Packing up your lifelong home to spend your golden years playing with grandchildren and attending weekly family dinners sounds like the ultimate retirement dream. Yet, an increasing number of retirees discover that relocating to be near adult children creates unexpected financial, emotional, and logistical hurdles. Moving across the state or country requires abandoning established social networks, navigating new healthcare systems, and often taking on exhausting childcare responsibilities that derail your personal retirement goals. Before you list your house and hire movers, you must evaluate the hidden costs of family relocation. Examining these eight common regrets will help you protect your nest egg, preserve your family relationships, and build a retirement lifestyle that actually serves your long-term needs.

1. The Built-In Babysitter Assumption

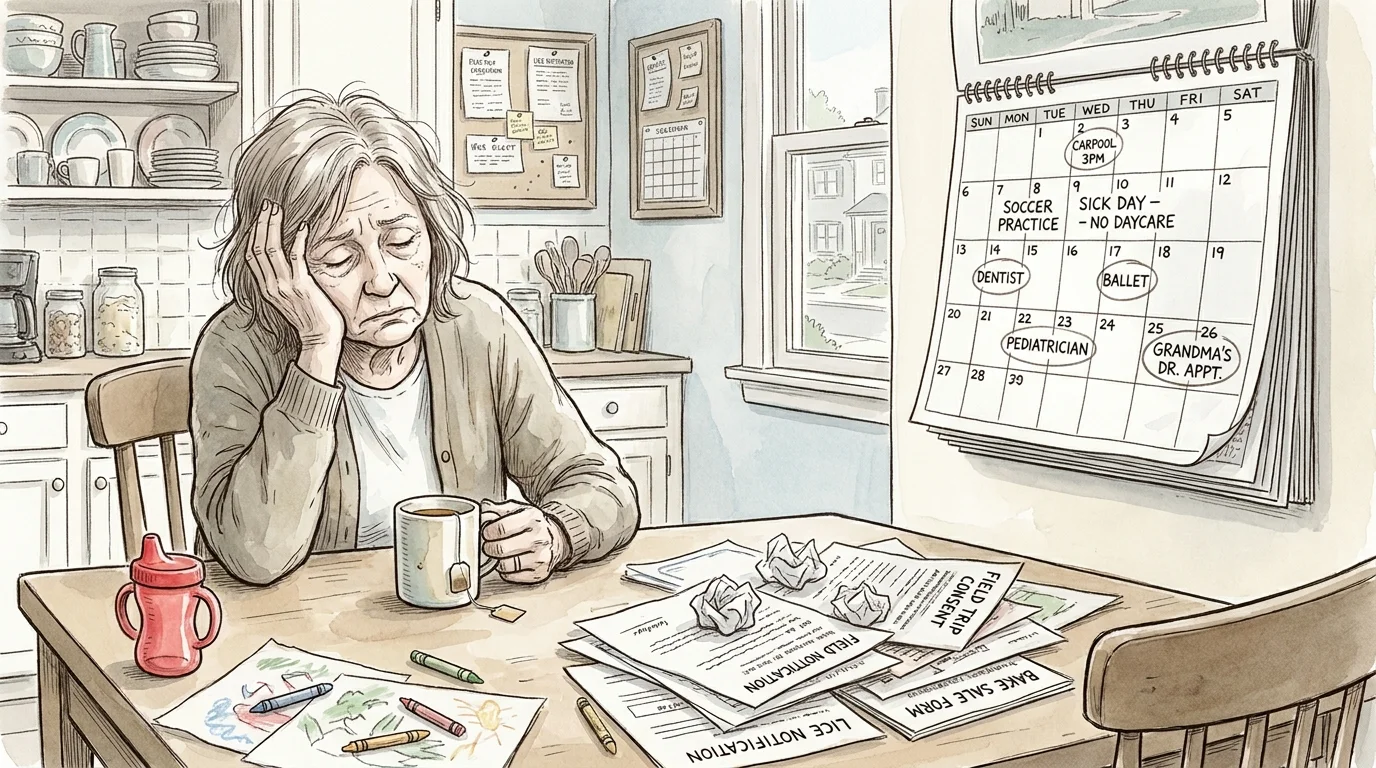

When you move to the same neighborhood as your adult children, unspoken expectations regarding childcare often surface immediately. Grandparents naturally want to spend quality time with their grandchildren; however, there is a massive difference between taking the kids for a fun Saturday afternoon and becoming a full-time, unpaid nanny Monday through Friday.

Adult children juggling demanding careers and high daycare costs may look at your open retirement schedule and assume you are eager to step in. Unfortunately, chasing toddlers or managing after-school carpools requires significant physical and mental energy. Many retirees find themselves exhausted, waking up to an alarm clock just as they did during their working years. Instead of enjoying leisurely mornings, traveling, or pursuing new hobbies, your calendar becomes entirely dictated by your grandchildren’s school schedules and sick days.

To prevent this regret, you must have candid conversations before signing a lease or mortgage. Set clear parameters around your availability. Explain that while you are thrilled to be the emergency backup or host Friday movie nights, you are not replacing traditional daycare. Protecting your time preserves your energy and keeps your relationship with your grandchildren joyful rather than resentful.

2. Sudden Shifts in Family Geography

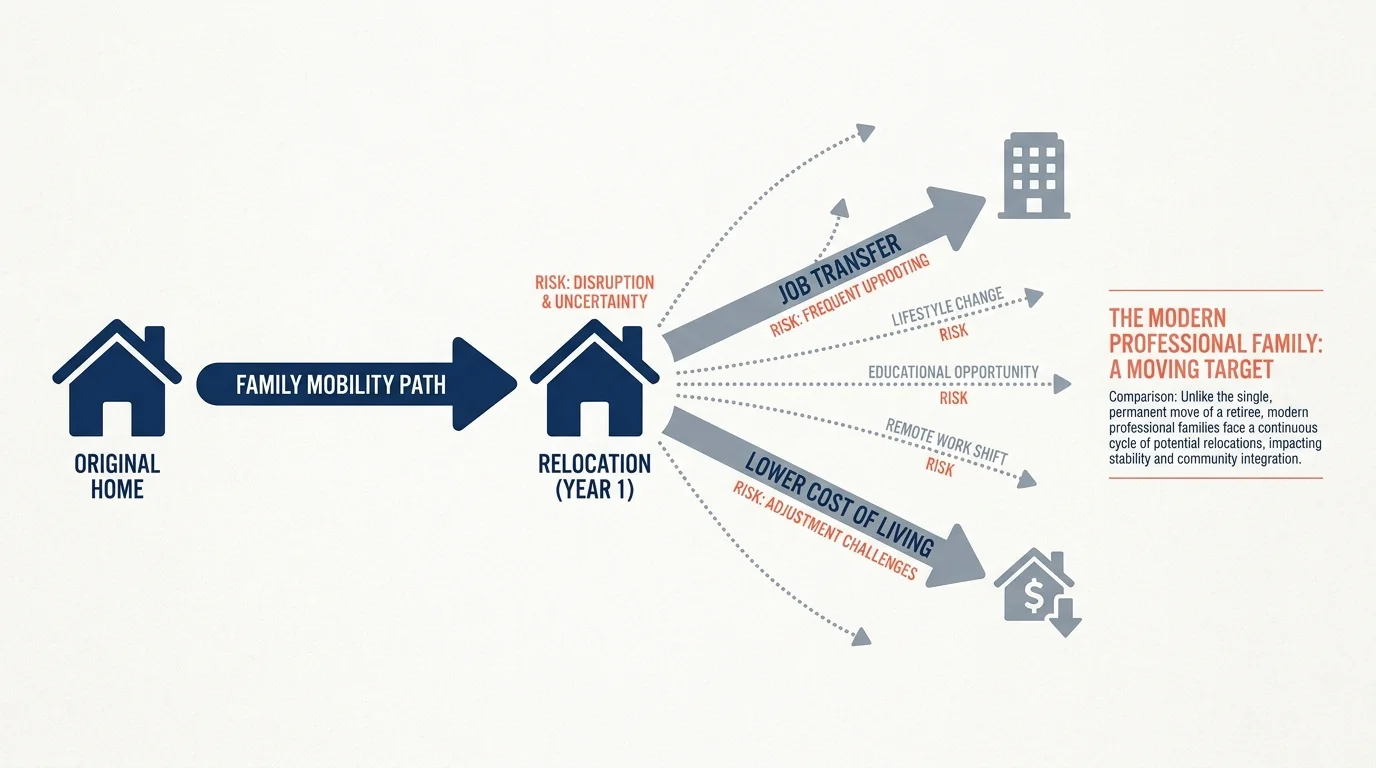

You sell your home, pack your belongings, and purchase a beautiful condo ten minutes from your son’s house. Two years later, his company transfers him across the country, or he decides to move for a better cost of living. Suddenly, you are stranded in a city you only chose because of family, stripped of your support system, and faced with the daunting prospect of moving all over again.

The modern workforce is highly mobile. Unlike previous generations who often stayed with a single employer for decades in one town, today’s professionals frequently relocate to advance their careers. Relying on your children’s current geographic location as the sole foundation for your retirement destination is incredibly risky.

If you choose to relocate, evaluate the destination on its own merits. Ask yourself whether you would genuinely enjoy living in that city if your children were to move away. Look at the local climate, recreational opportunities, cultural amenities, and overall vibe. If the only appealing factor is the proximity to your family, you may want to reconsider the permanence of your move.

3. The Financial Toll of Relocation

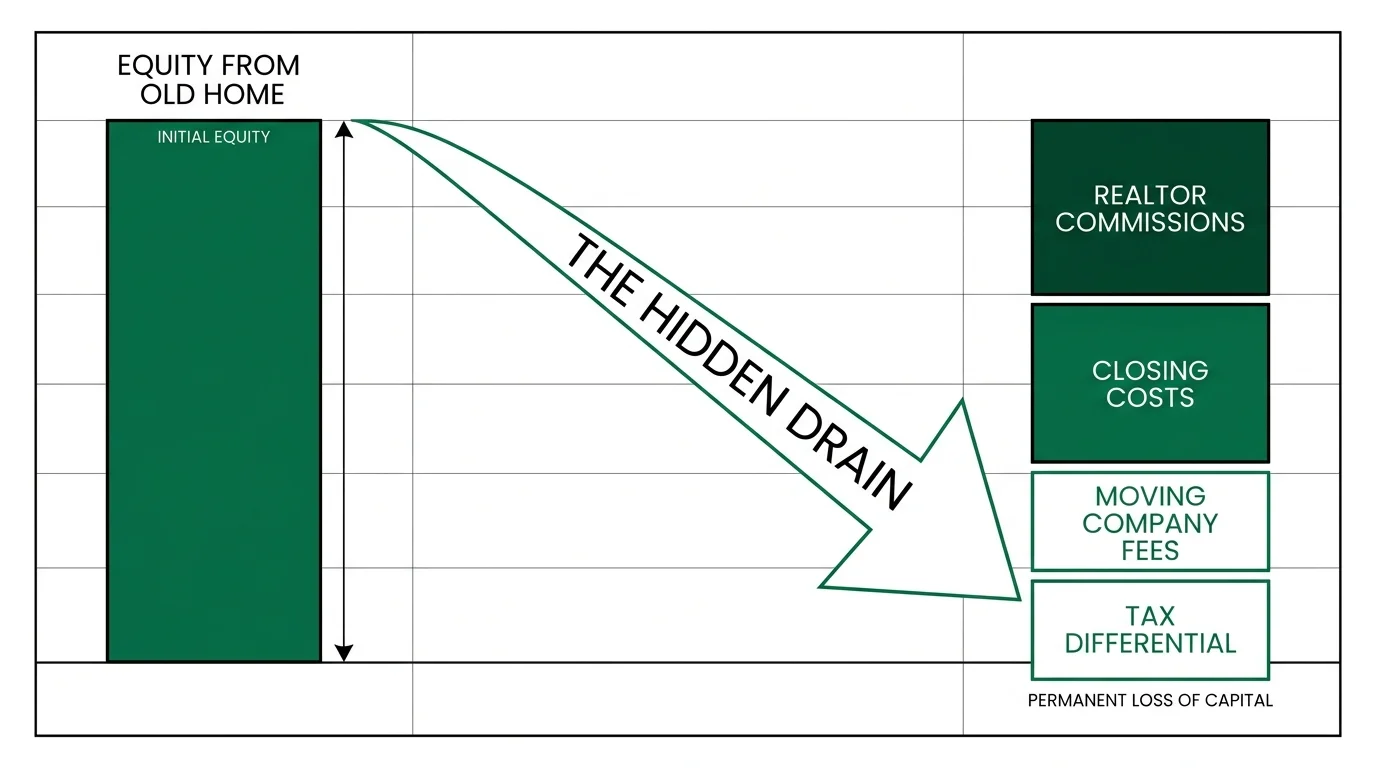

Moving is expensive; relocating to a new state in retirement can permanently alter your financial trajectory. Many retirees leave affordable, mortgage-free homes in low-cost areas to be near children who have settled in expensive metropolitan hubs or high-tax states. The financial shock can drain retirement accounts much faster than anticipated.

Real estate transaction costs alone—realtor commissions, closing costs, and moving company fees—can easily strip tens of thousands of dollars from your nest egg. Furthermore, transitioning from a state with no income tax to one that taxes pensions and retirement withdrawals drastically reduces your monthly cash flow. You also have to factor in property taxes, which might be double or triple what you paid in your previous hometown.

Before making a move, review state tax profiles through resources like Kiplinger to understand how your pension, Social Security, and property taxes will change. Run a comprehensive budget comparing your current living expenses with the projected costs in the new location. Relocating for family should never compromise your financial security or force you to outlive your savings.

4. Leaving Behind Your Established Social Network

Retirees often underestimate the deep psychological value of their current community. Over decades, you have built a complex network of friends, neighbors, club members, and local acquaintances. You know the best mechanic, you have a favorite table at the local diner, and you have friends who check in on you. Leaving that behind to be near family often results in profound isolation.

Adult children are usually entrenched in the busiest seasons of their lives—building careers, raising kids, and maintaining their own social circles. They cannot be your entire social life. When you move to their town, you may find yourself sitting in an empty house waiting for them to have a free hour to visit. The National Council on Aging (NCOA) notes that maintaining strong community connections is vital for cognitive health and preventing depression in older adults.

Rebuilding a social life from scratch in your sixties or seventies requires tremendous effort. If you do relocate, treat making friends as a part-time job. Join local volunteer organizations, religious groups, or golf leagues immediately upon arrival to ensure you have a support system outside of your immediate family.

5. Disruption of Trusted Healthcare Providers

As you age, the quality and accessibility of your medical care become paramount. Moving away from your long-term primary care physician and trusted specialists means starting over in a new healthcare system. This transition is not just inconvenient; it can be dangerous if you have complex, chronic health conditions that require coordinated care.

Navigating health insurance in a new state adds another layer of complexity. If you are enrolled in a Medicare Advantage plan, your coverage is likely tied to a specific regional network of doctors and hospitals. Moving across state lines—or even to a different county—often forces you to change plans entirely. You may discover that the top-rated specialists in your new city do not accept your new coverage, or that wait times for new patients stretch into months.

Take proactive steps to protect your health before moving. Use tools available on Medicare.gov to ensure your preferred hospitals and required specialists accept your coverage in the new zip code. Request comprehensive copies of your medical records and have your current doctors recommend peers in your future city.

6. Blurred Boundaries and Privacy Invasions

Proximity breeds familiarity, and familiarity can quickly erode boundaries. When you live hundreds of miles away, visits are planned, structured, and mutually agreed upon. When you live three streets over, the “drop-in” culture takes over. While spontaneous visits sound charming, they can quickly feel invasive when you never know when your adult children will walk through the front door.

Retirees frequently report feeling guilty for wanting privacy. You might want to spend a quiet Tuesday reading a book in your pajamas, only to have family members show up expecting to be entertained. Conversely, you might find yourself overly involved in your children’s household dynamics, offering unsolicited advice on parenting or home maintenance simply because you are always around to observe it.

“Retirement is not a time to retreat from life, but to engage in it on your own terms. True purpose comes from balancing your family legacy with your personal autonomy.” — Mitch Anthony, Retirement Expert

Establish clear boundaries early. Decide how you will handle keys to each other’s homes, and agree on a baseline rule of calling or texting before dropping by. Healthy boundaries do not diminish love; they protect the relationship from friction and resentment.

7. Conflicting Lifestyle Priorities

Your vision of retirement likely includes flexibility. Perhaps you want to take impromptu road trips, spend winters in a warmer climate, or dedicate your weekends to exploring local wineries and hiking trails. However, living near family often anchors you to their rigid schedules.

Retirees often feel tremendous guilt when their desired lifestyle conflicts with family events. If your grandson has a minor league baseball game every Saturday morning, you might feel obligated to attend, quietly sacrificing your own weekend plans. Over time, these small sacrifices compound. You may realize you are not living the retirement you saved forty years to enjoy; instead, you are living a supporting role in your children’s lives.

You must grant yourself permission to prioritize your own dreams. Communicate your travel plans and schedule well in advance. Remind your family—and yourself—that missing a few soccer games to take a cruise or visit friends does not make you a bad grandparent. A fulfilling retirement requires you to remain the protagonist of your own life.

8. Real Estate Compromises and Downsizing Disappointments

The urgency to find a house near family often leads to poor real estate decisions. In a competitive housing market, you might settle for a home that does not meet your aging-in-place needs simply because it is located in the right school district for your grandchildren.

Retirees frequently regret buying two-story homes with steep stairs, properties with high-maintenance yards, or houses in suburban sprawl that require a car to get anywhere. Others buy homes that are too large, maintaining extra bedrooms solely to host extended family for the holidays. Heating, cooling, and cleaning a four-bedroom house when you only use two rooms drains both your finances and your stamina.

Prioritize your physical needs and mobility when house hunting. Look for universal design features: single-story layouts, zero-step entrances, walk-in showers, and proximity to grocery stores and medical centers. Do not compromise your daily comfort and safety for the sake of occasional family gatherings.

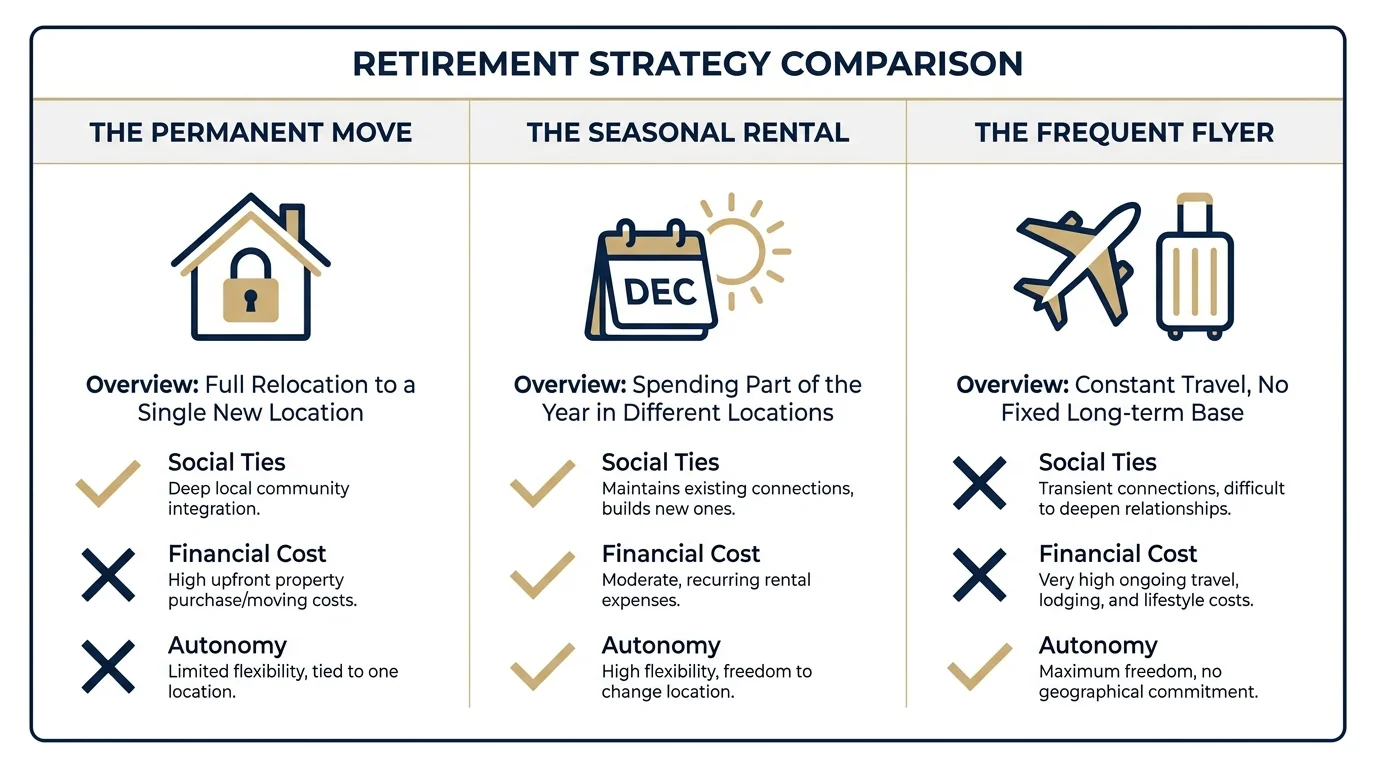

Comparing Relocation Strategies

Moving right next door is not the only way to maintain a close relationship with your family. Before committing to a permanent, localized move, consider how different strategies impact your finances, social life, and family dynamics.

| Strategy | Financial Impact | Social Impact | Family Dynamics |

|---|---|---|---|

| Moving to the Same Neighborhood | High variability; depends heavily on local real estate and state taxes. High moving costs. | High disruption. Requires completely rebuilding local friendships and community ties. | Maximum daily interaction, but highest risk of boundary issues and unpaid childcare assumptions. |

| The “Halfway” Regional Move | Moderate. Allows you to choose a tax-friendly or cheaper state within a 3-4 hour drive. | Moderate disruption. You still start over, but have more control over selecting a retiree-friendly town. | Excellent balance. Close enough for weekend visits and emergencies, far enough to prevent daily drop-ins. |

| Staying Put & Traveling Frequently | Predictable. Funds otherwise used for real estate fees are redirected to travel budgets and short-term rentals. | Zero disruption. You keep your doctors, friends, and established community roots. | High quality time. Visits are planned, intentional, and focused entirely on connection rather than chores. |

What Can Go Wrong: The Unspoken Expectations

The most devastating retirement regrets stem from assumptions rather than malice. When retirees and adult children fail to communicate their expectations prior to a cross-country move, relationships fracture quickly. To prevent catastrophic misunderstandings, you must treat the relocation almost like a business merger, discussing the uncomfortable details upfront.

Before you hire a real estate agent, sit down with your adult children and discuss the following practicalities:

- Childcare specifics: How many days a week, if any, are you expected to watch the grandchildren? What happens during summer breaks?

- Financial boundaries: Will you be expected to contribute to family dinners, vacations, or home repairs now that you are local?

- Social expectations: How often will you share meals? Are Sundays automatically assumed to be “family day”?

- Caregiving for you: If your health declines in the next decade, do your children have the capacity and willingness to assist you, or will you need to hire private help?

Clearing the air on these topics ensures everyone is operating with the same blueprint. If the answers make you uncomfortable, it is far better to discover that before you sell your current home.

Frequently Asked Questions

How long should I wait into retirement before deciding to move near family?

Financial planners generally recommend waiting one to two years after retiring before making a major geographic move. This cooling-off period allows you to adjust to your new financial reality, discover what you actually enjoy doing with your free time, and separate the initial excitement of retirement from long-term lifestyle needs. Rushing into a move the month you retire often leads to expensive reversals.

Does Medicare cover me if I move to another state?

Original Medicare (Parts A and B) is a federal program and covers you anywhere in the United States. However, if you have a Medicare Advantage plan (Part C) or a standalone Part D prescription drug plan, these are highly localized. Moving to a new state or county usually triggers a Special Enrollment Period, requiring you to select new coverage in your new area.

What is the “snowbird” strategy for family relocation?

The snowbird strategy involves maintaining your primary residence while renting an apartment or home near your family for a few months out of the year. This approach lets you enjoy extended, quality visits without committing to a permanent move, changing your tax domicile, or giving up your established social network. It is an excellent test run before making a permanent real estate decision.

Safeguard Your Golden Years

Relocating to be near family is a monumental decision that impacts every facet of your retirement—from your daily schedule and social life to your financial stability and healthcare access. While the desire to be an active part of your children’s and grandchildren’s lives is natural, you must balance that desire with your own need for independence, financial security, and personal fulfillment. Take your time, communicate openly, and explore alternative visitation strategies before putting a “For Sale” sign in your front yard.

This is educational content based on general retirement and financial principles. Individual results vary based on your situation. Always verify current benefit rules, tax laws, and eligibility requirements with official sources like SSA, Medicare.gov, or the IRS.

Last updated: May 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply