Your Social Security payment schedule dictates your monthly household budget, and missing a deposit date can create unnecessary financial stress. The Social Security Administration relies on a strict calendar to disburse benefits to more than 70 million Americans, but weekend shifts, federal holidays, and specific benefit types frequently alter when your money actually arrives.

Understanding how these timing rules work—especially when holiday shifts create double-payment months or push deposits forward—protects you from bounced checks and delayed bill payments.

This guide breaks down the precise rules governing your deposit dates, how to navigate recent security updates to your online portal, and the exact steps you need to take if a payment fails to arrive on time.

How the Social Security Administration Sets Your Payment Date

For decades, the federal government attempted to issue every single benefit check on the third day of the month. As the population of retirees and disabled workers surged, this single-day distribution model created severe administrative bottlenecks; processing tens of millions of financial transactions in a 24-hour window strained the Federal Reserve banking system and routinely overwhelmed government customer service call centers.

To resolve this logistical nightmare, the government completely overhauled the distribution system in May 1997. If you began claiming benefits after this date, your monthly deposit is strategically staggered across the month based on the day you were born. Rather than dumping all funds simultaneously, the Social Security Administration disperses the massive banking load across three distinct Wednesdays.

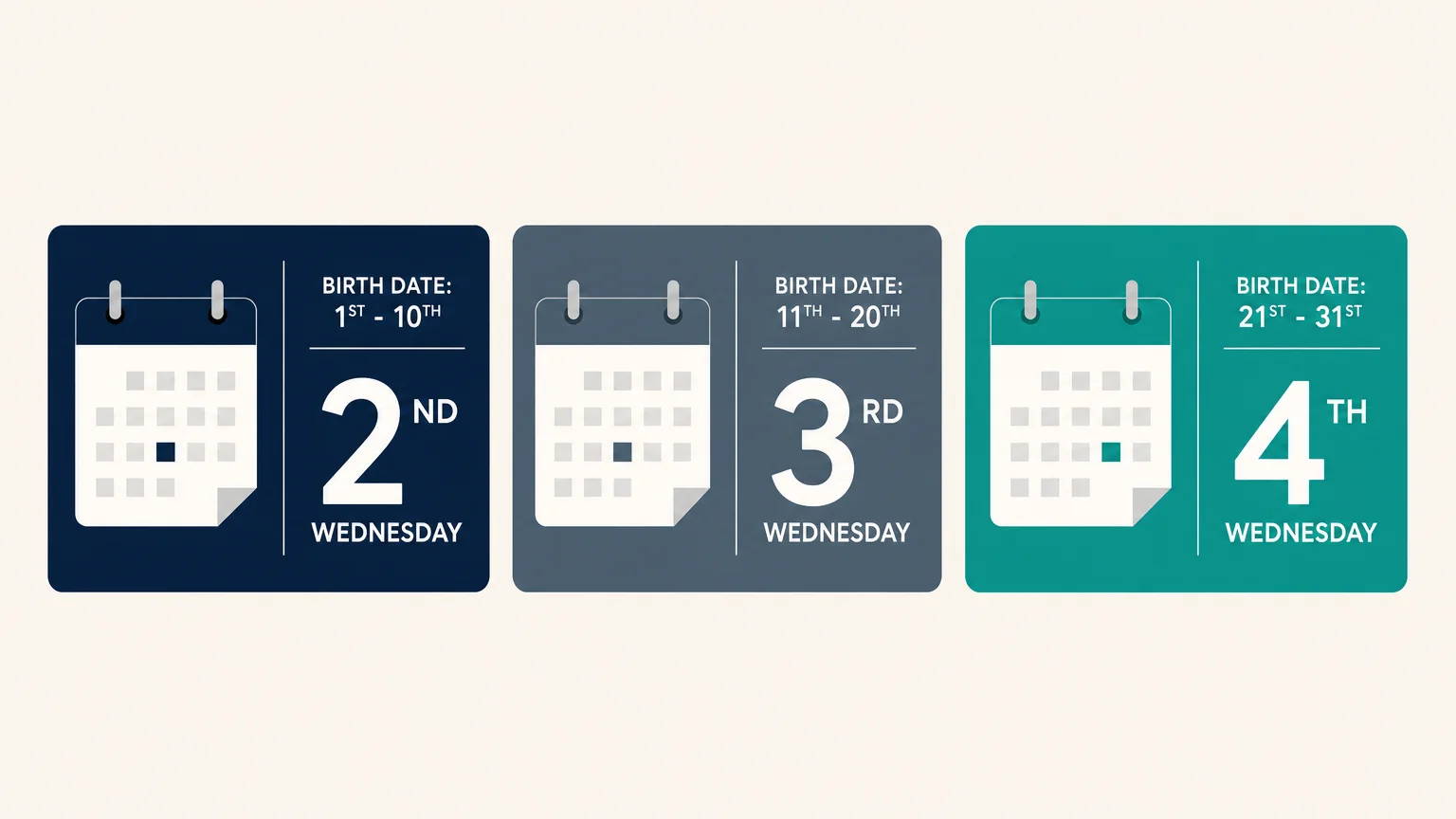

Your specific processing day is permanently tethered to the date of your birth. This system applies uniformly to standard retirement benefits, Social Security Disability Insurance (SSDI), and survivor benefits. Here is exactly how the modern payment calendar divides beneficiaries:

| Your Birth Date | Your Payment Day |

|---|---|

| 1st through the 10th of the month | Second Wednesday of every month |

| 11th through the 20th of the month | Third Wednesday of every month |

| 21st through the 31st of the month | Fourth Wednesday of every month |

Consider a practical example to understand how rigidly this system operates. If you were born on August 15th, your payment will always arrive on the third Wednesday of the month. If you were born on March 2nd, you are permanently assigned to the second Wednesday. It does not matter what month of the year it currently is; your assigned Wednesday remains your designated payday.

There is one crucial nuance regarding family benefits: if you receive benefits based on someone else’s work record—such as spousal benefits or survivor benefits—your payout date is entirely dictated by the primary earner’s birth date. If your spouse was born on the 5th, but you were born on the 25th, your spousal benefit will arrive on the second Wednesday of the month to align with your spouse’s record, completely ignoring your own birthday.

Thank you for this message. Very much appreciated.

Great article

Thank you for the monthly layout of the S.S. payment schedule.

Thank you very much for your message.

Excellent info thank you.

Thank you for your message .

We appreciate it

Thank you the article was very informative.

Thank you , it helps to see it in writing,

I am extremely grateful to you for such valuable information.