The unretiring trend in the USA is fundamentally shifting how Americans experience their post-career years. While you might have envisioned a life of pure leisure, modern economic realities and personal revelations are prompting thousands to return to the workforce. Whether driven by the pinch of inflation on a fixed income, the strategic desire to delay Social Security for a larger monthly payout, or simply the deep need for daily purpose, retirees returning to work is a mainstream strategy in 2026. If you are considering going back to work after retirement, understanding the specific motivations pushing your peers back into the labor market can help you clarify your own path forward.

1. Outpacing Persistent Inflation and Rising Living Costs

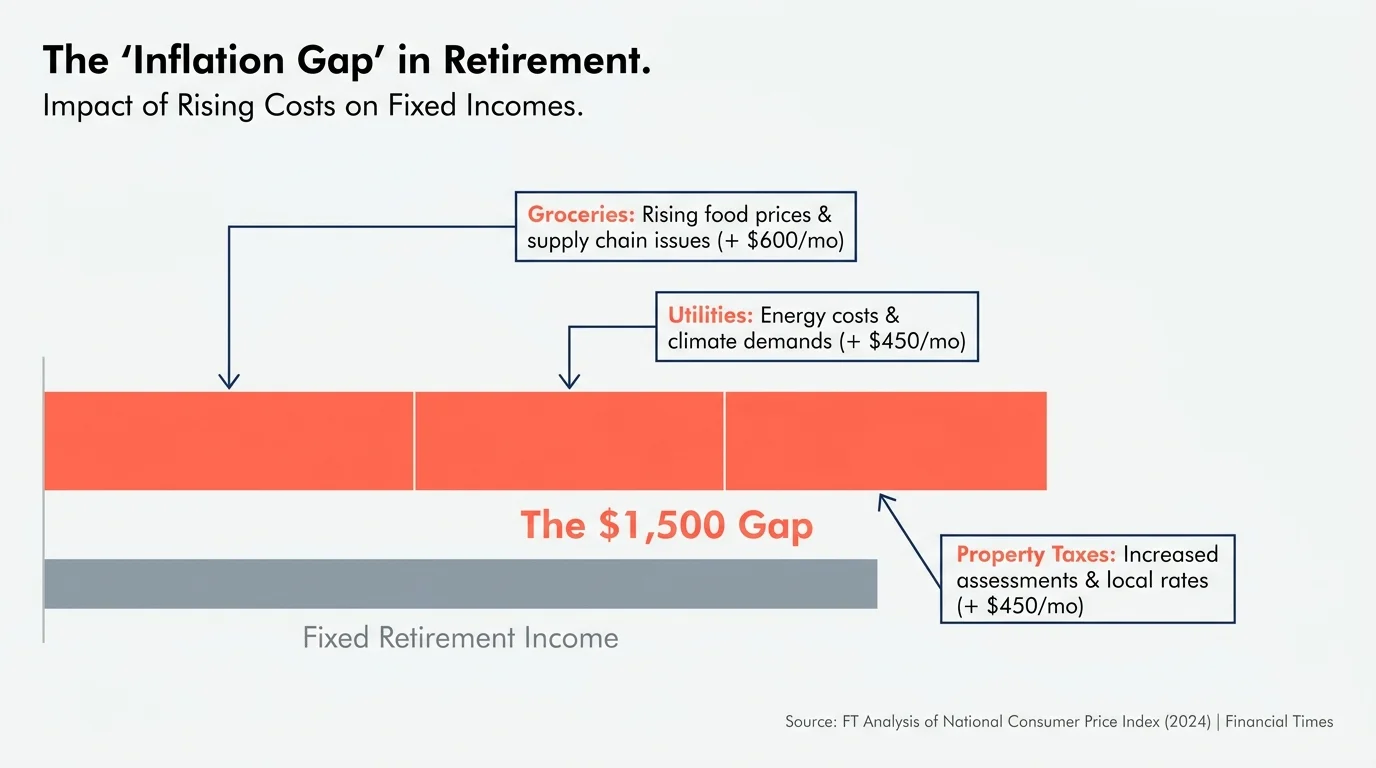

Even as economic conditions stabilize in 2026, the cumulative effect of recent inflationary years has permanently altered the cost of living. Prices for basic necessities—from groceries and utilities to property taxes and auto insurance—have settled at much higher baselines than many anticipated when they first drafted their retirement budgets.

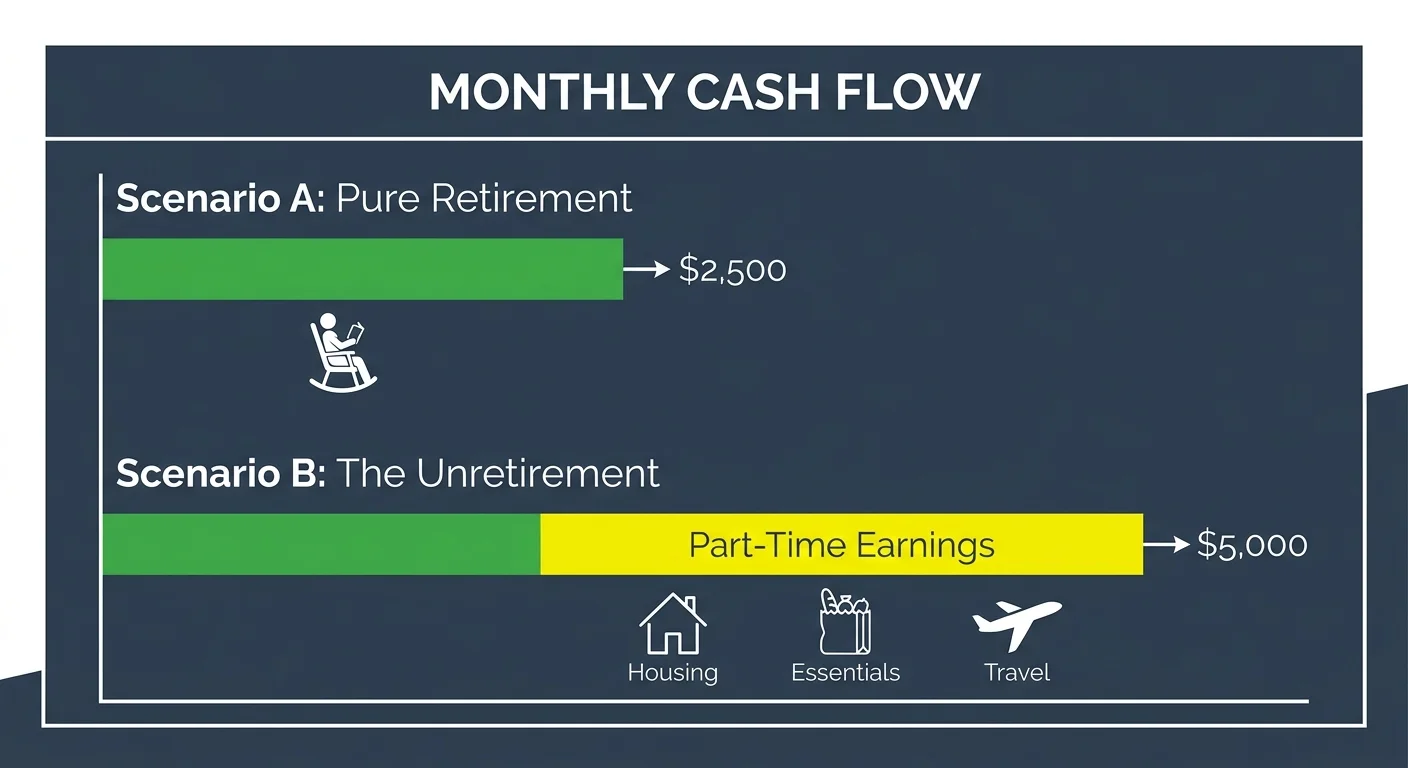

If you retired five or ten years ago, your fixed income sources might not stretch as far as they once did. Pensions rarely offer cost-of-living adjustments, and while Social Security provides annual bumps, those increases frequently lag behind the actual rate of inflation experienced by older adults. Going back to work after retirement offers an immediate cash flow injection that protects your purchasing power. A part-time income of just $1,500 a month can completely offset the rising costs of property taxes and household bills, allowing you to preserve your hard-earned nest egg for the future.

Many return to workforce seniors are not looking for high-stress executive roles. Instead, they seek low-stress, reliable income streams that simply bridge the gap between their fixed income and their actual monthly expenses.

2. Closing the Gaps in Healthcare and Medicare Coverage

Healthcare remains one of the largest and most unpredictable expenses in retirement. Many individuals retire before age 65, only to discover that purchasing private health insurance on the open market is prohibitively expensive. Returning to an employer that offers health benefits is a highly practical solution for bridging the gap until Medicare kicks in.

Even for those already enrolled in Medicare, out-of-pocket costs can be startling. Medicare Part B and Part D premiums, deductibles, copays, and the costs of comprehensive Medicare Advantage or Medigap plans add up quickly. Furthermore, routine dental, vision, and hearing care are largely excluded from Original Medicare. By working a few days a week, retirees can generate dedicated funds to cover these medical expenses without draining their retirement accounts. You can review official coverage details at Medicare.gov to better understand your potential out-of-pocket liabilities.

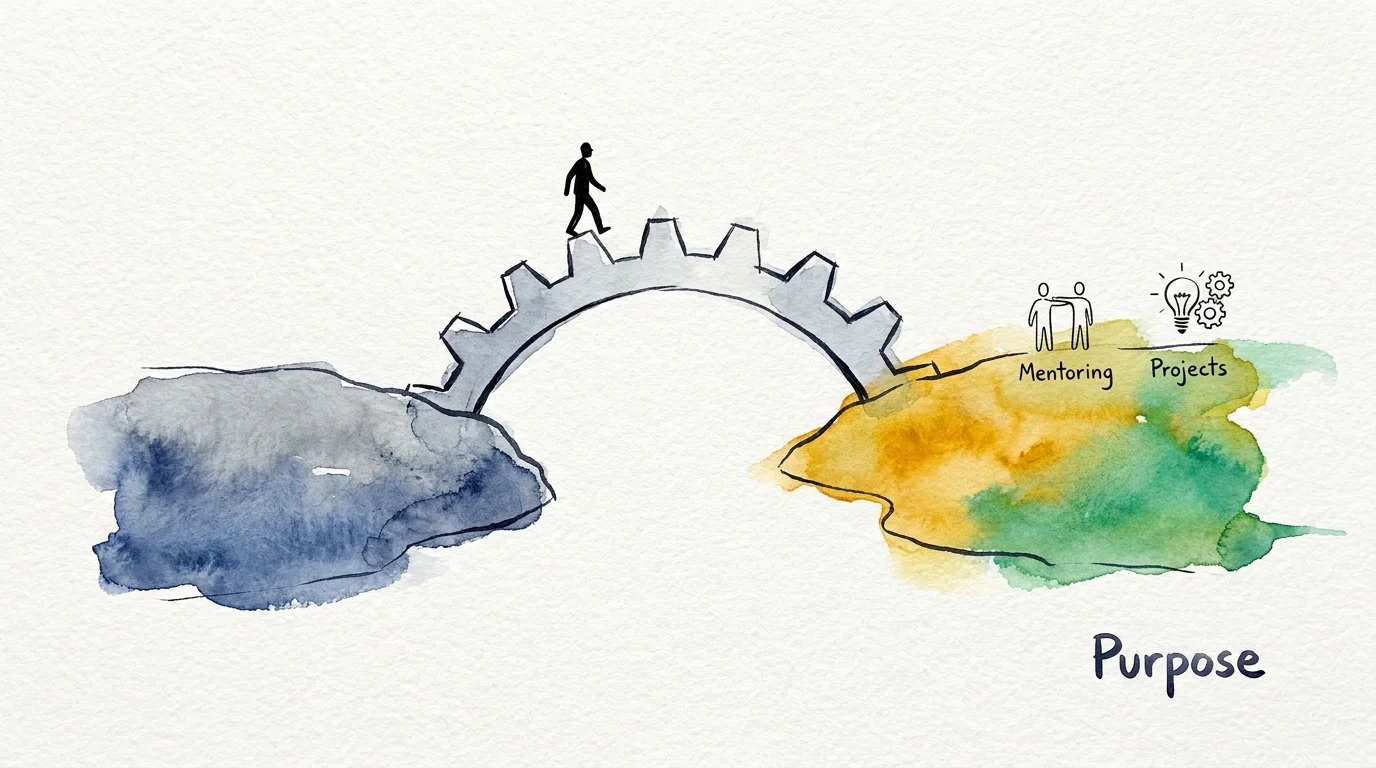

3. Seeking Purpose and Reclaiming Personal Identity

The transition from a high-engagement career to a life of complete leisure can trigger a profound sense of loss. For decades, your professional life dictated your schedule, provided complex problems to solve, and formed a core part of your personal identity. When that sudden stops, the honeymoon phase of retirement can quickly give way to feelings of stagnation.

“Retirement is an artificial finish line. People need to feel useful, and they need to feel engaged. A life of endless leisure is a myth that often leads to depression.” — Mitch Anthony, Retirement Expert

Why retirees work again often has nothing to do with money. They miss the intellectual stimulation, the satisfaction of completing a difficult project, and the structure that a workweek provides. Taking on a consulting role, mentoring younger professionals, or working in a completely different field allows you to reclaim a sense of purpose on your own terms. You get to apply a lifetime of expertise without the pressure of climbing the corporate ladder.

4. The Need for Daily Social Connection

Workplaces are built-in social networks. They force you to interact with diverse groups of people, share ideas, and engage in casual conversation. Without the daily rhythm of an office or worksite, it is remarkably easy for retirees to become isolated.

Returning to work provides a structured environment for socialization. Whether it involves greeting customers at a local retail shop, collaborating with a remote team online, or teaching a class, employment naturally fosters relationships. This social engagement is critical for cognitive health and emotional well-being. The unretiring trend USA is heavily populated by individuals who simply missed being part of a team. They view their part-time jobs as paid socialization—a way to stay sharp, stay connected, and stay active in their local communities.

5. Maximizing Social Security Benefits Through Delay

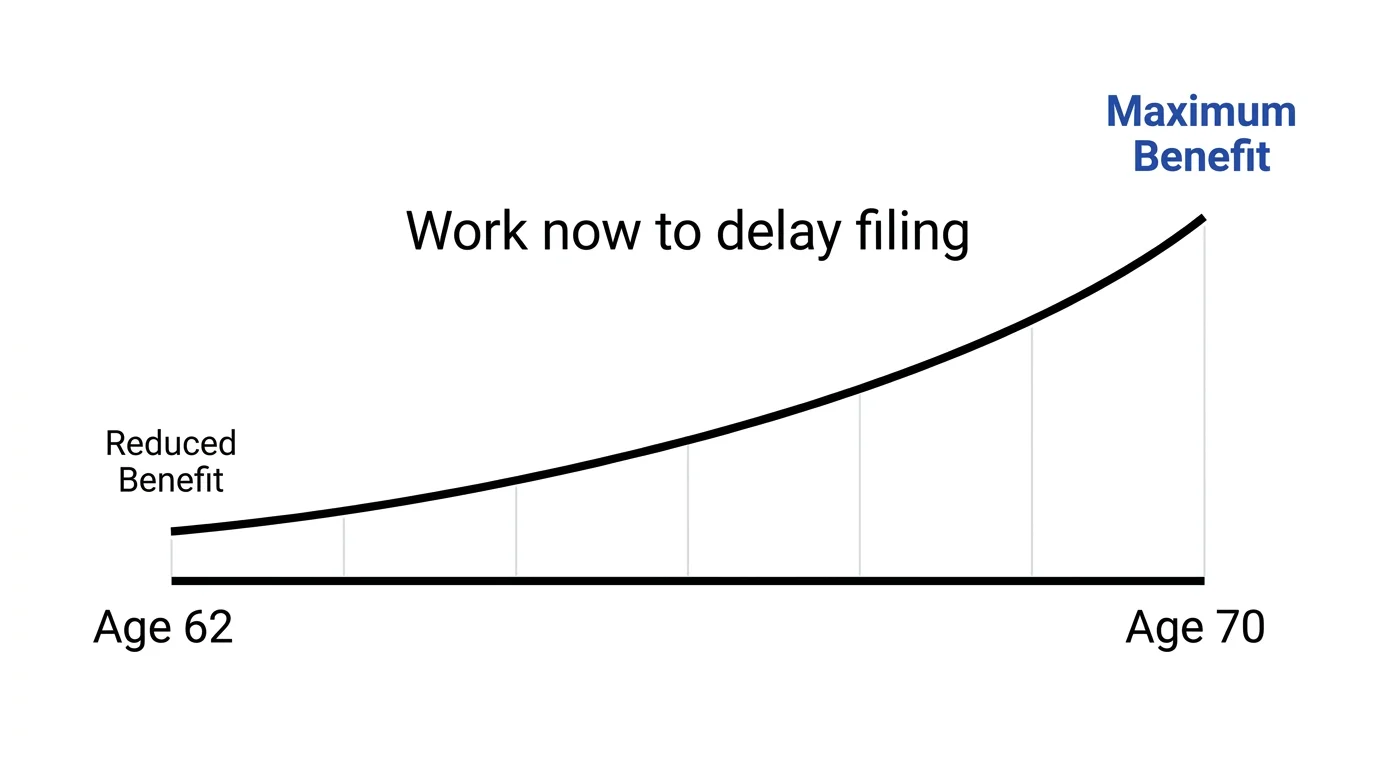

One of the most financially savvy reasons retirees are returning to work is to optimize their Social Security strategy. Your monthly benefit amount is heavily dependent on the age at which you file. Claiming at age 62 results in a permanently reduced payout, while delaying your claim past your Full Retirement Age (FRA) earns you delayed retirement credits. These credits increase your benefit by a guaranteed 8% per year until age 70.

“When it comes to Social Security, taking it at 62 is almost always the biggest financial mistake you can make if you are in good health.” — Suze Orman, Financial Expert

By returning to work, you can generate enough income to cover your living expenses, allowing you to delay your Social Security application. If your Full Retirement Age is 67 and your benefit would be $2,000 a month, waiting until age 70 increases that check to $2,480 a month—an increase that lasts for the rest of your life and benefits a surviving spouse. You can track your estimated benefits and understand the exact rules at the Social Security Administration website.

6. Shielding Portfolios from Market Volatility

Financial planners frequently warn about “sequence of returns risk.” This is the danger of experiencing a stock market downturn early in your retirement. If your portfolio drops by 20% and you are simultaneously withdrawing funds to pay for living expenses, you permanently lock in those losses. Your portfolio then has less capital available to recover when the market eventually bounces back.

Many savvy retirees monitor the economy closely. When the stock market experiences turbulence, they pause their portfolio withdrawals and temporarily re-enter the workforce. The income earned from a job covers their basic needs, giving their investments time to recover. This defensive financial maneuver can extend the life of a retirement portfolio by decades. For a deeper dive into managing market risks in retirement, resources like Investopedia offer extensive guides on safe withdrawal rates.

7. Funding the “Dream” Retirement Lifestyle

Sometimes the motivation to work is purely aspirational. You might have enough saved to cover your mortgage, groceries, and standard bills, but you want to experience a higher tier of luxury without feeling guilty. This is often referred to as “fun money.”

Retirees are taking on seasonal jobs, freelance writing, or local gig work specifically to fund bucket-list experiences. Earning an extra $10,000 a year can pay for a European river cruise, fund a grandchild’s college savings account, or cover the costs of an expensive hobby like restoring classic cars or extensive golf club memberships. Working for luxury rather than necessity completely changes the psychological dynamic of employment. The stress vanishes because you know you can quit at any time.

8. Taking Advantage of Unprecedented Workplace Flexibility

The modern workplace has evolved dramatically, making it easier than ever for older adults to participate on their own terms. Gone are the days when employment strictly meant a mandatory five-day, forty-hour commute. Employers in 2026 are increasingly accommodating, offering remote work, project-based contracts, and highly flexible scheduling.

Companies are also actively recruiting older workers to combat labor shortages and retain institutional knowledge. They value the reliability, emotional intelligence, and problem-solving skills that only come with decades of experience. If you can work from your home office three mornings a week, avoid rush hour traffic, and still earn a substantial side income, the barrier to re-entry is incredibly low. Organizations like AARP frequently feature job boards specifically dedicated to employers seeking the expertise of seasoned professionals.

Comparing the Financial Impact of Unretiring

If you are deciding how to re-enter the workforce, it helps to understand how different work structures impact your finances, taxes, and daily freedom. The table below breaks down the most common paths retirees take when unretiring.

| Work Arrangement | Income Predictability | Tax Implications | Best Suited For |

|---|---|---|---|

| Part-Time W-2 Employee | High; steady paycheck and set hours. | Standard payroll taxes deducted; employer pays half of FICA. | Those seeking routine, social interaction, and completely stress-free tax filing. |

| Freelance / 1099 Contractor | Variable; depends on client volume. | You must pay self-employment tax (15.3%) and manage quarterly estimated taxes. | Professionals who want total control over their schedule and the ability to work remotely. |

| Working to Delay Social Security | High; income replaces need for early filing. | Reduces immediate tax burden on retirement accounts; eventually higher taxes on larger Social Security checks later. | Healthy individuals looking to maximize their lifetime guaranteed income payout. |

| Seasonal / Gig Economy | Low to Medium; highly flexible. | Requires diligent tracking of mileage, expenses, and independent contractor taxes. | Those who only want to work during certain months to fund specific travel or hobbies. |

Common Mistakes to Avoid When Going Back to Work

While the benefits of unretiring are substantial, generating new income can trigger unexpected financial penalties if you do not plan carefully. Keep a close eye on these common pitfalls:

- Triggering the Social Security Earnings Test: If you claim Social Security before your Full Retirement Age and continue to work, the SSA will withhold $1 in benefits for every $2 you earn above a certain annual limit ($23,400 in 2024, adjusted annually for inflation). This withheld money is not lost forever—it is credited back to your benefit once you reach FRA—but it can cause a severe short-term cash flow crunch.

- Getting Hit with IRMAA Surcharges: Medicare Part B and Part D premiums are tied to your Modified Adjusted Gross Income (MAGI) from two years prior. If your new job pushes your income over the threshold, you will face the Income-Related Monthly Adjustment Amount (IRMAA), significantly increasing your healthcare costs.

- Miscalculating Tax Brackets: Earning a salary on top of your pension, Social Security, and Required Minimum Distributions (RMDs) can easily bump you into a higher marginal tax bracket. You might also trigger the taxation of your Social Security benefits if your combined income exceeds the IRS limits.

- Ignoring Pension Rules: If you return to work for the exact same employer who pays your pension, you might inadvertently violate the terms of your retirement plan, potentially suspending your pension payouts. Always verify the rules with your plan administrator.

Professional vs. Self-Guided: Managing Your Unretirement Income

Deciding whether to navigate your return to the workforce alone or hire an expert largely depends on the complexity of your financial situation.

When Self-Guided Makes Sense: If you are over your Full Retirement Age, have relatively simple tax returns, and are taking a low-paying part-time job just for extra spending money, you likely do not need professional intervention. The tax implications are straightforward, and there is no Social Security earnings limit to worry about once you reach FRA.

When to Hire a Professional: You should consult a Certified Public Accountant (CPA) or a Certified Financial Planner (CFP) if you are under your Full Retirement Age, managing substantial Required Minimum Distributions, or starting a lucrative consulting business. A professional can help you structure your business as an S-Corporation or LLC, implement strategies to avoid IRMAA surcharges, and optimize exactly which retirement accounts you should draw from while earning a salary.

Frequently Asked Questions About Returning to the Workforce

Will going back to work permanently reduce my Social Security benefits?

No. If you are subject to the earnings test because you are working before your Full Retirement Age, your current checks may be reduced or withheld entirely. However, once you reach FRA, the Social Security Administration recalculates your benefit upward to account for the months your checks were withheld. Your overall lifetime benefit is not penalized; it is simply deferred.

Do I have to keep paying for Medicare if my new employer offers health insurance?

It depends on the size of the employer. If your new company has 20 or more employees, their group health plan generally becomes your primary coverage, and you may be able to drop Medicare Part B to save on premiums without facing late enrollment penalties later. If the company has fewer than 20 employees, Medicare remains your primary coverage, and you must keep Part B active. Always confirm coordination of benefits with your HR department and Medicare.

Can I still contribute to a retirement account if I am unretiring?

Yes. As long as you have earned income from a job or self-employment, you can contribute to an IRA or Roth IRA, regardless of your age. If your new employer offers a 401(k) with a match, participating in it is a highly effective way to shield your new income from immediate taxes while securing free money from the employer match.

How does part-time work affect my Required Minimum Distributions (RMDs)?

Working does not exempt you from taking RMDs from your traditional IRAs once you reach the qualifying age (currently 73). However, if you roll your previous 401(k) funds into your new employer’s active 401(k) plan—and you do not own more than 5% of the company—you can delay taking RMDs from that specific 401(k) until you finally retire from that job.

Stepping Back into the Workforce on Your Terms

Choosing to unretire is a highly personal decision that blends financial pragmatism with emotional well-being. Whether you are returning to outpace inflation, delay your Social Security claims, or simply reclaim a sense of daily purpose, the modern workforce offers unprecedented flexibility for older adults. Take the time to evaluate your motivations, calculate the tax implications, and find an arrangement that enhances your life rather than complicating it.

This article provides general retirement education and information only. Every retiree’s situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: May 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply