Every day in 2026, thousands of Americans transition out of the workforce, leaving behind decades of daily routines, professional social circles, and geographic ties. For many, this milestone forces a critical look at their current living situation. The four-bedroom suburban home that perfectly accommodated a growing family often transforms into an empty, high-maintenance burden during retirement. Instead of simply downsizing into a smaller house down the street, a growing wave of older adults is relocating entirely. They are trading neighborhood sprawl for purpose-built 55 plus communities designed specifically around the retiree lifestyle.

The appeal of active adult living has shifted dramatically over the past decade. Modern developments look nothing like the quiet, isolated retirement villages of the past; they resemble luxury resorts combined with small-town main streets. Retirees are realizing that housing decisions dictate health, social engagement, and financial predictability just as much as portfolio allocation.

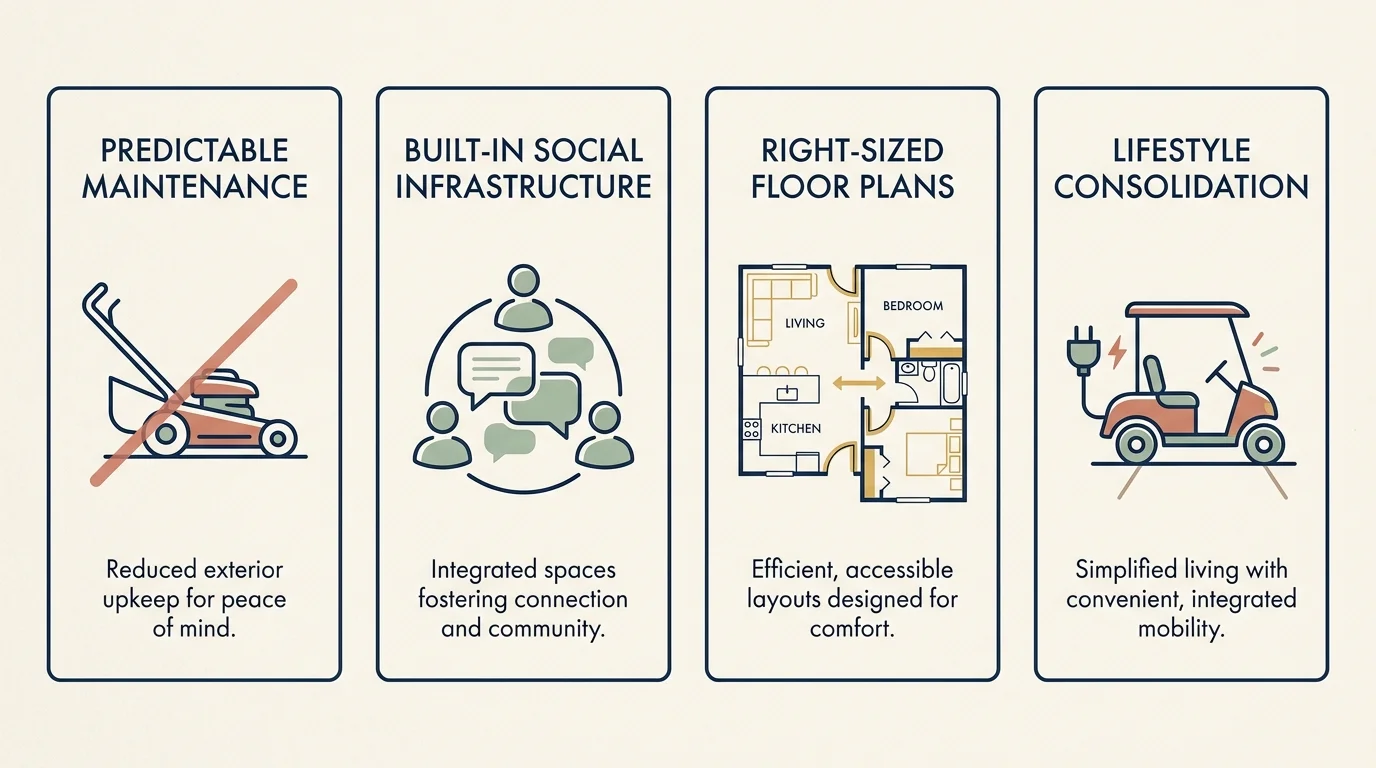

At a Glance: The Core Appeal

- Predictable Maintenance: Homeowners associations (HOAs) handle exterior upkeep, landscaping, and seasonal maintenance, freeing up hundreds of hours a year.

- Built-In Social Infrastructure: Daily calendars packed with clubs, fitness classes, and events naturally combat the isolation that often accompanies retirement.

- Right-Sized Floor Plans: Homes feature single-story layouts, wider doorways, and accessible bathrooms—allowing you to age comfortably without expensive future renovations.

- Lifestyle Consolidation: Having gyms, pools, walking trails, and dining options within a golf-cart ride reduces transportation costs and daily friction.

The Evolution of the Senior Neighborhood

If you still picture a retirement community as a sleepy enclave centered exclusively around a golf course, you need to update your perspective. The modern 55+ community has evolved to meet the demands of a new generation of retirees who prioritize wellness, lifelong learning, and active recreation over passive leisure. Today’s developers incorporate miles of paved walking trails, pickleball complexes, community gardens, woodworking shops, and even on-site continuing education centers.

This evolution aligns perfectly with a broader understanding of aging well. Research from organizations like the National Institute on Aging (NIA) continually highlights that remaining physically active and socially engaged dramatically improves cognitive health and longevity. When you live in a traditional neighborhood, organizing a social outing or finding a fitness class requires effort, driving, and coordination. In an active adult community, that friction disappears. The activities are quite literally outside your front door.

“Retirement is an artificial finish line. People need purpose, engagement, and connection just as much at 75 as they do at 45.” — Mitch Anthony, Financial Anthropologist and Author

By removing the barriers to socialization and physical activity, these communities engineer a healthier lifestyle by default. You are far more likely to join a Tuesday morning walking group or an evening wine-tasting club when the venue is three blocks away and attended by your immediate neighbors.

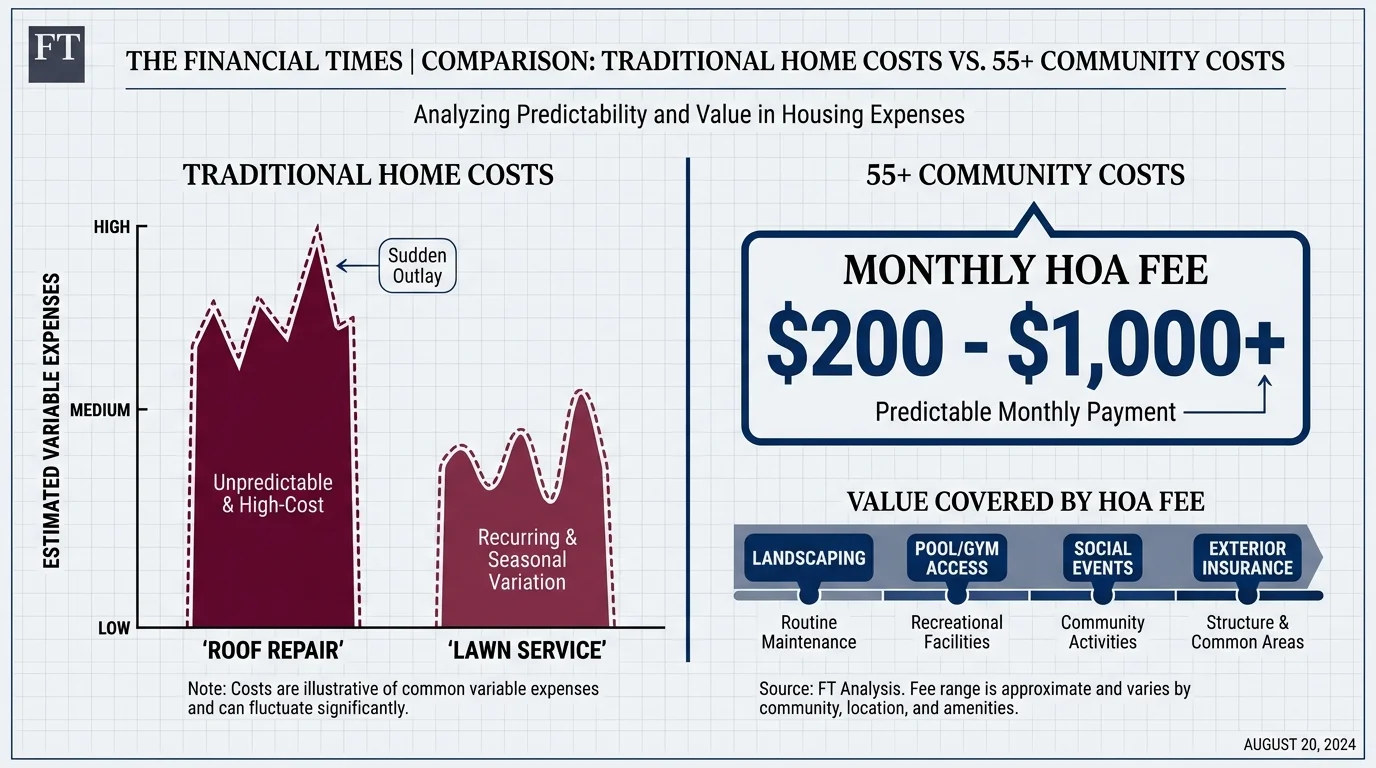

The Financial Reality: Weighing Costs Against Value

Moving to a 55+ community requires a careful financial analysis. While downsizing your square footage often yields a profit from the sale of your primary home, the ongoing carrying costs of a retirement community operate differently than a traditional neighborhood. The most significant variable is the Homeowners Association (HOA) fee.

HOA fees in active adult communities can range from $200 to over $1,000 per month, depending on the location and the extravagance of the amenities. At first glance, taking on a new monthly bill can feel counterintuitive for someone entering a fixed-income phase of life. However, you must evaluate what those fees replace in your current budget.

When you pay a comprehensive HOA fee, you typically eliminate individual bills for lawn care, snow removal, exterior home maintenance, gym memberships, pool upkeep, and sometimes even high-speed internet or basic cable. For a clear financial picture, you should consult resources from consumer protection advocates like the Consumer Financial Protection Bureau (CFPB) regarding reverse mortgages, housing costs, and managing debt in retirement.

“You want a retirement that is rich in experiences, not one where you are house-rich and cash-poor.” — Suze Orman, Personal Finance Expert

Comparing Your Options

To help you visualize the trade-offs, consider how a traditional neighborhood compares directly to an active adult community across various lifestyle and financial metrics.

| Feature | Traditional Neighborhood | 55+ Active Adult Community |

|---|---|---|

| Exterior Maintenance | 100% your responsibility; requires hiring contractors or personal physical labor. | Managed by the HOA; includes landscaping, snow removal, and sometimes roof/paint. |

| Demographics | Mixed ages; neighbors may be busy working families with varying schedules. | Peers in similar life stages; more available time for daytime socialization. |

| Home Design | Often multi-story; may require significant retrofitting for mobility issues later in life. | Purpose-built for aging; single-story, zero-step entries, walk-in showers. |

| Amenities | Typically limited to local municipal parks; requires driving to gyms or pools. | Private, resort-style facilities; clubhouses, fitness centers, sports courts on-site. |

| Cost Structure | Lower or nonexistent HOA fees; highly variable maintenance surprises. | Higher, mandatory HOA fees; highly predictable monthly housing expenses. |

Designing a Predictable and Accessible Future

One of the primary retirement community benefits lies in the architecture itself. Most homes in traditional suburbs were built for young families. They feature steep staircases, sunken living rooms, narrow hallways, and laundry machines located in basements. While these features rarely pose a problem in your fifties or sixties, they can become insurmountable obstacles in your eighties.

Active adult homes utilize universal design principles. Builders prioritize open floor plans, wide doorways that can accommodate walkers or wheelchairs, zero-threshold showers, and lever-style door handles. Even the placement of electrical outlets and appliances is thoughtfully considered to reduce bending and reaching.

Making this move in your early retirement years—rather than waiting until a health crisis forces you out of your two-story home—allows you to settle into a supportive environment while you are still healthy and energetic. You get to enjoy the resort amenities now, knowing that the physical layout of the home will support you if your mobility declines later. Organizations dedicated to aging well, such as the National Council on Aging (NCOA), emphasize that proactive environmental modifications are critical for maintaining independence in later life.

Navigating the Rules and Restrictions

Living in a deed-restricted community means abiding by community rules. For many retirees, the strict enforcement of covenants, conditions, and restrictions (CC&Rs) is a major selling point. It guarantees that the neighborhood will remain visually appealing, that no one will park an RV on their front lawn permanently, and that property values are aggressively protected.

For others, these rules can chafe. Before purchasing a home in an active adult community, you must thoroughly review the governing documents. You will encounter strict guidelines on everything from the color you can paint your front door to the types of plants allowed in your garden. There are also specific rules regarding who can live in the home and who can visit.

Under the Housing for Older Persons Act (HOPA), a 55+ community must ensure that at least 80% of its occupied units have at least one resident who is 55 years of age or older. Because of this, communities implement strict guest policies. You can certainly have your grandchildren visit, but the HOA will typically limit their stay to a specific number of days per year—often capping out at 30 to 60 days. If you plan on providing full-time childcare for your grandchildren, a 55+ community will not be a viable option.

Avoiding Common Errors When Choosing a Community

Even though active adult communities offer incredible lifestyle upgrades, the transition is not without potential pitfalls. Moving is expensive, and you want to ensure your chosen neighborhood serves you well for the long haul. Keep these common mistakes in mind as you evaluate your options.

- Underestimating HOA Fee Inflation: HOA fees never go down. They will increase over time to cover inflation, rising insurance premiums, and aging community infrastructure. Ensure your retirement budget can absorb a 3% to 5% annual increase in these fees without causing financial stress.

- Confusing “Active Adult” with “Assisted Living”: A 55+ active adult community provides housing and recreational amenities; it does not provide medical care, nursing staff, or daily living assistance. If you anticipate needing memory care or nursing support in the near future, you should look into Continuing Care Retirement Communities (CCRCs) instead.

- Skipping the Financial Health Check of the HOA: Before you close on a house, demand to see the HOA’s reserve study and recent financial statements. A beautifully manicured golf course means nothing if the association is secretly bankrupt. If the reserve funds are severely underfunded, you will eventually face massive special assessments to fix roofs, repave roads, or repair the clubhouse.

- Not Testing the Culture: Every community has a distinct personality. Some are highly political, others are heavily focused on daily golf, and some prioritize arts and quiet hobbies. Buying a home without understanding the social dynamics can leave you feeling isolated in a crowd. Always try to secure a short-term rental within the community before committing to a purchase.

Frequently Asked Questions

Can someone younger than 55 live in a 55+ community?

Yes, under specific circumstances. The federal 80/20 rule requires that 80% of the homes have at least one resident aged 55 or older. The remaining 20% of homes can theoretically be sold to younger buyers, but most communities write their own bylaws to strictly limit this. However, if a 58-year-old marries a 45-year-old, the younger spouse is generally permitted to live there because the older spouse satisfies the age requirement.

Are HOA fees in a retirement community tax-deductible?

Generally, no. HOA fees for your primary residence are considered personal living expenses by the IRS and cannot be deducted on your federal tax return. If you purchase a home in a 55+ community as an investment property and rent it out, the rules change, but for typical owner-occupants, there is no tax benefit.

Do these communities provide transportation?

While 55+ communities do not offer the scheduled medical transport vans typically found in independent living or assisted living facilities, many larger developments organize group excursions, shopping shuttles, or airport transfers through their activities director. However, you should plan to maintain your own vehicle or rely on local public transit and ride-sharing services for personal appointments.

What happens if the 55+ spouse passes away, leaving a younger spouse behind?

Most community bylaws are written with a “survivorship” clause. If the qualifying 55+ spouse passes away, the surviving younger spouse is usually permitted to remain in the home indefinitely. Always verify this specific clause in the HOA documents before purchasing to ensure your partner is protected.

Taking the Next Step

Deciding where to live during your retirement years is just as important as deciding when to retire. An active adult community offers a compelling blend of low-maintenance homeownership, vibrant social engagement, and an environment designed specifically for your comfort and longevity. However, it requires a clear-eyed assessment of your finances, your tolerance for community rules, and your long-term health outlook.

If you are intrigued by the retiree lifestyle these neighborhoods offer, start scheduling tours. Look beyond the shiny clubhouse and talk to the actual residents. Ask them what they love, what frustrates them about the HOA, and whether the monthly fees feel justified by the experience. Even better, rent an Airbnb within your target community for a month during their busiest season. There is no better way to discover if a neighborhood truly feels like home than by living the daily routine before signing a mortgage.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, health needs, tax situation, and goals—may require different approaches. When in doubt, consult a licensed professional.

Last updated: March 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

I have been looking into the 55+ communities, and they are all so expensive. Why is that ?. What if your retirement is not that much, so then those persons would have to live in the communities that are not safe.