Your Social Security claiming strategy could be the difference between a comfortable retirement and decades of financial stress. Because the rules governing your benefits change annually, relying on outdated advice can permanently reduce your lifetime income and expose you to unexpected taxes. Right now, navigating the complexities of the system requires a clear understanding of the latest cost-of-living adjustments, updated earnings limits, and shifting full retirement age requirements. Whether you are finalizing your exit from the workforce, working part-time while collecting, or simply trying to optimize your monthly check, mastering these current regulations is essential. This guide breaks down exactly how the system operates today, offering practical strategies to help you maximize your benefits and secure your financial future.

The 2026 Social Security Landscape: What Just Changed

The economic shifts of the past few years have dramatically altered the retirement landscape, prompting the Social Security Administration to implement several critical adjustments for 2026. Understanding these baseline numbers is the first step toward optimizing your retirement income.

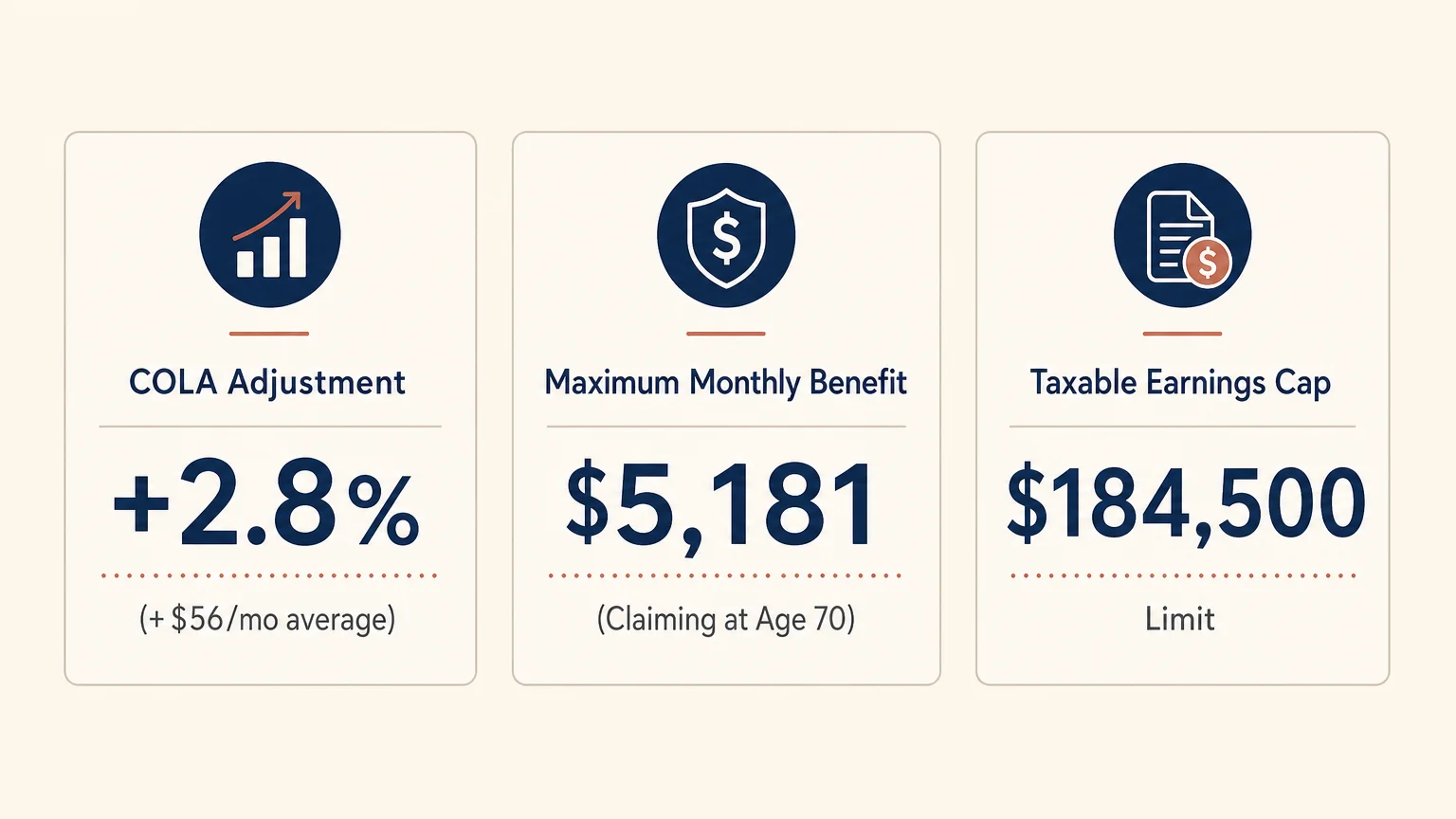

Most notably, beneficiaries saw a 2.8 percent Cost-of-Living Adjustment (COLA) take effect in January 2026. While this increase is more modest than the massive inflation-driven spikes seen earlier in the decade, it still provides a crucial buffer against rising living expenses. For the average retired worker, this 2.8 percent adjustment translated to an increase of approximately $56 per month, pushing the average monthly check higher. For high-income earners who strategically delayed their claims, the maximum possible benefit for an individual retiring at age 70 in 2026 has reached an impressive $5,181 per month.

However, the government also raised the threshold for the workers funding the system. The maximum taxable earnings limit—the wage base on which you must pay Social Security payroll taxes—increased to $184,500 in 2026. Any earned income above this line is free from the 6.2 percent Social Security tax. If you are still working, this means a larger portion of your high-end salary is subject to taxation this year, though it also means those earnings will ultimately factor into a higher future benefit calculation.

Understanding How Your Benefit is Calculated

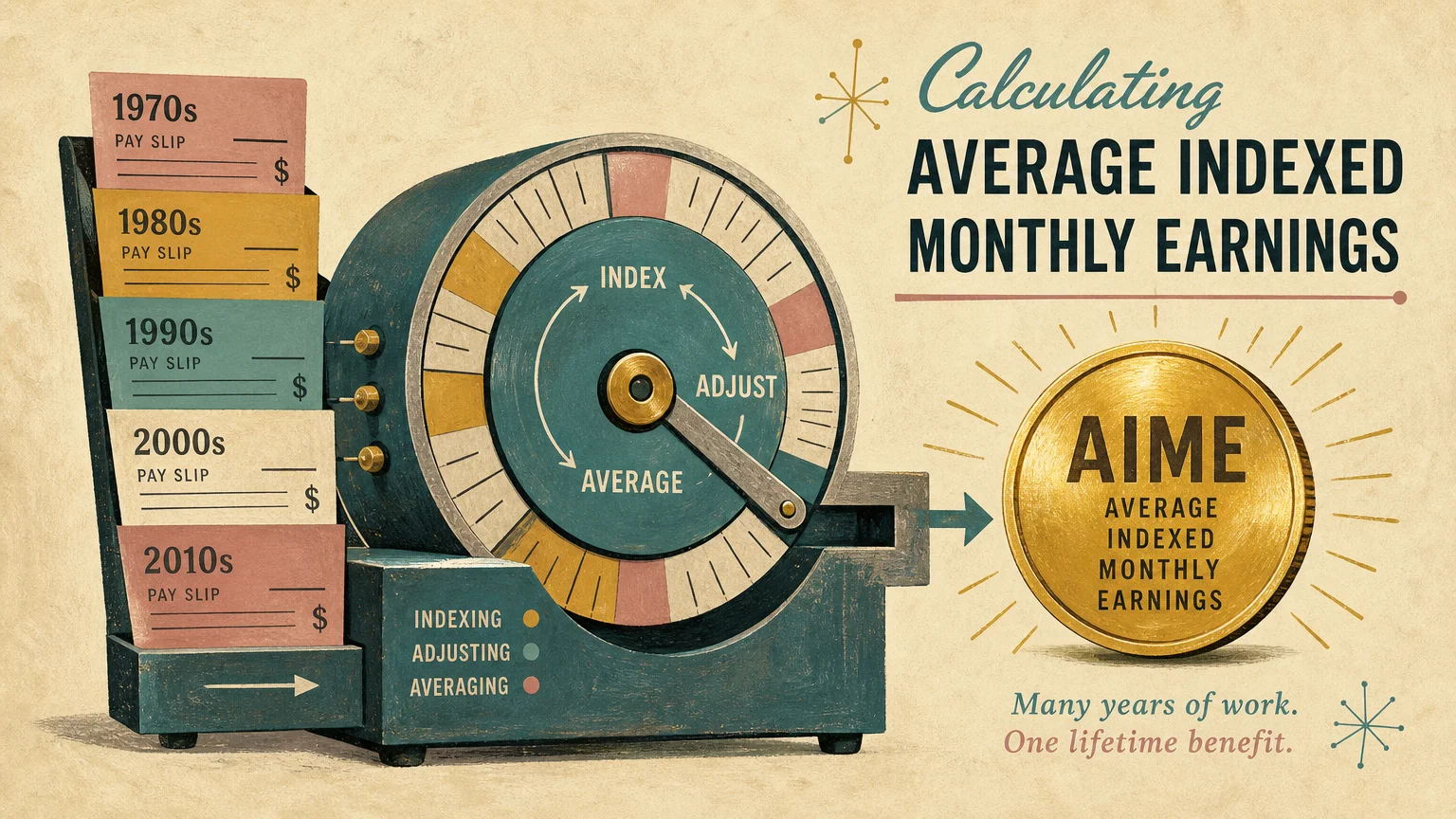

Before you can make an informed decision about when to claim, you need to understand exactly how the government calculates your check. Your benefit is not a flat rate, nor is it strictly based on your final few years of salary. Instead, the Social Security Administration uses a formula based on your Average Indexed Monthly Earnings (AIME).

The system reviews your entire lifetime earnings history and adjusts your past wages for inflation to ensure a dollar earned in 1990 carries the same weight as a dollar earned today. From there, the SSA plucks out your 35 highest-earning years. If you do not have 35 full years of earnings on your record, the administration inserts zeros for the missing years, which heavily dilutes your average. For those nearing retirement with fewer than 35 working years, working just a few extra years—even part-time—can replace those zeros and permanently lift your baseline benefit.

Once your AIME is established, the SSA applies a tiered formula to determine your Primary Insurance Amount (PIA). Your PIA is the exact monthly benefit you will receive if you claim at your precise Full Retirement Age. Every claiming strategy, spousal benefit, and survivor benefit uses this single number as its anchor.

Decoding Your Full Retirement Age (FRA)

Your Full Retirement Age is the chronological mile marker where you are entitled to 100 percent of your Primary Insurance Amount. Despite the common misconception that age 65 represents the standard retirement age—largely because that is when Medicare eligibility begins—your FRA is dictated strictly by your birth year.

For individuals born between 1943 and 1954, the FRA was 66. However, Congress implemented a sliding scale for subsequent birth years. If you were born in 1959, your FRA is 66 and 10 months—a milestone this cohort reached in 2025 and 2026. For anyone born in 1960 or later, your Full Retirement Age is permanently set at 67.

Claiming benefits even one month before your FRA results in a permanent reduction to your monthly check. Conversely, waiting past your FRA triggers delayed retirement credits, which supersize your payments. Recognizing your specific FRA is vital because it dictates your claiming timeline, your earnings limits if you continue working, and the exact percentage of benefits your surviving spouse may one day inherit.

Why Timing Your Claim is the Most Important Decision You Will Make

The single most powerful lever you have in retirement planning is the date you file for Social Security. You are legally allowed to claim your retirement benefits as early as age 62, but doing so comes at a steep, permanent cost. When you claim early, the system reduces your benefit by a fraction of a percent for every month you are shy of your Full Retirement Age. If your FRA is 67 and you claim at 62, you accept a 30 percent reduction in your monthly income for the rest of your life.

On the other end of the spectrum, delaying your claim past your FRA provides a massive financial reward. For every year you delay up to age 70, your benefit grows by a guaranteed 8 percent.

“The biggest mistake you can make with Social Security is claiming early out of fear. Delaying your benefits until age 70 is the best financial investment you can make, guaranteeing an 8 percent return every year you wait.” — Suze Orman, Personal Finance Expert

To visualize the dramatic difference your claiming age makes, consider a retiree whose Full Retirement Age is 67, with a Primary Insurance Amount of $2,000 per month.

| Claiming Age | Percentage of PIA | Monthly Benefit | Impact on Lifetime Income |

|---|---|---|---|

| Age 62 | 70% | $1,400 | Permanent 30% reduction. Lowest possible lifetime income if you live past age 80. |

| Age 67 (FRA) | 100% | $2,000 | Standard baseline benefit. No earnings limits apply after reaching this age. |

| Age 70 | 124% | $2,480 | Maximum possible payout. Increases base amount by 24% and maximizes future survivor benefits. |

Deciding when to claim generally comes down to a break-even analysis. If you delay until 70, you forgo eight years of checks you could have collected starting at 62. It takes roughly 10 to 12 years of collecting the larger, delayed checks to break even and surpass the total cumulative amount you would have received by claiming early. If you have a strong family history of longevity and sufficient portfolio assets to bridge the gap, delaying to age 70 acts as incredible longevity insurance against outliving your money.

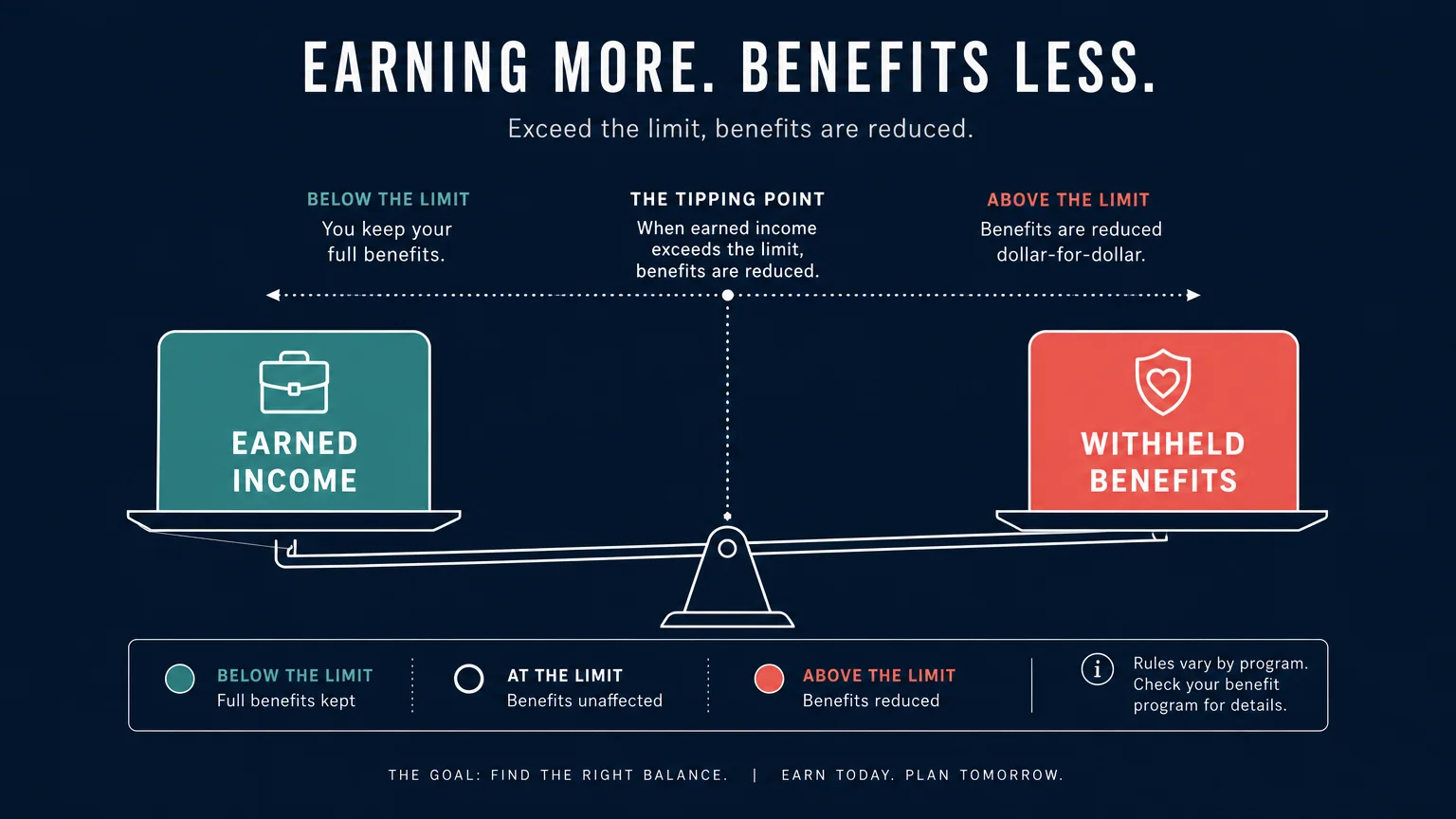

Working While Collecting: The Earnings Test Explained

Many retirees choose to ease out of the workforce by taking a part-time consulting role or starting a small business. If you decide to work while simultaneously collecting Social Security before you reach your Full Retirement Age, you will be subject to the Retirement Earnings Test. This rule is widely misunderstood and often leads to panic when retirees suddenly stop receiving their monthly checks.

The rules for 2026 are highly specific:

- If you are under your FRA for the entire year: You can earn up to $24,480 in 2026 without any penalty. For every $2 you earn above this limit, the SSA will withhold $1 in benefits.

- In the year you reach your FRA: A much more generous limit applies. In the months leading up to your birthday, you can earn up to $65,160 in 2026. For every $3 you earn above this threshold, the SSA will withhold $1 in benefits.

- Once you reach your FRA: The earnings limit disappears entirely. You can earn a million dollars a year, and the SSA will not withhold a single penny of your benefit.

It is vital to understand that the benefits withheld due to the earnings test are not a permanent tax or a fine. The money is not gone forever. When you reach your Full Retirement Age, the SSA automatically recalculates your benefit upward to account for the months you did not receive a check. Essentially, working while collecting early acts as a forced mechanism to delay your benefits, eventually resulting in a larger monthly payout later in life.

How Taxes Impact Your Monthly Check

One of the most unpleasant surprises for new retirees is discovering that the federal government taxes Social Security benefits. Whether or not you owe taxes depends on your “provisional income,” a unique metric used exclusively by the IRS for this purpose.

To calculate your provisional income, add your Adjusted Gross Income (AGI), any nontaxable interest (such as municipal bond yields), and exactly 50 percent of your total annual Social Security benefits. Once you have this number, compare it to the federal thresholds:

- Individual Filers: If your provisional income falls between $25,000 and $34,000, up to 50 percent of your benefits may be taxable. If it exceeds $34,000, up to 85 percent becomes taxable.

- Married Filing Jointly: If your combined provisional income falls between $32,000 and $44,000, up to 50 percent is taxable. If it exceeds $44,000, up to 85 percent is taxable.

Because Congress established these thresholds decades ago and never indexed them for inflation, they trap more middle-class retirees every single year. The steady march of annual COLAs virtually guarantees that over time, a larger portion of your benefit will cross into taxable territory.

To mitigate the so-called “tax torpedo,” proactive financial planning is essential. Strategies like drawing down traditional IRAs before claiming Social Security, funding Roth IRAs (which generate tax-free distributions that do not count toward provisional income), or utilizing Qualified Charitable Distributions (QCDs) can effectively keep your provisional income below the painful taxation thresholds.

Spousal and Survivor Benefits: Protecting Your Partner

Social Security is designed to protect families, not just individual workers. If you are married, your spouse may be eligible to claim a benefit based entirely on your earnings record. A spousal benefit can provide up to 50 percent of the higher earner’s Primary Insurance Amount. To qualify, the spouse claiming the benefit must be at least 62 years old, and crucially, the primary worker must have already filed for their own benefits.

If you are divorced, you might still be eligible to claim on your ex-spouse’s record. The rules require that your marriage lasted for at least 10 consecutive years, you are currently unmarried, and you are at least 62 years old. In cases where you have been divorced for more than two years, you can claim on your ex’s record even if they have not yet filed for their own benefits, provided they are eligible to do so.

Survivor benefits demand an entirely different strategy. When one spouse passes away, the surviving spouse steps up to the higher of the two benefit amounts, while the smaller benefit disappears. Because the survivor inherits 100 percent of the deceased spouse’s check, the highest earner in a household should almost always delay claiming until age 70. Maximizing that primary check ensures that the surviving spouse will retain the largest possible lifetime income when they are forced to drop down to a single Social Security payment.

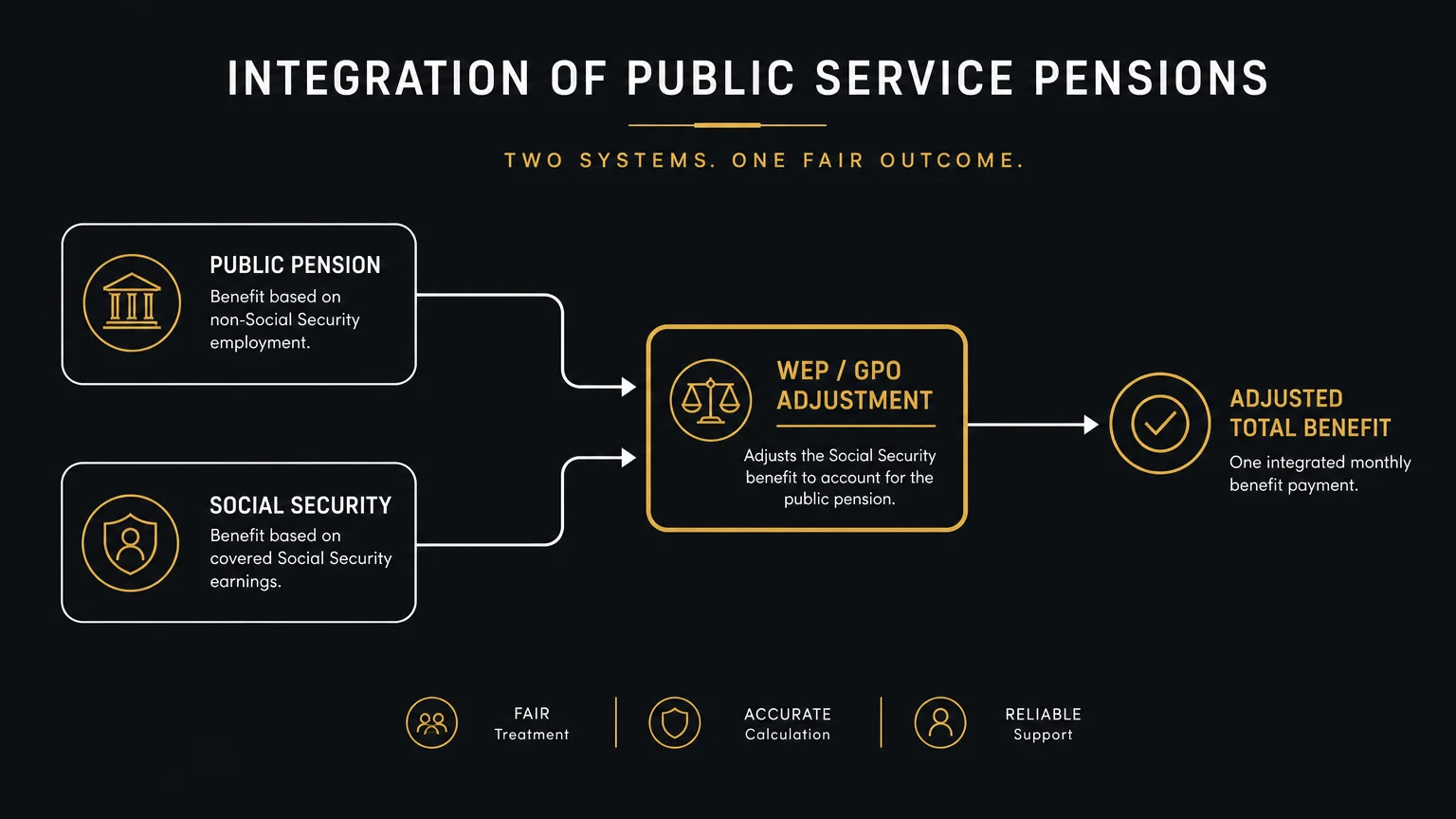

Navigating Public Service Pensions: The WEP and GPO

If you spent part of your career in the private sector paying into Social Security, and another part of your career working for a state or local government that did not participate in the Social Security system, you face unique reduction formulas. Teachers, police officers, firefighters, and postal workers frequently run into the Windfall Elimination Provision (WEP) and the Government Pension Offset (GPO).

The WEP affects your own personal retirement benefit. If you receive a pension from non-covered work, the SSA alters the standard formula used to calculate your AIME and PIA, which can significantly reduce your monthly Social Security check. The reduction cannot wipe out your benefit entirely, and it is capped at half the amount of your non-covered pension, but it represents a severe disruption for those unaware of the rule.

The GPO is often more devastating, as it applies to spousal and survivor benefits. If you receive a government pension from a job where you did not pay Social Security taxes, the GPO reduces any spousal or survivor benefit you might claim on your partner’s record by two-thirds of your government pension amount. For many public servants, this offset completely zeroes out their anticipated spousal or survivor benefits. Proper planning requires running these specialized calculations well before retirement day.

The Future of Social Security: Insolvency Projections

Headlines regularly warn that Social Security is marching toward bankruptcy, causing widespread anxiety among future and current retirees. It is crucial to separate legislative reality from media sensationalism. The Social Security trust funds are indeed facing a depletion date—historically projected around 2034 or 2035.

However, trust fund depletion does not mean the system goes bankrupt or drops to zero. Social Security is a pay-as-you-go system funded by the payroll taxes of current workers. Even if the reserve trust funds dry up entirely, ongoing tax revenues would still be sufficient to pay roughly 78 to 80 percent of promised benefits.

“Do not let the headlines dictate your retirement strategy. While the Social Security trust fund faces real depletion dates, the system is not going bankrupt—Congress has the tools to fix it, and panic-claiming will only lock in a permanent discount on your benefits.” — Jean Chatzky, Financial Editor and Author

Congress has a variety of levers available to close the shortfall before it occurs. They could increase the full retirement age for younger workers, further increase or eliminate the maximum taxable wage base, adjust the formula for calculating COLAs, or modestly increase the payroll tax rate. Current retirees are highly unlikely to see their nominal benefits cut, as doing so would be politically catastrophic. Therefore, you should not let fear of insolvency drive you to claim benefits early against your own mathematical best interests.

Pitfalls to Watch For

Retirees often stumble into a few common, costly traps when transitioning into the Social Security system. Being aware of these pitfalls can save you thousands of dollars over the course of your retirement.

- The Medicare Premium Trap: Social Security and Medicare are deeply intertwined. Your Medicare Part B premiums are deducted directly from your Social Security check. If your retirement income spikes—due to large IRA withdrawals, a Roth conversion, or a property sale—you may trigger the Income-Related Monthly Adjustment Amount (IRMAA). This surcharge drastically increases your Part B and Part D premiums, effectively shrinking your net Social Security check two years later.

- Assuming You Must Claim at 65: Many people mistakenly believe they must file for Social Security when they turn 65 to get Medicare. This is completely false. You should enroll in Medicare at 65 to avoid late penalties, but you can—and often should—leave your Social Security benefits untouched to continue earning delayed retirement credits.

- Ignoring State Taxes: While the IRS taxes benefits at the federal level, a handful of individual states also tax Social Security income. Depending on where you live, you might owe state income tax on your benefits. Reviewing your state’s specific tax code is vital before finalizing your relocation or retirement budget.

- Failing to Verify Your Earnings Record: The SSA relies on employer reporting to track your lifetime wages. If an employer made a clerical error, or a tax return was misfiled decades ago, your record might have a zero where there should be a substantial salary. You must create an account at SSA.gov to review your statement and correct any errors before you file your claim.

Getting Expert Help

While the basic mechanics of Social Security are easy to grasp, the strategic application of these rules to your unique life circumstances often requires professional guidance. Consider consulting a fee-only fiduciary financial planner or a CPA in the following scenarios:

- Coordinating Spousal Claims: If there is a massive discrepancy between your earnings and your spouse’s earnings, an advisor can run advanced breakeven software to determine exactly which months you each should file to maximize your combined lifetime yield.

- Navigating WEP and GPO Reductions: If you are a public worker facing pension offsets, generic online calculators will overestimate your benefits. A professional can help you structure your private assets to account for the exact shortfall.

- Tax Bracket Management: Deciding whether to pull income from a taxable brokerage, a tax-deferred 401(k), or tax-free Roth accounts while simultaneously claiming Social Security is incredibly complex. A tax professional can map out a withdrawal sequence that minimizes your provisional income and protects your benefits from the IRS.

Frequently Asked Questions

Can I change my mind after I claim Social Security?

Yes, but you only have one opportunity. If you claim early and regret it, you can withdraw your application within 12 months of your initial filing. However, you must repay every dollar you and your family received, including any Medicare premiums deducted from your checks. If you are past the 12-month window, you cannot withdraw, but once you reach your Full Retirement Age, you can suspend your benefits to start earning delayed retirement credits again.

Does rental income or investment profit count toward the earnings limit?

No. The Social Security Administration’s Retirement Earnings Test only penalizes you for W-2 wages and net earnings from active self-employment. Passive income streams—such as dividends, capital gains, rental property income, pensions, or IRA withdrawals—do not count toward the annual earnings limit.

Do my benefits automatically double when my spouse dies?

No. When a spouse passes away, the surviving partner does not keep both checks. You are entitled to the higher of the two benefit amounts. The lower benefit drops off entirely. This is why it is so critical for the higher earner in a marriage to delay their claim, ensuring the surviving spouse is left with the largest possible single check.

What happens to my benefits if I move out of the United States?

For the vast majority of retirees, you can receive your Social Security benefits while living abroad. The SSA will send payments to expats residing in dozens of approved countries. However, Medicare generally does not cover healthcare services outside the United States, meaning you will need to secure private international health insurance.

Taking Control of Your Retirement Income

Mastering the modern Social Security landscape requires proactive planning, an understanding of the current tax codes, and a clear vision of your longevity. The most powerful action you can take right now is to pull your latest earnings statement directly from the Social Security Administration, verify your wage history, and calculate your projected benefits at your Full Retirement Age. By treating Social Security as a vital, flexible asset rather than an automatic entitlement, you can strategically weave it into your broader financial plan to provide a durable foundation for your retirement.

This article provides general retirement education and information only. Every retiree’s situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: June 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply