The traditional American retirement dream often featured a sprawling family home with empty guest rooms waiting for holiday visits. In 2026, that dream is facing a harsh mathematical and practical reality. While inflation has technically cooled from its pandemic-era peaks, the localized costs of maintaining a large property—specifically homeowners insurance, property taxes, and routine maintenance—have surged. This financial squeeze, combined with a shifting desire for simpler living, is pushing a record number of retirees to rethink their housing footprint.

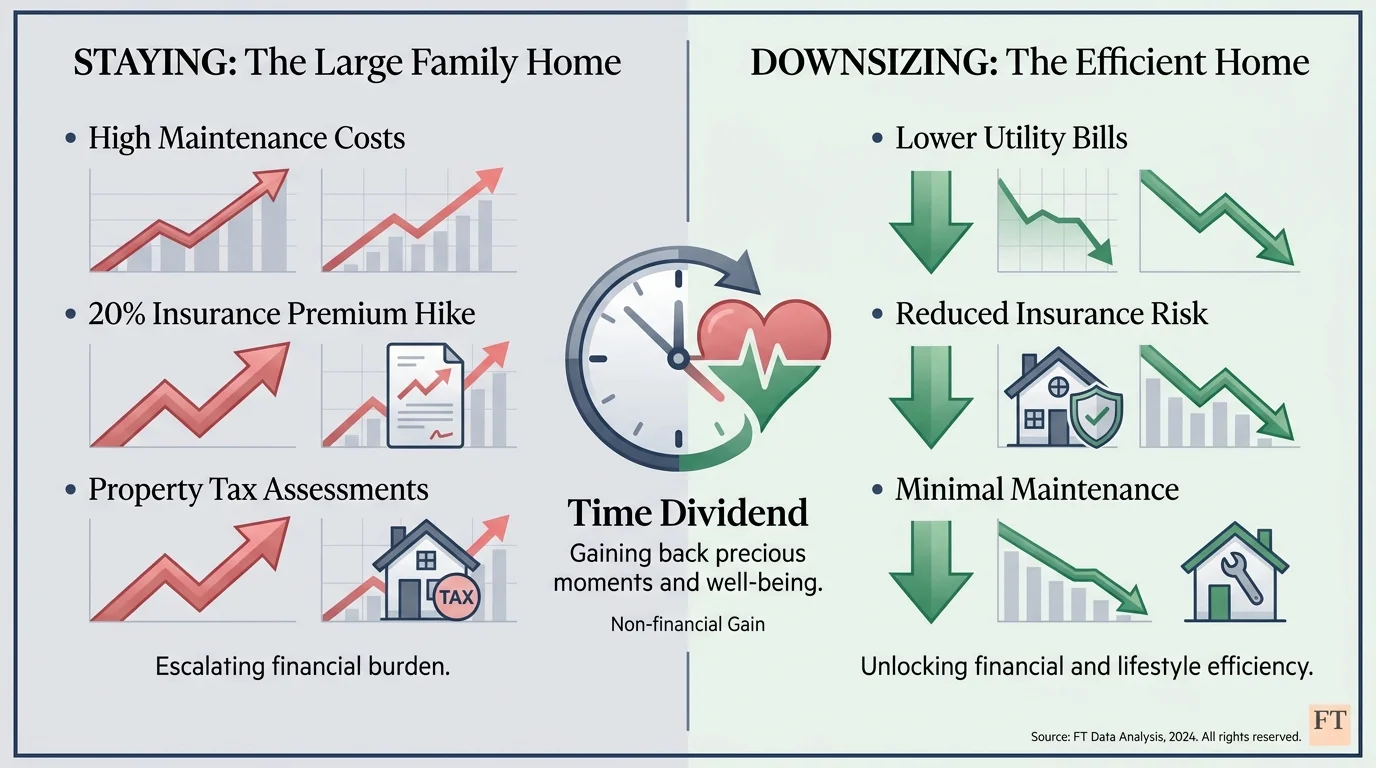

Downsizing is no longer just a reaction to an empty nest; it is a strategic defense mechanism against unpredictable expenses. When you maintain a home designed for a family of four or five, you pay to heat, cool, clean, and insure unused space. By trading square footage for efficiency, you reclaim not only your monthly cash flow but also your time and physical energy.

Whether you want to free up equity to fund travel, reduce the physical burden of yard work, or simply escape the relentless cycle of home repairs, moving to a smaller home offers tangible benefits. Understanding the economic forces driving this trend in 2026 will help you evaluate if right-sizing your living situation is the smartest move for your future.

The New Financial Math of 2026

Retirees living on fixed incomes face a unique set of economic pressures today. To understand why downsizing is accelerating, you have to look at the intersection of everyday living costs and retirement benefits.

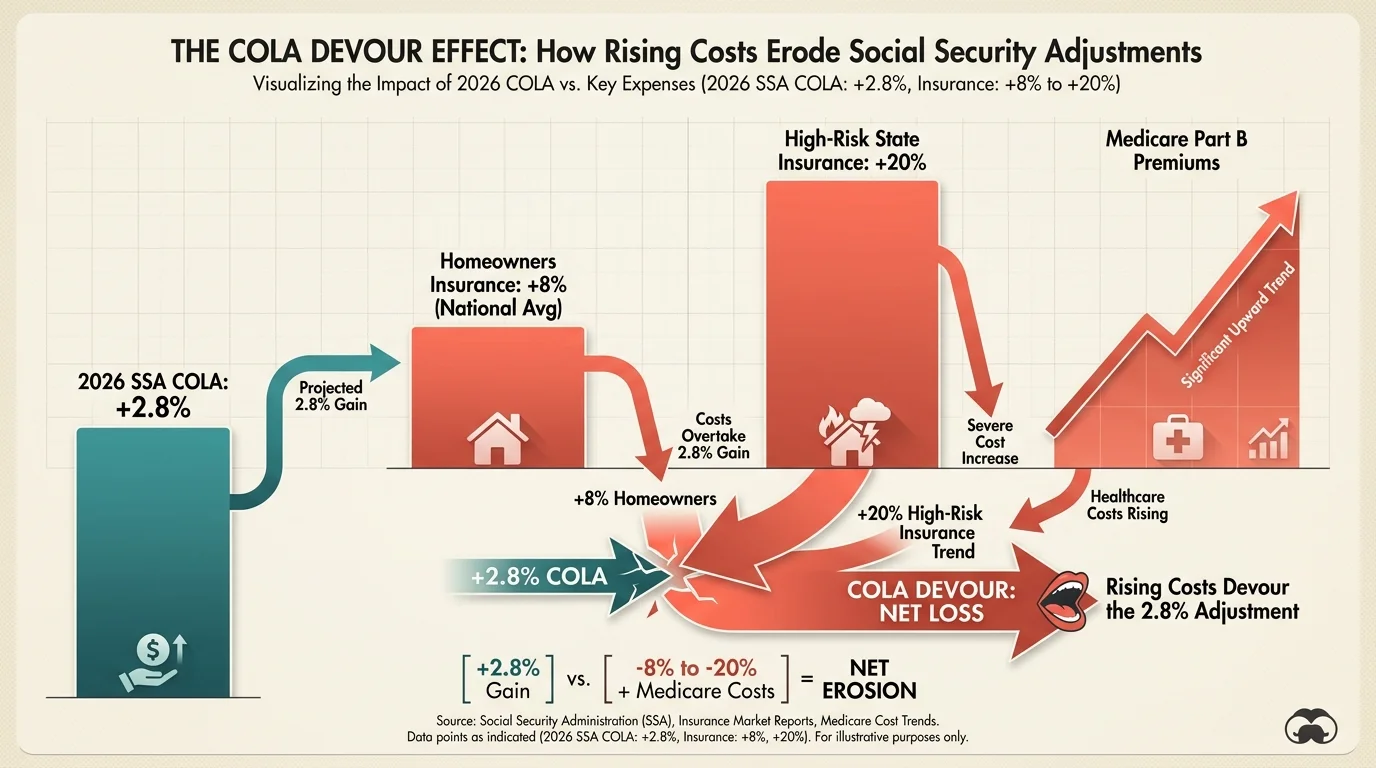

The 2026 Social Security Administration (SSA) cost-of-living adjustment (COLA) provided a modest 2.8 percent increase to monthly benefits. While helpful, this small bump is quickly devoured by rising healthcare costs. Medicare Part B premiums have seen significant increases in recent years, essentially wiping out a large portion of the COLA gains for millions of seniors. When your primary income sources barely keep pace with baseline inflation, you cannot afford to leak money through housing inefficiencies.

Homeowners insurance has become the most volatile line item in the retiree budget. Following several years of severe weather events and increased building material costs, national insurance premiums are projected to rise by an average of 8 percent in 2026 alone. If you live in a high-risk state—such as Florida, California, Louisiana, or Texas—you might experience premium hikes exceeding 20 percent, alongside forced moves to higher deductibles. Insurance companies are recalibrating their risk models, and older, larger homes carry the highest exposure.

Property taxes present another hurdle. As local municipalities grapple with their own increased operating costs, tax assessments on large properties have climbed steadily. Even if your mortgage is completely paid off, the combination of surging insurance premiums and property taxes can make a large home feel like a financial anchor.

“Your home should be your sanctuary, not a financial burden that drains your retirement savings. If a substantial chunk of your fixed income is going toward property taxes and maintenance, you are putting your long-term security at risk.” — Suze Orman, Financial Expert

Beyond the Math: The Lifestyle Shift

The decision to move is rarely driven by spreadsheets alone. Today’s retirees are prioritizing mobility, experiences, and peace of mind over the accumulation of physical property. Moving to a smaller home, a townhouse, or a managed community facilitates a lock-and-leave lifestyle that is highly sought after in 2026.

When you live in a smaller, more efficient space, you spend less time managing contractors, mowing lawns, and cleaning unused rooms. This time dividend allows you to focus on the activities that actually bring you joy—whether that means traveling, volunteering, or spending quality time with grandchildren.

Physical safety and aging in place also heavily influence the downsizing trend. A multistory home with steep staircases, sunken living rooms, and high-maintenance landscaping becomes a liability as mobility naturally changes. Retirees are actively seeking single-story layouts with wider hallways, walk-in showers, and minimal exterior maintenance. Moving while you are still healthy and energetic allows you to manage the transition on your own terms, rather than being forced into a sudden move due to a health crisis.

“Retirement is the time to right-size your life, not just your home. When you eliminate the physical and financial weight of maintaining empty rooms, you make space for the experiences that actually matter.” — Mitch Anthony, Retirement Lifestyle Expert

Comparing the Costs: Staying vs. Downsizing

To illustrate the financial impact of this decision, consider the typical monthly expenses associated with maintaining a large family home versus a downsized property. While exact numbers vary wildly based on your geographic location, the following table demonstrates how quickly the savings compound when you reduce your square footage.

| Expense Category | 2,500 Sq. Ft. Family Home | 1,200 Sq. Ft. Downsized Home | Expected Financial Impact |

|---|---|---|---|

| Property Taxes | High (Based on larger assessed value and lot size) | Lower (Based on smaller footprint) | Immediate annual savings, reducing the burden on fixed income. |

| Homeowners Insurance | Premium rates rising rapidly due to high replacement costs | Lower replacement cost; potentially lower risk profile | Protection against aggressive premium spikes in 2026. |

| Utilities (Gas, Electric, Water) | High consumption to heat/cool unused rooms | Highly efficient; only paying for the space you use | Consistent monthly cash flow improvement. |

| Routine Maintenance | Costly roof repairs, exterior painting, extensive yard work | Smaller roof, less siding, minimal landscaping | Fewer unexpected out-of-pocket expenses. |

| HOA / Community Fees | Often none, or nominal neighborhood fees | Potentially higher if moving to a managed senior community | May offset some savings, but shifts the physical labor to management. |

Pitfalls to Watch For

While the benefits of moving to a smaller home are compelling, the transition is not without financial risks. Downsizing is a major financial transaction, and failing to account for the hidden costs can quickly erode the equity you hoped to liberate.

Underestimating Transaction Costs

Selling a home is expensive. Between real estate agent commissions, staging costs, minor repairs to make the property market-ready, and closing costs on your new home, you can easily spend 8 to 10 percent of your home’s sale price on the transaction itself. If you are only downsizing slightly or moving to a comparable property in a more expensive zip code, the transaction fees might outweigh the long-term savings.

The HOA Fee Trap

Many retirees gravitate toward townhomes, condominiums, or 55-plus communities because they offer maintenance-free living. However, you must scrutinize the Homeowners Association (HOA) fees. A low-maintenance home loses its financial appeal if the monthly HOA dues rival your previous property tax bill. Furthermore, HOA fees are subject to regular increases, and special assessments for community repairs can catch you completely off guard.

Capital Gains and the IRMAA Trap

Selling a highly appreciated home can trigger unexpected tax consequences and healthcare costs. The IRS allows individuals to exclude up to $250,000 of capital gains on the sale of a primary residence ($500,000 for married couples filing jointly), provided you have lived in the home for two of the past five years. If your home has appreciated significantly beyond those limits, the excess gain is added to your Adjusted Gross Income (AGI).

A massive spike in your AGI does more than increase your income tax bill; it can directly impact your healthcare costs. The Medicare.gov program uses your modified adjusted gross income from two years prior to determine your Part B and Part D premiums. A large capital gain in 2026 could trigger an Income-Related Monthly Adjustment Amount (IRMAA) surcharge, causing your Medicare premiums to spike dramatically in 2028. Work closely with a tax professional to time your sale appropriately.

The Emotional Toll of Decluttering

Do not underestimate the psychological weight of parting with decades of possessions. The process of sorting through family heirlooms, children’s old belongings, and accumulated furniture is exhausting. Many retirees stall their downsizing plans simply because the thought of clearing out the garage or attic is too overwhelming. Start this process months—or even years—before you actually intend to list your house.

How to Execute a Successful Downsizing Strategy

If you have decided that a smaller home aligns with your retirement goals, a structured approach will minimize stress and protect your wealth. Treat this transition as a multi-phase project rather than a weekend chore.

First, conduct a rigorous lifestyle audit. Track which rooms in your current house you actually use on a daily basis. You might discover that you spend 90 percent of your time in the kitchen, living room, and primary bedroom, rendering the formal dining room and extra guest spaces obsolete. Use this insight to determine the exact square footage and layout you need for your next home.

Next, stress-test your future budget. Use resources from Bankrate to compare current mortgage rates if you plan to finance a portion of your new home. While many retirees aim to pay cash using the equity from their previous property, holding a small mortgage might make sense depending on your overall liquidity and investment strategy. Calculate the projected property taxes, insurance, and HOA fees of your target destination to ensure the move actually improves your monthly cash flow.

Finally, embrace the art of aggressive decluttering. Adopt a system where items are categorized into keep, sell, donate, or discard. Offer heirlooms to your children now rather than waiting; this allows you to enjoy seeing them appreciate the items while simultaneously clearing space. The less you have to pack, the cheaper your moving costs will be.

Frequently Asked Questions

Does downsizing always guarantee a lower cost of living?

No. Downsizing refers to reducing the physical size of your home, but your cost of living depends entirely on location and community structure. Selling a 3,000-square-foot home in the rural Midwest to buy a 1,200-square-foot condo in a premium coastal city will likely increase your living expenses. To guarantee savings, you must right-size both the square footage and the geographic cost of living.

How does selling my house affect my Medicare costs?

If the profit from selling your home exceeds the IRS capital gains exclusion limits ($250,000 for singles, $500,000 for married couples), the excess amount is treated as taxable income. This temporary income spike can trigger an IRMAA surcharge, which increases your Medicare Part B and Part D premiums. Because Medicare uses a two-year lookback period, a home sold at a massive gain in 2026 will impact your 2028 premiums.

Should I pay cash for a smaller home or take a small mortgage?

This depends on current interest rates and your portfolio’s performance. If mortgage rates are high, using your home equity to purchase the next property outright provides immense peace of mind and eliminates a major monthly expense. However, if tying up all your cash leaves you house-rich but cash-poor, taking a small mortgage to maintain liquidity for emergencies and healthcare costs might be the safer strategy.

Is it better to remodel my current home to age in place instead of moving?

According to data from AARP, the majority of older adults prefer to age in place. If you love your neighborhood and the primary issue is layout, remodeling—such as adding a main-floor master suite or widening doorways—can be highly effective. However, remodeling does not solve the issues of high property taxes, escalating insurance costs, or the burden of maintaining a large yard. You must weigh the construction costs against the transaction costs of moving.

Taking the Next Step

Moving to a smaller home is one of the most powerful levers you can pull to protect your retirement security. By shedding excess space, you insulate yourself against rising property taxes and unpredictable insurance premiums. More importantly, you buy yourself the freedom to spend your time and energy on the people and pursuits that matter most to you.

Start small. Begin sorting through one closet or one room this weekend. Speak with a local real estate agent to understand the current value of your home, and start touring smaller properties in areas that interest you. The sooner you understand your options, the more control you will have over your retirement lifestyle.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, health needs, tax situation, and goals—may require different approaches. When in doubt, consult a licensed professional.

Last updated: April 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply