?

It depends entirely on the size of the COLA and the finalized Medicare Part B premium. In years with a high COLA, the benefit increase easily covers the Part B hike, leaving extra cash in your monthly check. In years with a very low COLA, the Medicare premium increase can consume most or all of the adjustment. Fortunately, the “hold harmless” provision prevents your net Social Security check from decreasing due to standard Part B premium hikes.

How is the COLA applied if I have not claimed Social Security yet?

You do not miss out on COLAs just because you delay claiming. From the time you turn 62 until you eventually claim your benefits, every annual COLA is automatically applied to your primary insurance amount (PIA). When you finally file for benefits, your starting amount will reflect all the intervening adjustments.

Does the Social Security COLA apply to other federal benefits?

Yes. The percentage announced for Social Security also applies to Supplemental Security Income (SSI) payments. Furthermore, the Department of Veterans Affairs (VA) traditionally uses the exact same percentage to increase disability compensation and pension benefits for veterans.

Why does my personal inflation rate feel higher than the COLA?

The COLA is tied to the CPI-W, which measures the spending habits of urban wage earners and clerical workers. Because younger, working-age people spend a lower percentage of their income on healthcare and a higher percentage on things like education and apparel, the index often underestimates the inflation experienced by retirees whose budgets are dominated by medical costs, insurance, and housing.

A proactive approach to managing your fixed income is the surest way to navigate economic uncertainty. By understanding how the CPI dictates your benefits, anticipating the tax implications, and strictly monitoring your personal expenses, you can insulate your retirement lifestyle against the eroding effects of inflation. Use the upcoming months of data releases not as a source of anxiety, but as a strategic tool to refine your budget and tax planning for 2027 and beyond.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, health needs, tax situation, and goals—may require different approaches. When in doubt, consult a licensed professional.

Last updated: June 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply