Trading a high-cost American lifestyle for a sun-drenched terrace in Portugal or a mountain vista in Panama sounds like the ultimate retirement dream. Deciding to retire abroad offers a legitimate path to stretch your savings, access affordable healthcare, and experience a vibrant new culture during your later years. However, the reality of expat retirement requires navigating complex visas, unexpected tax obligations, and major shifts in your medical strategy. While you can certainly retire cheaper abroad, moving overseas demands rigorous financial planning and emotional resilience. This guide breaks down exactly what living overseas 60+ entails—from securing your Social Security benefits across borders to managing the psychological impact of leaving home—so you can confidently plan your international retirement.

The Financial Mechanics of an International Retirement

Moving your life across borders changes everything about how you manage your money. Many Americans assume that a lower cost of living automatically translates to financial freedom. While a geographic arbitrage strategy can stretch your dollars significantly, the mechanics of international finance introduce new variables that require ongoing management.

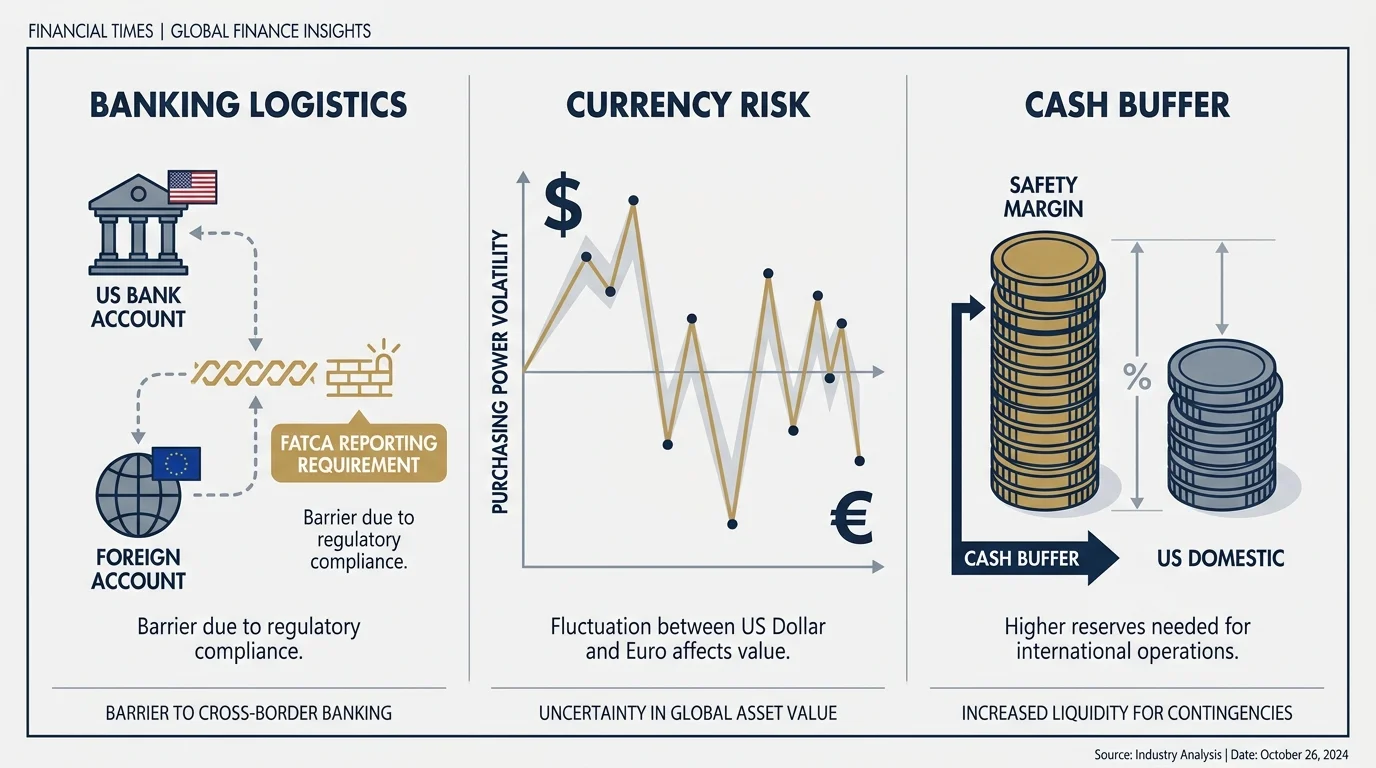

One of the first logistical hurdles you will face is banking. Because of the Foreign Account Tax Compliance Act (FATCA), many foreign financial institutions are hesitant to open accounts for US citizens. The reporting requirements are so burdensome for foreign banks that some simply refuse American clients. To navigate this, you will need to research which local banks in your destination country actively work with expats. Furthermore, maintaining a US bank account becomes crucial, yet many American banks will close your account if they detect you no longer have a physical US address. Savvy expats often use the address of a trusted family member or a specialized mail-forwarding service to keep their US financial infrastructure intact.

Currency risk is another silent threat to your retirement budget. If your income is in US dollars but your daily living expenses are in Euros, Pesos, or Colones, your purchasing power will fluctuate daily. A strong dollar makes you feel wealthy; a weak dollar can suddenly tighten your budget by ten or twenty percent without a single change in your spending habits. To manage this, you must build a larger cash buffer than you would at home. Investopedia provides comprehensive guidance on understanding currency risk, which is essential reading before committing your entire pension to a foreign economy.

Collecting Social Security Overseas

The good news is that you can receive your Social Security retirement benefits in most countries around the world. The Social Security Administration regularly sends payments to hundreds of thousands of beneficiaries living outside the United States. Your payments can be deposited directly into a US bank account, or, in many countries, directly into a foreign financial institution.

However, there are a few restricted countries—such as Cuba and North Korea—where the SSA cannot send payments. Additionally, countries with specific banking sanctions might require you to meet special conditions to access your funds. If you plan to be among the growing number of retire abroad Americans, you should review the Social Security Administration’s international payments guide to verify the exact rules for your chosen destination. You must also regularly fill out and return a “Foreign Enforcement Questionnaire” to prove you are still eligible to receive benefits; failing to return this form will result in suspended payments.

The Healthcare Shock: Leaving Medicare Behind

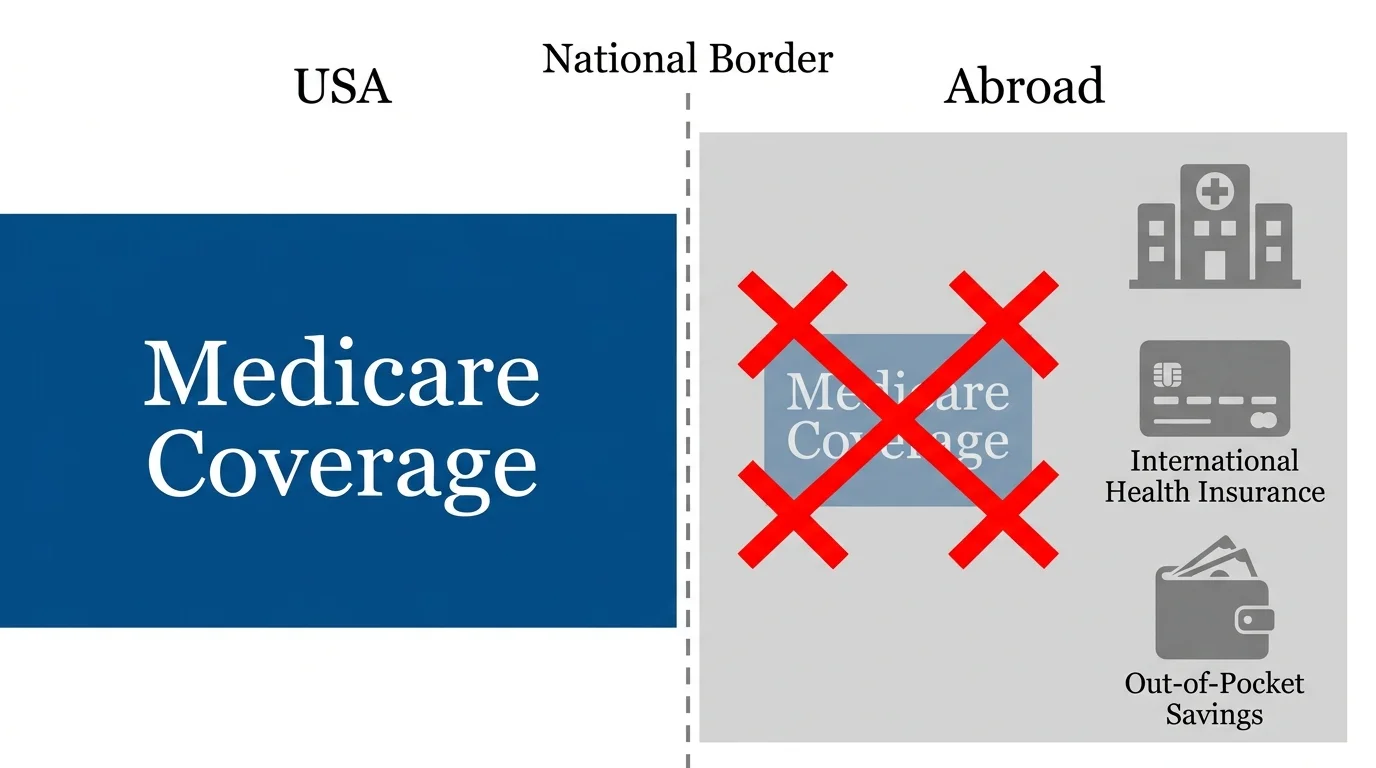

Perhaps the single biggest adjustment for Americans living overseas 60+ is healthcare. In the United States, Medicare is the cornerstone of senior healthcare planning. Once you cross international borders, that safety net disappears.

Medicare generally does not cover medical care outside the United States or its territories. This reality forces expats to develop a completely new healthcare strategy. Dropping your Medicare Part B coverage might seem like a smart way to save on monthly premiums since you cannot use it abroad. However, doing so carries a massive risk. If you ever decide to return to the United States—perhaps due to a health crisis that local foreign facilities cannot handle—you will face a lifetime late-enrollment penalty of 10% for every full 12-month period you were eligible for Part B but did not enroll. Many retirees choose to pay their Medicare Part B premiums while living abroad simply as an insurance policy for their eventual return.

To replace Medicare in your host country, you generally have three options:

- National Public Healthcare: Many popular retirement destinations, such as Spain, Portugal, and Costa Rica, offer excellent public healthcare systems. Once you become a legal resident, you can often buy into these systems for a modest monthly fee. These systems usually cover everything from routine visits to major surgeries, though wait times for non-emergency procedures can be longer than what you are accustomed to in the US.

- Private International Insurance: If you prefer to bypass public system wait times or want the comfort of English-speaking doctors in premium facilities, private international health insurance is the answer. While policies are much cheaper than equivalent private insurance in the US, premiums increase substantially as you age. Furthermore, unlike the Affordable Care Act in America, foreign private insurers can and often do deny coverage for pre-existing conditions.

- Paying Out of Pocket: In countries where the cost of medical care is exceptionally low—such as Mexico, Panama, or Thailand—some retirees choose to self-insure. They pay cash for routine care and minor emergencies, relying on medical evacuation insurance to fly them back to the US for major, catastrophic events where their Medicare coverage will kick in.

“By failing to prepare, you are preparing to fail.” — Benjamin Franklin, Founding Father

Franklin’s wisdom applies perfectly to international healthcare. Do not assume that out-of-pocket costs will always be manageable just because routine dental work is cheap. A comprehensive health strategy is non-negotiable for a successful international retirement.

Securing Your Right to Stay: Visas and Residency Requirements

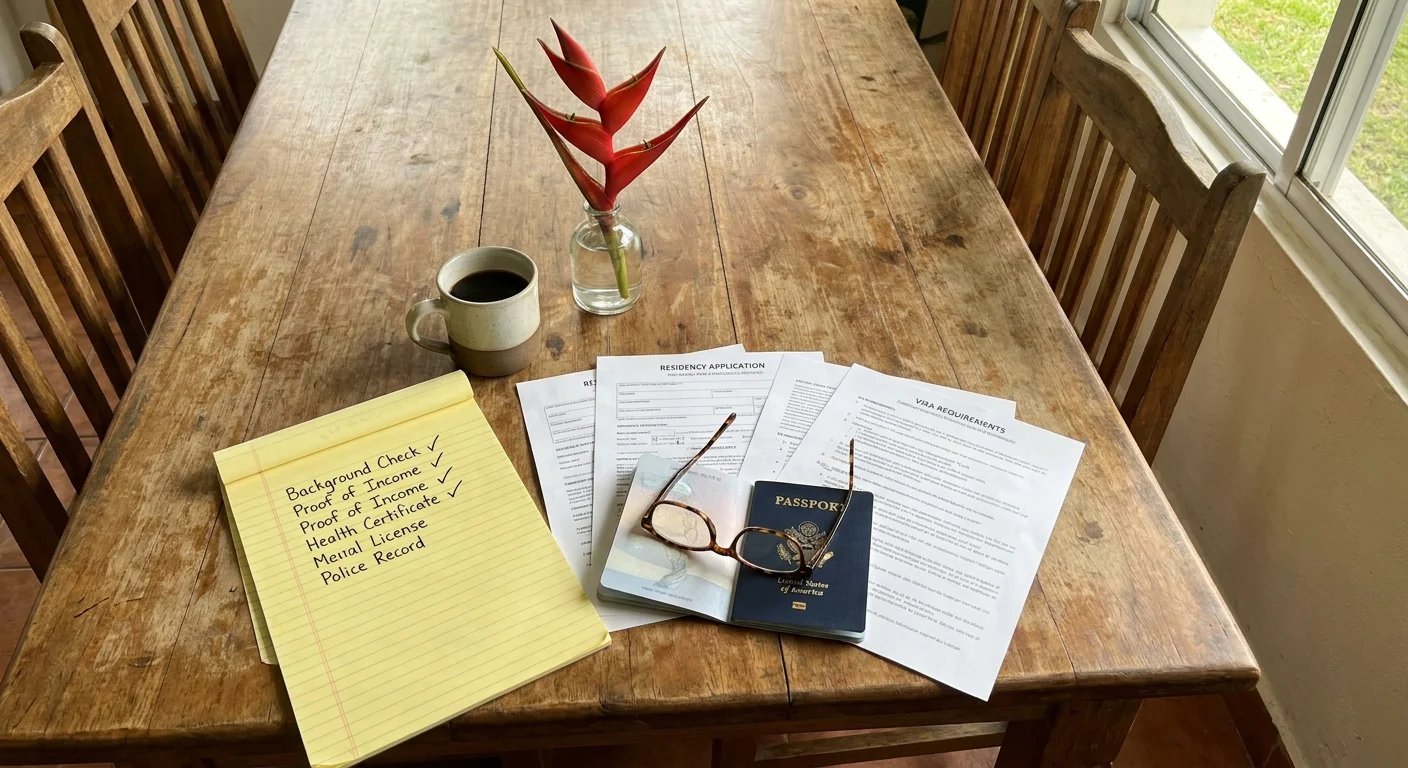

You cannot simply pack your bags and move to a foreign country on a tourist visa permanently. Every country has strict immigration laws, and violating them by overstaying your tourist allowance can result in deportation and lifetime bans. To retire legally, you must qualify for a residency visa.

Fortunately, many countries actively court foreign retirees because they bring stable, passive income into the local economy. These “retirement visas” generally require you to prove a guaranteed minimum monthly income. For example, Panama’s famous Pensionado visa requires proof of a lifetime monthly pension or Social Security income of at least $1,000. In exchange, residents receive permanent status and a suite of discounts on everything from utility bills to airline tickets and restaurant meals.

Portugal’s D7 visa is another incredibly popular option. It requires applicants to demonstrate sufficient passive income to support themselves, which is tied to the Portuguese minimum wage. While the income thresholds are generally low by US standards, the paperwork process can be grueling. You will need FBI background checks, apostilled birth certificates, proof of local housing, and comprehensive health insurance just to apply.

Before committing to a country, thoroughly research its residency requirements. Some nations require you to deposit a large lump sum in a local bank, while others might only grant temporary residency that must be renewed annually for several years before permanent residency is achieved.

The Tax Reality of Expat Retirement

One of the most persistent myths about an expat retirement is that moving abroad allows you to escape the Internal Revenue Service. This is completely false. The United States is one of the only countries in the world that taxes its citizens based on citizenship, not geography. As long as you hold a US passport, you must file a US tax return every year, reporting your worldwide income.

While the Foreign Earned Income Exclusion (FEIE) allows working expats to exclude a significant portion of their salary from US taxes, this exclusion does not apply to passive income. Your Social Security, pension payouts, IRA withdrawals, and capital gains are not considered “earned income.” Therefore, they remain taxable by the US government just as if you were living in Ohio or Texas.

In addition to US taxes, you may also become a tax resident of your host country. Countries like Spain and France tax residents on their global income, meaning you could face taxation from both nations. Fortunately, the US has tax treaties with dozens of countries to prevent double taxation, usually allowing you to take a Foreign Tax Credit for taxes paid to your host country. However, interpreting these treaties requires specialized knowledge. The Internal Revenue Service rules for US citizens abroad are complex and strictly enforced.

You must also contend with severe reporting requirements for foreign assets:

- FBAR (FinCEN Form 114): If the aggregate value of all your foreign bank and financial accounts exceeds $10,000 at any point during the calendar year, you must file a Report of Foreign Bank and Financial Accounts. The penalties for failing to file are notoriously steep, often starting at $10,000 per violation.

- FATCA (Form 8938): If your foreign financial assets exceed certain high thresholds, you must also report them directly to the IRS alongside your annual tax return.

Comparing Your Housing Strategy: Renting vs. Buying Abroad

When retirees discover they can buy a spacious villa in Latin America or a historic stone house in Europe for the price of a small condo in the US, the temptation to purchase real estate immediately is immense. However, buying property in a foreign country carries substantial risks. Real estate laws, title guarantees, and consumer protections vary wildly across the globe.

It is almost universally recommended that expats rent for at least six to twelve months before purchasing a home. Renting allows you to experience the neighborhood in all seasons, understand the local infrastructure, and decide if the culture is truly a good fit before locking up a significant portion of your net worth in an illiquid asset.

| Feature | Renting Abroad | Buying Abroad |

|---|---|---|

| Flexibility | High. You can easily relocate if the neighborhood gets noisy or if you decide the climate isn’t for you. | Low. Selling foreign real estate can take years, and the market may lack the urgency found in the US. |

| Financial Risk | Low. Your maximum risk is limited to your security deposit and lease terms. | High. You face currency exchange risks on the purchase price, unclear title laws, and potentially predatory real estate agents. |

| Maintenance | Minimal. The landlord is generally responsible for structural repairs, plumbing, and major appliances. | Significant. Finding reliable contractors who speak English and navigating local building codes falls entirely on you. |

| Legal Complexity | Moderate. You need to understand local lease laws and tenant rights. | Extreme. Concepts like title insurance and escrow often do not exist. You may need a local real estate attorney to avoid scams. |

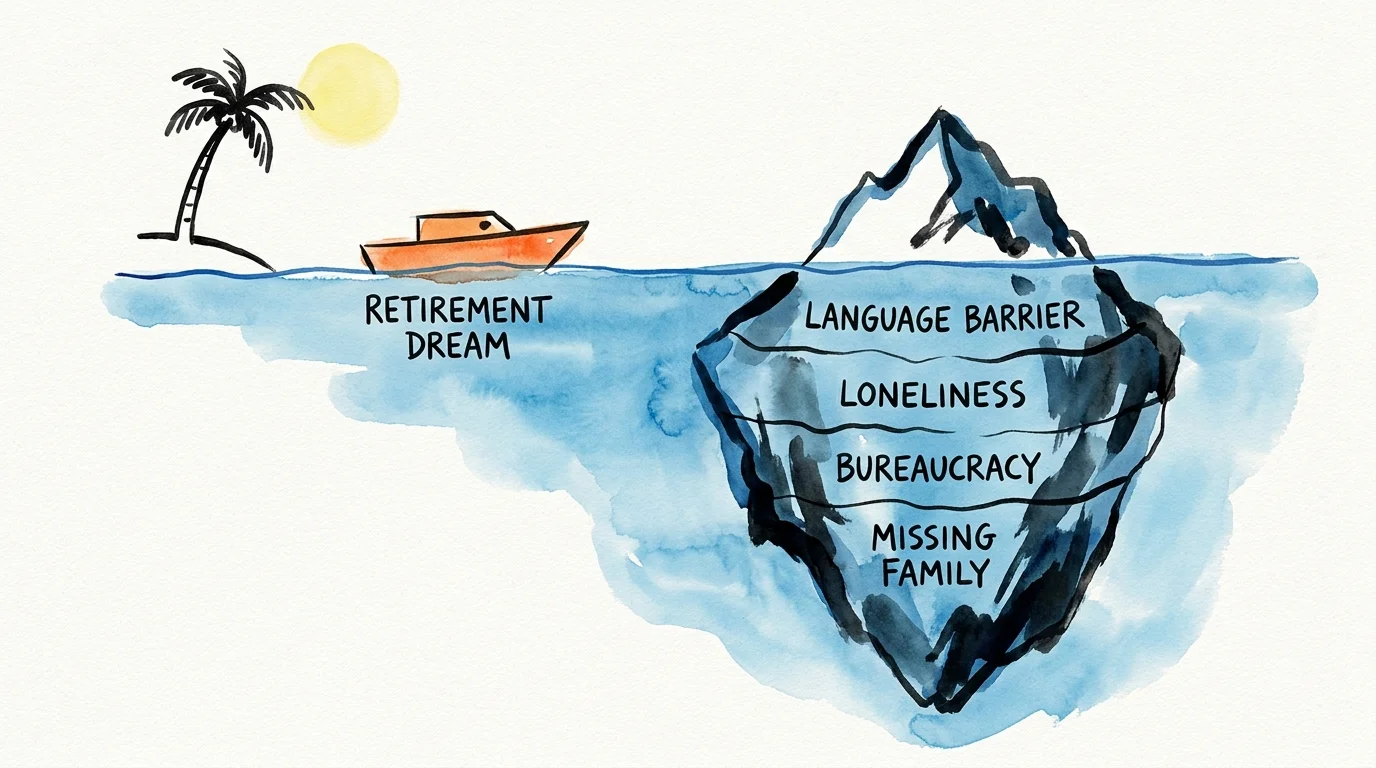

What Can Go Wrong: The Hidden Challenges of Expat Life

Articles highlighting how to retire cheaper abroad often gloss over the profound emotional and logistical challenges of expatriation. Understanding what can go wrong is critical to building a resilient retirement plan.

The most common reason Americans abandon their international retirement and return home is the pull of family. Being a 12-hour flight away when grandchildren are born, or when an aging parent in the US falls ill, creates immense emotional strain. The physical distance is compounded by time zone differences, making even simple phone calls difficult to coordinate.

Language barriers also contribute to an phenomenon known as “expat fatigue.” While navigating a grocery store with broken Spanish or Portuguese is an adventure during the first few months, it can become exhausting after three years. Dealing with complex tasks—such as disputing a utility bill, communicating symptoms to a doctor, or hiring a plumber—requires a level of fluency that takes years to develop. This frustration often isolates retirees, pushing them into “expat bubbles” where they only interact with other Americans, defeating the purpose of experiencing a new culture.

“Risk comes from not knowing what you’re doing.” — Warren Buffett, Chairman and CEO of Berkshire Hathaway

This principle extends beyond investing and perfectly describes the failure rate of overseas retirements. Those who move purely based on a spreadsheet without visiting during the rainy season, without understanding the local bureaucracy, or without a clear plan for long-term care are the most likely to experience a costly return to the United States.

When to Consult a Professional

Transitioning your life overseas is not a DIY project. While you can manage the initial research independently, executing the move requires specialized expertise to protect your assets and legal status. You should actively seek out professional guidance in the following scenarios:

- Tax Season Planning: Before you move, hire a CPA who specializes in expat taxation. They will help you structure your investments to minimize dual taxation, explain your FBAR reporting requirements, and ensure you do not trigger massive penalties from the IRS.

- Immigration and Residency: Do not rely on Facebook groups for legal advice. Hire an immigration attorney licensed in your destination country. They will guide you through the exact paperwork needed for your retirement visa, ensuring your application is flawless and expediting the approval process.

- Estate Planning: Your US will might not be recognized in your new host country, and foreign forced-heirship laws could override your wishes regarding how your property is distributed. You need an international estate planning attorney to draft compliant documents in both jurisdictions.

Frequently Asked Questions

Do I lose my Medicare benefits if I move out of the US permanently?

You do not lose your eligibility for Medicare, but Medicare will not pay for healthcare services received outside the United States. If you choose to stop paying your Part B premiums while living abroad, you will face a permanent 10% penalty for every year you were unenrolled if you ever return to the US and try to reinstate it.

Can I keep my US bank account when I move?

Yes, but it is becoming increasingly difficult. Many US banks require a physical domestic address and will close accounts if they detect you live overseas permanently. To prevent this, many expats maintain an address with a mail-forwarding service or utilize the address of a trusted family member.

Will my Social Security be taxed by my new home country?

It depends entirely on the tax treaty between the US and your destination country. Some countries (like Panama) do not tax foreign-sourced income at all. Others (like Spain) may tax your worldwide income, including your Social Security. You must review the specific tax laws of your chosen destination.

Is it safe to buy real estate in a foreign country?

It can be, provided you use reputable local legal representation. In many countries, the real estate industry is unregulated, meaning anyone can call themselves an agent. Escrow accounts and title insurance are often non-existent. Always hire an independent local attorney to verify property titles before transferring any funds.

Deciding to retire abroad is an incredible undertaking that offers the potential for profound personal growth and financial efficiency. By acknowledging the realities of cross-border taxation, preparing a solid healthcare strategy, and managing the emotional aspects of leaving home, you can build a fulfilling and secure life overseas. Take your time, rent before you buy, and treat the transition not as a final destination, but as the next great chapter of your life.

This article provides general retirement education and information only. Every retiree’s situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: March 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply