Your 2027 Social Security cost-of-living adjustment is shaping up to be noticeably smaller than the increases seen over the past few years, as recent inflation data points toward a cooling economy. This shifting social security forecast means you must prepare for tighter margins between your monthly benefits and your actual living expenses.

While a lower COLA signals price stability in the broader market, it rarely reflects the soaring healthcare and housing costs that directly impact your wallet. Understanding how the government calculates your retirement benefits update allows you to adjust your income strategies now.

By proactively managing your portfolio and tax liabilities today, you can protect your purchasing power before the official rate drops this October.

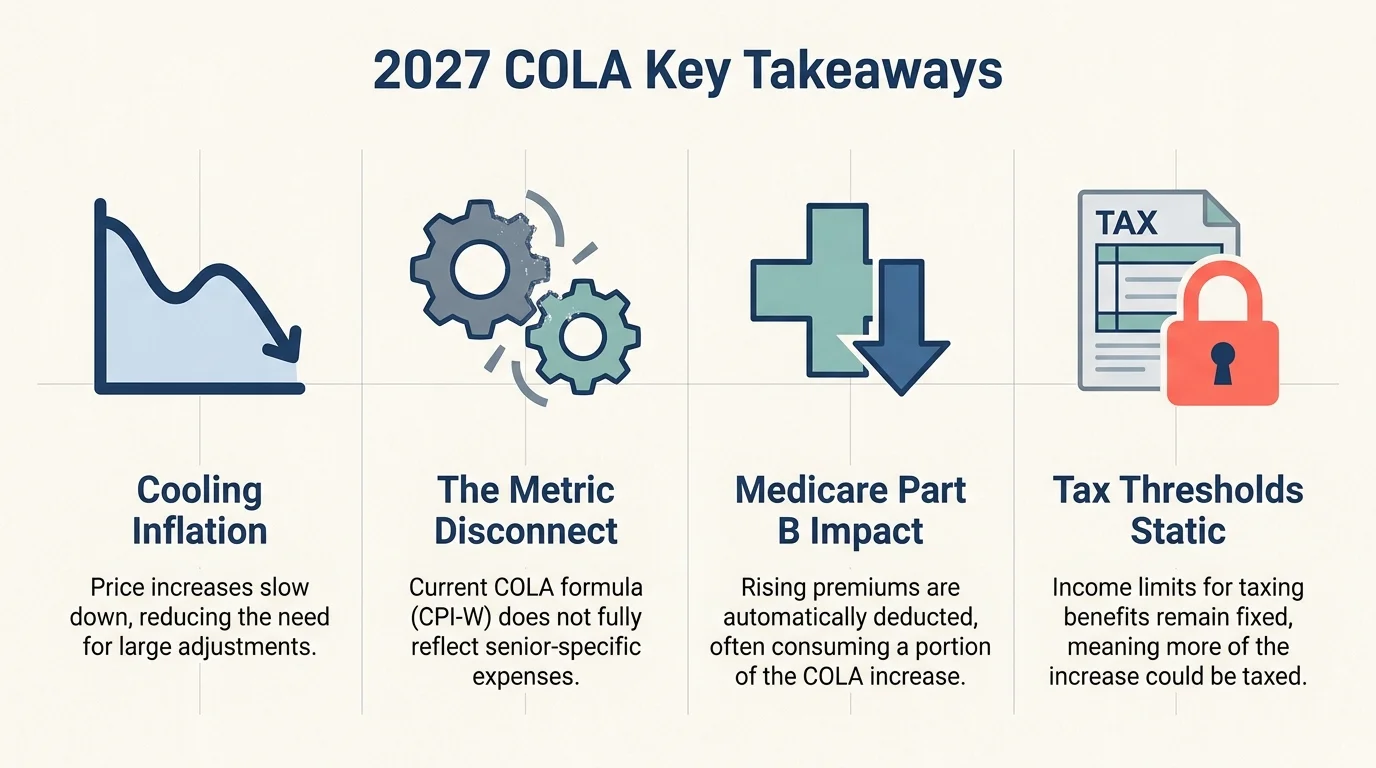

At a Glance

- Cooling Inflation: Recent economic data has lowered the projected cost-of-living adjustment for 2027, signaling a return to pre-pandemic historical averages.

- The Metric Disconnect: The government formula relies on the spending habits of urban workers, which often underrepresents the healthcare and housing costs experienced by seniors.

- Medicare Part B Impact: Rising Medicare premiums may absorb a significant portion of your net benefit increase next year.

- Tax Thresholds Remain Static: Because the IRS does not adjust Social Security taxation brackets for inflation, even a small benefit increase can expose more of your income to taxes.

UNSUBSCRIBE ME!

Rich get richer and the poor get poorer

I do t think we should pay taxes on our social security. We already payed taxes while we worked all those years. We can barely afford groceries and bill. Medicare part F is so high we’re paying over 659.00 a month for my husband and 397.00 for mine there goes our SSI check

How are suppose to buy food and our medicine. Everything keeps going up and there is not enough money left to pay rent, food, medicine. So poor gets poorer and there is no middle class only rich and richer. Soon there will be more homeless seniors on the streets cause we can’t afford the rent in increases. Thanks Mr Trump maybe your daddy can help us older people out. Hope one day you will be walking in our shoes. Trying to figure out to have some shelter or food to eat, or be sick or die

Why should someone who pays less get more? The more u pay……the more u get.

Seniors are a after thought. Food prices rising, utilities increasing and insurance is mandatory. Insurance is a poor example of what we all worked our life for. Nothing – mandatory pay into social security, along with Uncle Sam. Then Uncle Sam says nope, we will put you a allowance. Here’s your sign.

100% inflation 1%-2 cola past 3 yrs?

Inflation cooling, I don’t think so. May 4.2 and April 3.8, Fed’s probably going to have to increase the fed rate to slow down inflation. Correct me if I’m wrong.

By the time I am old enough to retire, there won’t be any Social Security left. Speaking of the left, we need to thank them for blowing all of this up for us and you know what, they’re not the ones losing any sleep over all of this! I totally agree, the rich get richer, forget the middle class, there isn’t one! All we can really do is pray, let the good Lord take over, he will provide.

Looks like Click Bait to me. You can “Search” COLA 2027, and even recent, hours old articles, say the exact opposite! Some state that the 2027 COLA could be the largest in years! Why do people post articles like this, that only contribute to fear and anxiety. Well, I think we all know why…. Advertisers. I’m sick of click bait. One doesn’t know what to believe anymore.

Looks like Click Bait to me. You can “Search” COLA 2027, and even recent, hours old articles, say the exact opposite! Some state that the 2027 COLA could be the largest in years! Why do people post articles like this, that only contribute to fear and anxiety. Well, I think we all know why…. Advertisers. I’m sick of click bait. One doesn’t know what to believe anymore.

I haven’t paid taxes on my SS in 8 years. If you are paying taxes on SS you are raking in a lot of money.

How is this Trump’s fault?? Thus has been an issue way before him!!

They make it sound like receiving SS is a gift or reward, it is our money! Paying taxes on it twice is a total rip off and manipulation that is so wrong. BOTH parties are at fault, but having a figure head as crude and disreputable as Trump is a total embarrassment. To think we are celebrating our 250 anniversary with Trump as our president is unfathomable, and such a shame. His horde of advisers and enablers are a disgrace….right little Mario!

More TDS. Get professional help.

i have been collecting social security for a few years now and have never paid taxes on it. the only way you need to pay taxes when you’re collecting social security is if you have other forms of income – you need to pay taxes on those, not social security itself.

Because Regan passed a bill so a president can burrow money from social security. Bush Jr. took 2.9 trillions from social security. And the Republicans never paid it back.

Just gimme gimme gimme my money!I earned it!

Dump will never be in your proverbial shoes; he is a thief and grifter and steals from everyone.

Congress should replace the money they took from SS, then maybe we could get enough to live on….Crooks….

I tend to agree with you, Mr. Minor. A “quick search” yields the following:

The official 2027 Social Security COLA will be announced by the Social Security Administration on October 14, 2026, and will be based on inflation data from July through September 2026. Current forecasts project a significant increase, with The Senior Citizens League estimating 3.8% and independent analyst Mary Johnson forecasting as high as 4.7%.

If the 3.8% estimate holds, the average monthly benefit for retired workers would rise by approximately $79 to $2,160. This projected increase is driven by elevated inflation, particularly in energy costs linked to geopolitical tensions, marking a potential “good news/bad news” scenario where higher payouts offset high consumer prices but strain Social Security trust funds. — AI-generated answer. Please verify critical facts.

This site could just unsubscribe me … except for the great probability that they would just list my info with dozens of other names they go by and/or sell my info; with the final result that I would receive 5 to 10 times the number of “junk” emails that I now do. I’m not sure when “Unsubscribe me” became an automatic “Please send me a lot more emails and sell my info to lots of others like you that I do not wish to hear from.”

And most of us did not pay taxes on SS, even when the 50% tax began in 1983, as the income levels for taxing were more than most retired folks income, then they jacked it to 85% but the income levels did not equal inflation. Retirees should pay zip if their income is under 100K . Never be fixed unless we put Congress and federal employees on SS instead of their inflated retirement plan we have to pay for.

We have always been puppets for the rich and nothing has or will ever change, they get richer and we get poorer. I am moving to PVR Mexico area where it is paradise and much cheaper to live.

Thank you, he had nothing to do with it!

What do you mean by racking a lot of money .? Im paying taxes on my SS money.

I have to add this, I keep getting mail. Wanting money for congress to pass the cola which they tell me I am owed by government 1200 dollars. They do not do their jobs,I am done voting for them,

Boy ain’t that the truth!!!

My husband and I live on approx 1,700.00 a month, combined! And im not complaining, except for the fact they’re giving illegalls

3k a month, free food, free Healthcare, and paying there rent, and they’ve NEVER worked a day in our country and never paid a CENT in taxes!! Low Income seniors keep getting screwed, over an over!!

Its not his fault, he’s the one who pushed to give everyone the big tax cuts and did just that while every single democrat voted to raise our taxes. Stock market is up, unemployment is down and so is inflation. Gas did go up for a couple months and he told us it was gonna go up for a little while before we knew about Iran but now it’s back under $3.00 gal the economy is the strongest it’s been in years. Only people that want to take money away from you is the usual suspects…. the same ones that keep making up all the lies about our President and somehow you believe them. By the way, this website comes out of Romania so don’t believe everything you read

What country do you live in?

Let all government employees put into Social security like the rest of us instead of the retirement program they voted in for themselves.

In addition, remove the cap on the income that the SSA gets. Why should those who make more than $189,000 (or whatever the cap currently is) pay no more than someone fortunate enough to make the cap. People such as Elon Musk, Jeff Bezos etc. wouldn’t miss the small percentage that would go into Social Security but the benefits to those who depend on it could be easily covered.

Disgusting!

Gotta take care of ISRAEL FIRST

Senators and congressmen should be the first to feel any pinch in the wallet. Oh! Take away a lot of their perks so that they really understand any damage they do.

The inflation kicked in on Biden’s watch. Remember all of that free covid money. That was the start amongst other things. TDS any.

Our esteemed former President Ronald Regan is the one who instituted taxing or “Double Taxing” Social Security in order to fund his Tax Cuts for the “Rich & Famous”. But then again, it was our other esteemed former President Richard Nixon who “Opened the Doors to China” in February 1972 and former President Bill Clinton championed China’s entry into the World Trade Organization (WTO) and look how that turned out. However, when Bill Clinton left office in January 2001, the U.S. Treasury had a unified federal budget surplus for 4 consecutive years from 1998-2001 spanning the end of President Clinton’s Administration. The Treasury Department reported a record surplus of $237 billion in Fiscal Year (FY)2000. This was the last Federal Government Surplus. Clinton was the last President to balance the Federl Budget. Look what shape G.W. Bush left us when he left office in 2009. It was called “The Great Recession”.

The costs went up higher and faster under Biden. Did you thank him?

Kim,

EVERYTHING is Trumps fault!!!!

It was not President Trump who caused the high inflationary costs. He is trying to get the spending down while the democrats are still wanting to keep increasing spending. Remember, he is trying to get the Congress,(democrats), to pass a bill that cancels Social Security taxes for us retired folks.

I voted 3 times for Trump & appreciate him as the best President we can have with the strong types of leaders in China, Russia, North Korea & Iran. However, the statement that there are no more taxes on social security is inaccurate, & I heard him make this exact statement on tv 3-4 months ago.

We got a 12k tax deduction in the big beautiful bill. 6k each. We do pay taxes on our social security but only about 2k each The 12k tax decduction keeps us in a lower tax bracket and it will continue thru 2028. Because of the Byrd rule changes can’t be made to your actual social security benefits. We will take the 12k deduction all day long.

We paid taxes all those many years we worked and I am 76 years old and still working because I can’t live on social security that just sucks like it is the rich get richer and the poorer get poorer what is the world coming to, seniors are just a forgotten, even doctors say now ell you know you are old what the hell maybe one day they will be there and how when their doctor can tell them that statement see how they feel. I just think we seniors are getting bad rap and the government knows it and yes, WE did pay social security on this money, and it is ours, so we are screwed. Thank you, government, this money was supposed to be set aside, but it was spent for something else and now we as seniors have to suffer. That’s all.