Eliminating federal income taxes on Social Security benefits would keep thousands of dollars in the pockets of middle-income retirees every year. For decades, the federal government has taxed up to 85 percent of these benefits for individuals whose combined income exceeds specific thresholds, directly reducing their spendable cash. If proposals to end this taxation become law, a typical married couple receiving average benefits and supplementing their income with retirement account withdrawals could retain an additional $2,500 to $4,500 annually. Understanding how this shift affects your budget requires looking closely at current income sources and tax brackets. Here is how the numbers break down and what complete tax relief means for your financial independence.

The Unseen Burden: How Social Security Taxation Works Today

Many individuals reach their retirement years under the assumption that their Social Security checks will be entirely theirs to keep. After all, you spent decades paying FICA payroll taxes on your wages to fund the system. However, the reality of filing your first tax return as a retiree often brings a sharp and unpleasant surprise: taxes on Social Security benefits.

The system we navigate today traces its origins back to a series of legislative changes designed to bolster the Social Security Trust Fund. Prior to 1984, Social Security benefits were completely exempt from federal income tax. Facing a severe funding crisis, Congress passed amendments in 1983 that subjected up to 50 percent of a retiree’s benefits to taxation if their income crossed a certain threshold. A decade later, the Omnibus Budget Reconciliation Act of 1993 added a second tier, subjecting up to 85 percent of benefits to taxation for those with slightly higher incomes.

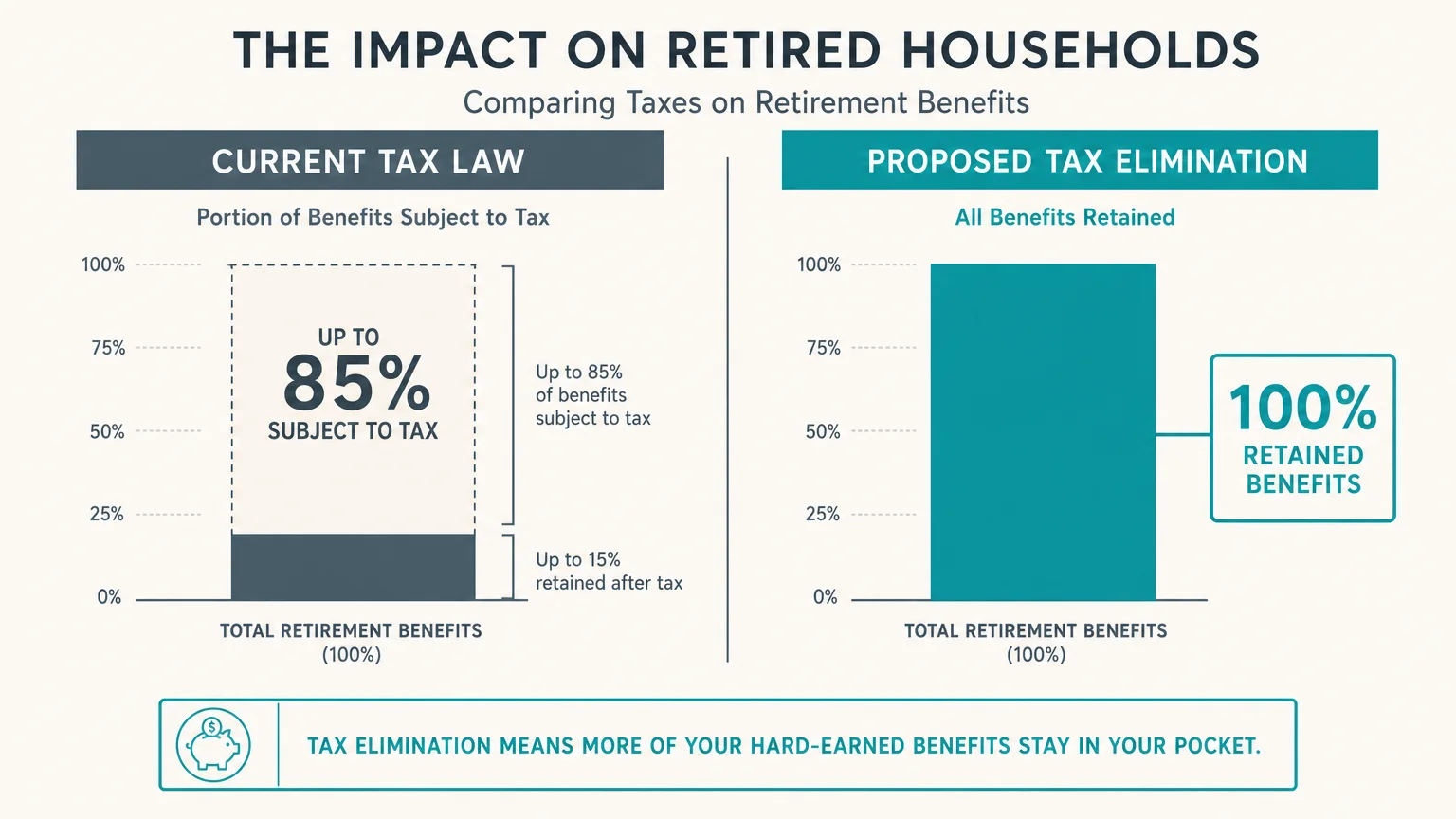

It is vital to understand that having 85 percent of your benefits subject to taxation does not mean you pay an 85 percent tax rate on that money. Rather, it means that up to 85 percent of your total annual benefit amount is added to your taxable income for the year, which is then taxed at your ordinary marginal tax rate. If you fall into the 12 percent or 22 percent federal income tax bracket, that portion of your benefit is taxed at 12 or 22 percent, respectively. Nonetheless, this mechanism routinely drains thousands of dollars from middle-class households—money that could otherwise cover rising healthcare premiums, property taxes, or basic living expenses.

The Mechanics of Combined Income and the Tax Torpedo

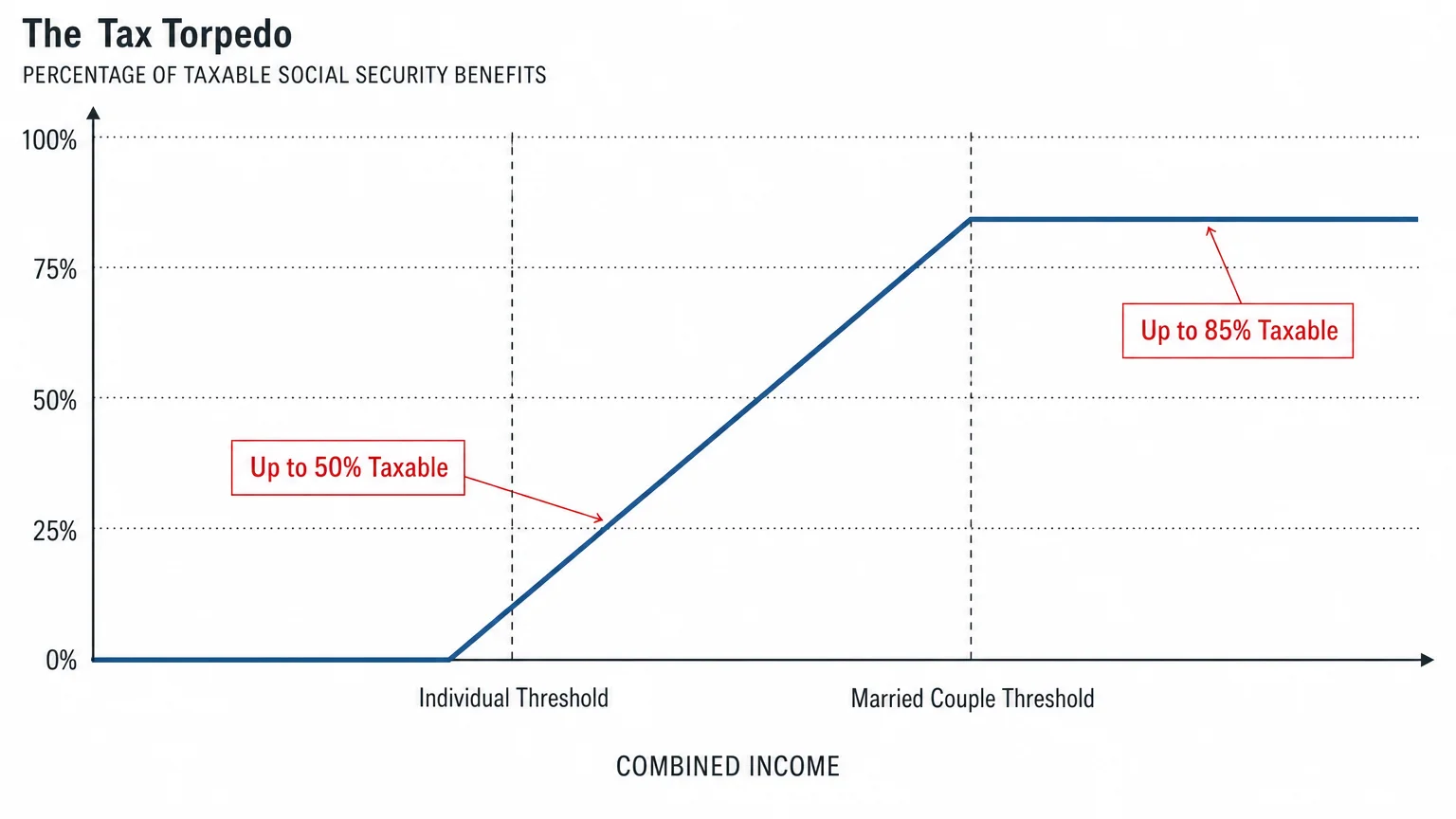

To fully grasp the magnitude of potential Social Security tax elimination, you must understand the convoluted formula the Internal Revenue Service (IRS) uses to determine your tax liability. The IRS calculates a figure known as “Combined Income” (often referred to as provisional income). Your combined income equals your Adjusted Gross Income (AGI), plus any nontaxable interest you receive (such as from municipal bonds), plus 50 percent of your annual Social Security benefits.

For individuals, the thresholds look like this:

- Under $25,000: You pay no taxes on your benefits.

- Between $25,000 and $34,000: Up to 50 percent of your benefits may be taxable.

- Over $34,000: Up to 85 percent of your benefits may be taxable.

For married couples filing jointly, the thresholds are only slightly more generous:

- Under $32,000: You pay no taxes on your benefits.

- Between $32,000 and $44,000: Up to 50 percent of your benefits may be taxable.

- Over $44,000: Up to 85 percent of your benefits may be taxable.

Because these thresholds are so low, pulling money from a traditional IRA or 401(k) to pay for a home repair or a medical bill can push your combined income over the edge. This triggers a phenomenon financial planners refer to as the “tax torpedo.” When you are in the phase-in range for Social Security taxation, taking an additional $1,000 from a traditional IRA does not just increase your taxable income by $1,000. It also pulls another $850 of your Social Security benefits into the taxable realm. Suddenly, your taxable income increases by $1,850 for every $1,000 you withdraw. This hidden marginal tax spike is one of the most punitive elements of the current tax code for middle-income seniors.

How Much Tax Relief Are We Actually Talking About?

If Congress were to implement complete Social Security tax relief, the financial impact on households would be immediate and profound. The exact amount of money you would keep depends entirely on your total retirement income, your filing status, and your marginal tax bracket.

Consider a married couple pulling $40,000 annually from traditional IRAs to supplement a combined $45,000 in Social Security benefits. Under the current law, their combined income is $62,500 ($40,000 from the IRA plus 50 percent of their $45,000 Social Security benefit). Because this exceeds the $44,000 threshold, a large portion of their benefits becomes taxable. Using the IRS formula, roughly $15,725 of their Social Security is added to their taxable income. If they sit in the 12 percent federal tax bracket, they owe approximately $1,887 in federal taxes solely because their Social Security benefits were taxed.

Now, shift the scenario to an upper-middle-class couple receiving $60,000 in Social Security and withdrawing $70,000 from their retirement accounts. Their combined income pushes them well past the top threshold, rendering the maximum 85 percent of their benefits ($51,000) taxable. In the 22 percent bracket, this couple pays a staggering $11,220 in federal taxes just on their Social Security income.

If taxes on Social Security benefits were eliminated entirely, these couples would keep that money. Over a 20-year retirement, that translates to tens of thousands—or even hundreds of thousands—of dollars returned to the retiree’s control, offering immense protection against the rising costs of long-term care and healthcare.

Case Studies: The Financial Impact of Tax Elimination

To visualize the tangible impact of Social Security tax elimination, reviewing side-by-side scenarios provides clarity. The table below illustrates three common retiree profiles and estimates the annual and long-term financial benefits they would experience if federal taxation on these benefits ceased.

| Retiree Profile | Current Annual Income Sources | Estimated Annual Tax on SS Benefits | 10-Year Compounded Savings (Assuming 5% Growth) |

|---|---|---|---|

| Single Retiree (Moderate Income) | $24,000 Social Security $20,000 Traditional IRA Withdrawal |

~$750 | ~$9,433 |

| Married Couple (Middle Income) | $45,000 Social Security $40,000 Traditional IRA Withdrawal |

~$1,887 | ~$23,734 |

| Married Couple (Upper-Middle) | $60,000 Social Security $70,000 Traditional IRA Withdrawal |

~$11,220 | ~$141,123 |

Note: The estimates above assume standard deductions for seniors and current federal marginal tax brackets. Actual individual results vary based on additional income sources and specific deductions.

As the data demonstrates, retiree tax savings compound significantly over time. Reinvesting that retained capital, or simply using it to avoid drawing down core principal in volatile markets, strengthens a retirement portfolio’s longevity. Removing this tax burden effectively gives retirees an instant, guaranteed raise without requiring them to assume any additional investment risk.

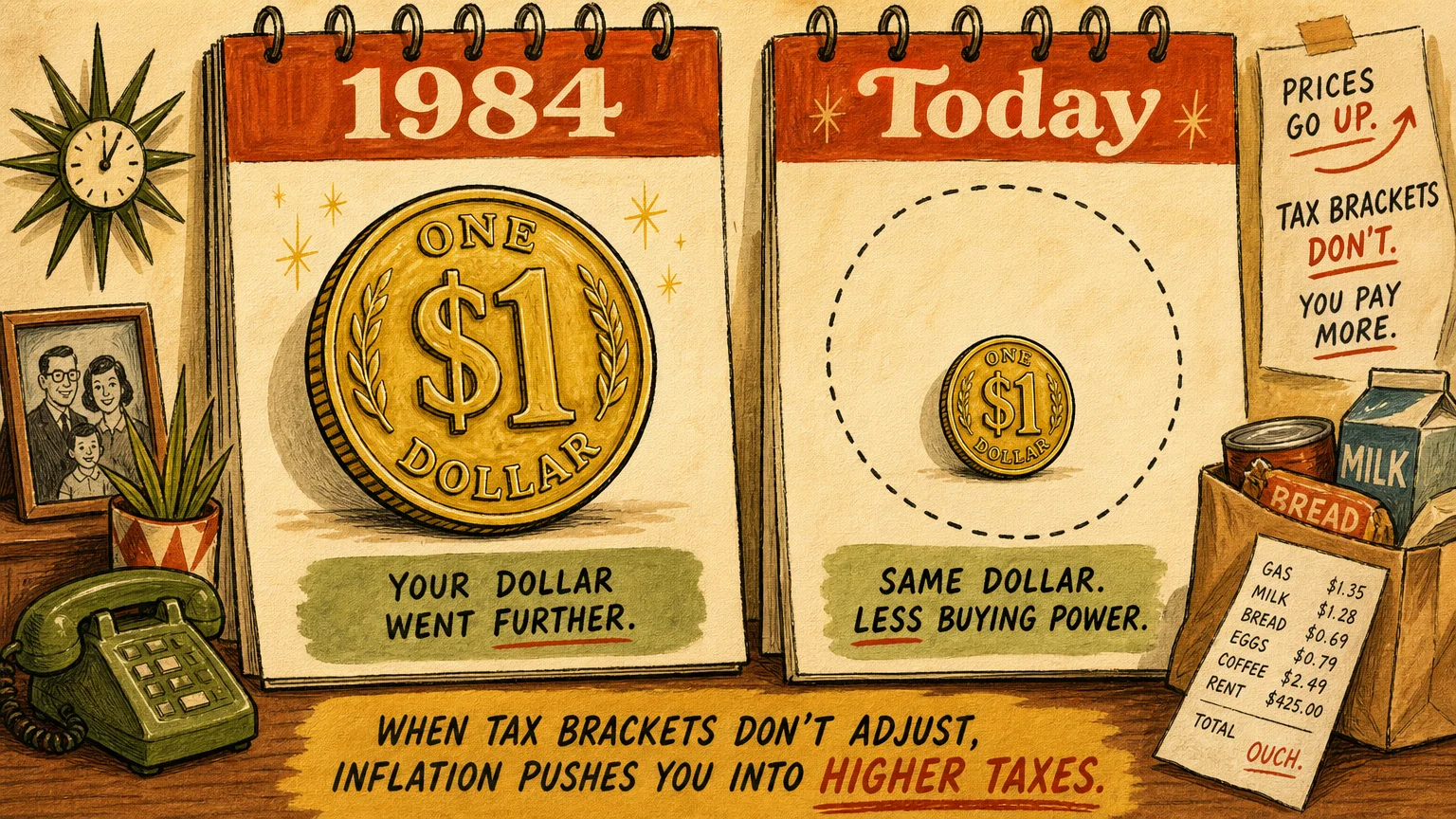

The Inflation Factor: Why the Original Law Hits Harder Today

One of the most frustrating aspects of the current taxation structure is its relationship with inflation—or rather, its lack thereof. When Congress established the income thresholds for taxing Social Security benefits in 1983 and 1993, they intentionally left them unindexed for inflation. This legislative decision created an aggressive, long-term “bracket creep.”

In 1984, the $32,000 threshold for a married couple represented a fairly high income, meaning the tax only affected about 10 percent of the wealthiest retirees. Today, decades of inflation and annual Cost of Living Adjustments (COLAs) have pushed the average retiree’s nominal income far higher. Because the thresholds remain frozen at $32,000 and $44,000, roughly half of all retirees now pay taxes on their benefits. The very mechanism designed to tax wealthy individuals has transformed into a sweeping tax on the middle class.

“Your Social Security is the one guaranteed source of income you can never outlive. Protecting that income from unnecessary taxes and inflation should be a cornerstone of every retirement plan.” — Suze Orman, Personal Finance Expert

Eliminating the tax would instantly correct decades of unadjusted bracket creep. It would restore the purchasing power that seniors have steadily lost as their annual COLAs repeatedly pushed them into higher taxable brackets without providing a corresponding increase in real wealth.

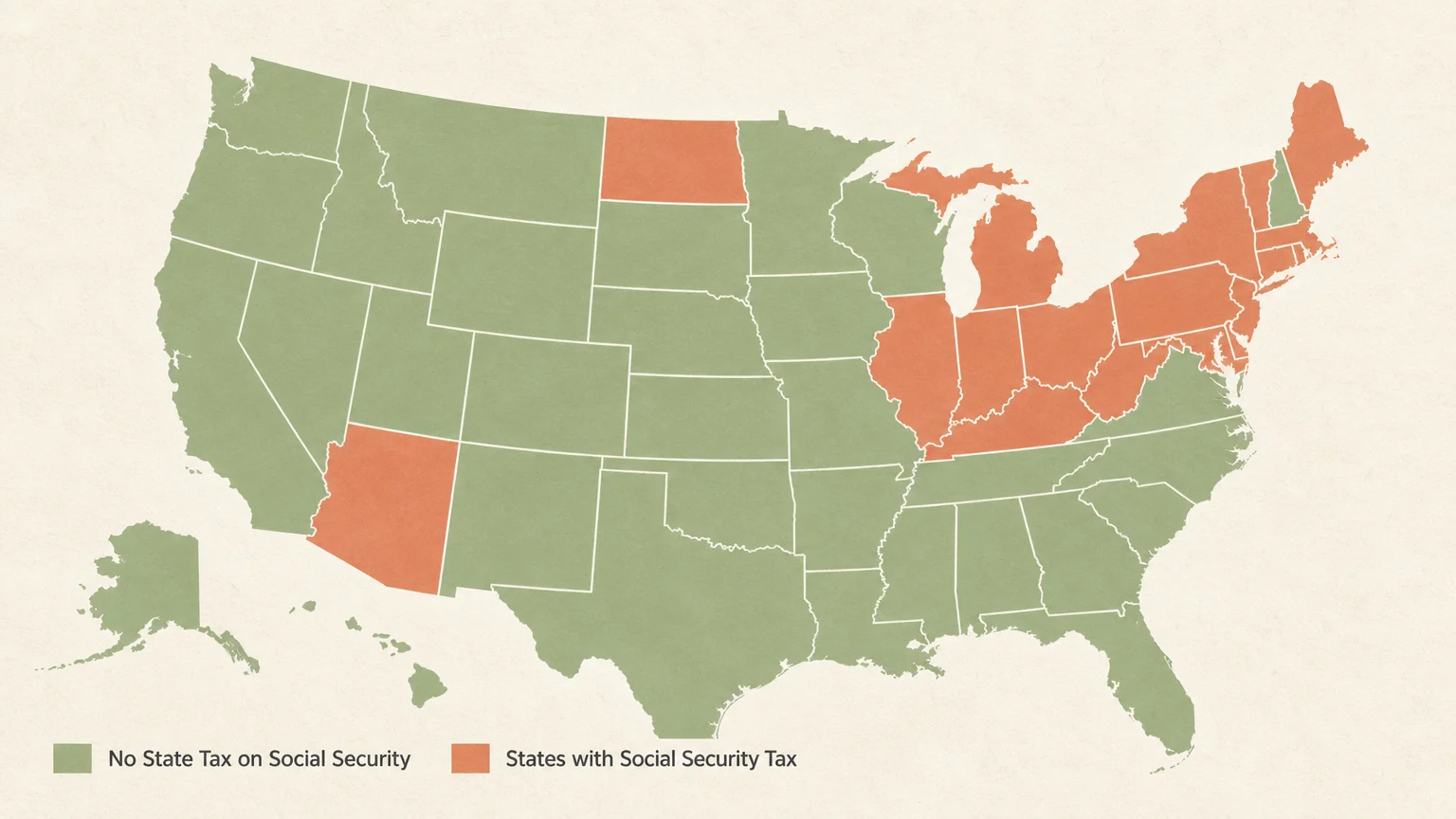

State Taxes Versus Federal Taxes: The Geography of Relief

While federal legislation to eliminate Social Security taxes would provide massive relief, your geographic location also dictates your total tax burden. It is critical to differentiate between federal tax laws and state tax laws, as they operate independently.

Currently, the vast majority of states do not tax Social Security benefits at all. As of 2026, fewer than ten states still levy a state-level income tax on these benefits, and several of those are actively phasing the taxes out or offering generous age and income-based exemptions. States like Colorado, Connecticut, Minnesota, Montana, New Mexico, Rhode Island, Utah, Vermont, and West Virginia have specific rules dictating how much of your benefit is subject to state taxation.

If the federal government eliminates taxes on Social Security benefits, it does not automatically force states to follow suit, though it would remove the federal AGI baseline many states use to calculate local taxes. Regardless of state action, the bulk of the tax burden for retirees comes from the federal side. Eliminating the federal tax alone is the primary driver of the wealth retention illustrated in our earlier case studies.

The Macro Impact: Trust Fund Solvency and Future Trade-Offs

While the prospect of tax relief is undeniably appealing for individual retirees, it is essential to look at the broader economic picture. The taxation of Social Security benefits was not implemented simply to punish seniors; it was enacted to raise vital revenue for entitlement programs.

The revenue generated from taxing up to 50 percent of benefits is directed straight back into the Old-Age and Survivors Insurance (OASI) Trust Fund, which pays out monthly benefits. The revenue generated from the 85 percent tier is directed into the Medicare Hospital Insurance (HI) Trust Fund, which helps fund Medicare Part A. According to the Social Security Administration (SSA), the taxes collected on benefits provide tens of billions of dollars annually to these trust funds.

If Congress permanently cuts this revenue stream, they must find a way to replace the funding to prevent accelerated depletion of the trust funds. Potential trade-offs could include raising the full retirement age, increasing the payroll tax rate on current workers, raising the cap on wages subject to FICA taxes, or reducing overall benefits for future generations. As a strategic retiree, monitoring these legislative debates is crucial because relief in one area (income taxes) may eventually result in increased costs elsewhere (such as higher Medicare premiums).

Current Strategies to Minimize Social Security Taxes

You do not have to wait for Congress to pass new legislation to start protecting your retirement income. Under current tax laws, proactive planning can drastically reduce or eliminate the taxes you pay on your benefits. Implementing these strategies requires careful coordination, but the financial payoff is substantial.

- Executing Strategic Roth Conversions: Moving money from traditional tax-deferred IRAs to Roth IRAs before you claim Social Security is a powerful strategy. You pay taxes on the conversion amount upfront, but all future qualified withdrawals from the Roth IRA are tax-free. More importantly, Roth IRA withdrawals do not count toward your Combined Income, keeping your provisional income low and your Social Security benefits tax-free.

- Managing Withdrawal Sequencing: Carefully choosing which accounts to draw from each year gives you control over your taxable income. Tapping taxable brokerage accounts (where you only pay capital gains tax on the growth) or using cash reserves can help you supplement your Social Security without triggering the tax torpedo.

- Utilizing Qualified Charitable Distributions (QCDs): If you are over age 70½ and charitably inclined, you can transfer up to $105,000 per year directly from your traditional IRA to a qualified charity. This satisfies your Required Minimum Distribution (RMD) but keeps the withdrawn amount entirely off your tax return, thereby keeping your combined income lower.

- Delaying Your Social Security Claim: By delaying benefits until age 70, you guarantee a larger monthly payout. You can spend down your heavily taxed traditional IRA balances during your early retirement years (ages 60 to 70) while your income is relatively low. Once your IRA balances are reduced, your RMDs will be smaller later in life, resulting in lower combined income and fewer taxes on your maximized Social Security checks.

What Can Go Wrong

As discussions about eliminating taxes on Social Security gain political traction, the biggest risk to your financial security is acting on proposed legislation before it officially becomes law. Financial plans built on assumptions rather than current legal realities often collapse.

One major mistake is halting proactive tax planning—such as pausing Roth conversions—because you assume Social Security tax elimination is imminent. If the legislation stalls in Congress, you lose valuable years where you could have shifted assets into tax-free vehicles at lower brackets. Always plan for the tax code as it is written today, while maintaining the flexibility to adjust if the law changes.

Another risk involves misunderstanding gross versus net income. If tax relief is enacted, your monthly Social Security deposit will increase if you were previously having federal taxes withheld. Some retirees might immediately increase their fixed lifestyle expenses (buying a new car, taking on new debt) based on this higher cash flow. However, if the legislation includes sunset provisions or causes Medicare Part B premiums to rise to offset trust fund losses, that increased cash flow could evaporate quickly. Always maintain a margin of safety in your monthly budget.

When to Consult a Professional

Navigating the complex intersection of tax laws, Medicare surcharges, and Social Security requires meticulous planning. While self-education is critical, specific financial transitions warrant the oversight of a certified fiduciary.

Consider consulting a professional in these specific scenarios:

- Managing a Sudden Windfall: If you inherit money, sell a business, or sell highly appreciated real estate during retirement, the massive spike in taxable income will temporarily subject the maximum amount of your Social Security to taxes. A tax professional can help structure the sale or utilize tax-loss harvesting to mitigate the damage.

- Navigating State Relocation: Moving from a high-tax state to a state with no income tax involves strict domicile rules. If you plan to relocate to stretch your retirement income, a CPA can ensure you do not inadvertently trigger a dual-residency tax audit.

- Coordinating IRMAA Surcharges: If your income fluctuates, you face the risk of triggering Medicare Income-Related Monthly Adjustment Amount (IRMAA) surcharges. A Certified Financial Planner can project your income to prevent a small withdrawal from causing a massive spike in your Medicare Part B and Part D premiums.

Frequently Asked Questions

At what income level does Social Security become completely tax-free right now?

Under current law, your benefits are completely tax-free if your Combined Income (Adjusted Gross Income + nontaxable interest + half of your Social Security benefits) remains below $25,000 for single filers or below $32,000 for married couples filing jointly.

Do capital gains count toward the income limits that make Social Security taxable?

Yes. Realized capital gains are included in your Adjusted Gross Income. Therefore, selling stocks, mutual funds, or real estate at a profit increases your AGI, which drives up your combined income and can push your Social Security benefits into taxable territory.

If they end taxes on Social Security, will Medicare premiums go up?

It is a significant possibility. Because taxes collected on Social Security benefits help fund the Medicare Hospital Insurance Trust Fund, eliminating that revenue source without replacing it could pressure the government to offset the loss. This offset might come in the form of increased Medicare Part B or Part D premiums, though specific impacts depend entirely on the final legislation.

Will eliminating this tax save me money if my only income is Social Security?

No. If your sole source of income in retirement is Social Security, you already pay zero federal income tax on those benefits because your combined income falls well below the base threshold. Tax elimination primarily benefits middle-class and upper-class retirees who have supplementary income from pensions, wages, or retirement accounts.

The potential elimination of taxes on Social Security benefits represents one of the most significant proposed shifts in retirement planning in recent history. Retaining an extra few thousand dollars a year provides a vital buffer against inflation, rising medical expenses, and market volatility. While the political debates surrounding the legislation and the trust funds continue, your focus must remain on what you can control. By optimizing your current withdrawal strategies, managing your tax brackets, and staying informed on legislative developments, you position yourself to maximize every dollar you have earned.

This article provides general retirement education and information only. Every retiree’s situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: June 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply