Many pre-retirees build detailed visions of their future lifestyle without pressure-testing the reality behind those daydreams. A financial strategy that looks flawless on paper or a lifestyle choice that sounds deeply fulfilling in conversation can quickly unravel when faced with unpredictable health changes, hidden costs, or social isolation. By examining the flaws in eight commonly idealized retirement scenarios—from full-time RV living to indefinitely relying on part-time work—you can protect your nest egg and build a more resilient strategy. Anticipating these hidden pitfalls allows you to pivot your approach, ensuring your hard-earned savings support a retirement that is both financially secure and genuinely rewarding.

1. Selling the Family Home to Travel Full-Time in an RV

Trading a stationary mortgage for the open road represents the ultimate vision of freedom for many retirees. Selling your primary residence to fund a high-end motorhome sounds like a brilliant way to eliminate property taxes, downsize your possessions, and see the country. You imagine waking up to mountain views on Tuesday and ocean waves on Friday.

The financial and logistical realities often paint a much harsher picture. Unlike traditional real estate, recreational vehicles are depreciating assets. A new luxury motorhome loses a massive percentage of its value the moment you drive it off the lot, and the depreciation continues year after year. Simultaneously, maintenance costs run exceptionally high. Finding specialized diesel mechanics on the road is stressful, and replacement parts can sideline your mobile home for weeks, forcing you into expensive short-term rentals or hotels.

Furthermore, full-time travel introduces complex healthcare hurdles. If you rely on a localized Medicare Advantage plan, securing in-network care while traveling across state lines becomes incredibly difficult and expensive. Traditional Medicare provides more geographical flexibility, but coordinating routine care and prescription refills on the move remains a logistical headache. Before committing to this lifestyle, rent an RV for three to four consecutive months. This trial run exposes the true costs of fuel, skyrocketing campground fees, and the emotional toll of constant relocation.

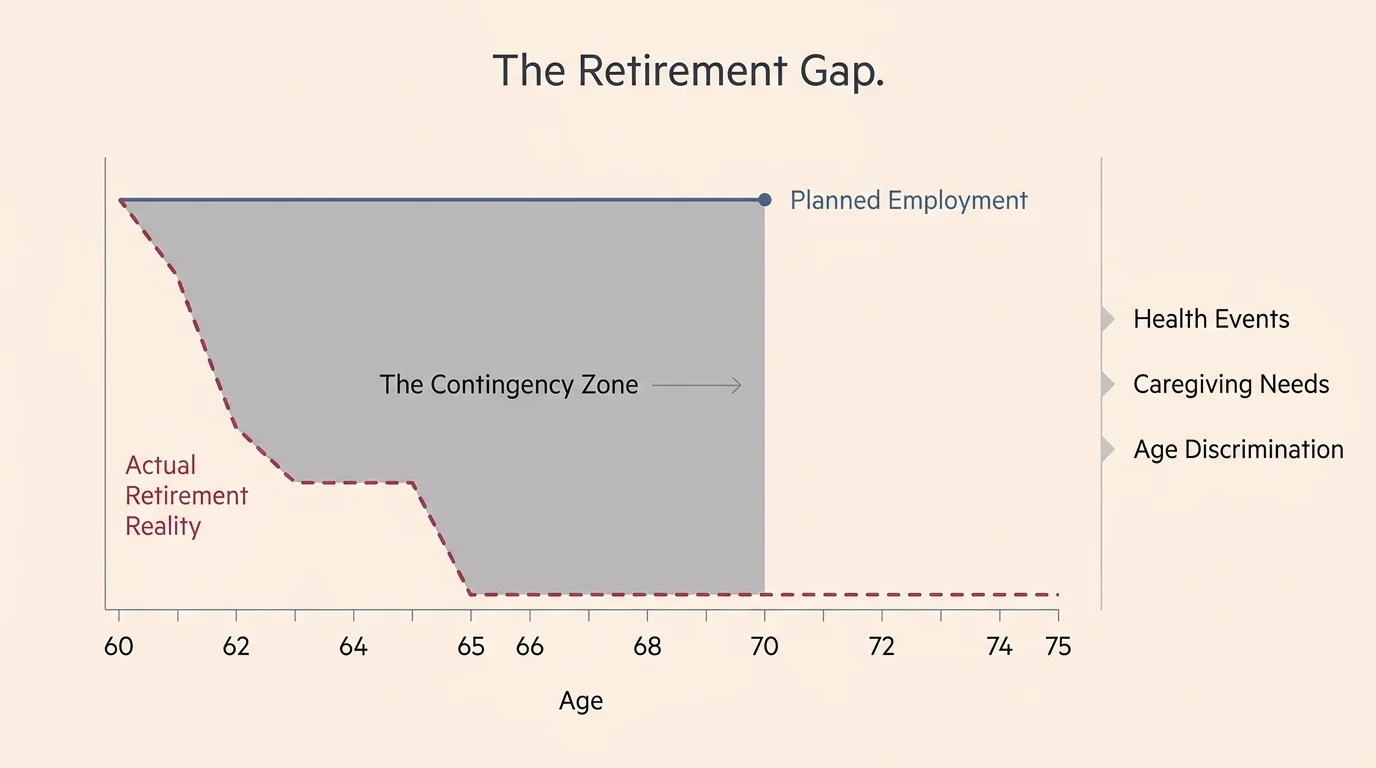

2. Working Part-Time Indefinitely to Delay Social Security

Planting your financial security on the assumption that you will work part-time until age 70 sounds incredibly responsible. The math undeniably works: continuing to earn an income allows your investment portfolio to grow untouched while maximizing your future Social Security Administration benefits through delayed retirement credits. You stay mentally engaged, remain socially active, and build a larger financial safety net.

However, reality rarely aligns with spreadsheet projections. Decades of data reveal that nearly half of all Americans leave the workforce years earlier than they originally intended. You cannot control the specific circumstances that force an early exit. Age discrimination, though illegal, remains a persistent barrier to securing or keeping part-time employment in your late sixties. Even more common are unpredictable health events—either your own physical decline or the sudden need to become a full-time caregiver for a spouse or aging parent.

When an unexpected life event severs your part-time income, you face a dangerous sequence of decisions. You might have to claim Social Security earlier than planned at a permanently reduced rate, or abruptly begin drawing down your retirement accounts during a potential market dip. A robust financial plan must include a contingency strategy that assumes your earning ability drops to zero at age 62 or 65, even if you hope to work much longer.

3. Relocating Solely for a Zero-Income-Tax State

Packing up and moving to Florida, Texas, Nevada, or Tennessee specifically to escape state income taxes represents one of the most common retirement planning maneuvers. Retirees diligently calculate how much they will save by shielding their pension payouts, IRA withdrawals, and part-time earnings from state governments. The prospect of keeping thousands of extra dollars every year creates a powerful incentive to relocate.

States must generate revenue to fund infrastructure, schools, and emergency services. If a state does not collect income taxes, it aggressively extracts that revenue through alternative channels. Texas and Florida, for example, heavily rely on property taxes and high sales taxes. When you factor in the soaring costs of homeowners insurance and specialized flood or hurricane coverage in coastal areas, the actual cost of living often eclipses whatever you saved on income tax.

| Tax Consideration | The Zero-Income-Tax Myth | The Financial Reality |

|---|---|---|

| State Income Tax | You keep 100% of your IRA distributions. | Accurate, but only represents one piece of the tax puzzle. |

| Property Taxes | Viewed as a standard, manageable expense. | Often double or triple the national average in zero-income-tax states to make up for lost revenue. |

| Sales and Excise Taxes | Usually ignored during initial planning. | Higher base rates and broader applications tax your daily consumption heavily. |

| Insurance Premiums | Assumed to be similar to current home state. | Catastrophic weather risks push premiums to record highs, functioning like a hidden property tax. |

Do not base a major relocation solely on one line item of your budget. Evaluate the total tax burden, the local cost of healthcare, and the proximity to your family support system before making a move.

4. Turning a Beloved Hobby Into a Full-Time Business

Retirement provides the time you never had during your working years to pursue your passions. Many retirees decide to monetize those passions. Whether it involves opening a boutique bakery, offering consulting services in your former industry, or turning woodworking into a retail operation, starting a business sounds like the perfect blend of income and personal fulfillment.

The trap lies in underestimating the difference between a hobby you do for relaxation and a business you run for profit. A hobby allows you to stop when you feel tired; a business demands relentless marketing, accounting, inventory management, and customer service. Taking on the stress of supply chain issues, demanding clients, and tax compliance often destroys the joy the activity once brought you.

More dangerously, funding a startup frequently requires tapping into your retirement nest egg. Small businesses carry extremely high failure rates. Pouring your hard-earned capital into an untested venture puts your baseline financial security at immense risk.

“If you are going to invest your retirement money into a new business, you have to be fully prepared to lose every single penny of it. Do not risk the money you need to keep a roof over your head and food on your table.” — Suze Orman, Financial Expert and Author

If you want to monetize a hobby, treat it as a micro-business. Keep overhead practically non-existent, avoid borrowing money, and never dip into your primary retirement accounts to fund its growth.

5. Moving to a Remote, Picturesque Dream Town

Retirees often dream of escaping the noise, traffic, and high costs of urban living by purchasing a cabin in the mountains or a quiet home in a secluded coastal village. The appeal of a slower pace, abundant nature, and a tight-knit small community strongly resonates after decades spent navigating rush hour and corporate stress.

While the scenery provides peace, the isolation introduces severe logistical risks as you age. The most critical factor in retirement living is access to high-quality healthcare. Remote towns rarely support specialized medical facilities or level-one trauma centers. A heart condition, joint replacement, or neurological issue will require you to drive hours to a major city for specialized care, a journey that becomes increasingly difficult in your seventies and eighties.

Furthermore, remote living often leads to profound social isolation. Leaving behind your established network of friends, former colleagues, and familiar community groups forces you to build a new social circle from scratch. Winter weather or declining driving ability can leave you physically trapped in your secluded home. A highly recommended alternative involves downsizing to a quieter suburb situated just outside a major metropolitan area, giving you access to nature without severing your lifeline to top-tier medical facilities and diverse social opportunities.

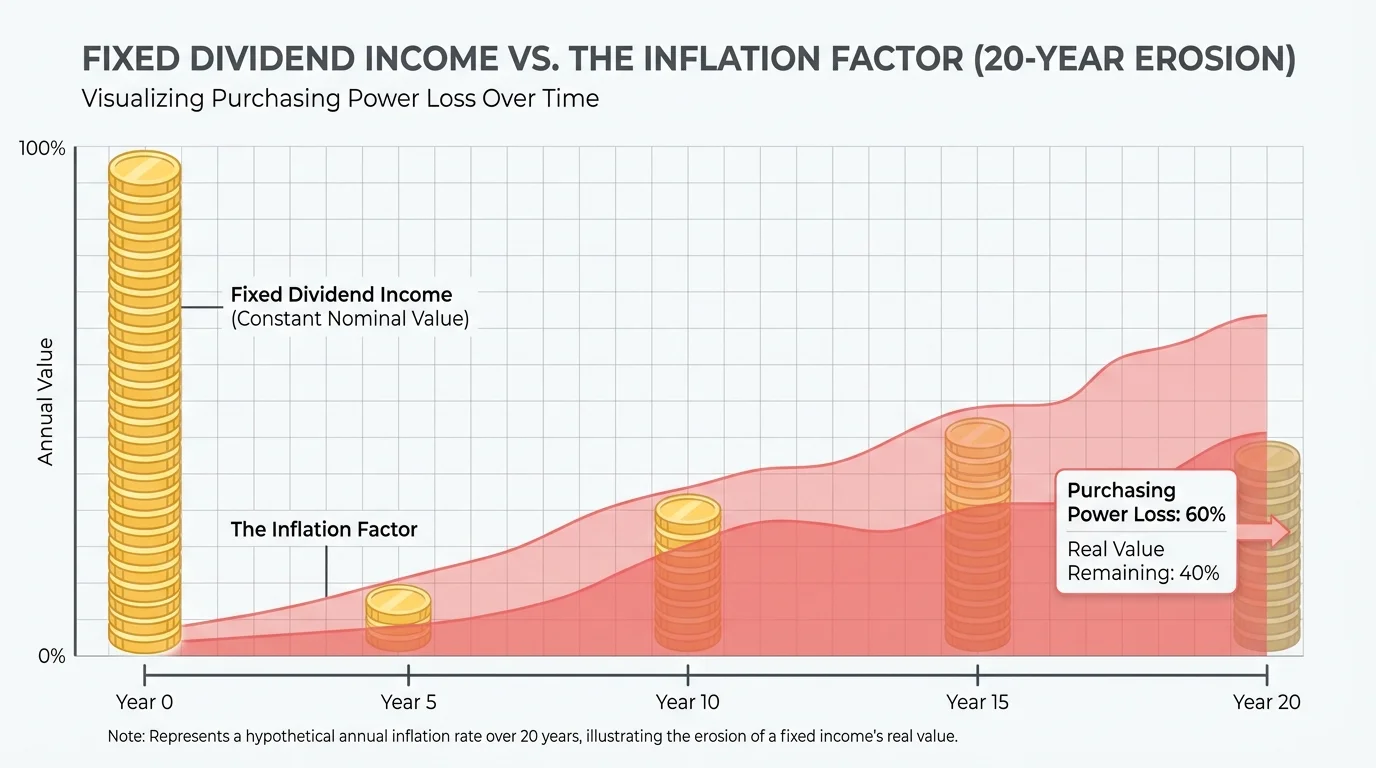

6. Living Entirely Off Dividends Without Touching the Principal

The strategy of living entirely on the interest and dividends generated by an investment portfolio, deliberately refusing to ever touch the principal balance, stands as a legacy goal for many conservative investors. It sounds incredibly safe. You preserve the core wealth to pass down to your heirs while skimming the top off the market to fund your lifestyle.

Implementing this strategy today requires an astronomical portfolio balance. Because standard dividend yields on high-quality companies typically hover between two and three percent, generating $60,000 in annual income requires a multi-million-dollar portfolio. To compensate for a smaller nest egg, retirees often fall into the trap of “chasing yield”—shifting their money out of broad, diversified index funds and into high-risk, high-yield alternative assets or heavily leveraged companies.

Additionally, this strategy ignores the devastating long-term impact of inflation. If you refuse to sell shares to increase your cash flow, your fixed dividend income will buy significantly less ten or twenty years into retirement. Modern financial planning embraces a total return approach. Liquidating a small percentage of your capital gains alongside collecting dividends provides a safer, more realistic way to fund your life without taking on extreme portfolio risk.

7. Banking on an Inheritance to Fund Your Lifestyle

Knowing that your parents built significant wealth can create a false sense of security regarding your own retirement. Pre-retirees who fall behind on their savings goals often rationalize the shortfall by assuming a substantial inheritance will arrive exactly when they need it, bridging the gap between their meager savings and their desired lifestyle.

Banking on money that you do not yet possess is a catastrophic financial mistake. People live much longer today than in previous generations, meaning your parents will need their wealth to sustain themselves for decades. More importantly, the staggering costs associated with end-of-life medical care can rapidly liquidate even the most robust estates. According to data from the Administration for Community Living, someone turning 65 today has almost a 70% chance of needing some type of long-term care services in their remaining years.

Consider the myriad ways an expected inheritance can vanish:

- Memory Care and Nursing Facilities: High-quality facilities easily cost over $100,000 per year, quickly draining liquid assets and forcing the sale of family real estate.

- In-Home Nursing Care: Round-the-clock home health aides can exceed the cost of institutional care over a multi-year physical decline.

- Market Volatility: A poorly timed market crash during your parents’ later years can permanently reduce the estate’s value.

- Remarriage and Changing Wills: Family dynamics shift. A surviving parent who remarries may alter their estate plan, directing assets to a new spouse rather than adult children.

Build your retirement plan based entirely on your own assets and projected Social Security benefits. Treat any potential inheritance as an unexpected bonus rather than a foundational pillar of your financial survival.

8. Flipping Real Estate to Generate Supplemental Income

Popular television networks make flipping houses look like a fast, straightforward way to generate massive influxes of cash. Retirees looking for a project that utilizes their handyman skills and generates high returns often view real estate flipping as the perfect semi-retirement gig. You buy a distressed property, fix it up over a few months, and sell it for a handsome profit.

The camera rarely shows the crushing reality of real estate speculation. Flipping houses is incredibly capital intensive. It ties up massive amounts of your liquid retirement savings in a highly illiquid asset. If the local housing market cools down while you are holding the property, you can easily end up underwater, unable to recoup your initial investment.

Beyond market risk, flipping houses demands immense physical labor. Demolition, flooring, and landscaping place intense strain on aging joints and muscles. If you outsource the labor to general contractors to save your back, your profit margins shrink drastically. You also face carrying costs—property taxes, utilities, and specialized builder’s risk insurance—that drain your cash flow every month the house sits unsold. For retirees seeking exposure to real estate without the physical labor or concentrated risk, investing in highly liquid Real Estate Investment Trusts (REITs) provides a much smarter alternative.

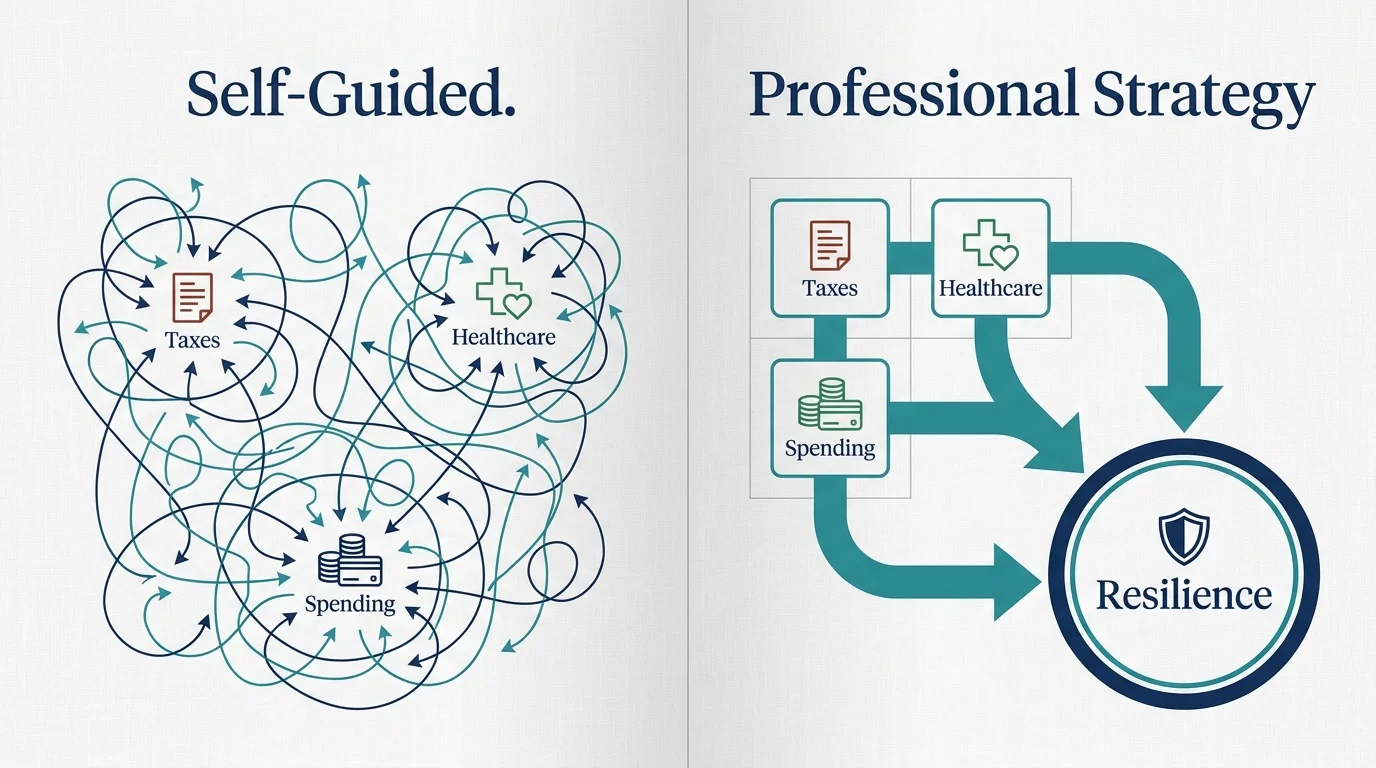

Professional vs. Self-Guided Retirement Adjustments

Navigating the transition into retirement involves complex decisions surrounding taxes, healthcare coverage, and withdrawal rates. Determining whether to manage these moving parts yourself or hire a professional depends heavily on your financial literacy and emotional discipline.

When to handle it yourself: If your financial picture consists entirely of a straightforward 401(k), basic Social Security benefits, and a paid-off primary residence, you can likely manage your own plan. Utilizing low-cost target-date funds and accessing free educational resources from federal agencies allows you to efficiently self-manage a simple portfolio.

When to hire a professional: You should consult a fiduciary advisor if your situation involves multiple income streams, real estate investments, complex tax planning, or small business ownership. A professional proves invaluable when deciding exactly which accounts to draw down first to minimize your lifetime tax burden.

When navigating Medicare options: Healthcare planning requires specialized knowledge. Comparing traditional Medicare with supplemental policies against various Medicare Advantage plans often necessitates guidance from an independent, localized insurance broker who understands the specific medical networks in your county.

If you choose to hire an expert, always seek out a fee-only fiduciary. Resources provided by organizations like the Certified Financial Planner Board help you verify credentials and ensure the advisor is legally obligated to act in your best financial interest.

Common Mistakes to Avoid

Even if you avoid the eight major pitfalls outlined above, subtle errors can still derail your lifestyle. Protect your peace of mind by actively managing these common blind spots.

First, never make permanent, irreversible financial decisions based on temporary emotional states. The exhaustion you feel during your final year of work might tempt you to sell everything and move to a remote island, but that fatigue will pass. Give yourself a cooling-off period before executing massive lifestyle changes. Ease into retirement by testing your new routines and locations before fully committing your capital.

Second, stop ignoring the impact of inflation on your daily living expenses. Retirees frequently project their current grocery, fuel, and utility bills thirty years into the future without applying a realistic inflation multiplier. A lifestyle that costs $5,000 a month today will cost significantly more two decades from now. Ensure your portfolio maintains enough exposure to growth assets, like equities, to outpace the rising cost of goods and services.

Your retirement should represent a period of profound freedom, but lasting freedom requires careful, realistic planning. Avoid the temptation of strategies that promise easy wealth or perfect isolation, and instead focus on building a resilient, adaptable framework. Test your lifestyle ideas through short-term rentals or trial periods, and ensure your investment portfolio accurately reflects the mathematical realities of inflation and total return.

This article provides general retirement education and information only. Every retiree’s situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: May 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply