Packing up your life and moving to a new destination represents one of the most exciting opportunities in retirement, but it also carries significant financial and emotional risks. A poorly planned relocation can quickly drain your retirement savings, disrupt your healthcare coverage, and leave you feeling isolated. Avoiding common retirement relocation mistakes requires looking past the glossy brochures of 55-plus communities and critically evaluating how a new zip code impacts your daily reality. Whether you are craving warmer weather, lower taxes, or proximity to grandchildren, careful preparation prevents expensive reversals. By understanding the typical missteps retirees make when changing addresses, you can confidently choose a location that supports both your financial goals and your long-term wellbeing.

Mistake 1: Treating a Vacation Destination Like a Year-Round Home

Many retirees fall in love with a location during a two-week vacation. You experience the perfect weather, eat at fantastic restaurants, and enjoy the relaxed pace of life. However, visiting a place as a tourist is entirely different from residing there as a full-time local.

When you vacation, you generally experience a location during its peak season. If you move to a coastal town in the Southeast based on how it feels in March, you might be unprepared for the oppressive heat, humidity, and hurricane threats of August. Conversely, a charming mountain town that feels magical during a crisp October getaway can become incredibly isolating during a brutal, snow-filled February.

To avoid this mistake, commit to a long-term trial run before buying property. Rent a furnished home in your target destination for at least three to six months, intentionally timing your stay to overlap with the area’s worst weather season. This extended stay allows you to experience the day-to-day realities of the community. You will discover how long it actually takes to get to the grocery store, whether the local healthcare facilities meet your standards, and if the off-season lifestyle still appeals to you once the tourist attractions close down.

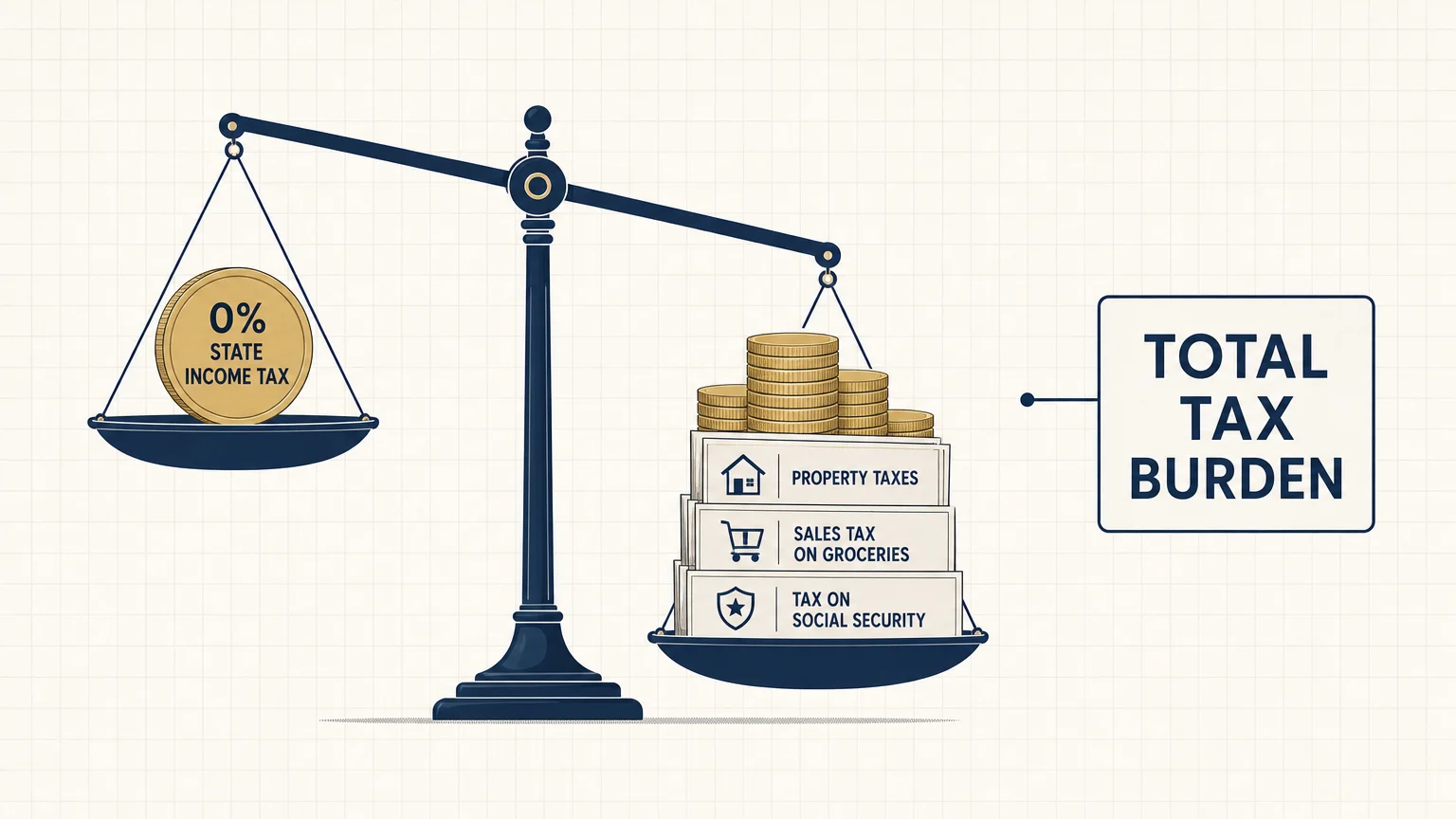

Mistake 2: Focusing Narrowly on Income Tax (and Ignoring the Total Tax Burden)

Moving to a state with no income tax—such as Florida, Texas, or Nevada—sounds like an immediate financial win. The prospect of keeping more of your hard-earned pension or investment withdrawals draws thousands of retirees across state lines every year. Yet, states must generate revenue somehow, and they often compensate for the lack of an income tax by levying heavy taxes elsewhere.

When evaluating the financial viability of a new location, you must calculate your total estimated tax burden. A state with no income tax might have exorbitant property taxes that easily wipe out any savings you gained on your income. Sales taxes also play a crucial role; some states tax groceries and prescription drugs, which make up a significant portion of a typical retiree’s budget.

Furthermore, you need to understand how a prospective state treats your specific types of retirement income. Some states tax Social Security benefits, while others exempt them. The treatment of military pensions, government pensions, and 401(k) withdrawals varies wildly across the country. Before making a move, lay out a mock tax return for your prospective state. By factoring in property, sales, and specific retirement income taxes, you gain a clear, mathematical picture of the actual cost of living.

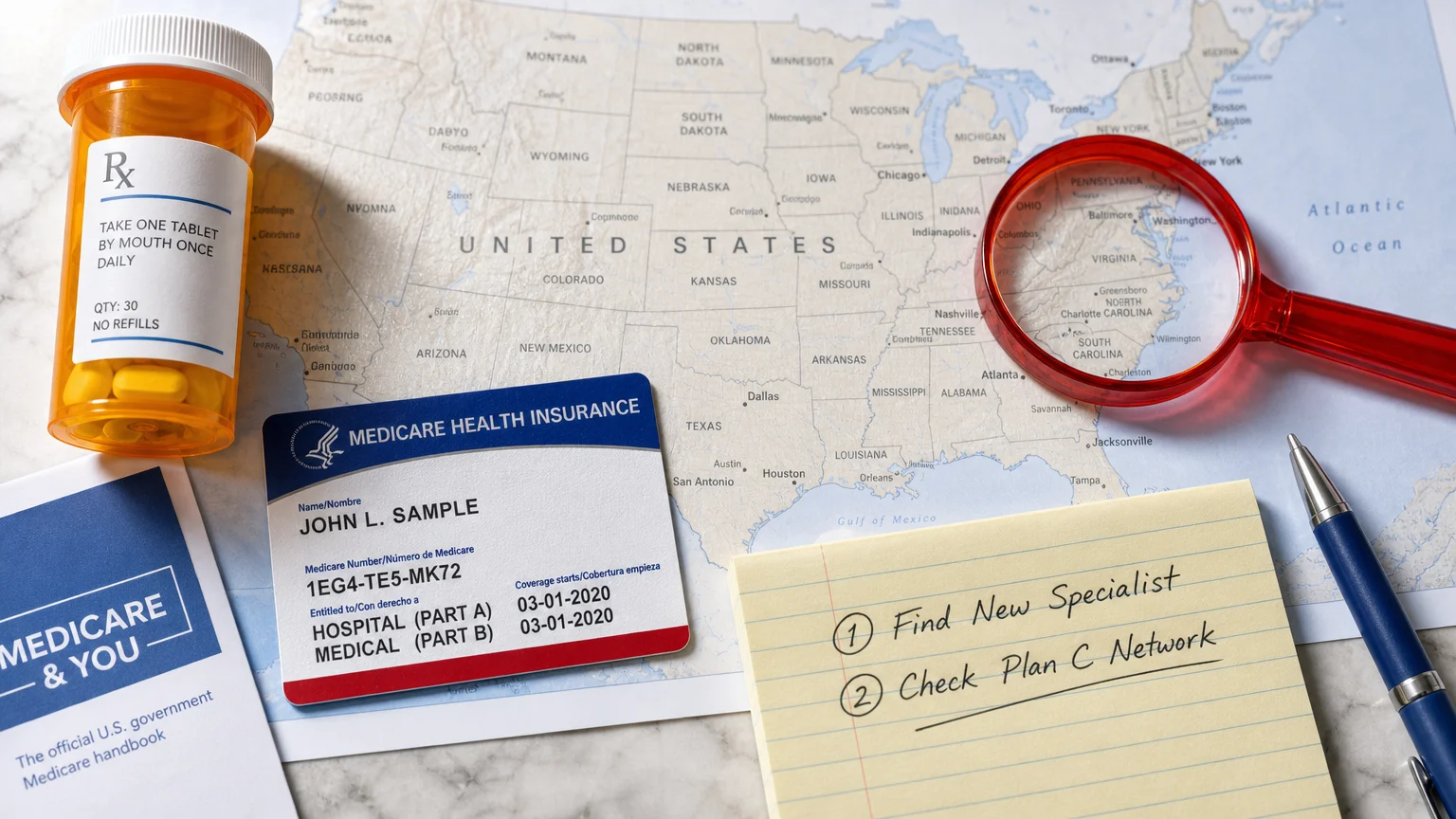

Mistake 3: Overlooking the Complexities of Healthcare Transitions

Healthcare requires rigorous planning when you relocate, yet many retirees leave this crucial element as an afterthought. If you are enrolled in Original Medicare (Part A and Part B), you can see any doctor or visit any hospital in the United States that accepts Medicare. However, if you rely on a Medicare Advantage plan (Part C) or a standalone prescription drug plan (Part D), moving out of your plan’s service area triggers a cascade of necessary changes.

Medicare Advantage plans operate on localized networks of doctors and hospitals. When you move to a new state—or even a new county within the same state—your current plan will likely not follow you. Moving out of your plan’s service area qualifies you for a Special Enrollment Period (SEP). You must use this window to enroll in a new plan, or you risk losing your coverage and facing late enrollment penalties. Resources available through Medicare.gov can help you compare plans in your new zip code before you pack your bags.

Beyond insurance logistics, you must evaluate the actual medical infrastructure of your destination. A secluded cabin in the woods offers wonderful peace and quiet, but it becomes a massive liability if you require specialized cardiac care and the nearest major hospital is two hours away. Look closely at the proximity of highly rated specialists, emergency response times, and the availability of home healthcare aides in the region you are considering.

Mistake 4: Relocating Solely to Follow Adult Children

The desire to watch your grandchildren grow up is a powerful and entirely understandable motivation for moving. Countless retirees uproot their lives to be five minutes away from their adult children. While this works beautifully for some, it ranks as one of the most frequently regretted retirement relocation strategies.

The modern workforce is highly mobile. You might sell your home, buy a new one near your daughter, and spend a year settling in—only to have her employer transfer her to another state six months later. Suddenly, you are left in an unfamiliar city without your primary support network.

Even if your children never move, their busy lives revolving around careers and their kids’ extracurricular activities mean they may not have as much free time to spend with you as you envision. If you relocate to be near family, ensure the destination appeals to you independently. Ask yourself: If my children had to move away next year, would I still want to live in this town? You must build your own social life, find your own hobbies, and connect with the community outside of your family circle.

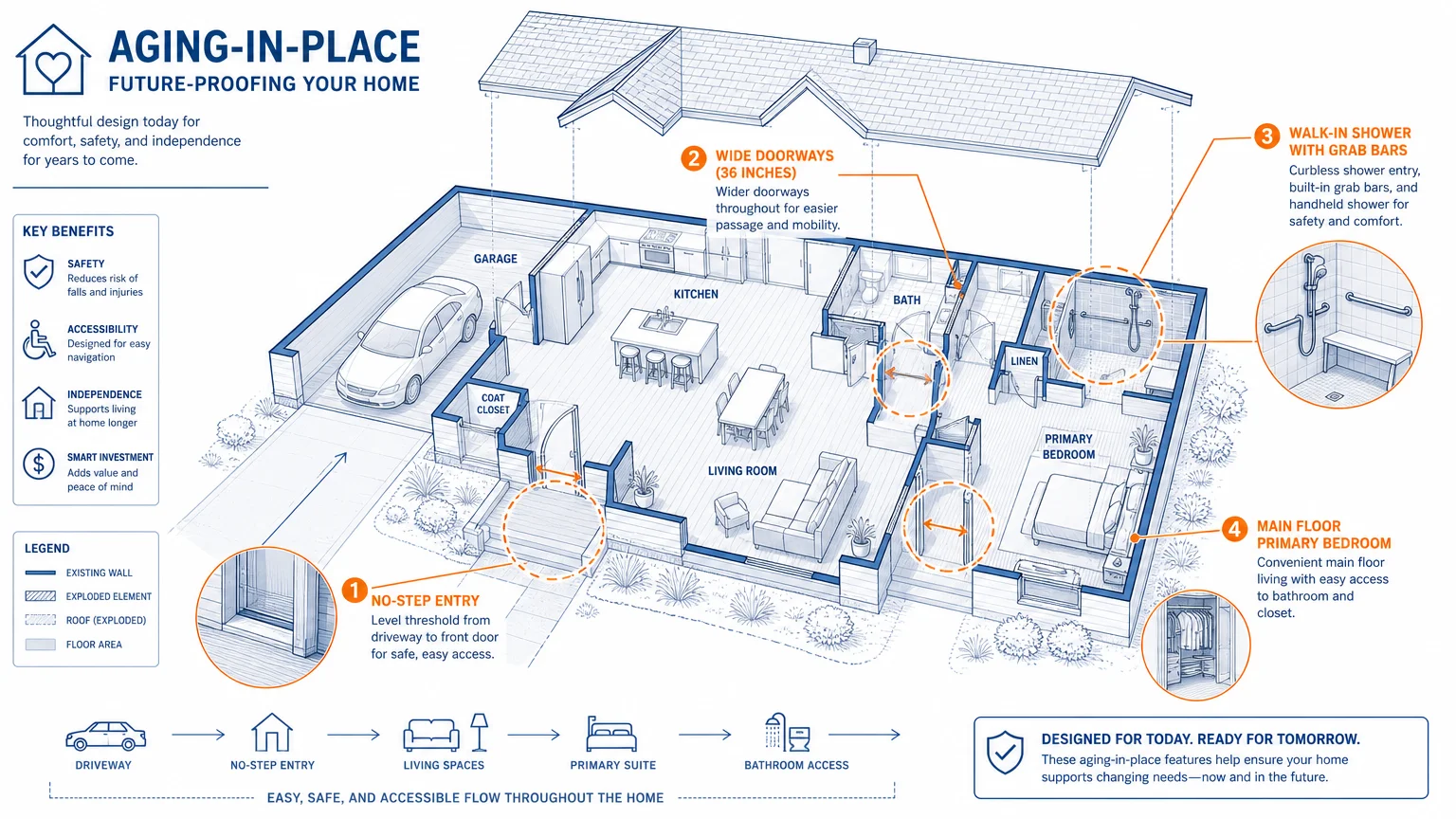

Mistake 5: Failing to Anticipate Long-Term Mobility and Aging Needs

The home you buy at age 65 needs to serve you well at age 85. When touring potential retirement homes, it is easy to fall in love with a multi-story historic house or a property featuring a steeply terraced garden. Unfortunately, physical mobility tends to decline as we age, turning charming architectural features into daily hazards.

A successful relocation anticipates your future physical requirements. Look for single-level living arrangements or homes where the primary bedroom, a full bathroom, and the laundry facilities are all on the ground floor. Check for step-free entryways and wider doorways that can accommodate walkers or wheelchairs if necessary.

Mobility extends beyond the walls of your home; it includes your ability to navigate the community. If your new neighborhood requires a car for every single errand, you could face severe isolation if your vision or reflexes eventually force you to stop driving. Evaluate the walkability of the neighborhood. Research the local public transportation options, ride-share availability, and community transit services designed specifically for seniors. Moving to an area with robust transportation alternatives preserves your independence long after you hand over your car keys.

Mistake 6: Downsizing Without Calculating the Hidden Costs of New Real Estate

Downsizing from a large family home to a smaller condo or patio home naturally seems like a money-saving strategy. A smaller footprint means lower utility bills and less maintenance, right? While generally true, the hidden costs of your new property can quickly eat into the equity you freed up by selling your previous home.

Many popular retirement communities operate under strict Homeowners Associations (HOAs). These organizations manage the exterior maintenance, landscaping, and community amenities. While convenient, HOA fees can be shockingly high and are subject to regular, sometimes steep, increases. Furthermore, special assessments—sudden bills levied on all residents to pay for major community repairs like a new roof or road repaving—can cost you thousands of dollars out of pocket with little warning.

Insurance premiums present another massive hidden cost, particularly if you are relocating to coastal states or regions prone to wildfires. Retirees moving to Florida, California, or coastal Carolinas frequently experience sticker shock when securing homeowners insurance. In some high-risk areas, securing coverage requires multiple expensive policies, including separate windstorm and flood insurance. Before committing to a purchase, consult resources from the Consumer Financial Protection Bureau to understand the full scope of property ownership costs, and obtain hard insurance quotes for the specific address you intend to buy.

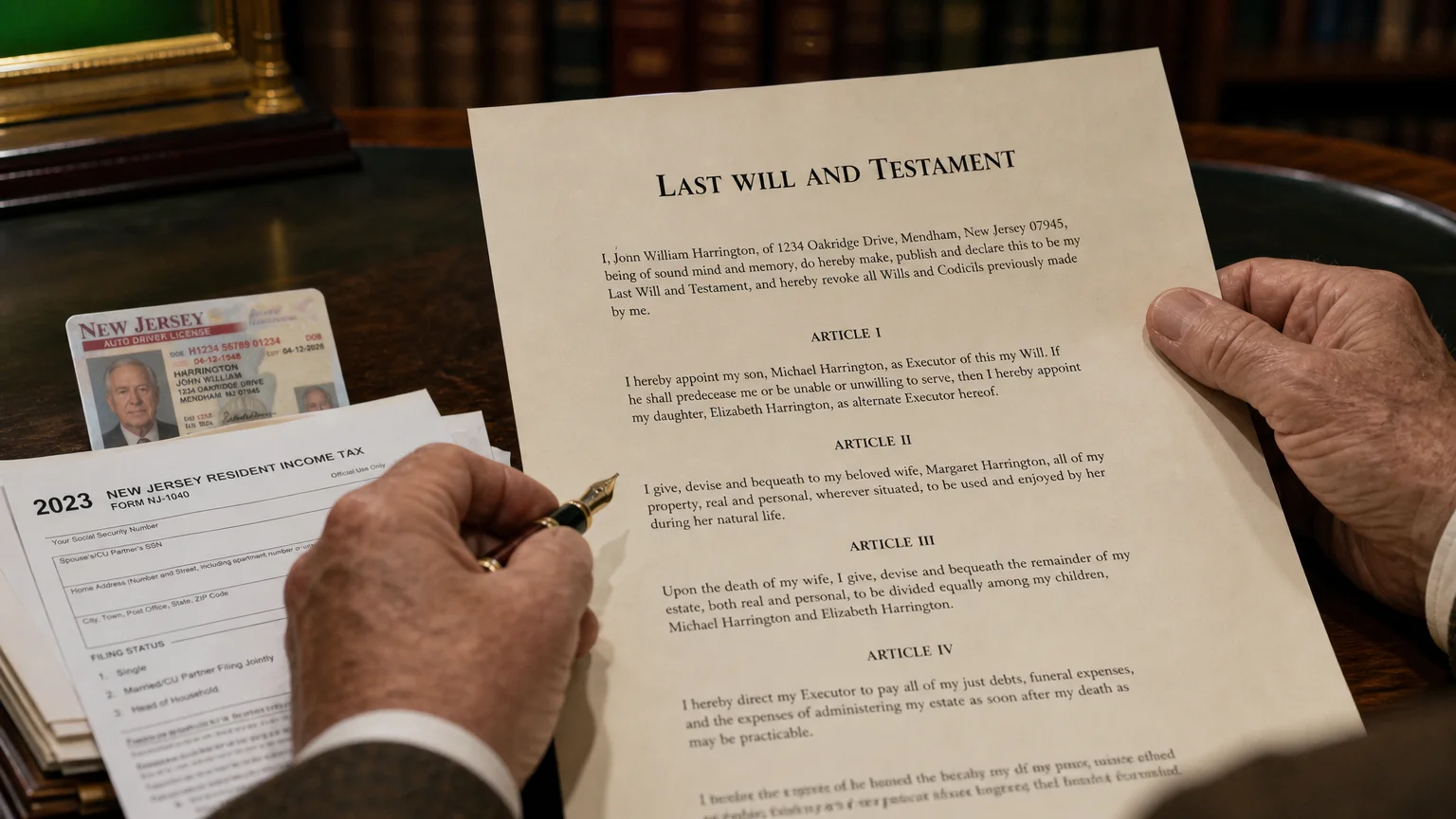

Mistake 7: Neglecting to Update Estate Plans for Your New State

Estate planning laws are dictated at the state level, not the federal level. The will, trust, and power of attorney documents you carefully drafted in Illinois might not be interpreted the same way if you establish residency in Arizona. Failing to update these critical documents ranks among the most legally hazardous relocation mistakes.

For example, if you move from a common law state to a community property state, the rules governing how your assets are owned and distributed after death change dramatically. State laws also dictate exactly how a power of attorney must be worded, witnessed, and notarized to be legally binding. If you suffer a medical emergency in your new state and your advance healthcare directive does not meet local legal standards, your family could face immense bureaucratic hurdles when trying to make decisions on your behalf.

Treat estate plan updates as an essential part of your moving checklist. Within a few months of establishing your new residency, hire a local estate planning attorney to review your existing documents. Often, a few simple amendments can align your plans with the laws of your new state, ensuring your legacy and healthcare wishes remain fully protected.

Mistake 8: Underestimating the Emotional Toll of Rebuilding Your Network

The financial and logistical components of moving often overshadow the psychological impact of uprooting your life. Over decades in your current town, you have woven a dense fabric of relationships and routines. You have a favorite grocery clerk, a mechanic who knows your car’s history, a trusted dentist, and neighbors who keep an eye on your house when you travel.

When you move, you lose that entire support system overnight. The isolation that follows a major relocation can trigger significant depression and anxiety for retirees. Making friends as an older adult requires much more deliberate effort than it did when you had a busy workplace or school-aged children forcing you into social interactions.

“The best retirement plan is one that focuses on maximizing your return on life, not just your return on investment.” — Mitch Anthony, Retirement Expert

To mitigate this emotional toll, you must approach socialization as a job during your first year in a new location. Research local volunteer opportunities, community centers, and special interest clubs before you even move. Check out organizations like AARP to find local chapters and events in your new area. Force yourself to say “yes” to invitations, introduce yourself to your new neighbors, and actively participate in the community. Rebuilding your network takes time, patience, and a willingness to put yourself out there.

Comparing Relocation Strategies

Before you commit to a cross-country move, weigh the benefits and drawbacks of your various housing options. Sometimes, the best move is no move at all, or a smaller shift within your current community.

| Strategy | Cost Predictability | Healthcare Continuity | Social Network Impact | Estate Planning Impact |

|---|---|---|---|---|

| Staying Put (Aging in Place) | High: Mortgages are often paid off; taxes are known. Remodeling for mobility may require upfront cash. | Excellent: You keep your established doctors, specialists, and current Medicare plans. | None: You maintain your lifelong friendships, routines, and community ties. | None: Existing legal documents remain fully valid and effective. |

| Downsizing Locally | Medium: Frees up home equity, but introduces new transaction costs, moving fees, and potential HOAs. | Excellent: You remain in the same geographic network for providers and insurance. | Low: You keep your friends and routines, though your immediate neighbors will change. | Minimal: A change of address is needed, but the governing state laws remain identical. |

| Out-of-State Relocation | Low: Subject to unfamiliar property taxes, diverse state income taxes, and changing insurance markets. | Disruptive: Requires finding entirely new doctors and triggering a Medicare Special Enrollment Period. | High: Complete disruption of your social circle; requires intentional effort to rebuild community. | High: Demands a comprehensive legal review to ensure documents comply with the new state’s laws. |

Pitfalls to Watch For During the Physical Move

Even if you select the perfect location and run the numbers flawlessly, the physical act of moving presents its own set of distinct hazards. Retirees are frequently targeted by moving scams. Rogue moving companies may offer an unbelievably low initial estimate, load all your worldly possessions onto a truck, and then hold your items hostage until you pay drastically inflated, unapproved fees.

Always hire licensed, bonded, and insured movers. Verify a prospective moving company’s credentials through the Federal Motor Carrier Safety Administration (FMCSA). Request in-home, binding estimates rather than quotes provided solely over the phone or internet.

Additionally, evaluate your moving insurance options carefully. Standard released-value protection typically covers a minuscule fraction of your belongings’ true worth—often just 60 cents per pound per item. This means if a mover drops your lightweight, expensive flat-screen television, you will receive just a few dollars in compensation. Invest in full-value protection coverage, especially if you are transporting family heirlooms, antiques, or valuable art collections.

Getting Expert Help

A major retirement relocation involves too many moving parts to manage entirely on your own. Engaging the right professionals can save you from costly missteps.

- Certified Financial Planner (CFP): A fiduciary advisor can run long-term cash flow projections based on the cost of living and tax structures of your target state. They ensure the move will not prematurely deplete your portfolio.

- Seniors Real Estate Specialist (SRES): This specific designation means a real estate agent has specialized training in the needs of buyers over the age of 50. They understand the nuances of reverse mortgages, universal design, and the financial transitions of retirement housing.

- Independent Medicare Broker: Navigating health insurance across state lines is incredibly complex. A licensed broker can map out your Medicare Advantage or Part D transition, ensuring you avoid penalties and maintain coverage during your move.

- Local Estate Planning Attorney: Once you arrive in your new state, this professional will adapt your will, trust, and advanced directives to comply with local statutes.

Frequently Asked Questions About Retirement Relocation

Does moving to a different state affect my Social Security payments?

No, your gross federal Social Security benefit remains exactly the same regardless of where you live in the United States. However, your net income might change. Different states have varying rules regarding the taxation of Social Security benefits. Some states tax a portion of it, while the majority do not. Make sure to update your address directly with the Social Security Administration to ensure uninterrupted delivery of important tax documents.

Can I keep my Medicare Advantage plan if I move out of state?

Generally, no. Medicare Advantage plans and standalone Medicare Part D prescription drug plans are based on regional networks. If you permanently move outside of your plan’s service area, you qualify for a Special Enrollment Period to choose a new plan in your new location. If you do not enroll in a new plan, you will automatically be returned to Original Medicare.

How long should I rent in a new retirement location before buying?

Most experts recommend renting for at least six to twelve months. This duration allows you to experience the area through multiple seasons, build an initial social network, and explore different neighborhoods without the pressure of a rushing into a real estate transaction. It acts as an affordable insurance policy against buyer’s remorse.

Relocating in retirement offers a brilliant chance to intentionally design the next chapter of your life. While the logistical hurdles are significant, they are entirely manageable with clear-eyed planning and a methodical approach. Focus on the total cost of living rather than just income taxes, secure your healthcare transitions, and prioritize your social and emotional needs just as highly as the financial ones.

By taking the time to test your new location and relying on qualified professionals to guide your housing and healthcare decisions, you position yourself to thrive in your new home. This article provides general retirement education and information only. Every retiree’s situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: March 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply