Moving into a smaller, more efficient home often unlocks the most immediate financial relief you will experience in retirement. When you swap a sprawling four-bedroom house for a manageable condo or single-story cottage, you instantly shed the invisible carrying costs that drain fixed incomes. Downsizing reduces your baseline living expenses, freeing up cash flow for travel, healthcare, or simply enjoying a debt-free retirement lifestyle. Beyond the obvious drop in mortgage payments or property taxes, a smaller footprint aggressively trims the everyday bills you have likely paid on autopilot for decades. By systematically evaluating your new living arrangement, you can permanently eliminate thousands of dollars in annual overhead and reclaim control over your monthly budget.

The Hidden Financial Power of Right-Sizing Your Home

Many retirees initially hesitate to leave the family home. The memories embedded in the walls, the familiarity of the neighborhood, and the sheer daunting task of packing up decades of accumulation create strong emotional anchors. Yet, the financial reality of maintaining excess space often overrides those sentiments once the numbers are laid bare. Large homes are hungry; they consume resources constantly, regardless of how many rooms you actively use.

When you shift your perspective from “losing space” to “gaining freedom,” downsizing becomes a strategic financial maneuver. Every square foot you eliminate represents a fraction of a heating bill, a portion of a property tax assessment, and a slice of your weekend dedicated to maintenance. By deliberately choosing a smaller footprint, you align your housing costs with your current lifestyle needs rather than your past family requirements.

“A house is a home, but it is also a very hungry beast. It requires constant feeding with your time, your energy, and your money. Downsizing puts that beast on a diet.” — Mitch Anthony, Retirement Lifestyle Expert

1. Property Taxes and Special Local Assessments

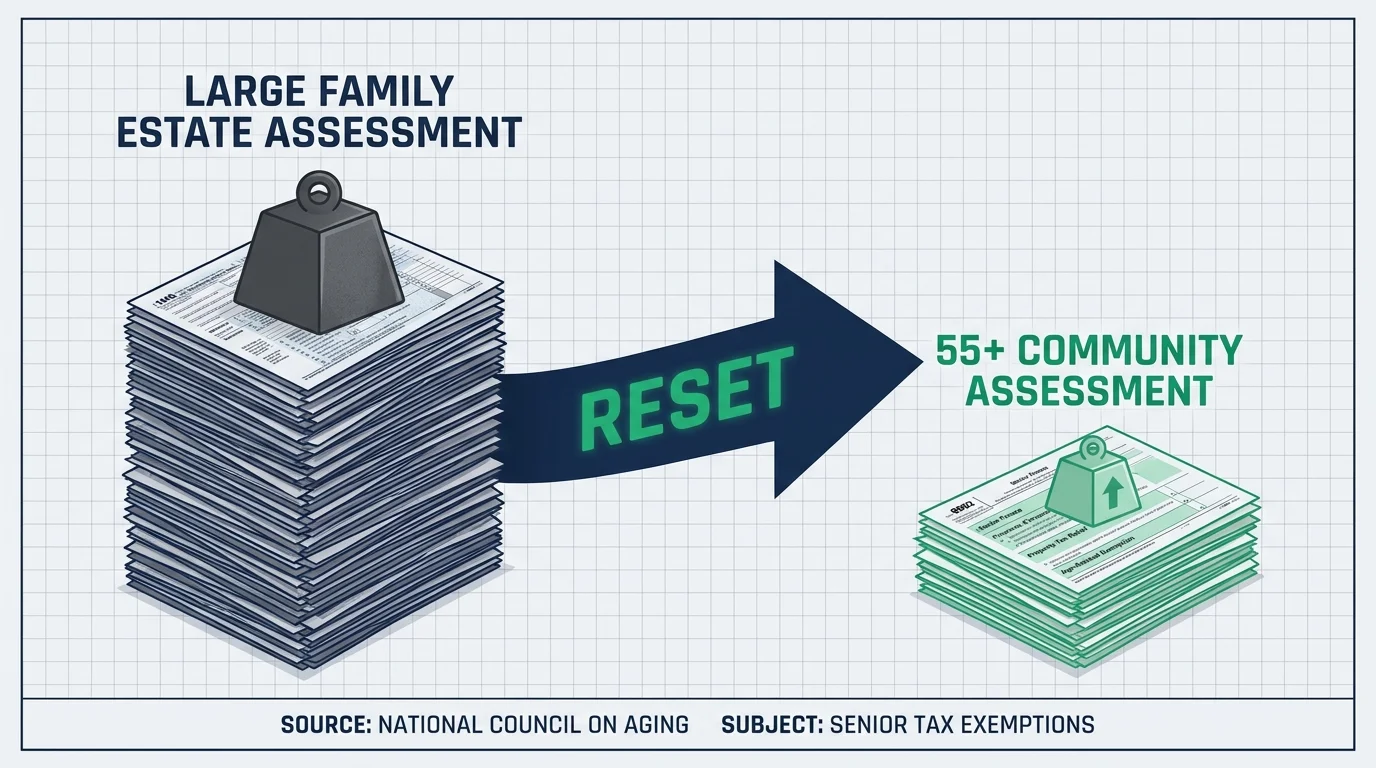

Property taxes represent one of the most volatile and uncontrollable expenses in a retiree’s budget. Because local governments reassess property values based on market conditions, your tax bill can surge even if your fixed income remains flat. Moving to a smaller home with a lower market valuation naturally compresses this annual liability.

The savings multiply if you relocate to a municipality or state with a more favorable tax structure for seniors. Many downsized communities—such as townhomes, condominiums, or targeted 55-plus developments—carry significantly lower assessed values than detached single-family estates. Furthermore, when you purchase a smaller home, you reset your baseline assessment. Organizations like the National Council on Aging (NCOA) often highlight how adjusting your housing wealth and utilizing local senior tax exemptions can dramatically improve month-to-month cash flow.

2. Heating, Cooling, and Base Utilities

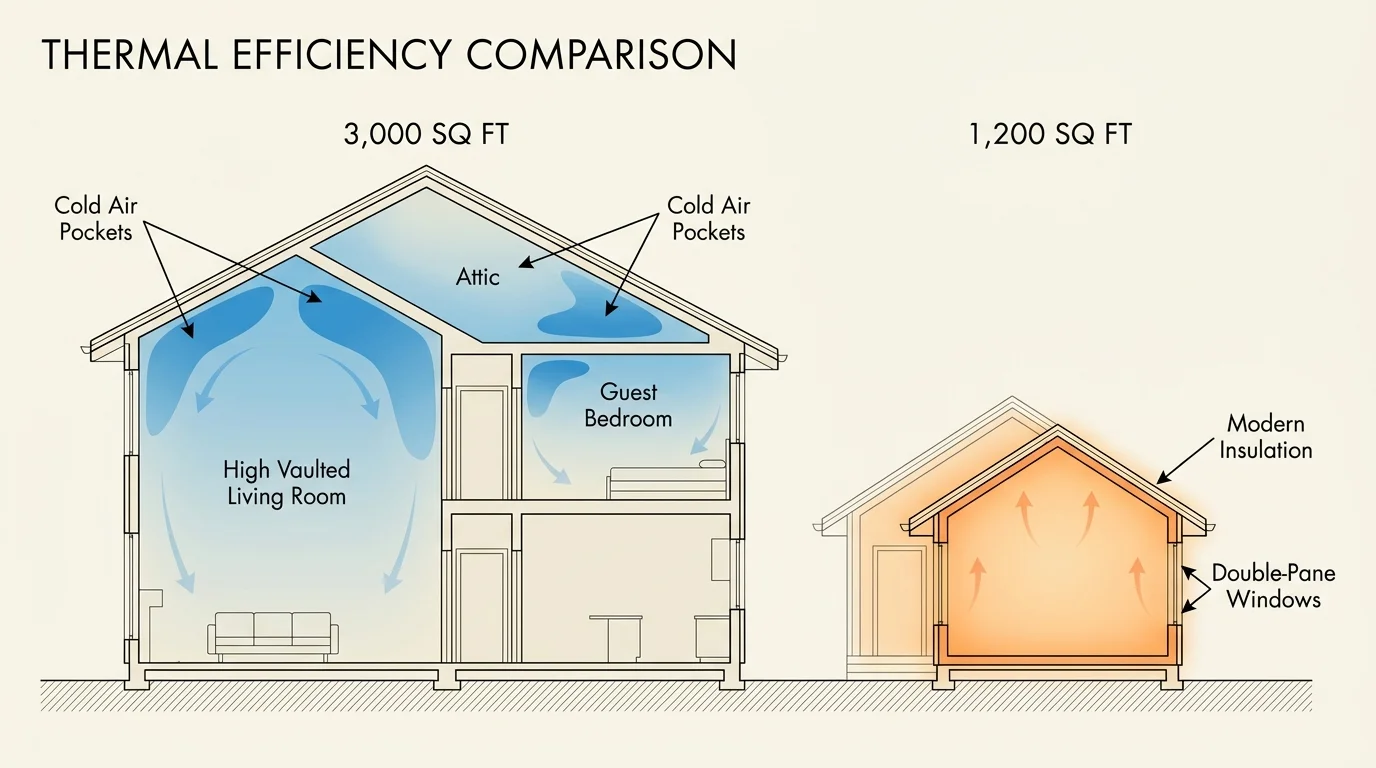

Climate control is fundamentally a matter of physics: the larger the cubic volume of air inside your home, the more energy required to heat and cool it. If you currently live in a 3,000-square-foot home but spend 90 percent of your time in the kitchen, living room, and primary bedroom, you are paying a premium to pump conditioned air into empty guest rooms and unused formal dining spaces.

Downsizing directly targets this inefficiency. A 1,200-square-foot home requires smaller HVAC equipment, consumes less natural gas or electricity, and reaches comfortable temperatures far faster. Additionally, newer downsized homes or recently renovated condos often feature modern insulation, double-pane windows, and high-efficiency appliances that older, larger family homes lack. The reduction in your monthly utility bill is immediate and permanent.

3. Homeowners Insurance Premiums

Insurance companies calculate your homeowners premium based heavily on the replacement cost of your dwelling. A large home with multiple rooflines, extensive square footage, and custom finishes costs significantly more to rebuild after a catastrophic loss than a modest cottage. Consequently, shedding square footage directly lowers your insurance risk profile.

If you downsize into a condominium or a cooperative housing arrangement, the savings become even more pronounced. In these environments, the homeowner’s association (HOA) master policy covers the exterior structure and common areas. You only need to purchase an “HO-6” policy, which covers your personal property and the interior elements of your specific unit. These policies are historically a fraction of the cost of a traditional single-family home insurance policy.

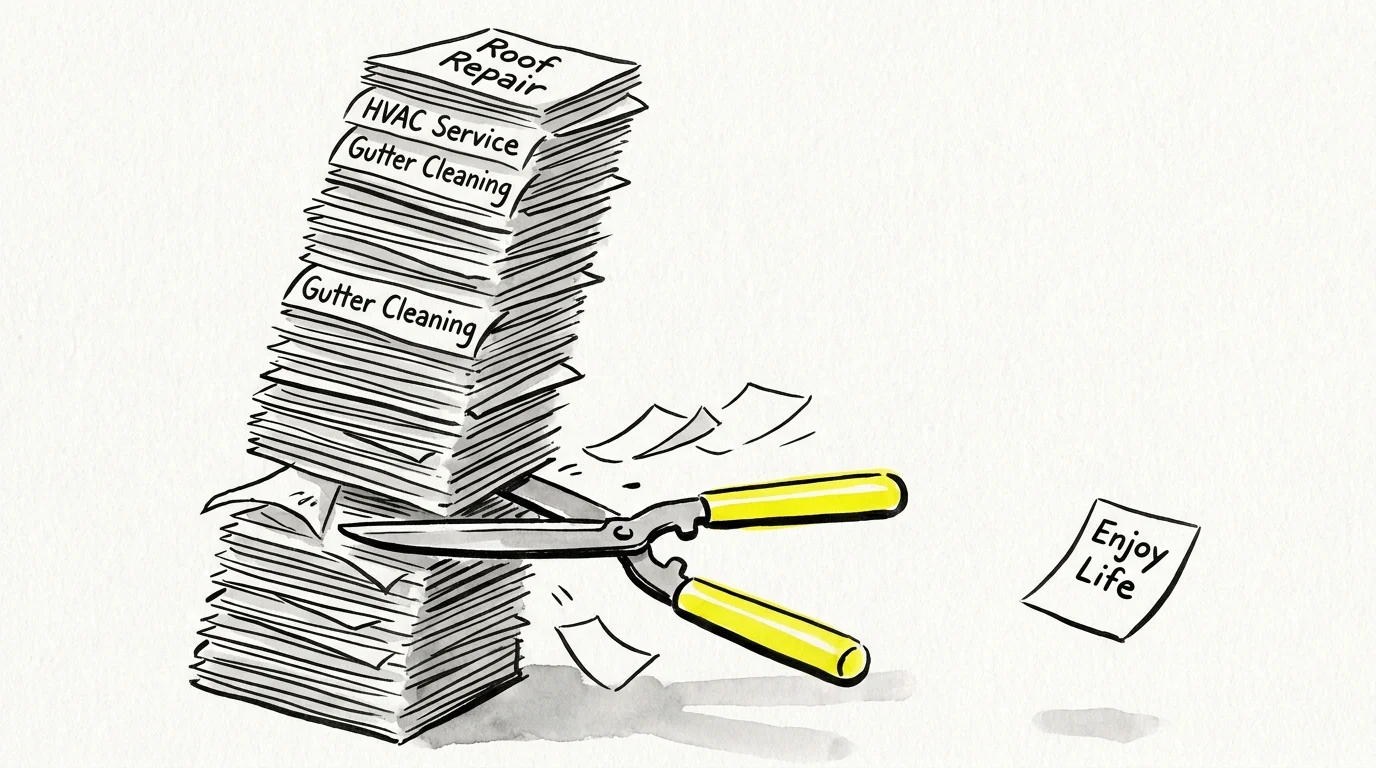

4. Routine Maintenance and Costly Repairs

Financial planners generally recommend budgeting one to two percent of your home’s total value annually for maintenance and repairs. For a $500,000 home, that translates to $5,000 to $10,000 every year just to replace aging water heaters, fix leaky roofs, service the HVAC system, and keep the exterior painted.

A smaller home drastically shrinks the surface area requiring maintenance. There are fewer windows to break, less siding to pressure wash, and a smaller roof to eventually replace. Furthermore, moving into a freshly updated smaller home or a new-construction townhouse resets the lifespan of your major systems. You effectively buy yourself a ten-year window where major capital expenditures—like replacing a furnace or repaving a massive driveway—are completely removed from your financial radar.

5. Lawn Care, Landscaping, and Snow Removal

Maintaining a manicured half-acre lot demands either significant physical labor or a hefty monthly fee paid to a landscaping service. As we age, the physical toll of pushing a mower in the summer heat or shoveling a sprawling driveway in freezing temperatures becomes prohibitive. Hiring out these services easily costs hundreds of dollars a month depending on your region.

Downsizing frequently eliminates this category entirely. Many retirees choose patio homes, townhouses, or condos where exterior groundskeeping is managed by the community. Even if you purchase a smaller single-family home, a compact yard requires minimal water, zero riding mowers, and can often be maintained with simple, low-cost electric tools. You reclaim both your money and your weekend leisure time.

6. Water, Sewer, and Municipal Services

Water usage might seem like a minor line item, but municipal water and sewer rates have outpaced inflation in many regions across the country. Large homes often feature sprawling irrigation systems to maintain expansive lawns, multiple bathrooms with aging, inefficient fixtures, and larger capacity appliances.

When you transition to a smaller property, your water footprint naturally shrinks. You no longer water a massive lawn, and you operate fewer bathrooms. Furthermore, downsized properties rarely carry the steep “base facility charges” or tiered usage penalties that some municipalities apply to massive residential lots. Over the course of a year, cutting your water and sewer bill in half yields substantial savings.

7. Home Security and Extensive Monitoring Systems

Securing a large property requires extensive hardware. You need sensors on a dozen ground-floor windows, multiple exterior cameras, motion detectors for a sprawling backyard, and higher monthly monitoring fees to cover the complex system.

A smaller home, particularly a condo or a home situated within a tight-knit retirement community, inherently offers better security with less required technology. Many 55-plus communities feature gated access, dedicated security patrols, and closely spaced neighbors who look out for one another. You can often downgrade your expensive, multi-zone security contract to a simple, self-monitored smart doorbell or cancel the premium service altogether.

8. The Hidden Cost of Clutter and Storage

Large homes act as magnets for consumer goods. When you have empty closets, spare bedrooms, and a three-car garage, you naturally accumulate furniture, seasonal decor, bulk purchases, and hobby equipment to fill the space. The invisible cost of a large home is the money you spend furnishing, cleaning, and organizing the extra square footage.

Downsizing forces an intentional curation of your belongings. You can no longer buy things simply because you have space for them. This shift in consumer behavior permanently lowers your discretionary spending. You buy less because you physically cannot store more. By embracing a minimalist approach tailored to your new space, you stop bleeding cash into the endless pursuit of home goods.

Comparing the Carrying Costs: Large Home vs. Downsized Property

To visualize the financial impact, consider this hypothetical monthly comparison between a paid-off 3,000-square-foot family home and a paid-off 1,200-square-foot townhome. Even without a mortgage, the carrying costs differ dramatically.

| Expense Category | Large Family Home (Monthly) | Downsized Townhome (Monthly) | Estimated Monthly Savings |

|---|---|---|---|

| Property Taxes | $650 | $280 | $370 |

| Homeowners Insurance | $180 | $65 (HO-6 Policy) | $115 |

| Gas & Electricity | $280 | $120 | $160 |

| Water & Sewer | $110 | $45 | $65 |

| Lawn Care & Snow Removal | $150 | $0 (Covered by HOA) | $150 |

| Maintenance Sinking Fund | $400 | $150 | $250 |

| HOA Fees | $0 | $250 | -$250 |

| Total Monthly Overhead | $1,770 | $910 | $860 |

Note: In this realistic scenario, the retiree saves $860 per month ($10,320 annually), even after factoring in a new $250 monthly HOA fee for the townhome community.

What Can Go Wrong: Downsizing Traps to Avoid

While the financial benefits of downsizing are compelling, poor execution can quickly erode your anticipated savings. Navigating the real estate transition requires careful planning and a clear understanding of the hidden costs associated with moving.

- The Storage Unit Trap: The single biggest mistake retirees make is downsizing their living space but refusing to downsize their possessions. If you rent a $200-per-month climate-controlled storage unit to house furniture that will not fit in your new home, you are subsidizing a museum of your past and instantly destroying a large portion of your monthly utility savings.

- Underestimating HOA Fees: Moving into a maintenance-free community sounds idyllic until you examine the fine print. Homeowner association dues can range from $100 to over $1,000 per month depending on the amenities. You must ensure the HOA fee is less than what you currently spend on individual maintenance and insurance. Furthermore, investigate the HOA’s reserve fund; a poorly managed association can hit you with massive special assessments for roof repairs or community paving.

- Ignoring Capital Gains Taxes: If you have lived in a highly appreciated property for decades, selling it might trigger capital gains taxes. The IRS allows single filers to exclude up to $250,000 of capital gains on a primary residence ($500,000 for married couples filing jointly). If your home’s appreciation exceeds these limits, your tax bill could eat into the equity you planned to use for your next purchase.

- Failing to Account for Transaction Costs: Real estate agent commissions, staging, moving companies, closing costs, and furnishing a new home can easily consume eight to ten percent of your current home’s sale price. You must calculate the “break-even” point to ensure the monthly savings justify the upfront cost of moving.

For more detailed guidance on managing housing wealth and understanding the financial implications of selling a home late in life, the Consumer Financial Protection Bureau (CFPB) offers extensive, unbiased resources designed specifically for older adults.

Frequently Asked Questions About Downsizing Savings

Does downsizing always guarantee I will save money?

No. If you downsize from a paid-off home in a low-cost rural area to a smaller luxury condo in a high-cost urban center, your monthly expenses will likely increase. Downsizing only saves money when you are moving to an area with comparable or lower costs of living, and when you successfully avoid high HOA fees and storage unit rentals.

Should I downsize before or after I officially retire?

Executing your move one to two years before your actual retirement date offers several advantages. You can use your working income to qualify for a new, smaller mortgage if needed, and you avoid the stress of navigating a major life transition at the exact same time you are adjusting to a fixed-income lifestyle. Furthermore, AARP suggests that early downsizing allows you to build a social network in your new community while you still have the energy and mobility to explore.

How do I handle the emotional toll of getting rid of my belongings?

Start early and go slow. Begin with rooms you rarely use, such as the attic, basement, or guest bedrooms. Give sentimental items to children or grandchildren now, so you can enjoy watching them use the items. Focus on the reality that your memories reside within you, not within physical objects. Taking photographs of bulky sentimental items can help you let go of the physical piece while preserving the memory.

What if my adult children need to move back in?

This is a common fear that keeps retirees trapped in excessively large homes. Financial independence in retirement requires prioritizing your own stability first. If you must accommodate family, look for downsized homes with flexible spaces—such as a small den with a pull-out sofa—rather than maintaining empty bedrooms 365 days a year for a situation that may never occur.

Adjusting Your Budget for the Next Chapter

Downsizing is not a retreat; it is a strategic repositioning of your assets. By shedding excess square footage, you eliminate the friction of high utility bills, relentless maintenance, and bloated property taxes. The resulting monthly surplus allows you to redirect your fixed income toward the experiences, healthcare security, and leisure activities that define a successful retirement.

Take the time to track your current housing expenses meticulously for a few months. Once you have a clear picture of what your large home truly costs to operate, you can make an informed, data-driven decision about your next move. Freedom in retirement rarely comes from having more space; it comes from having more choices.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, health needs, tax situation, and goals—may require different approaches. When in doubt, consult a licensed professional.

Last updated: March 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply