Retiring in a paid-off home provides peace of mind, but escalating property taxes can turn that sanctuary into a financial burden. When you transition to a fixed income, local tax assessors do not pause annual reassessments. This leaves many seniors struggling with housing costs that rise faster than Social Security adjustments. Identifying the states where property taxes hurt retirees the most allows you to make informed decisions about staying put, downsizing, or relocating entirely. While some regions lure retirees with zero state income tax, they frequently make up the difference by imposing exorbitant levies on real estate. Understanding these geographic tax traps protects your hard-earned retirement savings from being silently drained by local municipalities year after year.

The Fixed-Income Squeeze

Property taxes represent a unique threat to senior finances because they tax unrealized wealth rather than actual cash flow. If you purchase a home for $150,000 during your working years and it appreciates to $600,000 by the time you retire, your net worth looks fantastic on paper. However, you cannot buy groceries or pay for healthcare with home equity unless you sell or borrow against the property. Local governments assess taxes based on that new $600,000 value, sending you a bill that requires cold, hard cash.

For retirees relying heavily on Social Security and modest portfolio withdrawals, a sudden 15% spike in assessed home value can derail a carefully planned monthly budget. While inflation adjustments help fixed-income sources modestly, they rarely match the aggressive pace of real estate appreciation in desirable areas. This dynamic forces many retirees into a corner; they must either drain their liquid savings faster than anticipated or abandon their beloved family homes simply to escape the carrying costs.

To evaluate the true cost of retirement across the country, you must look beyond income tax brackets. States fund public services like schools, police, and infrastructure through varying combinations of income, sales, and property taxes. When a state lacks revenue in one category, it inevitably leans harder on another. For retirees who no longer earn a traditional paycheck, high property taxes become the most significant recurring expense draining their retirement accounts.

“If you’re going to stay in your home, you have to be able to afford the taxes, the insurance, and the upkeep.” — Suze Orman, Personal Finance Expert

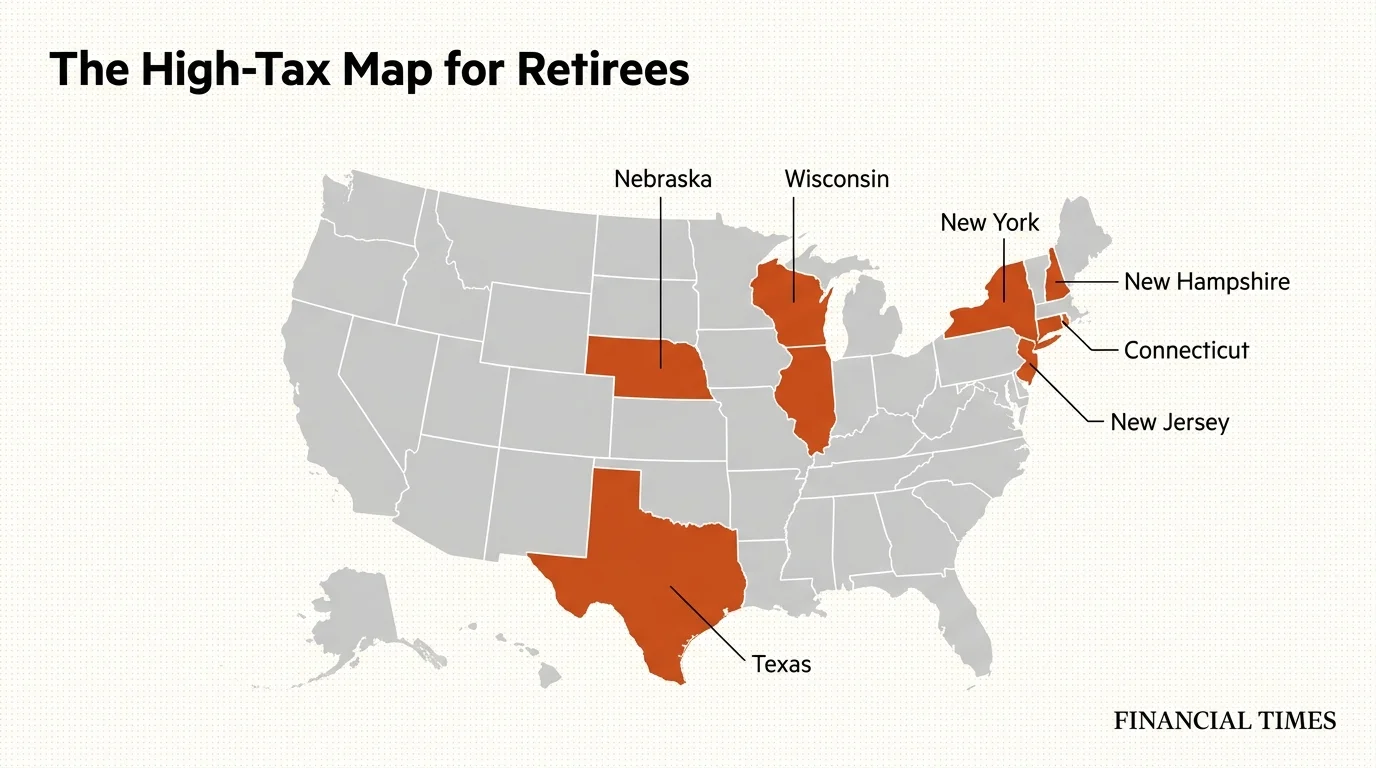

8 States Taking the Biggest Bite Out of Retiree Budgets

The following eight states consistently rank at the top of the nation for the highest effective property tax rates. If you currently live in one of these areas or are considering moving to one, managing these costs must become a central pillar of your retirement tax strategy.

1. New Jersey: The Undisputed Heavyweight

New Jersey holds the unfortunate distinction of levying the highest property taxes in the United States, with an average effective rate hovering around 2.49%. For a home valued at $400,000, a retiree can expect an annual tax bill approaching $10,000—an astonishing baseline expense before factoring in utilities, maintenance, or insurance. The state’s heavy reliance on property taxes stems from a fragmented system of small municipalities, each maintaining its own school district, police force, and administrative overhead.

To combat the exodus of seniors fleeing these punishing costs, New Jersey introduced the Senior Freeze program. This initiative reimburses eligible retirees for property tax increases that occur after their baseline year in the program. Additionally, the ANCHOR (Affordable New Jersey Communities for Homeowners and Renters) program provides direct property tax relief to residents meeting specific income thresholds. Despite these relief measures, the sheer volume of the initial tax assessment still makes New Jersey one of the most hostile environments for property taxes retirees face.

2. Illinois: The Midwestern Tax Burden

Illinois sits closely behind New Jersey with an effective property tax rate of roughly 2.27%. The primary driver behind these staggering bills is the state’s massive unfunded pension liabilities for public workers. Local municipalities must levy heavy property taxes simply to cover historical pension debt, leaving less revenue available for current civic improvements. In collar counties surrounding Chicago, it is entirely common for retirees to pay upwards of $8,000 to $12,000 annually on moderately priced homes.

If you live in Illinois, securing your senior exemptions is non-negotiable. The state offers a General Homestead Exemption, a Senior Citizens Homestead Exemption, and a Senior Citizens Assessment Freeze Homestead Exemption for those who meet income criteria. The latter prevents your home’s equalized assessed value from increasing, though your actual tax bill may still fluctuate based on local tax rate changes. Retirees must proactively reapply for these programs, as municipalities rarely grant them automatically.

3. New Hampshire: The Income Tax Illusion

New Hampshire frequently appears on lists highlighting the best states for retirees because it completely lacks a general state income tax and a state sales tax. However, the state government must fund its operations somehow, and the burden falls squarely on the shoulders of property owners. With an effective property tax rate of approximately 2.18%, retirees trading a high-income tax state for New Hampshire often experience acute sticker shock when their first municipal tax bill arrives in the mail.

Because local municipalities shoulder the vast majority of public school funding, towns with fewer commercial properties levy massive residential rates to balance their budgets. Retirees relying on savings and Social Security—which are already shielded from income taxes in many states—gain very little from New Hampshire’s lack of income tax while suffering immensely from its property tax structure. The state does offer a Low and Moderate Income Homeowners Property Tax Relief program, but the income limits are strict, leaving middle-class retirees fully exposed to the high rates.

4. Connecticut: High Costs Across the Board

Connecticut offers a double threat to senior finances: an effective property tax rate of roughly 2.14% combined with steep state income taxes and a generally high cost of living. Retirees in Connecticut find it difficult to execute any geographic arbitrage within the state, as nearly all counties feature aggressive property valuations and high mill rates. The state’s ongoing fiscal challenges and significant debt obligations mean property tax relief rarely gains legislative traction.

For seniors struggling to remain in their homes, Connecticut provides the Circuit Breaker program, formally known as the Homeowners’ Elderly/Totally Disabled Tax Relief Program. This provides a tax credit based on a graduated income scale. Local municipalities also have the option to offer their own localized tax relief for seniors, meaning a retiree’s financial survival often depends entirely on the specific town line they reside behind.

5. Texas: The Big State with Big Bills

Texas boasts a massive economy, a warm climate, and zero state income tax, making it a highly popular destination for relocating seniors. Yet, the Lone Star State relies heavily on property taxes to fund its independent school districts and county services. The average effective rate sits at 1.80%, but in rapidly growing metro areas like Austin, Dallas, and Houston, aggressive home appreciation has sent actual tax bills skyrocketing over the past decade.

The saving grace for older Texans is the robust Over-65 Exemption. Once you turn 65, Texas law requires school districts to offer a mandatory $10,000 exemption on your home’s value, and many districts offer far more. More importantly, obtaining the Over-65 exemption establishes a tax ceiling for school district taxes; the absolute dollar amount you pay to the school district cannot increase as long as you own and live in the home, barring major structural additions. Without this critical protection, Texas would easily rank as unlivable for fixed-income retirees.

6. New York: A State of Extremes

New York presents a complex landscape for retirees, with an average effective property tax rate of 1.73%. However, that average masks a massive geographic disparity. While New York City features surprisingly low property tax rates offset by high city income taxes, Upstate New York municipalities frequently impose effective property tax rates well over 3%. In areas like Rochester, Syracuse, and Buffalo, depressed housing values force local governments to aggressively hike rates just to maintain basic infrastructure and public schools.

The primary defense mechanism for older residents is the STAR (School Tax Relief) program. The Enhanced STAR exemption is specifically designed for seniors aged 65 and older who meet income requirements, exempting a significant portion of the home’s value from school taxes. Understanding how to navigate the complex application process for Enhanced STAR is vital for anyone attempting to balance retirement costs in the Empire State.

7. Wisconsin: Heavy Local Reliance

Wisconsin requires property owners to shoulder a significant portion of the state’s educational and municipal funding, resulting in an effective tax rate of roughly 1.51%. While this rate sits lower than New Jersey or Illinois, it remains high enough to squeeze Wisconsin retirees who also face state income taxes on certain retirement distributions. The harsh winters necessitate high home maintenance costs, compounding the financial strain on older homeowners.

To help residents manage these costs, Wisconsin offers a Homestead Credit, which functions as a circuit breaker designed to soften the impact of property taxes on lower-income households. Unfortunately, the income limits for this credit have remained stubbornly low for years, disqualifying many middle-class retirees who still feel the very real pain of their annual property tax assessments. Relocating to neighboring states with more favorable tax climates frequently tempts retirees living near the state borders.

8. Nebraska: The Agricultural Overspill

Nebraska’s effective property tax rate of 1.51% places a surprisingly heavy burden on its residents, driven by a tax code heavily skewed toward funding K-12 education through local real estate valuations. For decades, agricultural land values dictated the state’s tax politics, but as residential values in cities like Omaha and Lincoln surge, retirees bear an increasing share of the public funding burden.

The Nebraska legislature frequently debates property tax relief, but comprehensive solutions remain elusive. The state does offer a homestead exemption for residents over 65 who fall below specific income thresholds, exempting all or a portion of the home’s value from taxation. However, for retirees relying on modest pensions and Social Security that push them just over the income limit, the full weight of Nebraska’s property taxes must be paid out of pocket.

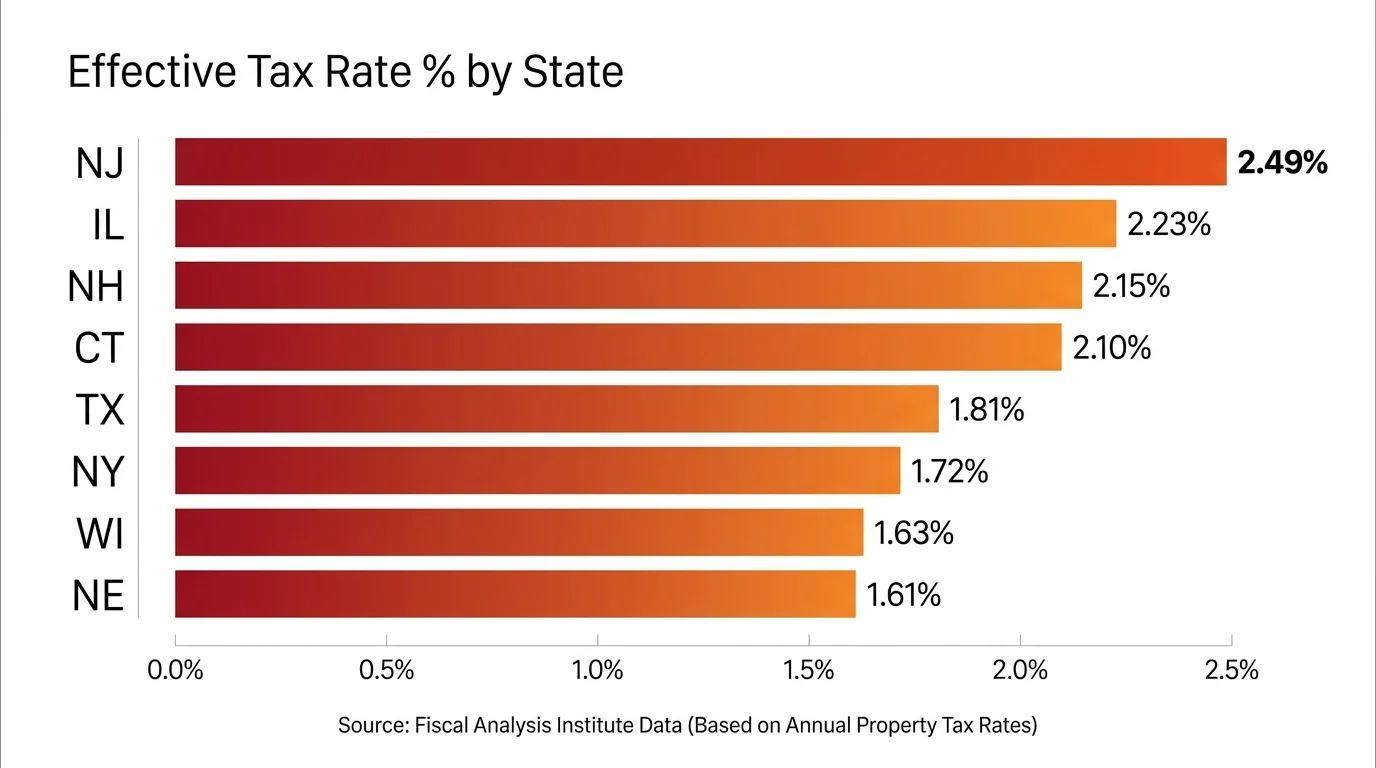

Comparison of the Worst Offenders

To put these numbers into practical perspective, look at how these rates impact a hypothetical $350,000 home. Keep in mind that actual tax bills vary significantly down to the specific neighborhood block, based on municipal and school district borders.

| State | Average Effective Rate | Estimated Annual Tax on $350k Home | Notable Senior Relief Program |

|---|---|---|---|

| New Jersey | 2.49% | $8,715 | Senior Freeze Program |

| Illinois | 2.27% | $7,945 | Senior Citizens Assessment Freeze |

| New Hampshire | 2.18% | $7,630 | Low/Moderate Income Relief |

| Connecticut | 2.14% | $7,490 | Circuit Breaker Program |

| Texas | 1.80% | $6,300 | Over-65 Tax Ceiling |

| New York | 1.73% | $6,055 | Enhanced STAR Program |

| Wisconsin | 1.51% | $5,285 | Homestead Credit |

| Nebraska | 1.51% | $5,285 | Homestead Exemption |

Pitfalls to Watch For

Managing your senior finances requires vigilance, especially when dealing with municipal bureaucracies. Retirees frequently fall into costly traps regarding their property taxes because they assume the system works automatically in their favor. Avoid these common mistakes to keep your hard-earned money in your own accounts.

Missing Exemption Deadlines

Municipalities rarely grant age-based property tax exemptions automatically. When you turn 65, the tax assessor does not cross-reference your birthday and lower your bill. You must locate the proper forms, compile proof of age and residency, and submit the paperwork before strict local deadlines. Missing the deadline by a single day can force you to pay the full, unadjusted tax rate for an entire year. Set calendar reminders three to six months before your 65th birthday to research exactly what documents your local tax office requires.

The “No Income Tax” Blind Spot

Retirees often fixate entirely on state income taxes when planning a relocation, assuming states like Texas, New Hampshire, or Florida offer a cheaper overall retirement. This narrow focus completely ignores the broader tax structure. If you generate your retirement income largely from Social Security and a Roth IRA, you already pay zero state income tax on those funds in the majority of states. Moving to a high-property-tax state solely to avoid income taxes provides you with absolutely no benefit while drastically increasing your monthly housing costs.

Ignoring the Appeals Process

Tax assessors make mistakes. They mass-appraise neighborhoods using algorithms that might incorrectly assume your home has a finished basement, a renovated kitchen, or extra square footage. Many retirees simply accept their annual reassessment notices without question. If you notice your home’s assessed value jumps significantly higher than similar homes on your street, or if the assessor’s description contains factual errors about your property, you have the right to appeal. Successfully appealing your assessment permanently lowers the baseline upon which future taxes are calculated.

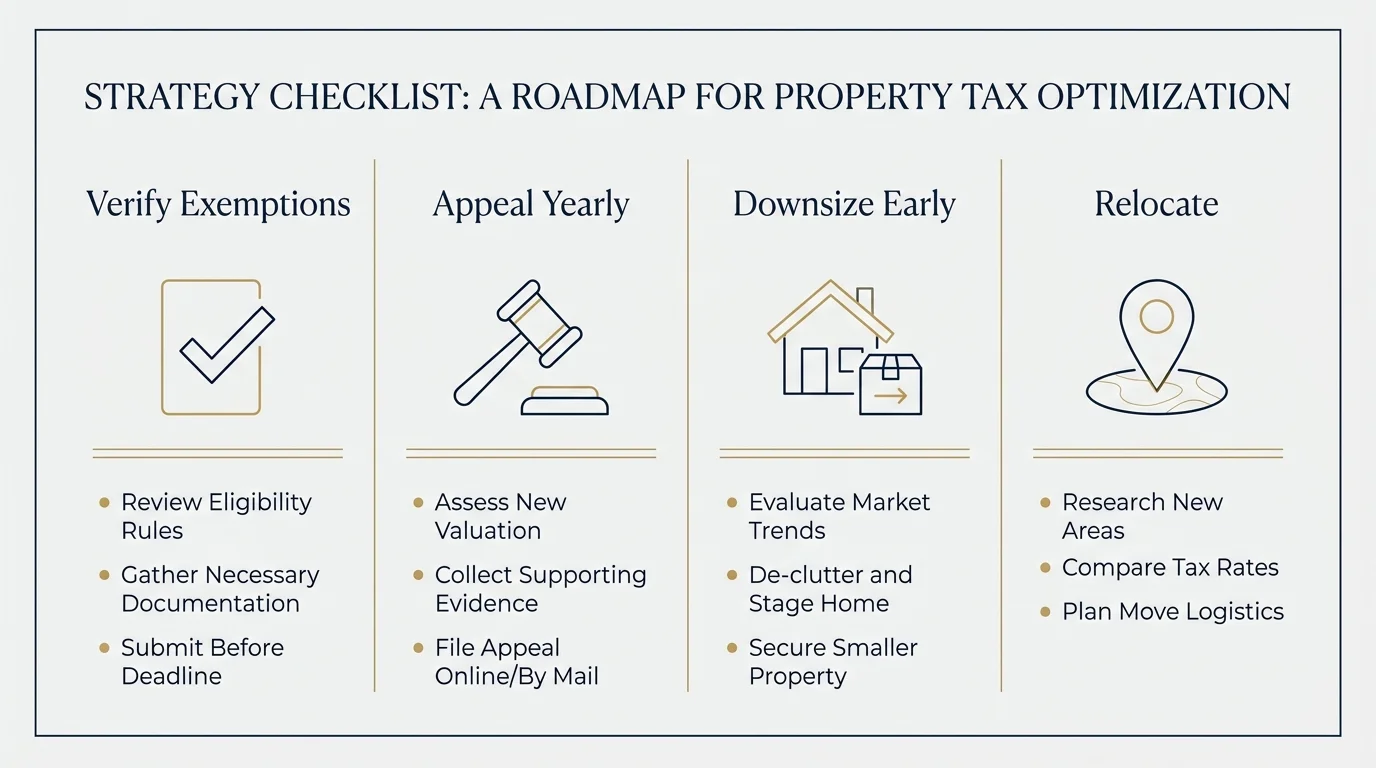

Strategies to Manage Your Property Tax Burden

You are not powerless against rising property taxes. Implementing proactive strategies protects your cash flow and extends the longevity of your investment portfolio.

- Downsize Strategically: Moving to a smaller home naturally reduces your property tax burden, but you must factor in the location. Downsizing from a $500,000 house in New Jersey to a $400,000 townhouse in the exact same town still leaves you with a staggering tax bill. Look for properties in neighboring counties or towns with lower mill rates and stronger commercial tax bases to subsidize residential costs.

- Hire a Professional Appraiser: If you plan to appeal your property tax assessment, arm yourself with concrete data. Hiring an independent appraiser costs a few hundred dollars but provides you with an authoritative document to present to the local tax board. If the professional appraisal comes in lower than the municipal assessment, you have an incredibly strong case for a reduction.

- Investigate Portability Laws: Some regions allow older residents to downsize and transfer their current, capped property tax rate to a new home. While famously utilized in Florida (Save Our Homes), other states have enacted variations of portability. Verify with your local tax authority whether moving within the state allows you to bring your favorable tax basis with you.

- Leverage Trusted Resources: Navigating state-specific tax laws requires accurate, localized information. Utilize free resources provided by organizations like AARP to research state tax guides, or consult the Internal Revenue Service (IRS) guidelines regarding the deduction of state and local taxes (SALT) if you still itemize your federal returns. Financial publications like Kiplinger also offer excellent, annually updated maps detailing the most tax-friendly states for retirees.

Frequently Asked Questions

Can I freeze my property taxes when I retire?

It depends entirely on your state and local municipality. Several states, including New Jersey, Illinois, and Texas, offer specific programs that freeze your property tax assessment or place a hard ceiling on your tax bill once you reach a certain age (usually 65). However, these freezes frequently come with strict income limitations to ensure the relief targets those on fixed, modest incomes. You must apply for these programs directly through your county or local tax assessor’s office.

Are property taxes deductible in retirement?

If you itemize your deductions on your federal tax return, you can deduct up to $10,000 combined for state and local taxes (known as the SALT deduction), which includes property taxes. However, following the 2017 tax reforms, the standard deduction increased significantly. Most retirees now find that taking the standard deduction provides a larger tax benefit than itemizing, rendering the property tax deduction moot for federal purposes.

Do reverse mortgages help pay property taxes?

A reverse mortgage allows you to convert a portion of your home equity into cash, which you can absolutely use to pay your property taxes. However, obtaining a reverse mortgage does not absolve you of the responsibility to pay local taxes. If you secure a reverse mortgage and subsequently fail to pay your property taxes or homeowner’s insurance, the lender can foreclose on the home. For guidance on housing costs and reverse mortgage rules, the Consumer Financial Protection Bureau (CFPB) offers comprehensive educational resources.

What happens if I cannot pay my property taxes?

Failing to pay property taxes results in severe consequences. The municipality will place a tax lien on your property. Eventually, the local government can sell that lien to private investors or foreclose on the home entirely to recoup the unpaid taxes. If you find yourself unable to pay, contact your local tax office immediately. Many municipalities offer payment plans or hardship deferrals for seniors to prevent foreclosure.

Managing your senior finances means looking beyond the balance of your retirement accounts and actively minimizing your recurring expenses. Do not allow exorbitant property taxes to dictate your quality of life. By researching local exemptions, aggressively appealing unfair assessments, and understanding the true cost of living across state lines, you take firm control over your financial future. Ensure you mark your calendar for essential exemption filing deadlines, and never assume a zero-income-tax state automatically translates to a cheap retirement.

This is educational content based on general retirement and financial principles. Individual results vary based on your situation. Always verify current benefit rules, tax laws, and eligibility requirements with official sources like SSA, Medicare.gov, or the IRS.

Last updated: March 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply