The surging cost of urban living combined with a desire for slower-paced lifestyles is driving a massive wave of retirement migration in 2026. If you are preparing to leave the workforce, trading a metropolitan area for a smaller town or mid-sized suburb can stretch your retirement savings while improving your daily quality of life. High property taxes, soaring healthcare costs, and urban congestion push seniors to seek out regions where housing equity goes further. By strategically relocating, you can unlock trapped home value, reduce your annual tax burden, and build a retirement lifestyle centered around space, security, and community rather than the relentless pace of a major city.

The Financial Mathematics of Relocation

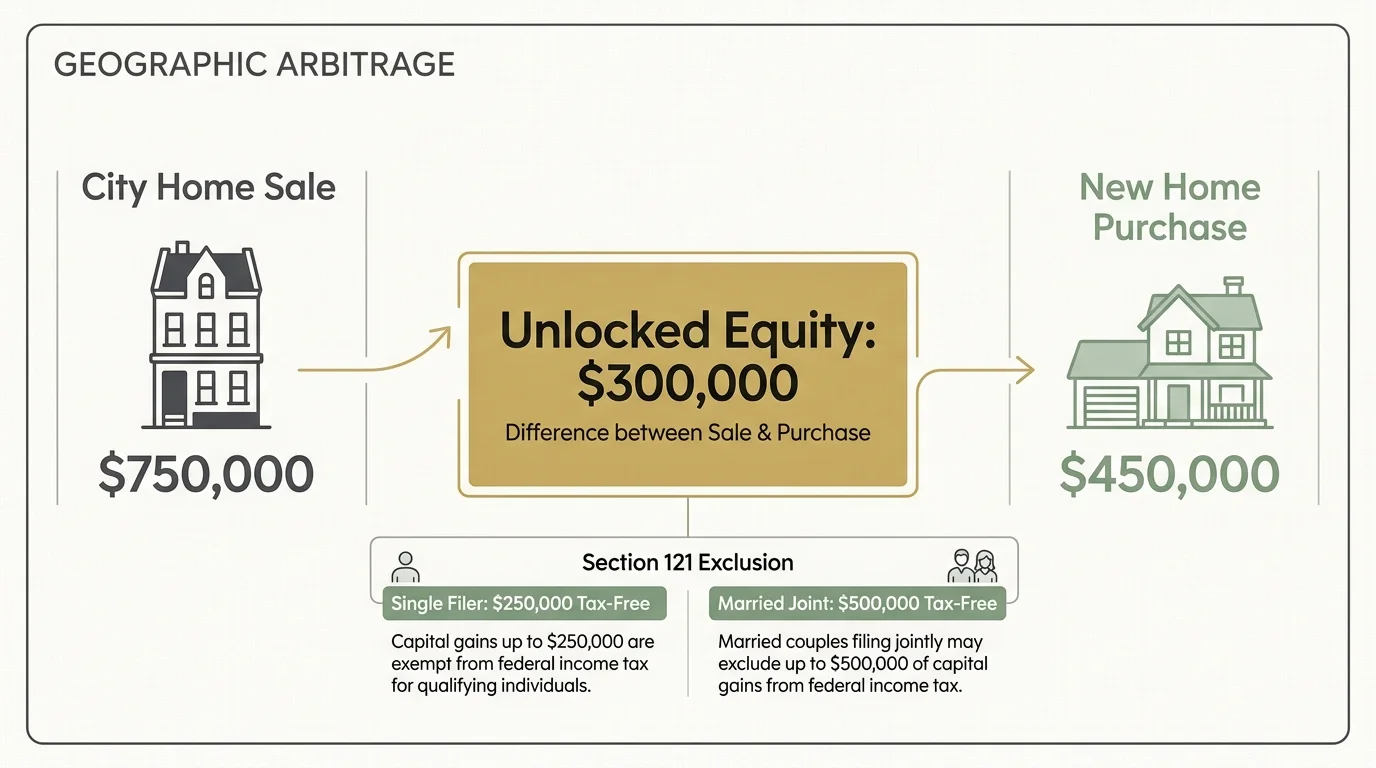

Selling a primary residence in a major metropolitan market often represents the single largest capital event of a retiree’s life. Decades of urban property appreciation mean that you likely sit on substantial home equity. However, keeping that wealth locked inside a highly taxed city home forces you to withdraw more heavily from your investment portfolios just to cover daily living expenses and rising property taxes.

By moving to a secondary market, a mid-sized suburb, or a rural community, you can leverage geographic arbitrage. This strategy involves selling an asset in a high-cost area and purchasing a comparable or better asset in a low-cost area, pocketing the difference to fund your retirement lifestyle. When executed correctly, this move dramatically reduces your structural overhead.

Consider the tax advantages provided by the federal tax code. Under current regulations, you can exclude a significant portion of capital gains from the sale of your primary residence, provided you meet the ownership and use tests. Single filers can typically exclude up to $250,000 of profit, while married couples filing jointly can exclude up to $500,000. Navigating these exclusions allows you to turn a highly appreciated city house into a massive injection of tax-free liquidity. You can review the exact eligibility requirements for the Section 121 exclusion directly through the Internal Revenue Service (IRS).

Beyond the immediate cash infusion, relocating transforms your ongoing monthly expenses. Lower property taxes preserve your cash flow. Reduced sales taxes in many regional municipalities make everyday purchases more affordable. Even auto insurance premiums generally drop when you register a vehicle in a less congested zip code.

Navigating the Changing Tax Landscape

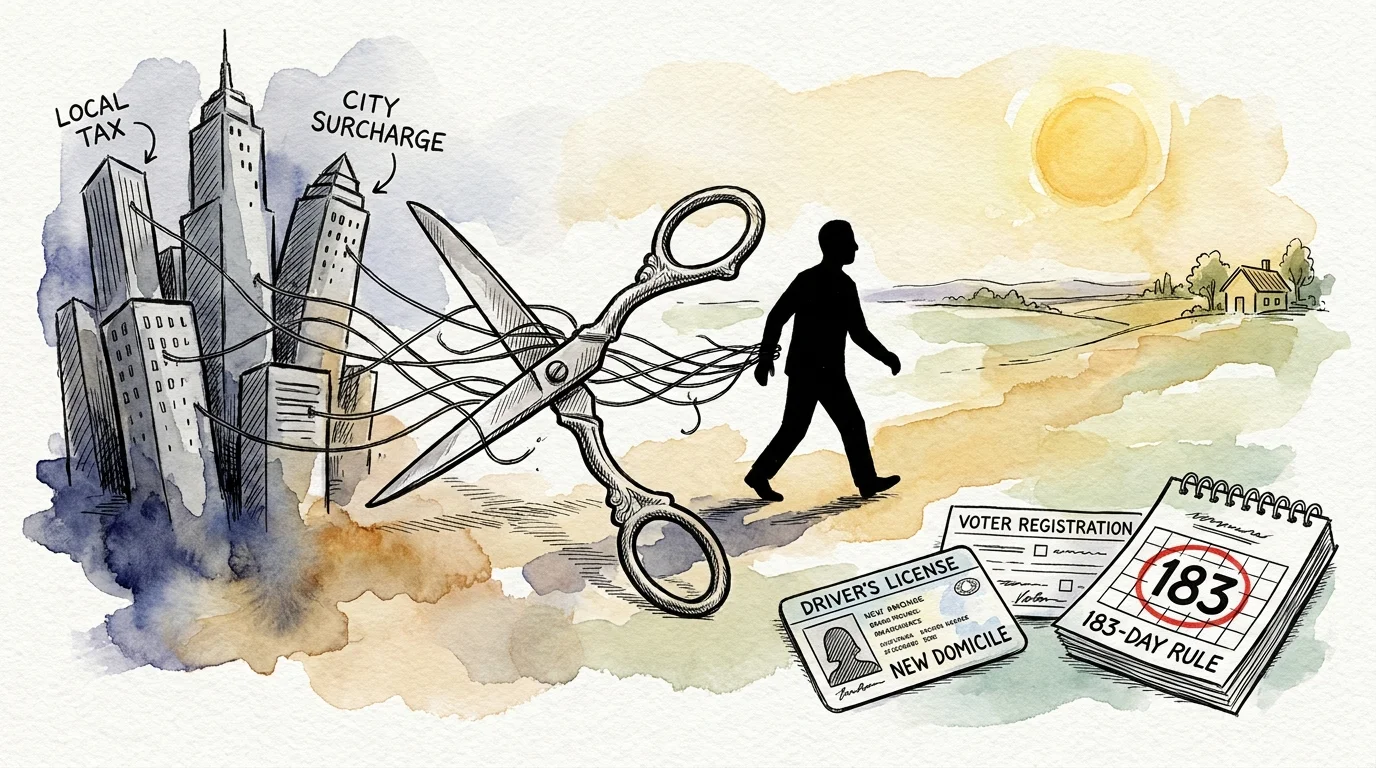

Taxes do not stop in retirement; they simply change shape. Urban centers frequently overlay municipal income taxes on top of high state income taxes. When you live on a fixed income composed of Social Security, pension payouts, and 401(k) withdrawals, giving up a double-digit percentage of your gross income to local governments severely limits your spending power.

Retirees leaving major cities look closely at state tax environments. Several states currently exempt Social Security benefits from state income tax entirely, while others offer generous exemptions for pension income and retirement account withdrawals. Moving across state lines requires careful attention to the concept of “domicile.” Simply buying a house in a low-tax state does not free you from your former high-tax city and state obligations. You must definitively break ties with your former urban residence.

To establish a new domicile and legally benefit from a more favorable tax environment, you generally need to:

- Spend more than 183 days per year in your new location.

- Update your driver’s license, vehicle registration, and voter registration immediately upon moving.

- Shift your primary banking relationships and medical providers to your new hometown.

- File a Declaration of Domicile in your new local county courthouse, if your state provides this option.

“A big part of financial security is living within your means and knowing that your money will last your lifetime.” — Suze Orman, Personal Finance Expert

Medicare and Healthcare Considerations When Relocating

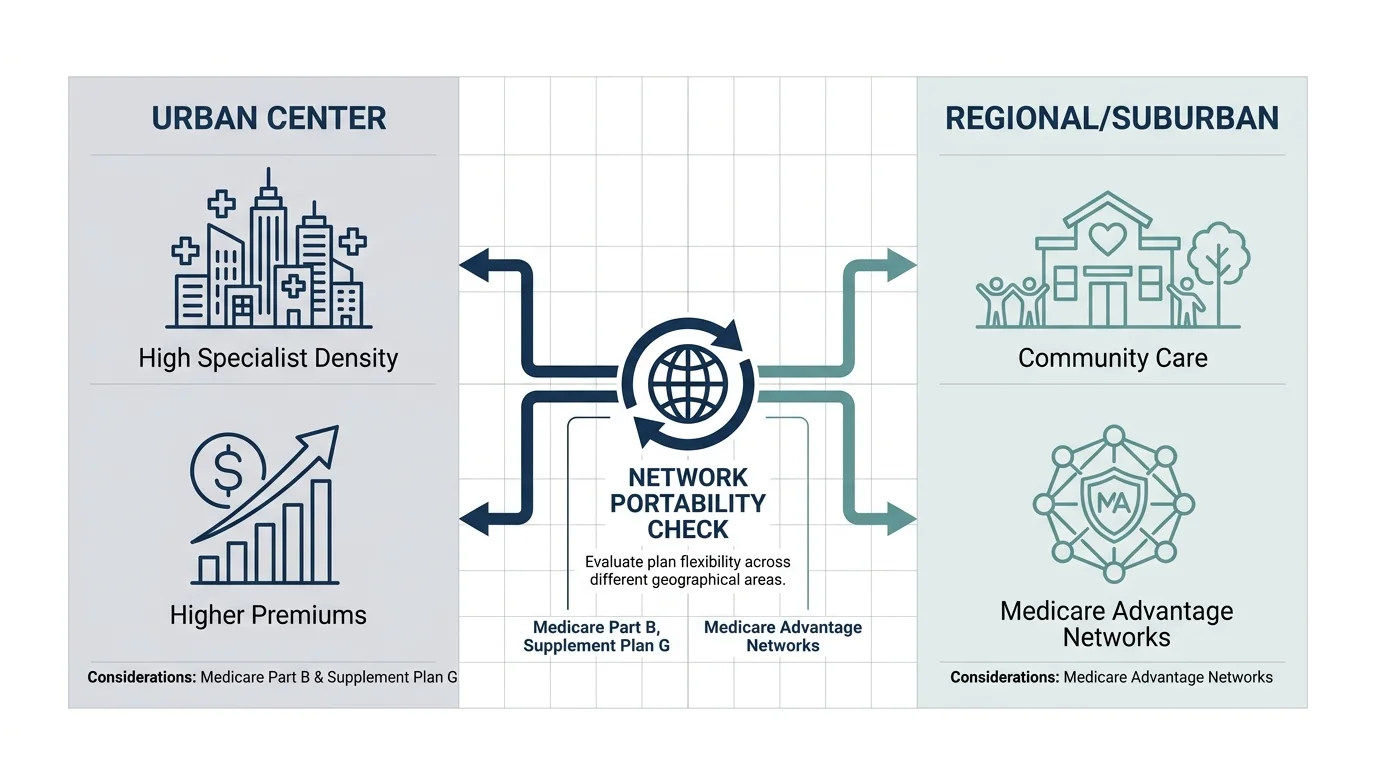

Healthcare access stands as the most critical variable when moving away from a major urban center. Cities boast massive research hospitals, abundant specialists, and highly competitive healthcare networks. Moving to a quieter community requires adjusting your healthcare strategy, particularly regarding how you use your Medicare benefits.

Many retirees misunderstand how relocation impacts their specific Medicare coverage. If you utilize Original Medicare (Part A and Part B) along with a standardized Medicare Supplement (Medigap) policy, your coverage travels with you nationwide. You can see any doctor or visit any hospital in the United States that accepts Medicare. This provides ultimate flexibility for retirees making long-distance moves.

However, if you are enrolled in a Medicare Advantage (Part C) plan or a standalone Part D prescription drug plan, moving out of your city will likely trigger a Special Enrollment Period. Medicare Advantage plans operate on localized networks, usually defined by county lines. A plan that provides excellent coverage in Chicago or Los Angeles will not cover you if you move to a quiet town in the Carolinas or the Mountain West—except in strict medical emergencies.

Before committing to a move, research the healthcare landscape of your destination. Check the hospital ratings, confirm the availability of primary care physicians accepting new Medicare patients, and evaluate local specialist access. You can compare available plans in your prospective new zip code using the official tools provided at Medicare.gov.

The Psychological Shift and Community Connection

Leaving the city is not purely a financial transaction; it represents a profound psychological transition. Urban environments offer constant stimulation, immediate convenience, and a built-in sense of hustle. Suburbs and smaller towns operate on a different frequency. You must intentionally build your social network and find new avenues for engagement.

Many retirees discover that smaller communities offer deeper, more authentic connections. Without the transient nature of big city living, regional towns often foster strong neighborhood associations, active volunteer networks, and highly engaged local councils. To evaluate the social infrastructure of a potential new hometown, look at the investments the community makes in senior centers, public parks, continuing education programs at local community colleges, and regional arts.

Organizations like AARP publish livability indexes that evaluate neighborhoods based on civic engagement, walkability, housing affordability, and clean air. Utilize these data points to ensure your new destination aligns with the vibrant lifestyle you envision for your later years.

Comparing Relocation Environments

Deciding exactly where to move requires weighing competing priorities. This comparison table highlights the practical differences between common retirement destinations.

| Feature | Major Urban Center | Mid-Sized Suburb | Rural Community |

|---|---|---|---|

| Housing Costs | Highest; limited square footage; high property taxes. | Moderate; larger homes; property taxes vary widely by region. | Lowest; extensive acreage; very low property taxes. |

| Healthcare Access | Immediate access to top-tier specialists and research hospitals. | Excellent regional hospitals; most specialists available within 30 minutes. | Limited; primary care local, but specialists may require significant travel. |

| Transportation | Robust public transit; driving optional but parking is expensive. | Car-dependent; predictable traffic patterns; ample free parking. | Entirely car-dependent; requires reliable vehicles for winter weather. |

| Pace of Life | Fast, dense, and highly stimulating. | Balanced, predictable, and community-focused. | Slow, quiet, highly private, and self-reliant. |

| Social Opportunities | Endless events, museums, and dining options. | Strong neighborhood groups, local clubs, and community centers. | Tight-knit but smaller circles; relies heavily on local churches or civic groups. |

What Can Go Wrong

Relocating for retirement requires defensive planning. A poorly researched move can lead to buyer’s remorse and significant financial waste. Pay close attention to the most common pitfalls retirees encounter when leaving the city.

The Vacation Trap: Many people decide to move to a town where they once spent a wonderful two-week summer vacation. Living somewhere year-round is fundamentally different from visiting. The bustling beach town may shut down completely from November to March, leaving you isolated and lacking basic amenities. Always rent in your target destination for at least a month during its worst season before committing to a home purchase.

Underestimating Infrastructure Constraints: City dwellers take certain utilities for granted. High-speed fiber internet, municipal water, city sewer systems, and rapid emergency response times are standard in urban areas. Moving further out may introduce you to the realities of maintaining a private septic system, relying on well water, managing satellite internet latency, and waiting longer for an ambulance to arrive.

The “Halfback” Phenomenon: A known trend in retirement migration involves retirees moving from northern cities to the deep south for tax and weather benefits, only to find the summer heat intolerable or the distance from family too stressful. They eventually move “halfway back” to mid-Atlantic or Midwestern states. Moving twice in retirement destroys wealth through repeated real estate transaction costs. Measure the distance to your grandchildren and honestly assess your tolerance for regional climates before signing a deed.

When to Consult a Professional

Relocating across state lines or liquidating a high-value urban property involves complex legal and financial mechanics. While you can manage much of the research yourself, certain scenarios demand expert guidance. Engage a professional when you encounter the following situations:

- Managing a High-Value Home Sale: If your city property has appreciated so much that your profits exceed the IRS capital gains exclusion limits, consult a Certified Public Accountant (CPA). They can help you identify eligible home improvement deductions that increase your cost basis and lower your tax liability.

- Structuring a Multi-State Move: If you plan to keep your city home as a rental while buying a primary residence elsewhere, you need a fiduciary financial advisor to navigate the dual-state tax implications. You can find vetted fiduciaries through the Certified Financial Planner Board.

- Navigating Chronic Healthcare Needs: If you or your spouse manage a complex chronic illness, engage an independent, licensed Medicare insurance broker. They will verify that your specific medications are covered under the formularies available in your new zip code and ensure your preferred specialists are in-network.

Frequently Asked Questions

Does moving to another state reduce my Social Security benefits?

No. Social Security is a federal program. Your gross monthly benefit amount remains exactly the same regardless of where you live in the United States. However, moving can change your net income, as some states tax Social Security benefits while others do not.

Do I have to change my Medicare plan if I move out of the city?

It depends on your current coverage. If you have Original Medicare (Part A and Part B) with a Medigap policy, you do not need to change plans, as these are accepted nationwide. If you have a Medicare Advantage plan or a standalone Part D prescription drug plan, you will almost certainly need to switch to a new plan that services your new specific county.

How long does it take to establish residency in a new state for tax purposes?

The standard rule requires living in the new state for more than 183 days of the year. However, high-tax cities and states aggressively audit wealthy retirees who claim to have moved. You must demonstrate true “domicile” by severing social, medical, and financial ties with your old city and establishing them firmly in your new town.

Should I buy a house immediately or rent first when leaving the city?

Renting for six to twelve months in your new target location is universally recommended by financial planners. Renting prevents you from locking up your equity in a neighborhood you might ultimately dislike, giving you the flexibility to learn local traffic patterns, weather quirks, and social dynamics before making a permanent commitment.

Preparing for Your Next Chapter

Leaving the familiar rhythm of a major city requires courage, extensive research, and a clear vision of what you want your later years to look like. The financial benefits of cashing out urban home equity and escaping high municipal taxes are undeniable, but the true measure of a successful relocation lies in your day-to-day happiness. Take your time visiting potential new communities, talking to the locals, and testing the infrastructure.

By mapping out your healthcare needs, understanding your tax liabilities, and acknowledging the psychological shifts ahead, you can transition smoothly into a highly rewarding, lower-stress environment. Your retirement is an opportunity to design an entirely new daily routine—one that prioritizes your comfort, security, and financial longevity.

This is educational content based on general retirement and financial principles. Individual results vary based on your situation. Always verify current benefit rules, tax laws, and eligibility requirements with official sources like SSA, Medicare.gov, or the IRS.

Last updated: March 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply