Taking advantage of above-the-line tax breaks allows you to lower your adjusted gross income while still claiming the massive standard deduction available in 2026. The vast majority of retirees no longer itemize their taxes, but that does not mean you must leave valuable savings on the table. Adjustments to income reduce your tax bill dollar-for-dollar before the IRS even applies your standard deduction. By understanding how to strategically combine specific write-offs with your baseline deduction, you can preserve more of your retirement income. We explore exactly which expenses qualify for these unique benefits, how the rules apply to older adults, and the precise steps required to claim them on your next tax return.

Why the Standard Deduction Dominates in 2026

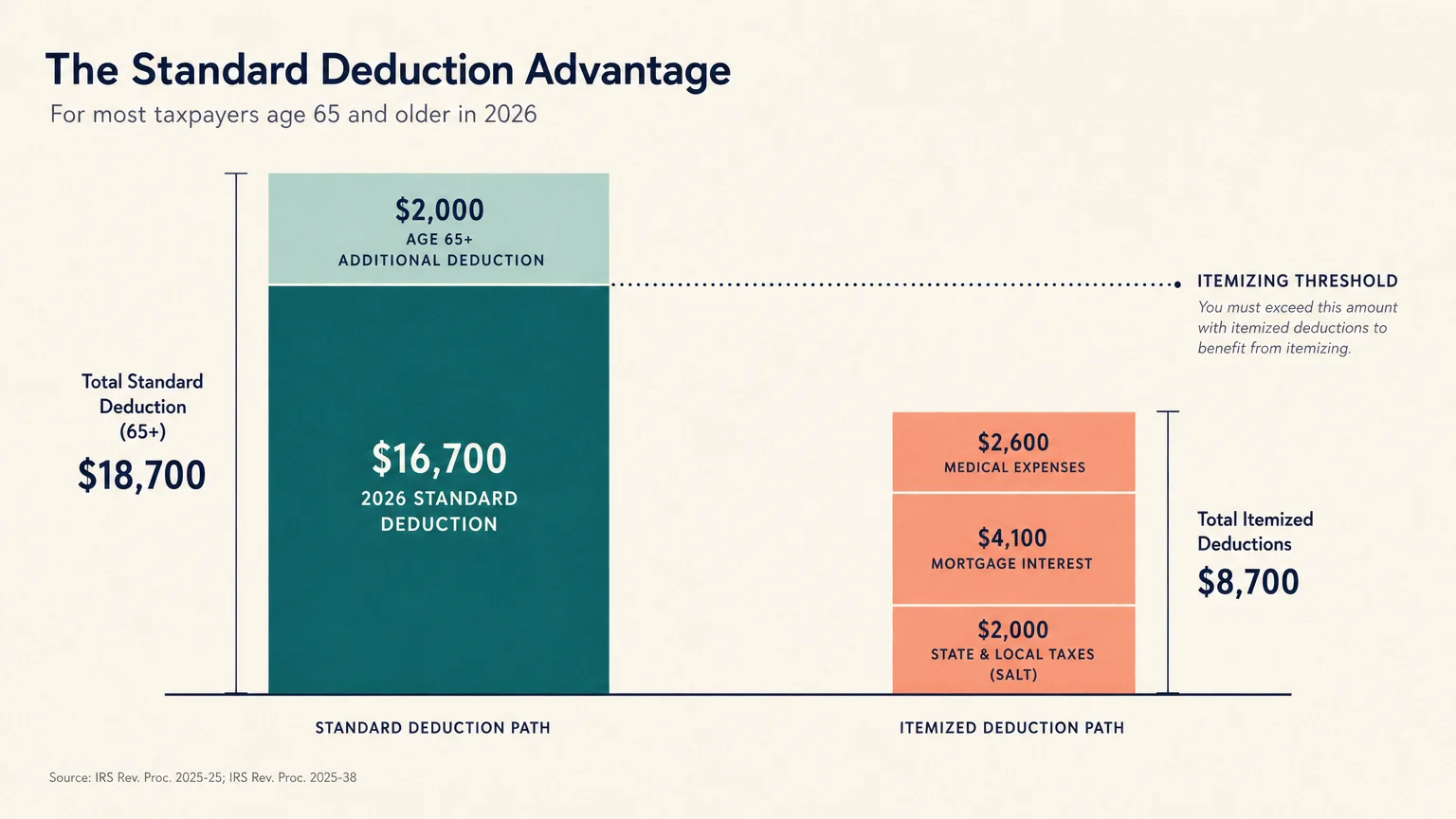

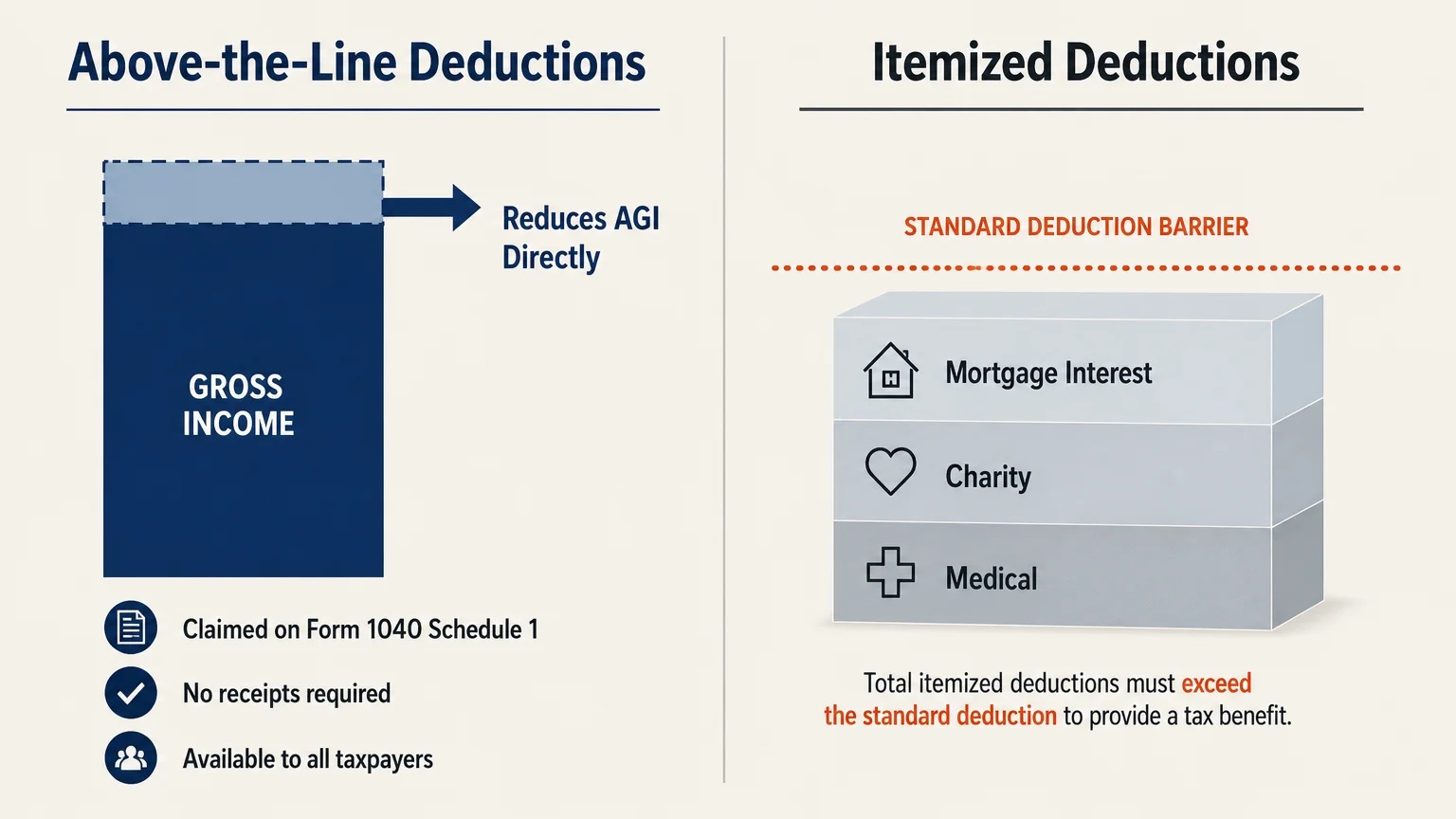

The tax landscape remains heavily tilted toward the standard deduction. Following major legislative overhauls in previous years, the internal revenue code essentially forced a choice: itemize individual expenses—like mortgage interest, state taxes, and medical bills—or take a flat, guaranteed deduction based on your filing status. For most retirees, the flat amount simply pays better.

By 2026, the standard deduction amounts provide a formidable shield against income taxes. A married couple filing jointly receives a baseline deduction that completely shelters tens of thousands of dollars from federal taxation. Furthermore, taxpayers aged 65 and older receive an additional standard deduction amount. If you and your spouse are both over 65, you get two additional bumps to your baseline deduction. Blind taxpayers receive yet another increase. When you add these up, the threshold to make itemizing worthwhile becomes nearly insurmountable for the average retired household.

This creates a distinct challenge. If you no longer itemize, you lose the traditional tax benefits of writing off charitable donations, high medical expenses, and property taxes. They disappear into the math of the standard deduction. This is exactly why “above-the-line” deductions—formally known as adjustments to income—are the most powerful tools in your tax-planning arsenal. You claim these specific write-offs directly on Schedule 1 of Form 1040. They shrink your Adjusted Gross Income (AGI) before the IRS even looks at your standard deduction. You get to stack your tax breaks, claiming both the specific adjustment and the full standard deduction.

1. Qualified Charitable Distributions (QCDs)

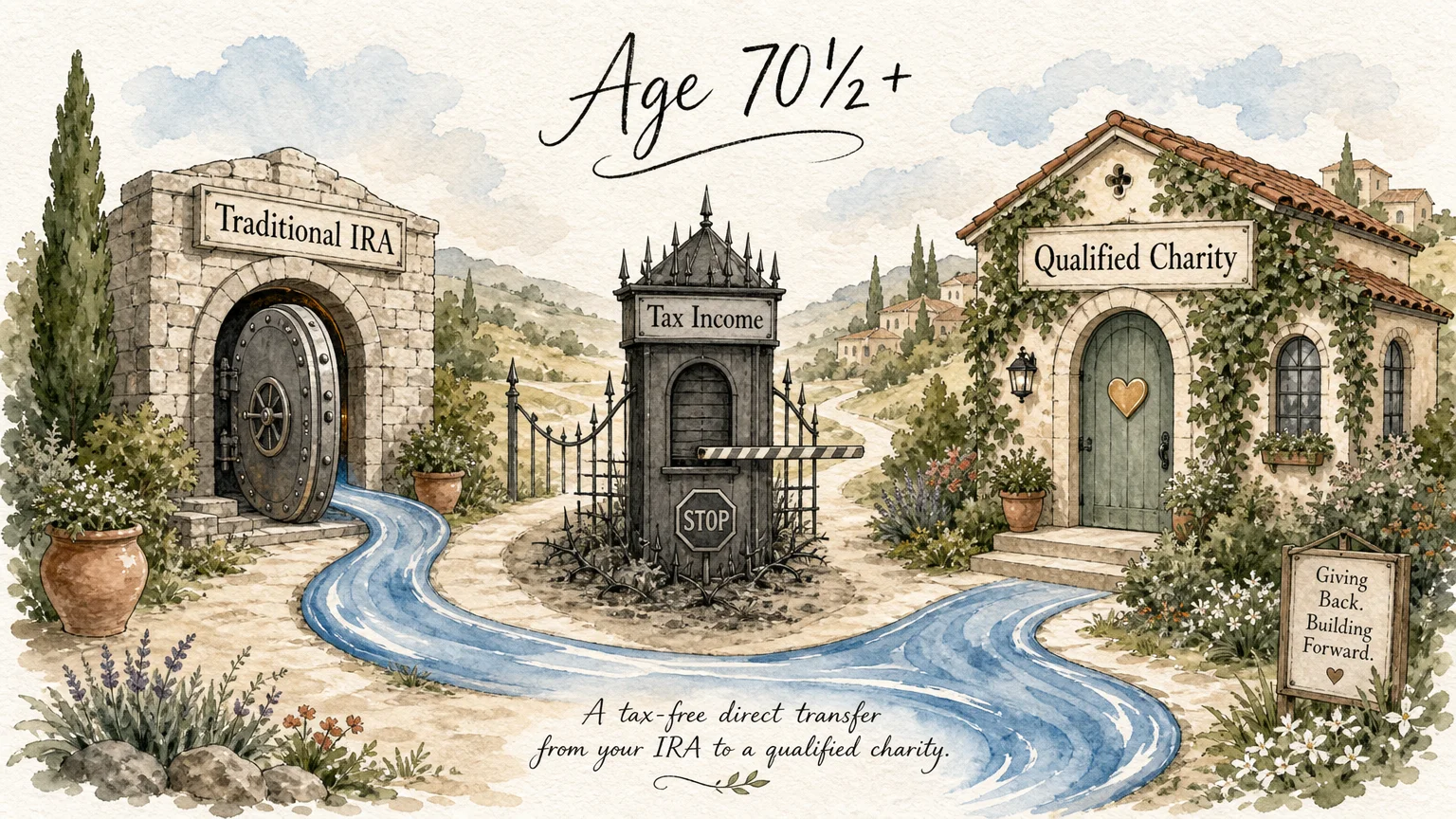

If you give money to charity and you have money in a Traditional IRA, writing a check from your personal bank account is highly inefficient. Because you take the standard deduction, that cash donation provides zero tax relief. Instead, the tax code offers a remarkably elegant solution: the Qualified Charitable Distribution, or QCD.

A QCD allows individuals who are age 70½ or older to transfer funds directly from their Individual Retirement Account to a qualified 501(c)(3) charity. The money you transfer is completely excluded from your taxable income. While this is not technically an “above-the-line deduction” in the traditional sense of Schedule 1, it functions exactly like the ultimate non-itemizer tax break. It lowers your gross income on the front page of your tax return while you simultaneously claim the full standard deduction.

The rules governing QCDs are strict but straightforward. The transfer must go directly from your IRA custodian to the charity; if you withdraw the money first and then write a personal check, the IRS treats the withdrawal as taxable income. You can transfer up to $105,000 per year using this method, a limit that is now indexed for inflation. If you are married and both spouses have their own IRAs, each of you can utilize the maximum limit.

The most profound benefit of a QCD occurs when you reach your Required Minimum Distribution (RMD) age. The IRS forces you to pull money out of your tax-deferred accounts, which artificially inflates your income. A QCD counts toward satisfying your annual RMD. By directing your required distribution to a charity, you fulfill your legal obligation to the IRS without adding a single dollar to your adjusted gross income. This maneuver keeps your taxable income artificially low, which can prevent you from sliding into a higher tax bracket.

2. Health Savings Account (HSA) Contributions

For retirees and pre-retirees navigating the gap years before Medicare, the Health Savings Account represents the most tax-advantaged vehicle in the federal tax code. An HSA offers a triple-tax advantage: your contributions are deductible above the line, the funds grow tax-free, and your withdrawals are completely tax-free when used for qualified medical expenses.

You can claim an HSA deduction without itemizing. Every dollar you deposit into your HSA lowers your AGI. To qualify to make a contribution in 2026, you must be enrolled in a High Deductible Health Plan (HDHP) and you cannot have any other disqualifying coverage. The IRS provides generous contribution limits, and if you are 55 or older, you can make an additional $1,000 catch-up contribution. For a married couple where both spouses are 55 or older, each spouse must have their own separate HSA to claim their respective catch-up contributions, though the primary family limit can be deposited into just one account.

You must navigate one massive trap regarding HSAs and aging: the Medicare enrollment rule. The very month you enroll in any part of Medicare—even premium-free Part A—you lose your eligibility to contribute to an HSA. You can still spend the money already inside the account tax-free for the rest of your life, but you cannot add new funds.

If you plan to delay claiming Social Security and Medicare past age 65 while continuing to work and use an employer HDHP, you can legally continue funding your HSA. However, when you finally do apply for Medicare Part A later, the government applies a six-month retroactive coverage rule. Your Part A coverage will be backdated up to six months (but no earlier than your 65th birthday). If you made HSA contributions during that retroactive window, the IRS considers them excess contributions subject to steep penalty taxes. You must proactively stop your HSA contributions six months prior to filing your Medicare application.

3. Traditional IRA Contributions

A persistent myth suggests that once you reach retirement age, you can no longer save money in a tax-advantaged retirement account. Recent legislation permanently eliminated the age restriction for Traditional IRA contributions. As long as you have earned income, you can contribute to a Traditional IRA and deduct the contribution directly from your income without itemizing.

The phrase “earned income” is the critical threshold. Earned income includes W-2 wages from a job, net earnings from self-employment, and consulting fees. It specifically excludes pensions, Social Security benefits, annuity payments, rental property income, and investment dividends. If you take a part-time job at a hardware store, do freelance consulting, or run a small Etsy business in retirement, that income qualifies you to make an IRA contribution.

For married couples where only one spouse continues to work, the tax code offers the Spousal IRA strategy. If you are fully retired but your spouse brings in W-2 wages, your spouse can contribute to their own IRA and use their remaining earned income to fund an IRA in your name. This effectively doubles the household’s above-the-line deduction power.

Keep in mind that if you or your spouse are covered by a retirement plan at work—such as a 401(k)—your ability to deduct a Traditional IRA contribution phases out at higher income levels. However, if neither of you has access to a workplace plan, you can deduct the full amount regardless of how high your income reaches.

4. Student Loan Interest Deductions

Many retirees are surprised to learn they can deduct student loan interest, assuming this tax break is reserved for recent college graduates. However, a growing demographic of older Americans carry student loan debt into retirement. You might be paying off your own delayed educational pursuits, or more commonly, you might have taken out Parent PLUS loans to help finance a child’s or grandchild’s university education.

The IRS permits you to deduct up to $2,500 of interest paid on a qualified student loan during the year. This is an above-the-line adjustment, completely independent of the standard deduction. To claim this break, you must meet a few rigid criteria. You must be legally obligated to pay the loan. If the loan is strictly in your grandchild’s name and you simply write the check each month as a gift, you cannot claim the deduction. The loan must bear your name as the primary borrower or a legally bound co-signer.

Furthermore, you cannot be claimed as a dependent on someone else’s tax return, and your filing status cannot be married filing separately. The deduction is subject to Modified Adjusted Gross Income (MAGI) phase-outs. If your retirement income pushes you above the IRS threshold, the allowable deduction slowly reduces to zero. You will receive Form 1098-E from your loan servicer documenting exactly how much interest you paid during the year; this form serves as your official record when entering the deduction on Schedule 1.

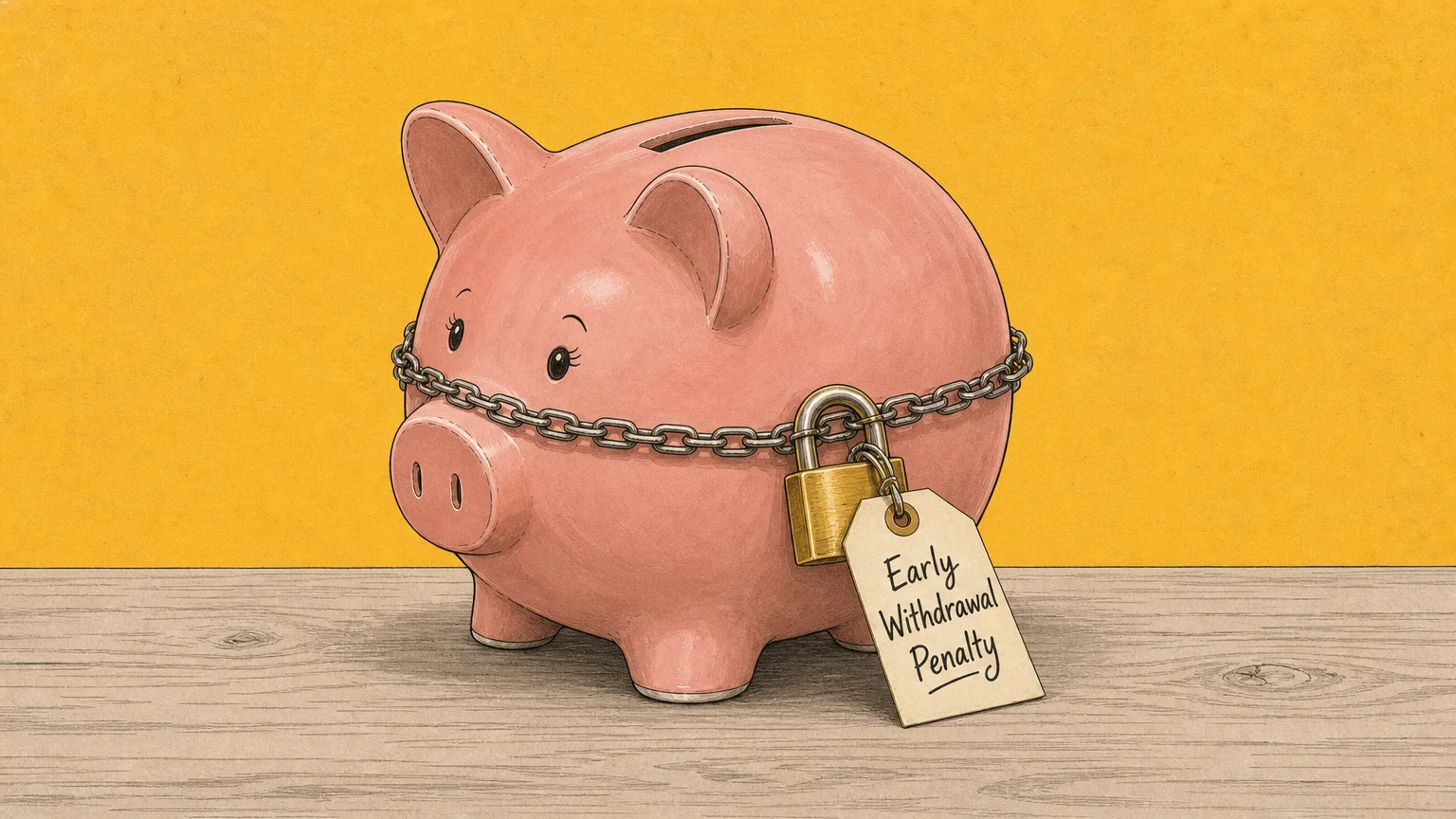

5. Penalty on Early Withdrawal of Savings

Retirees rely heavily on Certificates of Deposit (CDs) to generate safe, predictable yield. Banks offer higher interest rates on CDs in exchange for your promise to lock the money away for a specific term—anywhere from three months to five years. If an unexpected expense arises—such as an emergency roof repair or a sudden medical bill—you might be forced to break the CD before maturity. When you do, the bank charges an early withdrawal penalty, often equivalent to several months of interest.

The IRS softens this blow by allowing you to deduct the entire penalty amount. This is an explicit above-the-line deduction. You do not need to itemize, and there is no cap on the penalty amount you can deduct. You can deduct the penalty even if it exceeds the amount of interest you actually earned on the CD during the tax year.

At tax time, your bank will send you Form 1099-INT. Box 2 of this form explicitly lists the “Early withdrawal penalty.” You simply take this exact figure and enter it into the appropriate line on Schedule 1 of your Form 1040. This lowers your AGI precisely by the amount you were penalized, ensuring you do not pay income tax on interest you technically had to forfeit back to the bank.

The Cascading Benefits of Lowering Your AGI

Why does lowering your Adjusted Gross Income matter so much when your standard deduction already wipes out your tax liability? Because your AGI acts as the gatekeeper for nearly every other financial calculation in retirement. The IRS and the Social Security Administration do not look at your final taxable income when determining your benefits; they look at your AGI (or variations of it).

First, consider the taxation of your Social Security benefits. The IRS determines how much of your Social Security is taxable using a formula called “Provisional Income.” Provisional Income equals your AGI, plus non-taxable interest, plus half of your Social Security benefits. If this formula produces a number above certain thresholds, up to 85% of your benefits become taxable. Every dollar you claim through an above-the-line deduction lowers your AGI, which in turn lowers your Provisional Income, potentially rescuing your Social Security checks from taxation.

Second, consider Medicare Part B and Part D premiums. The government utilizes a system called the Income-Related Monthly Adjustment Amount (IRMAA). If your Modified Adjusted Gross Income crosses specific, rigid thresholds, you are hit with a surcharge on your monthly Medicare premiums. These thresholds operate as cliffs—earning just one dollar over the limit triggers the full surcharge for the entire year. Strategic use of HSA contributions, Traditional IRA contributions, or QCDs can suppress your income just enough to keep you under the IRMAA cliffs, saving you thousands of dollars in Medicare premiums.

“In this world nothing can be said to be certain, except death and taxes.” — Benjamin Franklin

Comparing Deductions: Above-the-Line vs. Itemized

Understanding the mechanical differences between these deductions is crucial for tax planning. Here is how above-the-line adjustments compare to the itemized deductions you likely left behind.

| Feature | Above-the-Line Deductions (Schedule 1) | Itemized Deductions (Schedule A) | Qualified Charitable Distributions (QCD) |

|---|---|---|---|

| Requires giving up Standard Deduction? | No. You claim these in addition to the standard deduction. | Yes. You must forfeit the standard deduction to claim these. | No. Bypasses income entirely. |

| Reduces Adjusted Gross Income (AGI)? | Yes. Lowers your AGI dollar-for-dollar. | No. Only reduces Taxable Income, not AGI. | Yes. Keeps the distribution completely out of AGI. |

| Impact on Medicare IRMAA? | Can help lower Medicare premiums by suppressing AGI. | Zero impact. Does not affect IRMAA calculations. | Highly effective at preventing IRMAA surcharges. |

| Common Examples | HSA, IRA contributions, CD penalties, Student Loan Interest. | Medical bills, State/Local Taxes (SALT), Mortgage Interest. | Direct transfers from an IRA to a 501(c)(3) charity. |

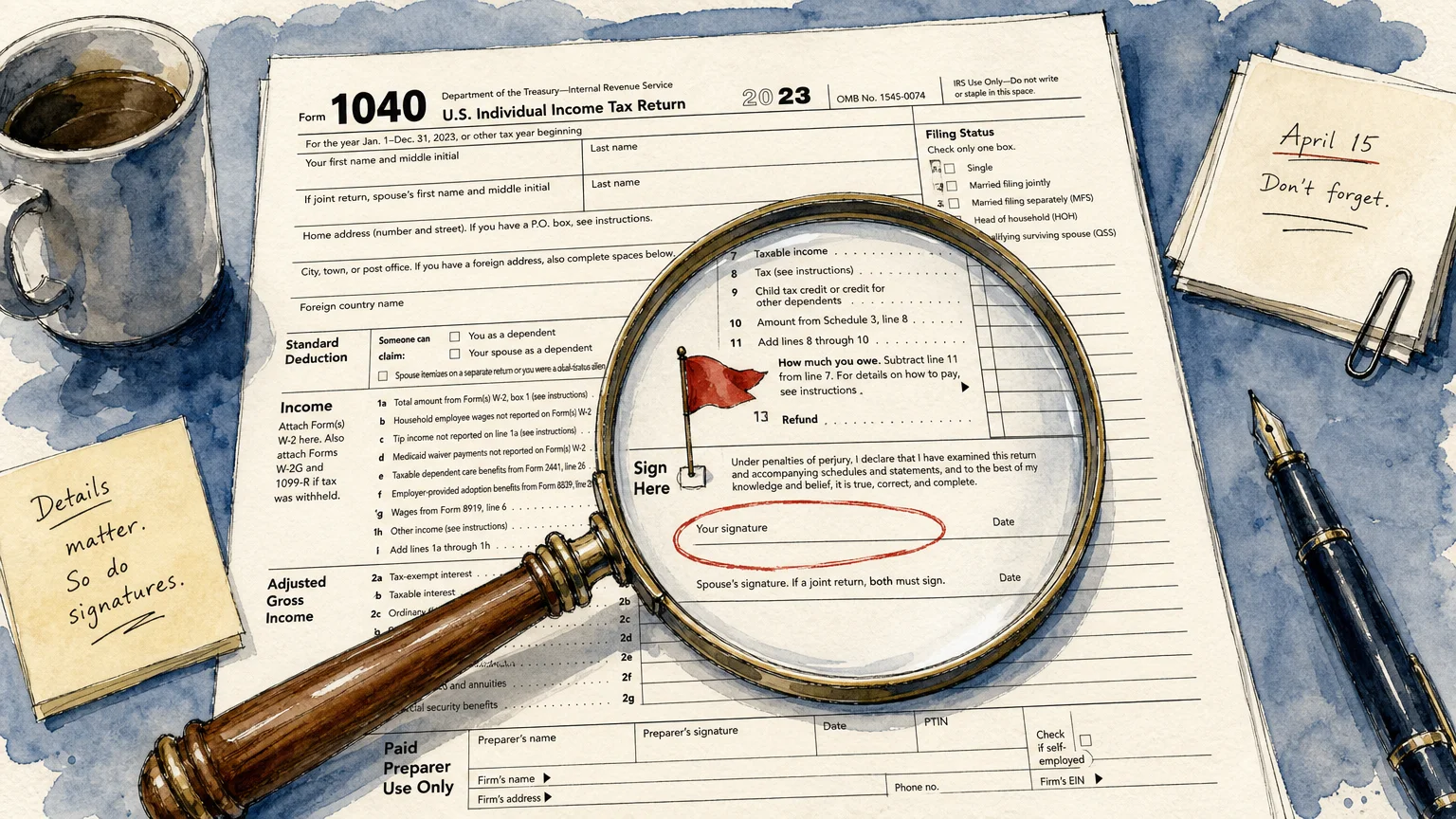

What Can Go Wrong: Common IRS Mistakes

Attempting to claim these tax breaks without understanding the nuances can trigger IRS correspondence audits or unexpected tax liabilities. You must actively manage the paperwork, as financial institutions often leave the final reporting responsibilities entirely up to you.

Failing to report QCDs correctly: This is the most prevalent error retirees make. When you execute a Qualified Charitable Distribution, your IRA custodian will send you a Form 1099-R at the end of the year. The custodian does not mark this form to indicate the money went to charity; the distribution looks exactly like a normal, taxable withdrawal. It is entirely your responsibility to report the total distribution on Line 4a of your Form 1040, but write “0” on Line 4b (the taxable amount) and physically write “QCD” next to the line. If you forget to tell your tax software or CPA that the withdrawal was a QCD, you will pay taxes on the money you gave away.

Tripping over the HSA Medicare trap: As mentioned earlier, funding an HSA while enrolled in Medicare creates an excess contribution nightmare. The IRS assesses a 6% excise tax penalty on the excess funds for every year they remain in the account. Fixing this requires withdrawing the excess funds and the earnings associated with them, which then becomes taxable income.

Confusing active vs. passive income for IRAs: You cannot fund a Traditional IRA using investment dividends or Social Security. If you make a $7,000 contribution to an IRA but your only income for the year came from a pension and an annuity, the IRS will flag the contribution as invalid. You must have verifiable, taxable earned income to back up the deposit.

When to Consult a Tax Professional

While the standard deduction simplifies tax filing for millions, optimizing your remaining tax breaks requires precision. There are specific scenarios where attempting to self-prepare your taxes can cost you thousands of dollars in missed opportunities or penalties.

- Managing the IRMAA Cliffs: If your projected income is within a few thousand dollars of an IRMAA tier, a Certified Public Accountant (CPA) or Enrolled Agent (EA) can help you aggressively deploy above-the-line deductions to sneak under the threshold. The math required to project Provisional Income and MAGI simultaneously is complex.

- Coordinating RMDs and QCDs: The IRS “first money out” rule dictates that the very first dollars withdrawn from your IRA in a given year count toward your RMD. If you take your RMD in January to pay for living expenses, and then try to do a QCD in December, the QCD will not offset the RMD you already took. A professional will sequence your withdrawals to ensure maximum tax efficiency.

- Handling Inherited IRAs: If you inherited a retirement account under the new 10-year depletion rules, the sudden influx of forced distributions will violently disrupt your tax brackets. You need professional guidance to offset that income using HSAs, specific write-offs, and strategic withdrawal timing.

You can verify current IRS tax forms and publications directly through official federal resources to ensure you are looking at the exact guidelines for the current tax year.

Frequently Asked Questions

Can I deduct medical expenses without itemizing my taxes?

No, traditional out-of-pocket medical expenses can only be written off if you itemize using Schedule A, and only the portion that exceeds 7.5% of your AGI is deductible. However, if you have a Health Savings Account, you essentially achieve the same goal. You take an above-the-line deduction when you put money into the HSA, and then use that tax-free money to pay the medical bills.

Does my standard deduction automatically increase when I retire?

The standard deduction does not increase simply because you retire; it increases when you reach age 65. The IRS grants an “additional standard deduction” to taxpayers age 65 or older. If you retire early at age 60, you will claim the normal standard deduction until the year you turn 65.

Can I claim the student loan interest deduction if I pay my child’s loan directly?

You cannot claim the deduction if your child is the only legally obligated borrower on the loan note, even if you are the one transferring money from your bank account to the servicer. To claim the above-the-line deduction, you must be the primary borrower or a legally bound co-signer on the debt instrument itself.

If I use a QCD, do I still get a charitable deduction receipt?

You must still obtain a standard acknowledgment letter from the charity stating the amount received and that no goods or services were provided in exchange for the donation. While you do not attach this letter to your tax return, you must keep it in your files to prove the transfer was a legitimate qualified distribution if the IRS ever questions the transaction.

Optimizing your tax footprint in retirement requires shifting your perspective. Instead of hunting for receipts to itemize, focus relentlessly on lowering your Adjusted Gross Income. By leveraging QCDs, funding healthcare accounts strategically, and claiming the specific adjustments you are entitled to, you protect your wealth from unnecessary taxation. Review your current financial setup, identify which of these five mechanisms align with your life, and take action before the tax year ends.

This is educational content based on general retirement and financial principles. Individual results vary based on your situation. Always verify current benefit rules, tax laws, and eligibility requirements with official sources like SSA, Medicare.gov, or the IRS.

Last updated: March 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply