How the Earnings Limit Impacts Your Monthly Check

To grasp the real-world impact of these Social Security rules, you need to see the math in action. The withholding process does not simply reduce your monthly check by a few dollars. Instead, the SSA halts your payments entirely until they recover the amount you owe. They withhold whole checks, starting in January, until the penalty is satisfied.

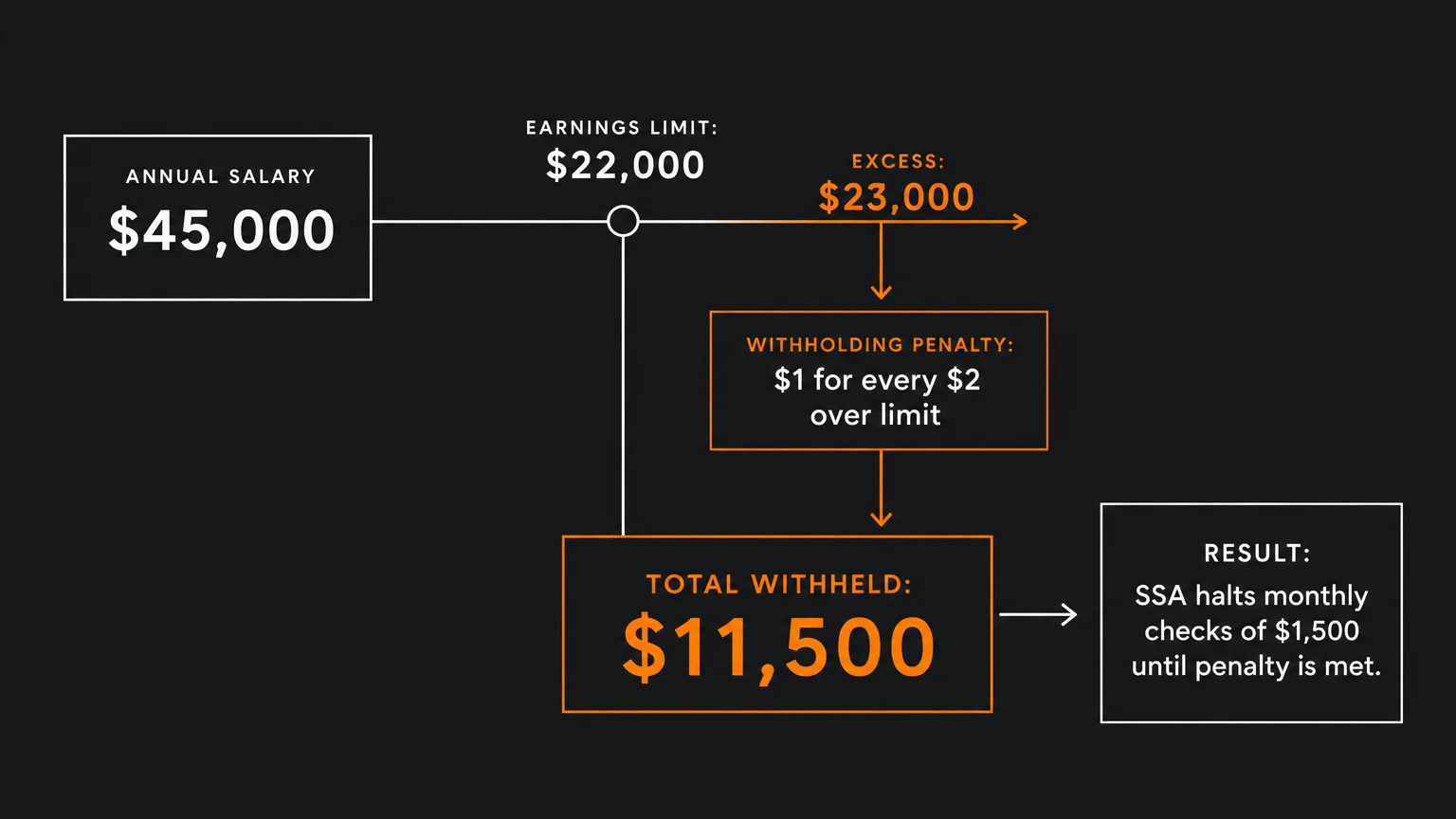

Consider a practical example. Suppose your Full Retirement Age is 67, but you claim benefits at age 63 to supplement your income. Your monthly benefit amount is $1,500, giving you an expected $18,000 per year. However, you continue working and earn $45,000 a year from your employer. Assuming the annual earnings limit is roughly $22,000, you are $23,000 over the limit.

Because the rule mandates withholding one dollar for every two dollars over the limit, the SSA must withhold $11,500 of your benefits. They accomplish this by stopping your checks completely for the first eight months of the year ($1,500 x 8 = $12,000).

You will receive zero Social Security income from January through August. In September, they will pay you the remaining $500 difference, and then you will finally receive your standard $1,500 checks in October, November, and December. Many retirees unknowingly trigger this scenario and face a terrifying cash flow drought for the first three-quarters of the year.

It is critical to distinguish between earned income and passive income. The earnings test only looks at wages from an employer (W-2 income) and net earnings from self-employment. The government does not count the following toward the limit:

- Distributions from traditional IRAs or 401(k) accounts

- Pension payments and annuities

- Capital gains, dividends, and interest from investments

- Rental property income (unless you are in the business of real estate)

- Inheritances or lottery winnings

Leave a Reply