The traditional retirement model of settling quietly onto a golf course is officially obsolete in 2026, replaced by dynamic strategies that protect your wealth and lifestyle. You must balance unprecedented longevity with shifting economic realities by adapting your approach to housing, healthcare, and income generation. Modern retirees are rewriting the rules of the post-career years, prioritizing flexible living arrangements and strategic spending over rigid accumulation. From climate-driven relocation patterns avoiding skyrocketing insurance premiums to the rapid adoption of subscription-based medical care, these sudden shifts demand attention. Anticipating these eight emerging trends allows you to design a more fulfilling, financially resilient next chapter, ensuring your portfolio and your health keep pace with an evolving landscape.

Trend 1: The Silver Gap Year Replaces Immediate Downsizing

For decades, the standard retirement playbook dictated that you leave your job, immediately sell your family home, and downsize into a smaller property or a dedicated senior community. In 2026, a rapidly growing segment of new retirees is hitting pause on permanent real estate decisions to embrace the “Silver Gap Year.”

Taking inspiration from college students, modern retirees are utilizing their first twelve to eighteen months of financial independence for extended, immersive travel or passion projects. Instead of rushing to pack boxes, many are renting out their primary residences and booking long-term stays in locations they always wanted to explore. This allows you to test out potential relocation destinations—from coastal towns to mountain retreats—without committing hundreds of thousands of dollars to a new mortgage.

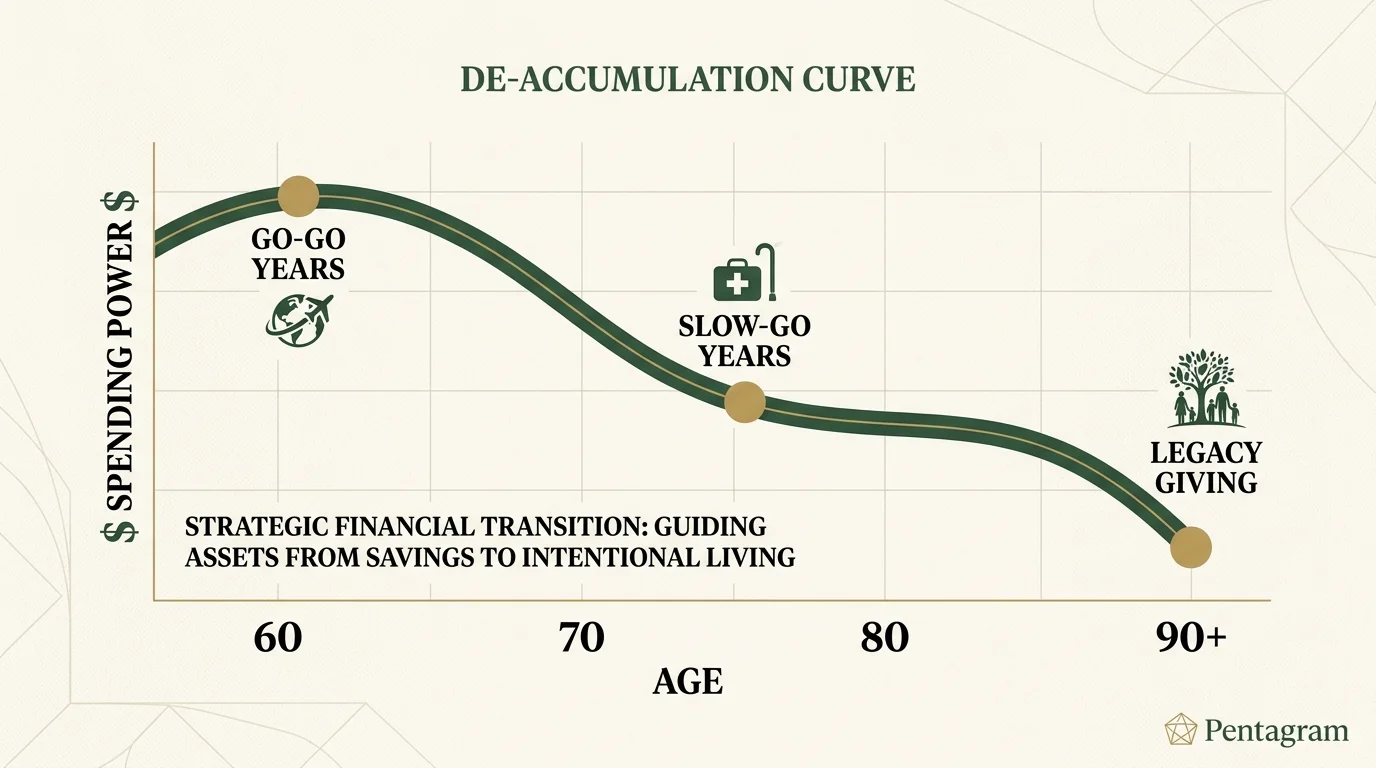

This trend capitalizes on the “go-go” years of retirement. Financial planners often divide retirement into three phases: the go-go years characterized by high energy and travel, the slow-go years where you stay closer to home, and the no-go years focused on healthcare and comfort. By prioritizing aggressive travel and experiential spending immediately upon leaving the workforce, you maximize your physical health and mobility when it matters most.

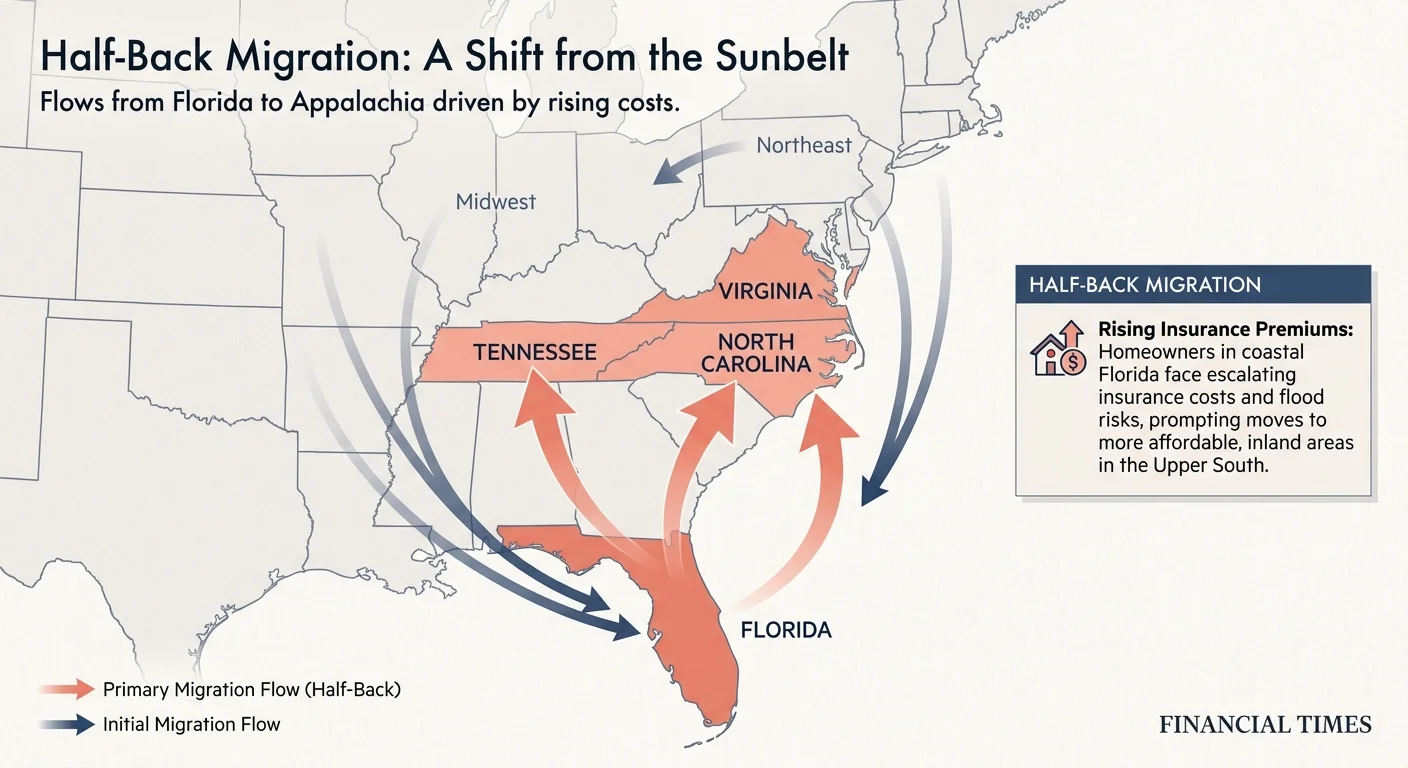

Trend 2: Climate and Insurance Costs Drive the “Half-Back” Migration

The predictable migration pipeline from the Northeast and Midwest straight to Florida or Arizona has fractured. Severe weather events and exponentially rising property insurance premiums have forced a massive recalculation for retirees living on fixed incomes. When coastal property insurance policies double or triple in a single year, the dream of a beachfront retirement quickly turns into a financial liability.

We are now seeing the acceleration of the “half-back” migration and the rise of climate-resilient retirement destinations. Retirees who initially moved to deep Southern coastlines are moving halfway back north to states like North Carolina, Tennessee, and Virginia. Furthermore, inland areas in the Midwest and the Appalachian regions are experiencing a surge in retiree populations. These areas offer moderate climates, manageable cost of living, and most importantly, stable property insurance markets.

If you are planning a relocation, you must factor in the total cost of ownership—not just the property tax rate. A state with no income tax might initially look appealing, but if home insurance and extreme cooling costs consume your monthly budget, your overall financial security will suffer.

Trend 3: The Surge of “Giving While Living”

Waiting until you pass away to transfer wealth to the next generation is becoming a relic of the past. The 2026 economic landscape—marked by high housing costs for younger adults—has accelerated the trend of “giving while living.” Retirees are increasingly opting to distribute portions of their legacy early, directly witnessing the impact of their wealth.

This approach offers immense practical benefits. Helping an adult child secure a down payment on a home or funding a grandchild’s college education provides immediate family stability. Financially, it often makes more sense to help your children avoid high-interest mortgage debt today rather than leaving them a lump sum decades from now.

Executing this strategy requires an understanding of tax regulations. You can leverage the annual gift tax exclusion to move wealth efficiently. For the most accurate and current limits on tax-free gifting, you should always consult the official guidelines provided by the Internal Revenue Service (IRS) to avoid unintended tax consequences for you or your heirs.

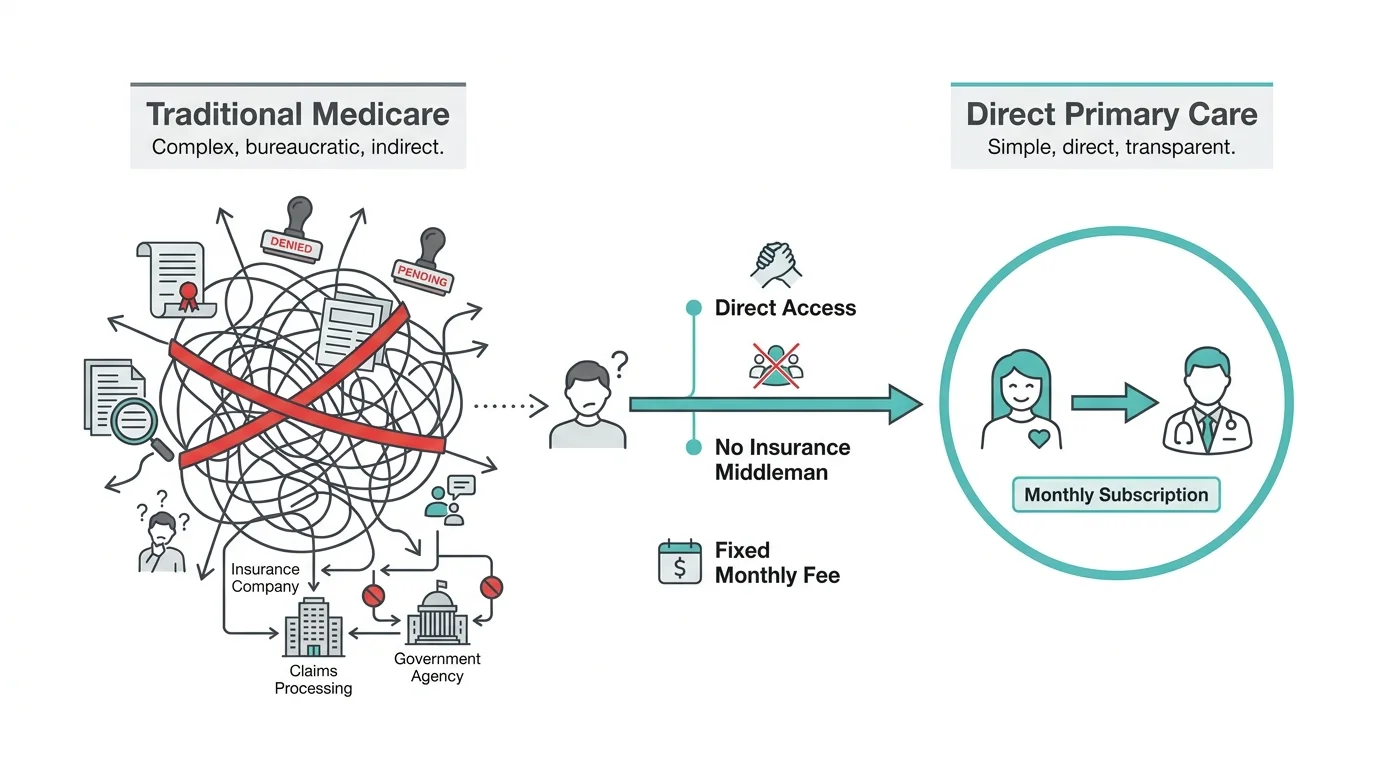

Trend 4: Direct Primary Care as a Healthcare Supplement

Navigating the healthcare system is often the most stressful aspect of aging. While Medicare remains the foundation of retiree healthcare, access to primary care physicians has become increasingly difficult due to doctor shortages and shrinking appointment times. Enter the mainstream adoption of Direct Primary Care (DPC).

Once confused with expensive “concierge medicine” reserved for the ultra-wealthy, modern DPC is highly accessible. For a flat monthly subscription fee—often ranging from $75 to $150—you gain unrestricted access to a primary care physician. This includes same-day appointments, extended visits, and direct text or email communication with your doctor.

DPC practices do not bill insurance, which removes massive administrative overhead for the clinic and allows doctors to take on fewer patients. It is crucial to note that a DPC membership does not replace traditional health insurance. You still need comprehensive coverage through Medicare.gov or a Medicare Advantage plan to cover hospitalizations, surgeries, prescriptions, and specialist care. However, pairing standard Medicare with a DPC subscription guarantees you have a dedicated doctor ready to manage your day-to-day health proactively.

Trend 5: Micro-Consulting and the “Returnship”

The concept of a hard-stop retirement—working forty hours a week on Friday and zero hours on Monday—is fading. Many retirees find that an abrupt exit from the workforce leads to a loss of identity, reduced cognitive stimulation, and an unexpected sense of isolation. In response, 2026 has brought the rise of the “returnship” and micro-consulting.

Advancements in remote work infrastructure have made it incredibly easy for older professionals to monetize their decades of expertise on their own terms. Instead of taking low-wage retail jobs just to stay busy, retirees are acting as fractional executives, industry mentors, or project-based consultants. You might work ten hours a week entirely from your home office, commanding a high hourly rate while maintaining total control over your schedule.

“Retirement is an illusion. We need a balance of vocation and vacation. It is not about the money; it is about having a reason to get out of bed in the morning and a purpose that keeps you engaged with the world.” — Mitch Anthony, Retirement Expert

This phased approach to retirement allows you to keep your professional network alive, generate supplemental income that protects your investment portfolio from early drawdowns, and maintain a profound sense of purpose.

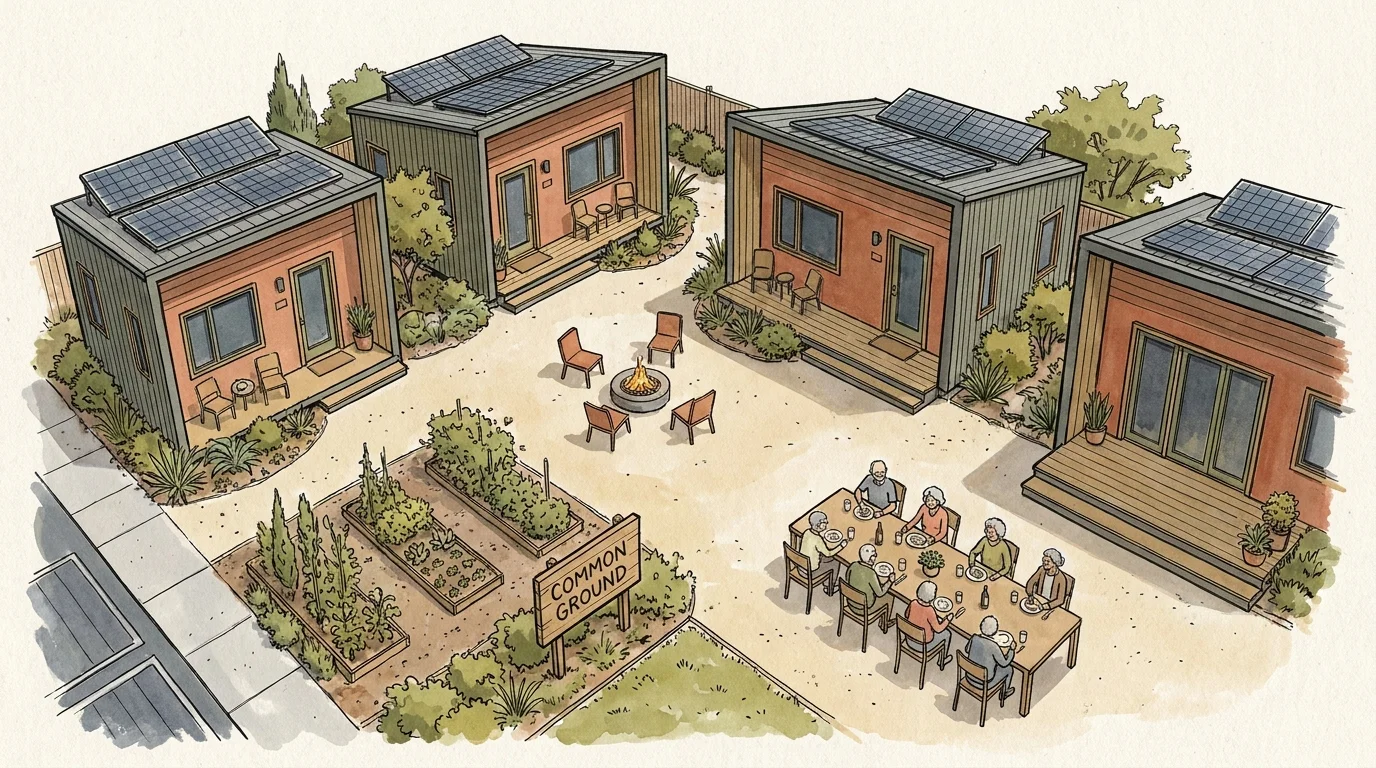

Trend 6: Micro-Communities and Senior Co-Housing

Loneliness is one of the most significant health risks older Americans face. To combat isolation and reduce the soaring costs of independent living facilities, creative retirees are pioneering senior co-housing arrangements. Often dubbed the “Golden Girls” model, this trend involves two or more unrelated adults purchasing or renting a large home to share.

By pooling resources, you can afford a more accessible, luxurious home than you could alone, often enabling you to hire shared household help, private chefs, or in-home care workers. It provides built-in socialization while maintaining private living quarters. According to resources from organizations like AARP, shared housing is one of the fastest-growing living arrangements for adults over sixty-five.

| Living Arrangement | Financial Structure | Social Interaction | Independence Level |

|---|---|---|---|

| Traditional Aging in Place | Bear 100% of mortgage, taxes, and maintenance alone. | Low; high risk of isolation. | High; complete autonomy over lifestyle. |

| Senior Co-Housing | Split housing costs, utilities, and potential in-home care 2-4 ways. | High; built-in community and daily engagement. | Moderate; requires compromise on shared spaces and house rules. |

| Independent Living Facility | High monthly fees covering rent, meals, and amenities. | Very High; organized activities and dining halls. | Moderate; subject to facility schedules and corporate policies. |

Trend 7: De-Accumulation Coaching Becomes Mainstream

If you have spent forty years diligently saving and investing, shifting your mindset to actually spending that money can be psychologically jarring. Many retirees suffer from a scarcity mindset, living far below their means out of fear that their money will run out, ultimately leaving behind massive portfolios but missing out on experiences they could easily afford.

The financial services industry has recognized this anxiety. In 2026, financial advisors are increasingly acting as “de-accumulation coaches.” Rather than just telling you how to grow your wealth, modern advisors focus on giving you the psychological permission to spend it safely. They utilize advanced software to create dynamic withdrawal strategies, showing you exactly how much you can spend each month—even adjusting for inflation and market downturns—without endangering your long-term security.

This coaching helps you transition from being a wealth accumulator to a confident wealth distributor, ensuring you actually enjoy the fruits of your lifelong labor.

Trend 8: AI-Assisted Benefit Optimization

Navigating the labyrinth of government benefits used to require spreadsheets, guesswork, and endless phone calls. Today, artificial intelligence is democratizing elite financial planning. Retirees are using specialized AI tools to model thousands of different claiming scenarios for their government benefits.

These algorithms analyze your health status, life expectancy, portfolio size, and tax brackets to pinpoint the exact month you should claim benefits to maximize your lifetime payout. While you should always verify your basic earnings record and formal claiming rules directly with the Social Security Administration (SSA), leveraging modern technology to run the mathematical permutations ensures you do not leave tens of thousands of dollars on the table due to suboptimal claiming timing.

Pitfalls to Watch For

Embracing new retirement trends requires careful planning to avoid self-inflicted financial wounds. Keep these critical pitfalls in mind as you navigate this evolving landscape:

- Moving blindly without a trial run: Relocating based on a week-long vacation is dangerous. Always rent in a new city during its worst weather season (e.g., August in the South, February in the Midwest) before buying property.

- Triggering unintentional tax burdens: “Giving while living” can trigger generation-skipping transfer taxes or capital gains issues if you gift appreciated assets incorrectly. Always consult a tax professional before making large transfers.

- Overlapping healthcare costs: If you purchase a Direct Primary Care membership, ensure you are not simultaneously paying for a premium Medicare Advantage plan that includes overlapping services you will no longer use.

- Entering co-housing without legal contracts: Sharing a home with friends requires formal legal structures—like a Tenancy in Common agreement or an LLC—dictating what happens if someone wants to sell, becomes ill, or passes away.

Frequently Asked Questions

Will working a micro-consulting job reduce my Social Security benefits?

It depends on your age. If you have not yet reached your Full Retirement Age (FRA), earning income above a specific annual limit set by the SSA will cause a temporary withholding of a portion of your benefits. However, once you reach your FRA, you can earn an unlimited amount of money through consulting or employment without any reduction to your monthly Social Security check.

Can I use funds from a Health Savings Account (HSA) to pay for a Direct Primary Care subscription?

The rules regarding DPC memberships and HSAs are complex and have been subject to legislative debate. Historically, the IRS has viewed DPC fees as a health plan rather than a qualified medical expense, making them ineligible for HSA funds. However, specific legislative updates may change this status. Always verify current IRS guidelines with a tax advisor before using HSA funds for subscription fees.

Do I have to pay taxes on the money I gift to my adult children?

Generally, the giver is responsible for any gift tax, not the recipient. However, the IRS provides a generous annual exclusion limit per recipient. If you give less than this annual limit, you do not have to report it. Even if you exceed the annual limit, you likely will not owe taxes immediately; the excess simply counts against your lifetime estate and gift tax exemption limit, which currently sits in the millions of dollars.

Your Next Steps for a Resilient Retirement

The retirement landscape of 2026 demands flexibility and proactive planning. You do not have to adopt every trend listed here to succeed, but you should evaluate which of these shifts could improve your quality of life. Start by reviewing your current financial plan and identifying one area—whether it is exploring a Direct Primary Care doctor, discussing a trial gap-year travel plan, or assessing your home insurance risks—where you can take immediate action.

This article provides general retirement education and information only. Every retiree’s situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: March 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply