Stepping into retirement brings a sudden urge to reinvent your lifestyle, prompting major purchases that promise to define your next chapter. Yet, retirees frequently discover that the big-ticket items meant to maximize their freedom quickly become financial anchors draining their savings. Before you sign a deed, buy a recreational vehicle, or commit to a luxury club membership, you must understand how these assets perform over a ten-year timeline. Examining the long-term carrying costs and practical realities of popular retirement buys reveals a sharp contrast between initial excitement and everyday utility. We will examine eight common purchases that seem like brilliant ideas on day one but routinely transform into profound regrets as your retirement unfolds.

1. The Massive Recreational Vehicle (RV)

The vision of touring the national parks and waking up to new vistas every morning drives thousands of retirees to purchase a luxury Class A or Class C motorhome. The dealership showroom highlights the stainless steel appliances and expanding slide-outs, making the vehicle feel like a perfect rolling condominium. However, the financial realities of RV ownership often hit hard within the first three years.

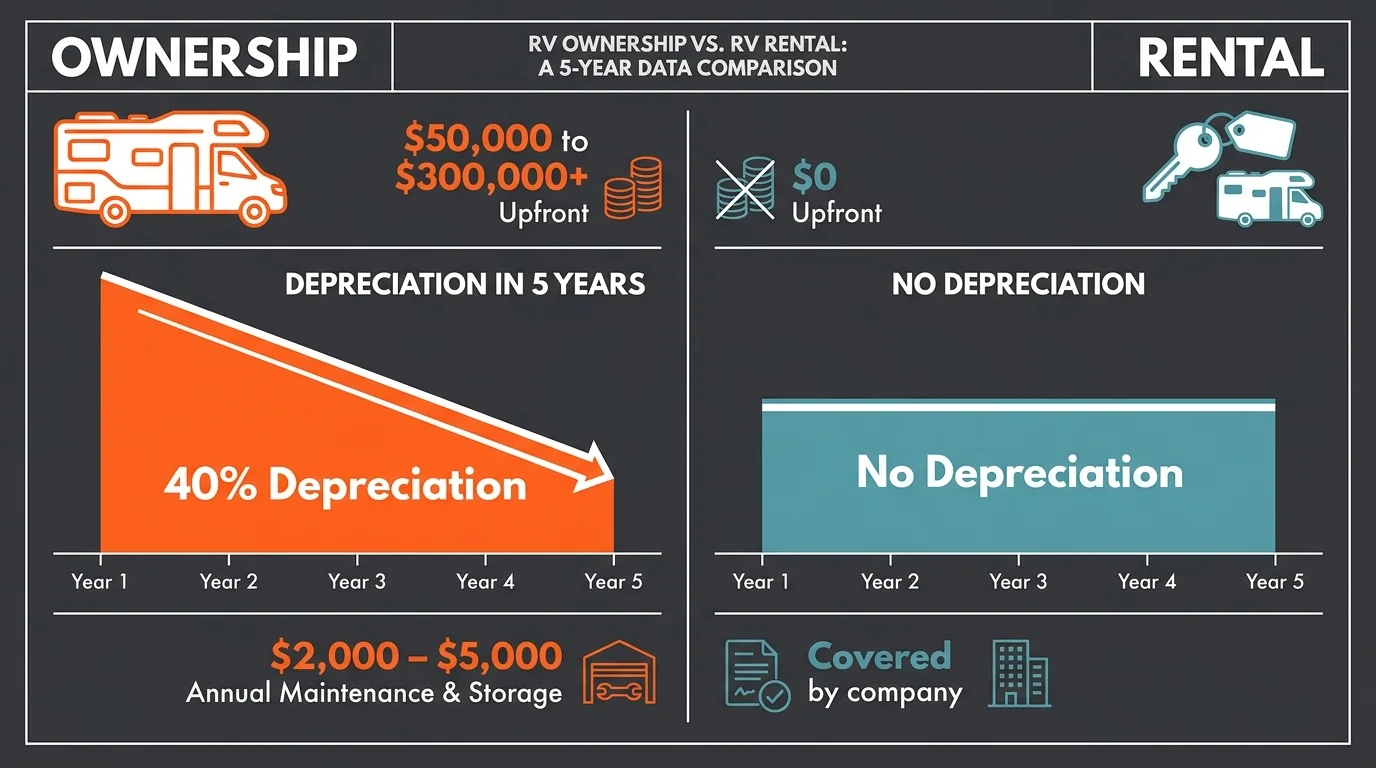

New motorhomes experience catastrophic depreciation, often losing 20% of their value the moment you drive them off the lot. Beyond the initial purchase price, which can easily exceed $150,000, you face a constant barrage of carrying costs. Fuel efficiency rarely tops ten miles per gallon, specialized insurance policies carry high premiums, and campsite fees rival the cost of mid-range hotels. When you are not traveling, you must pay for secure, climate-friendly storage. Maintenance requires specialized mechanics who understand both automotive engines and residential plumbing systems, leading to expensive repair bills.

| Financial Factor | RV Ownership | RV Rental (Peer-to-Peer or Commercial) |

|---|---|---|

| Upfront Cost | $50,000 to $300,000+ | $0 upfront (pay per trip) |

| Depreciation | Steep and immediate (up to 40% in 5 years) | None |

| Maintenance & Storage | $2,000 – $5,000+ annually | Covered by the rental company |

| Flexibility | Tied to one specific vehicle type | Choose different sizes based on the specific trip |

2. The Remote Vacation Cabin

Buying a secluded cabin in the mountains or a quiet lake house seems like the ultimate way to secure peaceful getaways and host family gatherings. The idea of a legacy property that your children and grandchildren will visit every summer provides a strong emotional pull. Unfortunately, managing a secondary property transforms quickly from a relaxing retreat into a part-time job.

A second home means you now shoulder the burden of two roofs, two property tax bills, two sets of utility costs, and double the landscaping. Remote properties often suffer from harsh weather, leading to burst pipes or storm damage that goes unnoticed until your next visit. Furthermore, family dynamics shift over time. Adult children navigate demanding careers and their own children’s sports schedules, making those idyllic summer-long visits incredibly rare. If you find yourself tied down to the cabin because you feel financially obligated to use it, the property has restricted your retirement freedom rather than expanding it. Consulting resources from the Consumer Financial Protection Bureau (CFPB) regarding secondary mortgages and housing costs can provide a sobering look at the true financial weight of holding multiple properties.

3. The Family “Compound” (Upsizing)

Many retirees believe they need a larger house to serve as the ultimate gathering place for the extended family. You might feel tempted to purchase a five-bedroom home with a massive dining room and a sprawling backyard, anticipating lively holidays and weekend visits. This emotional purchase assumes that if you build it, they will come.

In reality, you spend 350 days a year living in a massive, echoing space, paying exorbitant heating and cooling bills, and cleaning rooms that gather dust. As mobility naturally declines with age, navigating a large, multi-story home becomes physically taxing. Downsizing is often the smarter financial and lifestyle choice. A smaller, well-designed space in a walkable community frees up capital and reduces your daily maintenance burden. If family comes to visit, it is often significantly cheaper to rent them an Airbnb or hotel rooms down the street than to finance and maintain a massive home year-round.

“You have to make sure that your money outlives you, not the other way around.” — Jean Chatzky, Financial Editor and Author

4. Timeshares and Vacation Clubs

Vacation clubs and timeshares aggressively target people entering retirement, promising guaranteed luxury vacations at locked-in prices. The high-pressure sales presentations play on your desire to travel and make memories. However, timeshares remain one of the most notoriously poor financial commitments a retiree can make.

When you purchase a timeshare, you buy into an ongoing liability. The upfront cost represents only a fraction of the actual expense. Consider these severe drawbacks:

- Escalating Maintenance Fees: Annual fees routinely increase at rates well above inflation, regardless of whether you use the property that year.

- Special Assessments: When the resort needs a new roof or pool renovations, management passes those substantial costs directly to the owners.

- Near-Zero Resale Value: The secondary market for timeshares is practically nonexistent. Many owners end up paying companies thousands of dollars just to legally surrender their contracts.

- Booking Frustrations: Exchanging points for different locations or securing highly desired weeks requires navigating complex, restrictive booking systems.

Organizations like AARP routinely warn retirees about the dangers of the timeshare trap and the difficulty of exiting these ironclad contracts.

5. The Maintenance-Heavy Boat

The old joke states that the two best days in a boat owner’s life are the day they buy it and the day they sell it. For retirees, this cliché holds an uncomfortable amount of truth. A boat represents the ultimate leisure purchase, signaling a life of fishing, sunset cruises, and marine exploration.

The financial reality of boat ownership centers on the “10% rule,” which dictates that you should expect to spend roughly 10% of the boat’s purchase price annually on maintenance and operation. Slip fees, winterizing, trailer registration, specialized insurance, and marine fuel create a constant financial drain. Saltwater environments rapidly corrode mechanical parts, requiring frequent and expensive professional servicing. Much like the RV, you may find that renting a boat or joining a local boat club provides 90% of the enjoyment with none of the maintenance anxiety or long-term financial liability.

6. Complex Permanent Life Insurance Policies

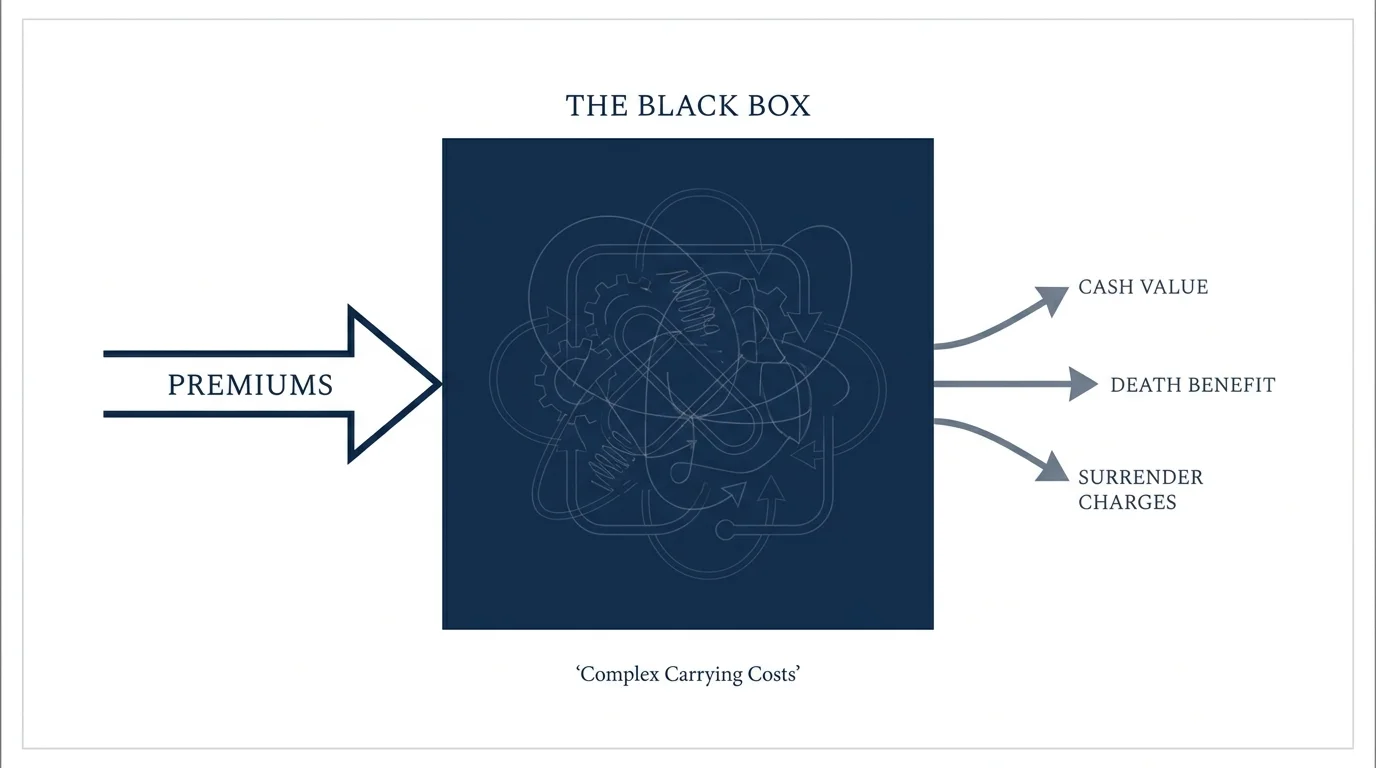

As you transition out of the workforce, financial salespeople may approach you with complex insurance products, such as Indexed Universal Life (IUL) or certain types of Whole Life insurance. These products are frequently pitched not just as death benefits, but as “safe” retirement investments or tax-free income vehicles.

While permanent life insurance has valid estate-planning applications for ultra-high-net-worth individuals, it is often a poor choice for the average retiree. These policies typically feature exceptionally high internal costs, massive upfront commissions for the salesperson, and severe surrender charges if you need to access your money early. Tying up your liquid retirement savings in a highly restrictive insurance contract reduces your financial flexibility. For independent guidance on evaluating complex financial products, the SEC’s Investor.gov portal provides excellent, bias-free educational materials on the true costs of annuities and permanent insurance.

7. The Luxury “Dream” Car

After decades of driving practical family sedans and economical commuters, many retirees decide to reward themselves with a high-end luxury vehicle or a classic sports car. You have worked hard, and writing a check for an $80,000 luxury coupe feels like a well-deserved trophy for a successful career.

Unfortunately, expensive vehicles represent rapidly depreciating assets purchased at exactly the moment you transition to a fixed income. Luxury cars require premium fuel, specialized synthetic oil changes, and expensive proprietary parts. Insurance premiums for high-performance vehicles remain notoriously high. Furthermore, as we age, the low clearance of a sports car or the overly complex digital interfaces of modern luxury vehicles can become daily frustrations. Enjoying your driving experience is important, but tying up a significant portion of your nest egg in a depreciating asset limits your ability to adapt to future health or housing needs.

8. Professional-Grade Hobby Equipment

Retirement provides the gift of time, allowing you to finally pursue passions you sidelined during your working years. The mistake occurs when you purchase professional-grade equipment for a hobby you have not yet fully adopted. We frequently see retirees drop $15,000 on a complete professional woodworking shop, buy $8,000 worth of specialized camera gear, or install a state-of-the-art indoor golf simulator.

If you discover six months later that the sawdust aggregates your allergies, hauling heavy camera lenses hurts your back, or you simply prefer playing golf outdoors, that expensive equipment gathers dust. The smart approach relies on incremental spending. Start with entry-level or rented equipment. Take a local class to confirm your interest. Only upgrade your gear when your skill level explicitly demands it and your passion for the hobby has proven sustainable.

Pitfalls to Watch For

The first twelve to eighteen months of retirement are particularly vulnerable times for your finances. This period, often called the “honeymoon phase,” carries high emotional momentum. You feel an overwhelming urge to celebrate your freedom, which can lead to impulsive spending. Watch out for the justification trap, where you tell yourself, “I worked 40 years for this.” While you certainly deserve to enjoy your wealth, wrapping your identity in new, expensive possessions rarely provides lasting fulfillment.

Another major pitfall is failing to account for inflation in your carrying costs. When you calculate the affordability of a boat or a second home, you might look at today’s insurance and maintenance rates. In ten years, those costs could double, placing severe stress on your portfolio withdrawals.

Getting Expert Help

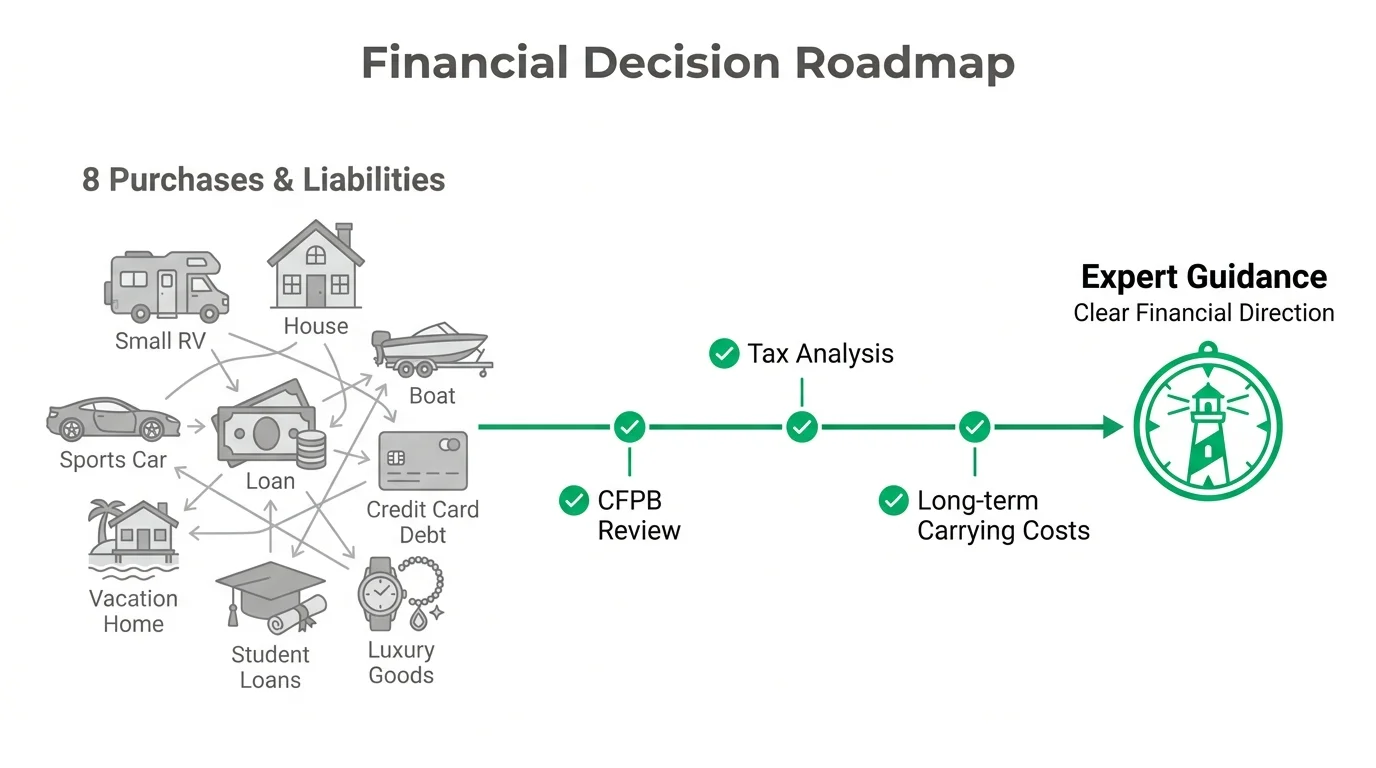

Before executing any purchase that requires a massive layout of cash or locks you into ongoing monthly expenses, run the scenario past a neutral professional. Seeking expert advice creates a necessary cooling-off period and introduces objective math into an emotional decision. Consider reaching out for help in these specific scenarios:

- Evaluating a Second Home: Ask a fiduciary financial planner to model how a secondary property purchase affects your portfolio survivability over a 30-year timeline.

- Reviewing Insurance Pitches: If an agent pitches a complex life insurance product as a retirement investment, have a fee-only advisor review the contract and commission structure before you sign.

- Structuring Large Purchases: If you do decide to buy an RV or luxury vehicle, a professional can advise you on the most tax-efficient way to withdraw the funds from your IRA or 401(k) to avoid bumping yourself into a higher tax bracket. You can locate verified fiduciaries through organizations like the Certified Financial Planner Board.

“Do not save what is left after spending, but spend what is left after saving.” — Warren Buffett, Investor and CEO

Frequently Asked Questions

Is it ever a good idea to buy a timeshare in retirement?

From a purely financial perspective, timeshares are rarely good investments. They are lifestyle purchases with guaranteed, escalating costs and almost zero resale value. If you want guaranteed vacation time, setting aside a dedicated travel budget and renting resorts on the open market provides far more flexibility and financial safety.

How long should I wait before making a big purchase after retiring?

Financial experts generally recommend waiting six to twelve months after your official retirement date before making major lifestyle purchases. This cooling-off period allows you to settle into your new daily routine, understand your actual fixed-income cash flow, and separate genuine long-term desires from the initial euphoria of quitting work.

Should I pay cash or finance large retirement purchases?

This depends heavily on current interest rates and your tax situation. Liquidating a large chunk of a traditional IRA to pay cash for an RV could trigger a massive tax bill and increase your Medicare premiums. Conversely, taking on high-interest debt on a fixed income creates immediate cash-flow stress. A tax professional should analyze any withdrawal exceeding your normal monthly needs.

What is the best alternative to buying a vacation home?

Long-term rentals are the best alternative. Renting a house in your desired location for two or three months out of the year gives you the immersive experience of living there without the property taxes, maintenance burdens, or year-round commitment. It also allows you to change locations easily if you get bored with the area.

Navigating Your Retirement Spending

The core theme of successful retirement spending is prioritizing flexibility over permanent commitments. Every dollar you keep out of an illiquid, depreciating asset is a dollar that can support your healthcare needs, fund spontaneous travel, or provide peace of mind during market downturns. Before making a massive purchase, test the waters through renting, taking classes, or taking extended trips. True retirement freedom comes from owning your time, not from allowing expensive possessions to own you.

This article provides general retirement education and information only. Every retiree’s situation is unique—what works for others may not work for you. For personalized advice, consider consulting a qualified financial professional such as a CFP or CPA.

Last updated: May 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply