Deciding when to claim Social Security and Medicare benefits ranks among the most consequential financial choices you will ever make. Nailing your benefit timing secures thousands of dollars in additional lifetime income and protects your lifestyle against inflation. Many pre-retirees mistakenly assume that claiming benefits upon reaching their minimum retirement age is the safest path; however, this rush often locks them into permanently reduced monthly checks. Because these foundational retirement decisions are largely irrevocable, understanding how your filing age interacts with spousal benefits, taxation, and your overall portfolio is crucial before submitting any paperwork. Taking the time to master these nuanced rules ensures your Social Security income provides maximum stability for the decades ahead.

Understanding Your Full Retirement Age

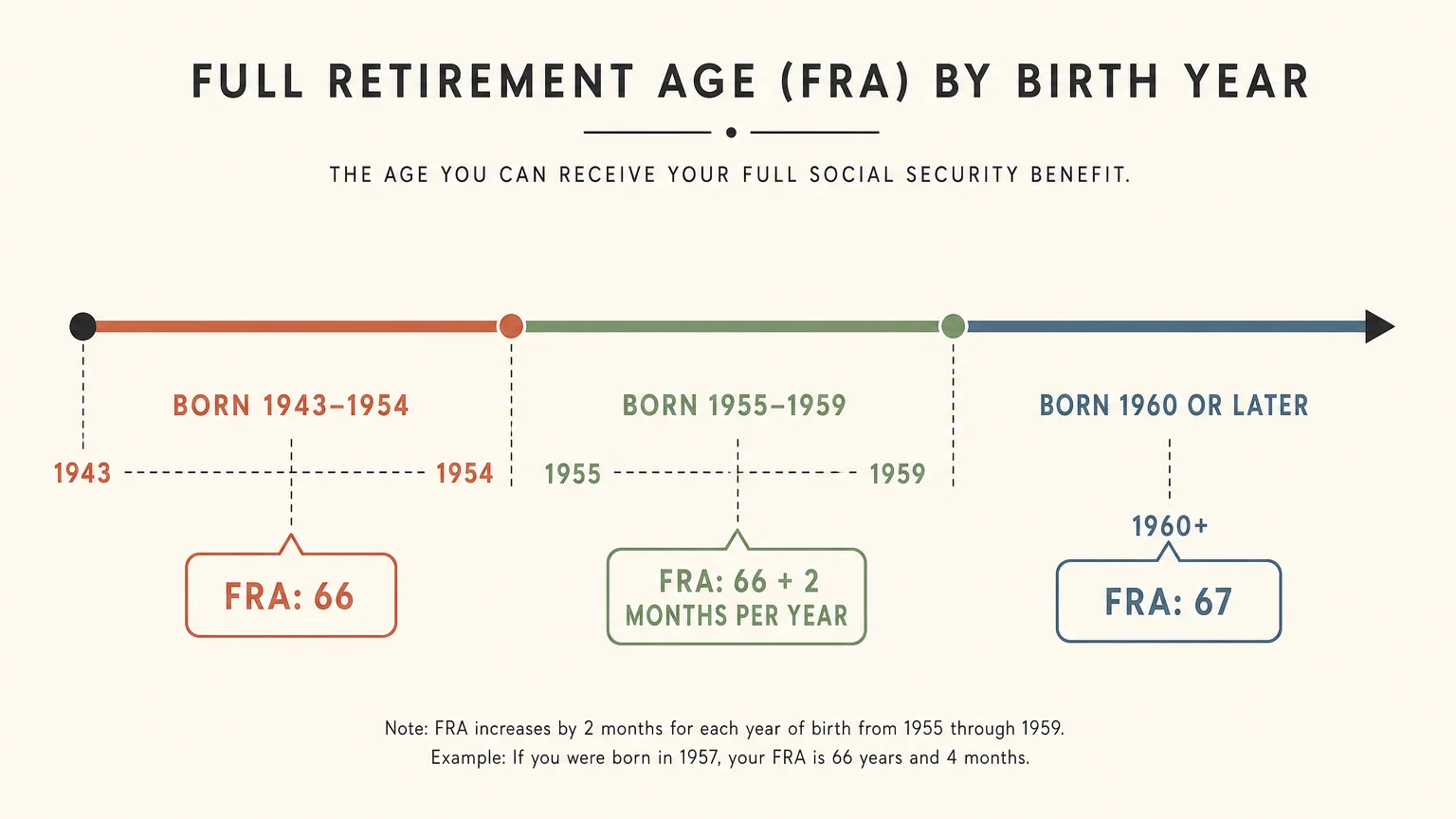

Before you evaluate any claiming strategies, you must identify your Full Retirement Age (FRA). The government designates this specific age as the point when you become eligible to receive 100 percent of your earned primary insurance amount, without any reductions for early filing. While past generations consistently aimed for age 65 as their finish line, legislative changes over the past few decades have shifted the goalposts to account for longer life expectancies.

If you were born between 1943 and 1954, your FRA is 66. For anyone born between 1955 and 1959, the FRA increases by two months for each sequential birth year. Anyone born in 1960 or later faces a Full Retirement Age of 67. Memorizing your specific FRA acts as the baseline for all subsequent retirement decisions—every mathematical calculation the Social Security Administration performs regarding your monthly check hinges on this exact date.

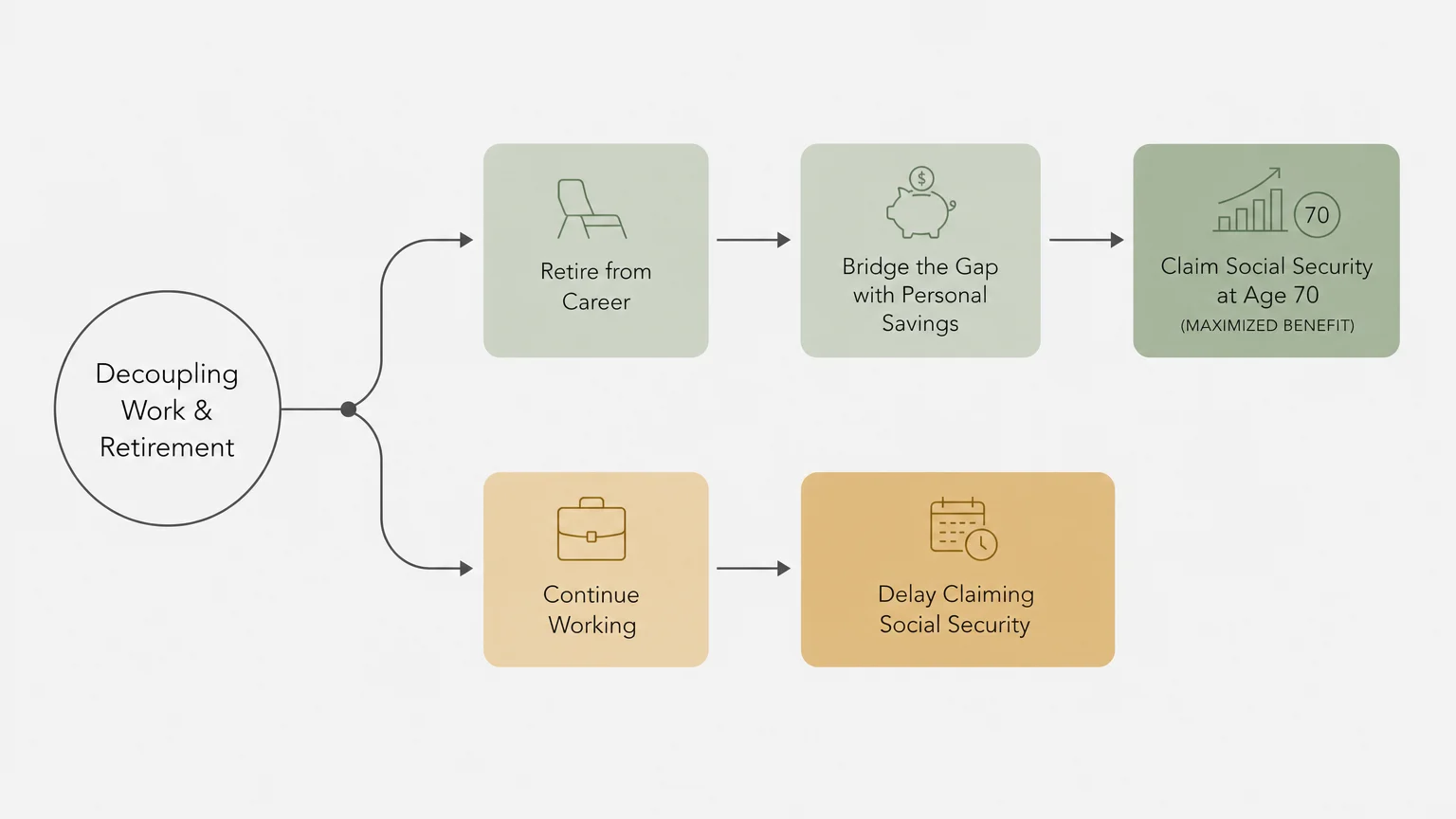

Filing before your FRA introduces permanent reductions to your benefits, while delaying past your FRA generates guaranteed increases. Many people blur the lines between stopping work and filing for benefits, assuming the two events must happen simultaneously. You possess the freedom to retire from your career at 62 while utilizing other savings to bridge the gap until you claim your benefits at FRA or later. Separating your work timeline from your benefit timeline grants you immense flexibility in designing a resilient retirement plan.

How Benefit Timing Impacts Your Monthly Check

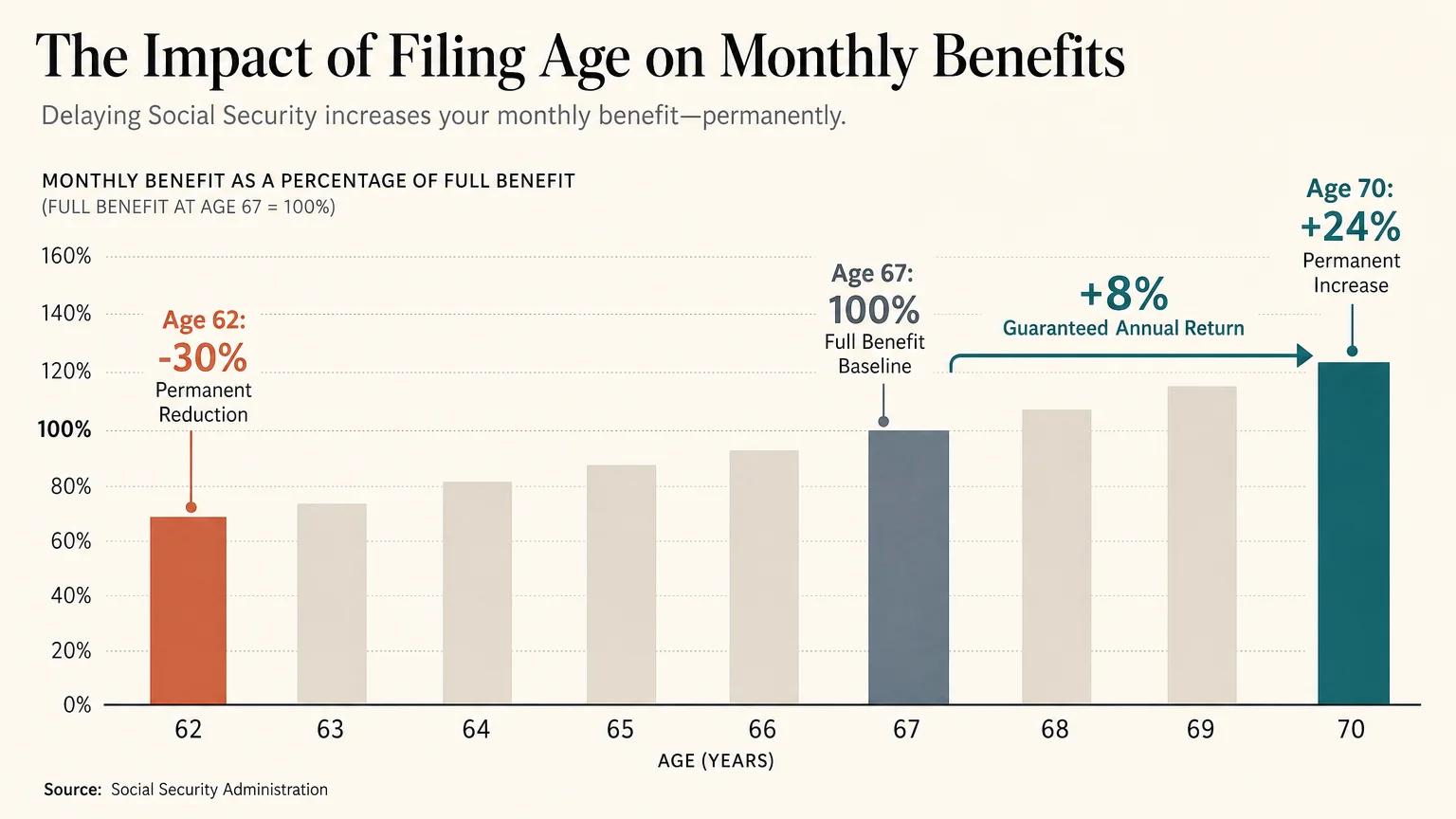

The age at which you initiate your claim dictates the size of your monthly deposit for the rest of your life. The earliest you can claim your retirement benefits is age 62, but doing so triggers a severe, permanent reduction. If your FRA is 67 and you file at 62, your monthly check drops by 30 percent. This penalty persists throughout your entire retirement—it does not reset when you eventually reach your FRA.

Conversely, the system rewards patience. For every month you delay filing beyond your FRA, you earn delayed retirement credits. These credits increase your eventual benefit by 8 percent per year, culminating at age 70. Waiting from age 67 to age 70 enhances your base benefit by 24 percent, permanently elevating your monthly income.

“Delaying Social Security is the best investment you can make, as it guarantees an eight percent return for every year you wait past your full retirement age until age 70.” — Suze Orman, Personal Finance Expert

Beyond the baseline numbers, delaying your claim supercharges your protection against inflation. The annual Cost of Living Adjustments (COLAs) are calculated as a percentage of your current benefit. Earning an 8 percent increase on a larger baseline check at age 70 yields substantially more actual dollars than applying that same percentage to a reduced benefit claimed at age 62. For retirees deeply concerned about outliving their resources or losing purchasing power late in life, delaying acts as premium longevity insurance.

| Claiming Age | Percentage of Base Benefit (Assuming FRA of 67) | Strategic Fit |

|---|---|---|

| Age 62 | 70% | Best for individuals facing severe health issues or enduring immediate, unresolvable financial needs. |

| Age 67 (FRA) | 100% | Ideal for those who have stopped working and require baseline income without incurring permanent penalties. |

| Age 70 | 124% | Optimal for retirees expecting long lifespans who want maximum lifetime inflation protection and higher survivor benefits. |

Navigating Spousal and Survivor Benefits

Marriage introduces complex layers to the claiming process. Spousal benefits allow a lower-earning spouse to claim up to 50 percent of the higher-earning spouse’s primary insurance amount, provided the lower-earning spouse files at their own FRA. If the lower earner files early, that 50 percent maximum is permanently reduced. Importantly, the rules require you to file for your own worker benefit first; the system then automatically tops up your payment if your spousal entitlement proves higher. You can no longer pick and choose which benefit to claim while allowing the other to grow.

Survivor benefits demand even more strategic foresight. When one spouse passes away, the surviving spouse inherits the single largest monthly check between the two partners, while the smaller check disappears. Because of this rule, the primary earner in a household carries a profound responsibility regarding benefit timing. By delaying their claim until age 70, the higher earner maximizes their own monthly income and completely locks in a larger survivor benefit for their widow or widower. Rushing to claim the primary earner’s benefit at age 62 permanently cripples the financial safety net left behind for the surviving spouse.

Divorced individuals also maintain access to these marital benefits, provided their marriage lasted at least ten consecutive years and they remain currently unmarried. An ex-spouse can claim benefits based on their former partner’s earnings record without requiring their permission, notifying them, or reducing the amount the ex-spouse or their new family receives. Exploring these divorce stipulations carefully can unearth substantial income streams that retirees frequently overlook.

The Interplay Between Working and Claiming Benefits

Many Americans prefer to transition smoothly into retirement by working part-time or consulting. If you choose to claim benefits before reaching your FRA while simultaneously earning a paycheck, you run headfirst into the Retirement Earnings Test (RET). This mechanism temporarily withholds a portion of your Social Security income if your wages exceed specific annual limits.

If you fall beneath your FRA for the entire year, the government withholds one dollar in benefits for every two dollars you earn above the annual limit. In the specific year you reach your FRA, the penalty drops to one dollar withheld for every three dollars earned above a significantly higher limit, counting only the months prior to your birth month. Once you attain your exact FRA, the earnings test vanishes completely, allowing you to earn an unlimited salary while receiving your full monthly benefit.

A widespread misconception states that benefits withheld by the earnings test are confiscated and lost forever. In reality, the government temporarily suspends these funds. Once you reach your FRA, the system recalculates your monthly payout, crediting you for the months you did not receive a check. This adjustment permanently increases your future monthly payments, eventually returning the withheld funds over your projected lifetime. Despite this restorative mechanism, triggering the earnings test often causes immediate cash flow disruptions that require careful budget adjustments.

Tax Implications of Social Security Income

Generating Social Security income rarely occurs in a tax-free vacuum. Depending on your overall financial picture, up to 85 percent of your benefits could be subject to federal income taxation. To determine your exposure, the Internal Revenue Service uses a specific formula known as “combined income” or provisional income. You calculate this figure by adding your Adjusted Gross Income (AGI), any nontaxable interest you receive, and exactly 50 percent of your annual Social Security benefits.

If you file your taxes as an individual and your combined income falls between $25,000 and $34,000, up to 50 percent of your benefits may be taxed. If your combined income breaches the $34,000 threshold, up to 85 percent of your benefits become taxable. For married couples filing jointly, the initial threshold sits at $32,000, jumping to the 85 percent taxation tier once combined income crosses $44,000. These thresholds are not indexed for inflation, meaning standard cost-of-living increases routinely push more retirees into higher taxation brackets each year.

Understanding these tax cliffs allows you to maneuver your retirement accounts strategically. Pulling heavy distributions from a traditional IRA or 401(k) inflates your Adjusted Gross Income, which in turn subjects more of your Social Security benefits to federal taxes. Conversely, drawing from a Roth IRA or a standard savings account does not increase your AGI. By carefully sequencing which accounts you tap into each year, you can actively manage your combined income and shield your benefits from unnecessary taxation.

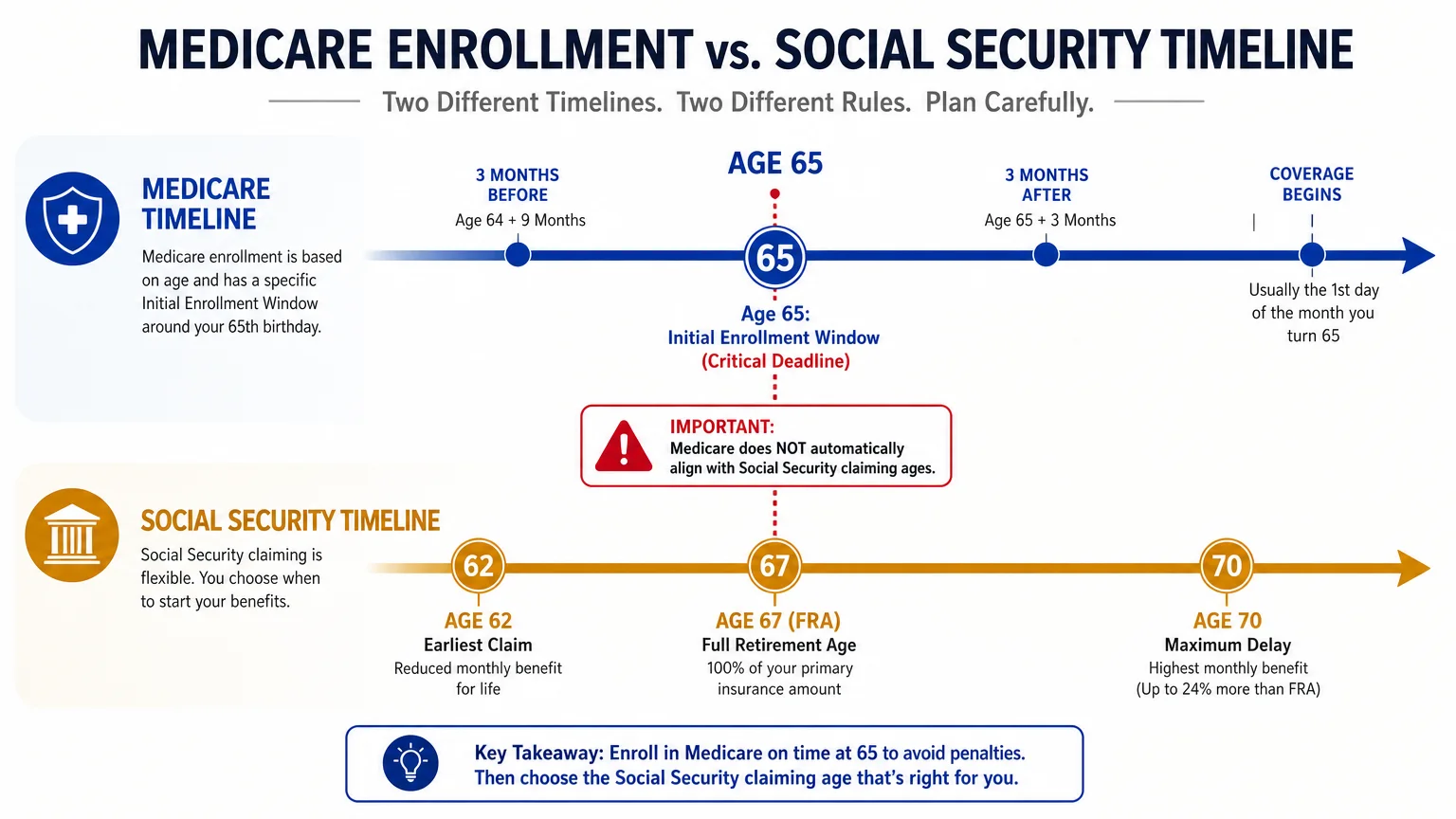

Medicare Enrollment: A Separate but Critical Timeline

While Social Security grants you the flexibility to claim anywhere between age 62 and 70, Medicare demands strict adherence to a much tighter timeline. Your Medicare Initial Enrollment Period (IEP) spans exactly seven months—it includes the three months prior to your 65th birthday, your birth month, and the three months immediately following. Failing to navigate this window correctly exposes you to lifelong financial penalties and dangerous gaps in your healthcare coverage.

If you already receive Social Security benefits when you turn 65, the government automatically enrolls you in Medicare Part A (hospital insurance) and Part B (medical insurance). However, if you are delaying your income benefits, you must proactively apply for Medicare through the Medicare.gov portal. Missing your initial window for Part B triggers a late enrollment penalty of 10 percent for every full 12-month period you could have had Part B but declined it. This penalty attaches to your monthly premium for the rest of your life.

The only valid reason to delay Medicare Part B without incurring penalties is if you or your spouse actively work for an employer with 20 or more employees and you maintain creditable group health coverage through that job. Retiree health plans, COBRA coverage, and veteran benefits do not qualify as creditable coverage for delaying Part B. Confusing these definitions frequently leads intelligent retirees into permanent premium penalties.

Additionally, high-income retirees must prepare for the Income-Related Monthly Adjustment Amount (IRMAA). If your Modified Adjusted Gross Income from two years prior exceeds specific thresholds, the government tacks a substantial surcharge onto your Part B and Part D premiums. Managing your taxable income in your early sixties is vital, as an unexpected spike in income—such as selling a property or executing a large Roth conversion at age 63—directly impacts what you pay for Medicare at age 65.

Pitfalls to Watch For

Navigating the transition into retirement requires vigilance. Even well-prepared individuals routinely stumble into easily avoidable traps when claiming their benefits. Keep these common missteps firmly on your radar to protect your long-term security.

- Claiming Early Out of Fear: Headlines constantly warn of impending trust fund depletion, prompting pre-retirees to claim at 62 simply to grab what they can. Even in the worst-case scenario where Congress takes absolutely no legislative action by the mid-2030s, ongoing tax revenues would still cover the vast majority of promised benefits. Slashing your lifetime baseline by 30 percent out of panic rarely serves your financial best interests.

- Ignoring State Taxation: While federal tax rules apply uniformly, state laws vary wildly. A minority of states continue to tax Social Security benefits at the local level. Failing to account for these state-specific reductions can leave you with a monthly shortfall that disrupts your budget.

- Neglecting Spousal Coordination: Married couples often view their benefits in isolation, failing to map out a joint strategy. When both spouses rush to claim early, they unnecessarily suppress the survivor benefit. Coordinating your claiming dates ensures the surviving partner will eventually inherit the highest possible monthly payment.

- Treating Medicare and Social Security as a Single Event: Assuming that delaying your income stream means you should also delay your healthcare coverage leads directly to massive Part B penalties. These are entirely separate systems governed by distinct rules and rigid deadlines.

Getting Expert Help

Given the permanence of these decisions, relying on guesswork or neighborly advice carries too much risk. Certain scenarios dramatically increase the complexity of your retirement outlook and strongly warrant professional intervention.

First, if you control a sizable portfolio of taxable, tax-deferred, and tax-free accounts, a professional can design a withdrawal sequence that minimizes taxes on your benefits while keeping you under the costly IRMAA thresholds for Medicare. Second, business owners navigating an exit strategy need guidance to avoid tripping the Retirement Earnings Test during their transition years. Third, widows, widowers, and divorced individuals must untangle a highly nuanced web of eligibility rules to ensure they are capturing every dollar they rightfully deserve.

When seeking assistance, look for professionals operating as fiduciaries, meaning they are legally bound to put your interests ahead of their own. Consulting the Certified Financial Planner Board provides a reliable starting point to locate vetted, fee-only advisors who specialize in holistic retirement income planning.

Frequently Asked Questions

Can I change my mind after claiming Social Security?

Yes, but you have a very narrow window. You are allowed one lifetime opportunity to withdraw your application, provided you do so within 12 months of your initial claim. To execute this reversal, you must repay every dollar you and your family received based on your record. Once repaid, your record resets, allowing your benefits to grow again as if you had never filed.

Do I have to claim Medicare and Social Security at the same time?

No, you do not. This is a crucial distinction. You can file for Medicare at 65 while delaying your income benefits until 70. Conversely, you can claim your income benefits at 62 and wait until you turn 65 to enter the Medicare system. Managing these timelines independently gives you the greatest leverage over your finances.

Will my benefits stop completely if the trust fund runs dry?

No. The program operates primarily as a pay-as-you-go system, meaning current workers continuously fund the benefits of current retirees through payroll taxes. Even if the dedicated trust fund depletes entirely, ongoing tax collection would be sufficient to pay the majority of promised benefits. Congress also possesses numerous legislative tools—such as adjusting the FRA or increasing the payroll tax cap—to shore up the system long before any automatic reductions would occur.

Stepping into retirement requires shifting your mindset from wealth accumulation to precise income distribution. The choices you make regarding your claiming ages cast a long shadow over your golden years. By taking the time to understand your Full Retirement Age, coordinating carefully with your spouse, respecting the rigid Medicare deadlines, and analyzing the associated tax impacts, you build a resilient foundation. Empower yourself with this knowledge, weigh your options patiently, and step into this next chapter of life with absolute confidence.

Last updated: June 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources. The information in this guide is meant for educational purposes. Your specific circumstances—including income, health needs, tax situation, and goals—may require different approaches. When in doubt, consult a licensed professional.

Leave a Reply