Retirement no longer means a hard stop at age 65, followed by decades of unstructured leisure time. As we navigate through 2026, modern retirees are actively redesigning their later years to balance extended longevity, shifting economic realities, and a deep desire for ongoing purpose. Economic pressures and medical advancements have transformed how you will fund your lifestyle, manage your healthcare, and choose your living arrangements. Rather than settling into a predictable routine, today’s older adults are embracing phased work schedules, integrating smart home technology, and rethinking traditional housing to stay independent longer. By understanding these eight accelerating trends, you can make proactive adjustments to your own retirement strategy, protect your nest egg, and build a more fulfilling, secure daily life.

1. The Rise of Phased Retirement and “Silver” Entrepreneurship

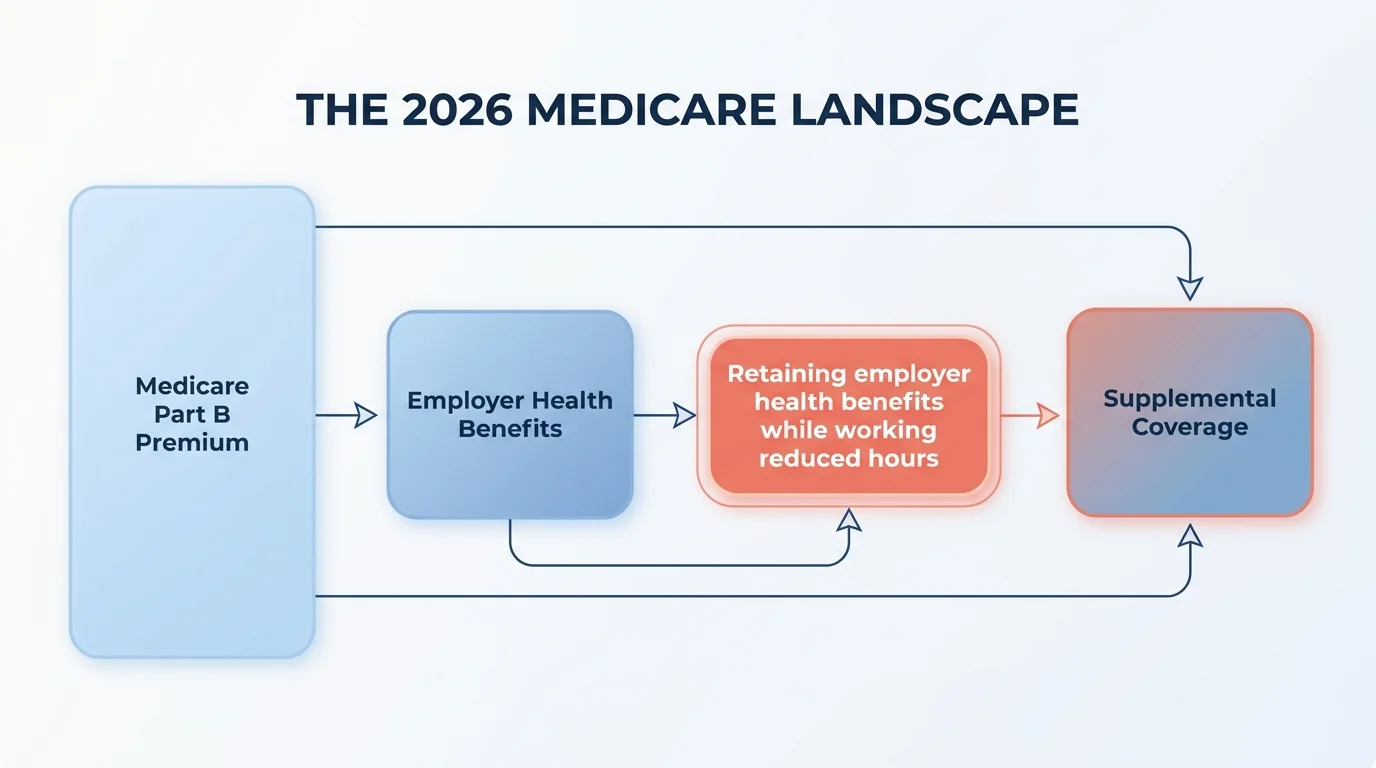

The traditional model of working exactly forty hours a week and then suddenly dropping to zero is rapidly disappearing. Instead, older adults are negotiating phased retirements with their current employers. Companies, eager to retain institutional knowledge in a shifting labor market, are increasingly willing to let senior employees gradually scale back their hours over three to five years.

This phased approach provides a profound psychological benefit by softening the emotional blow of losing a career identity overnight. Financially, it allows you to cover your daily living expenses without tapping into your portfolio, granting your investments more time to compound. Even a part-time income of a few thousand dollars a month can significantly reduce the sequence of returns risk—the danger of drawing down your nest egg during a market dip early in your retirement.

Beyond staying with long-term employers, a surge of older adults are launching consulting businesses, freelancing, or engaging in gig work. This “silver entrepreneurship” leverages decades of industry expertise on your own schedule, transforming work from a mandatory chore into a flexible, intellectual pursuit.

| Factor | Abrupt Retirement | Phased Retirement (The 2026 Trend) |

|---|---|---|

| Income Source | Immediate reliance on portfolio, pensions, and Social Security. | Partial salary covers baseline expenses; delays portfolio withdrawals. |

| Healthcare | Must secure Medicare or private coverage immediately. | May retain employer health benefits while working reduced hours. |

| Social Security | Often claimed early out of financial necessity, reducing lifetime payout. | Allows for strategic delay until Full Retirement Age or age 70. |

| Mental Transition | High risk of identity loss and lack of daily structure. | Gradual adjustment; maintains social connections and mental engagement. |

2. Smart Home Integration Making “Aging in Place” Attainable

For decades, the desire to stay in one’s own home was often derailed by physical decline and safety concerns. In 2026, accessible smart home technology has bridged the gap between independent living and necessary medical oversight. Today’s smart home goes far beyond voice-activated thermostats and security cameras; it integrates directly into your health and wellness routines.

Ambient sensors can now detect changes in your daily gait or routine, alerting you or a family member to potential mobility issues before a fall occurs. Smart pill dispensers track medication compliance and notify caregivers if a dose is missed. Wearable technology monitors blood oxygen levels, heart rhythms, and sleep quality, sending data directly to your healthcare provider’s dashboard.

To implement this trend successfully, you must proactively upgrade your home environment while you are still healthy. The National Institute on Aging (NIA) recommends making structural safety modifications alongside technological upgrades. Consider the following essential aging-in-place modifications:

- Installing zero-threshold walk-in showers with reinforced grab bars.

- Upgrading home Wi-Fi networks to support uninterrupted telehealth connections and continuous medical monitoring.

- Replacing traditional knobs with lever-style handles on all doors and faucets.

- Deploying voice-activated lighting to illuminate hallways and bathrooms during the night automatically.

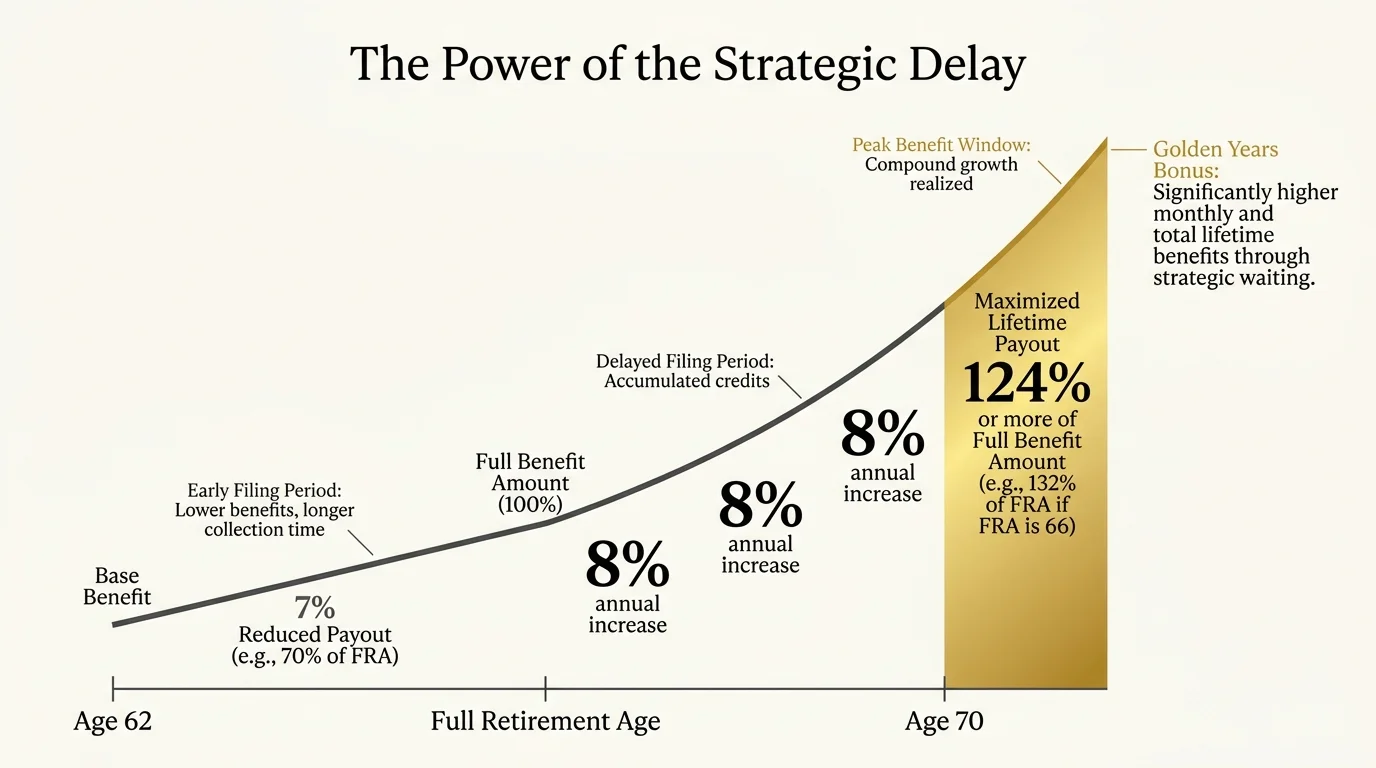

3. Strategic Delay of Social Security Benefits

As life expectancies push well into the late 80s and 90s for healthy adults, the mathematics of claiming Social Security have shifted drastically. While you can claim benefits as early as age 62, doing so permanently locks in a reduced monthly payout. The dominant trend among educated retirees is delaying claims to maximize guaranteed, inflation-adjusted income.

For every year you wait past your Full Retirement Age (FRA) up to age 70, your benefit increases by a guaranteed 8%. In an era where market returns fluctuate and inflation poses a constant threat, locking in an 8% guaranteed return on your baseline income is one of the most powerful financial strategies available. Furthermore, maximizing your benefit provides vital protection for a surviving spouse, who will inherit the higher of the two monthly payments when one partner passes away.

“Retirement is an artificial finish line. It’s an invention. We need to rethink the idea of ceasing to be useful and start thinking about transitioning to a new phase of usefulness.” — Mitch Anthony, Retirement Expert and Author

This mindset shift—treating your 60s as a transitional phase rather than an end date—makes delaying benefits much more feasible. You can explore exact benefit projections and verify your FRA directly through the Social Security Administration (SSA) portal.

4. Maximizing the New Medicare Landscape

Healthcare costs remain one of the largest expenses in retirement, but 2026 brings a more predictable landscape for out-of-pocket costs. Following legislative changes over the past few years, the $2,000 annual cap on out-of-pocket prescription drug costs under Medicare Part D is now fully entrenched. This provides massive financial relief for retirees managing chronic conditions or requiring expensive specialty medications.

Retirees are also becoming highly analytical about their Medicare choices, moving away from auto-renewing plans and actively comparing Original Medicare with Medicare Advantage. Telehealth, once a temporary pandemic measure, is now a permanent and heavily utilized feature of senior healthcare. Routine check-ups, mental health therapy, and chronic disease management are routinely handled via secure video links, saving you time and reducing exposure to clinical waiting rooms.

To navigate these shifts effectively, you should conduct an annual review of your health coverage during the Open Enrollment period. Formularies change, and a plan that covered your medications perfectly last year might not be the most cost-effective option today. Utilize the tools available at Medicare.gov to input your specific prescriptions and project your exact costs for the upcoming year.

5. Downsizing to “Middle Housing” and Walkable Communities

The concept of downsizing used to mean selling a large family home in the suburbs and moving into a massive retirement community in the Sunbelt. Today, seniors are increasingly seeking “middle housing”—smaller, highly functional living spaces integrated directly into vibrant, multi-generational neighborhoods.

This includes moving into townhomes, cottage courts, or apartments located in walkable suburban cores where driving is optional. Walkability heavily influences retirement housing decisions in 2026, as older adults prioritize easy access to grocery stores, cafes, healthcare facilities, and cultural events without relying on a vehicle.

Accessory Dwelling Units (ADUs)—also known as granny flats or backyard cottages—are another exploding trend. Building an ADU on an adult child’s property allows you to maintain independent living quarters while staying intimately connected to your family’s daily life. It also serves as a brilliant financial maneuver; you can sell your primary residence, fund the construction of the ADU, and invest the substantial remaining equity to generate ongoing retirement income.

6. The “Silver Divorce” Financial Recalibration

Divorce rates among adults over the age of 50 have remained persistently high, creating a unique set of financial challenges often referred to as “silver divorce.” Splitting a marital estate late in life drastically alters your retirement timeline. Instead of funding one household, the same pool of assets must now sustain two separate lives, effectively doubling housing and utility expenses.

Navigating a late-in-life divorce requires meticulous attention to asset division, particularly regarding retirement accounts. A Qualified Domestic Relations Order (QDRO) is absolutely critical when dividing 401(k)s or pensions, ensuring the transfer of funds occurs without triggering massive tax penalties or early withdrawal fees.

If you find yourself facing a silver divorce, you must immediately recalibrate your financial plan. This often involves delaying retirement by a few years, aggressively downsizing your housing, and updating your estate documents. You must ruthlessly revise your beneficiary designations on all life insurance policies, IRAs, and bank accounts to reflect your new reality.

7. Multi-Generational Living for Financial Defense

In response to elevated housing costs and childcare expenses, families are increasingly pooling their resources under one roof. Multi-generational living is no longer seen as a compromise; it is a strategic financial defense mechanism that benefits everyone involved.

For retirees, contributing to a shared household can dramatically lower your monthly overhead. You might provide essential childcare for your grandchildren, allowing your adult children to advance their careers without the crushing burden of daycare costs. In return, your adult children provide you with immediate housing security and a built-in support system as you age.

When entering a multi-generational living arrangement, clear financial boundaries are paramount. Draft formal agreements outlining who pays for utilities, property taxes, and groceries. Discuss long-term care expectations openly so that all generations understand their financial and physical responsibilities before a health crisis forces the issue.

8. Purpose-Driven Spending and “Giving While Living”

The traditional estate planning model focused on accumulating wealth until death and passing down a lump sum to heirs. In 2026, modern retirees are embracing the philosophy of “giving while living.” Rather than leaving adult children a large inheritance when they are already established in their 50s or 60s, retirees are deploying their capital when it can make the most significant impact.

This might involve helping a grandchild avoid student loan debt by funding a 529 plan, assisting an adult child with the down payment on a first home, or funding a multi-generational family vacation to create lasting memories. Experiencing the joy of your wealth alongside your family provides an emotional return on investment that a posthumous transfer simply cannot match.

Charitable giving has also evolved. Retirees are utilizing strategies like Qualified Charitable Distributions (QCDs) to transfer funds directly from their IRAs to qualified charities. This satisfies their Required Minimum Distributions (RMDs) without increasing their taxable income, allowing them to support causes they care about while optimizing their tax liability.

What Can Go Wrong

Even with careful preparation, a few common missteps can threaten your financial security during your later years. Avoid these major pitfalls:

- Underestimating Healthcare Inflation: While Medicare caps help with prescriptions, standard medical inflation often outpaces general economic inflation. Failing to build a dedicated healthcare buffer into your savings can force you to drain your primary portfolio.

- Remaining “House Rich and Cash Poor”: Holding onto a massive family home ties up hundreds of thousands of dollars in illiquid equity while driving up your maintenance, insurance, and property tax costs.

- Falling for Sophisticated Digital Scams: As seniors adopt more technology, they become prime targets for AI-driven voice cloning scams and sophisticated phishing attacks. Never transfer funds or provide account details based on an inbound phone call or text message.

- Ignoring Tax Diversification: If all your savings are in pre-tax 401(k)s or traditional IRAs, you have a looming tax problem. Every withdrawal will be taxed as ordinary income, which can push you into higher brackets and cause your Medicare premiums to spike via the Income-Related Monthly Adjustment Amount (IRMAA).

When to Consult a Professional

While educating yourself is crucial, certain situations require specific expertise to prevent costly permanent errors. You should seek guidance from a fee-only fiduciary advisor found through the Certified Financial Planner Board in these scenarios:

Approaching Your Required Minimum Distributions (RMDs): At age 73 (or 75 depending on your birth year), you must begin withdrawing funds from traditional retirement accounts. A professional can help you sequence these withdrawals to minimize your lifetime tax burden.

Navigating a Late-in-Life Divorce: Do not attempt to divide complex pensions, stock options, or 401(k) accounts without legal and financial counsel. A specialized advisor will ensure your QDRO is executed flawlessly.

Structuring a Reliable Income Floor: If you are transitioning from a steady paycheck to living off a portfolio, an advisor can help you build an income floor using guaranteed sources (Social Security, pensions, fixed annuities) to cover your non-negotiable living expenses.

Frequently Asked Questions

Can I still work if I collect Social Security?

Yes, but if you claim benefits before your Full Retirement Age (FRA) and earn over a certain annual limit, the SSA will temporarily withhold a portion of your benefits. Once you reach FRA, you can earn an unlimited amount of money without any reduction to your monthly Social Security check.

How do Medicare out-of-pocket caps work in 2026?

Under Medicare Part D, your out-of-pocket spending for covered prescription drugs is capped at $2,000 annually. Once you hit this limit, you pay nothing out-of-pocket for covered Part D drugs for the remainder of the calendar year. This cap applies whether you have a standalone Part D plan or a Medicare Advantage plan with drug coverage.

What is an Accessory Dwelling Unit (ADU)?

An ADU is a secondary housing unit located on the same lot as a primary single-family home. Often called a backyard cottage or an in-law suite, an ADU includes its own kitchen, bathroom, and living space. They are increasingly popular for retirees who want to downsize and live near family while maintaining full independence.

Should I pay off my mortgage before retiring?

Entering retirement debt-free drastically lowers your monthly living expenses, which reduces the amount you must withdraw from your retirement accounts. However, if you have a historically low fixed interest rate, it may make mathematical sense to keep the mortgage and allow your investments to continue compounding at a higher rate of return. A financial planner can help you weigh the psychological comfort of being debt-free against the mathematical reality of your specific interest rate.

The retirement landscape of 2026 offers more flexibility, technological support, and lifestyle options than any previous generation experienced. By embracing phased transitions, optimizing your healthcare choices, and thoughtfully designing your living arrangements, you can build a resilient plan that supports you for decades to come. Take the time to review your strategy this year, update your financial models, and ensure your daily life aligns with your long-term goals.

This is educational content based on general retirement and financial principles. Individual results vary based on your situation. Always verify current benefit rules, tax laws, and eligibility requirements with official sources like SSA, Medicare.gov, or the IRS.

Leave a Reply