Protecting your fixed income in retirement requires looking past sunny beaches to measure the true daily cost of living in your chosen destination. Moving to one of the cheapest states retirees favor allows your savings to stretch significantly further through low housing prices, affordable healthcare, and favorable tax laws. While high-insurance regions can quickly deplete your nest egg, a financially friendly location buys you a higher quality of life with less stress. By analyzing real estate markets, state taxes, and everyday expenses, you can identify regions that actively preserve your wealth. Here is an in-depth look at seven states where you will pay the least to fund your retirement years.

What Makes a State Truly Affordable for Retirees?

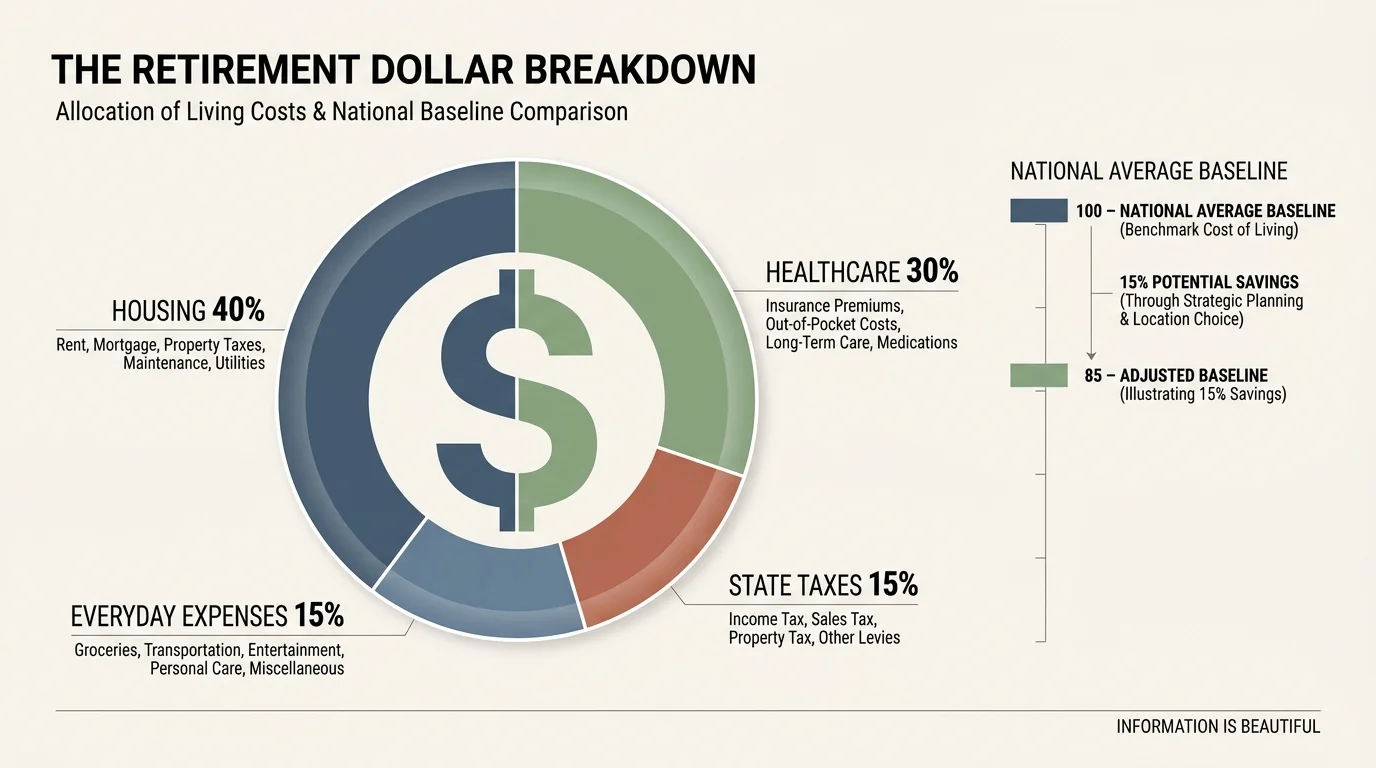

Affordability involves far more than tracking the median home price in a new neighborhood. Achieving an affordable retirement usa lifestyle requires evaluating every dollar that leaves your bank account each month. Many retirees relocate to save on property taxes, only to discover that their new state levies massive sales taxes on groceries or charges exorbitant vehicle registration fees. True affordability requires a holistic view of your monthly budget.

To determine where retirees pay the least, you must analyze the overall cost of living usa index for each state. This index measures the average cost of necessities—like housing, food, transportation, and healthcare—against the national average, which is always set at a baseline of 100. If a state has a cost of living index of 85, living there is 15 percent cheaper than the national average. When you combine a low baseline cost of living with tax policies that favor older adults, you create a powerful environment for preserving your wealth.

Below is a comparison of seven states that consistently rank at the bottom for living expenses, making them ideal destinations for retirees seeking financial breathing room.

| State | Cost of Living Index | Median Home Price (Est. 2026) | Social Security Taxed? |

|---|---|---|---|

| Mississippi | 85.1 | $160,000 | No |

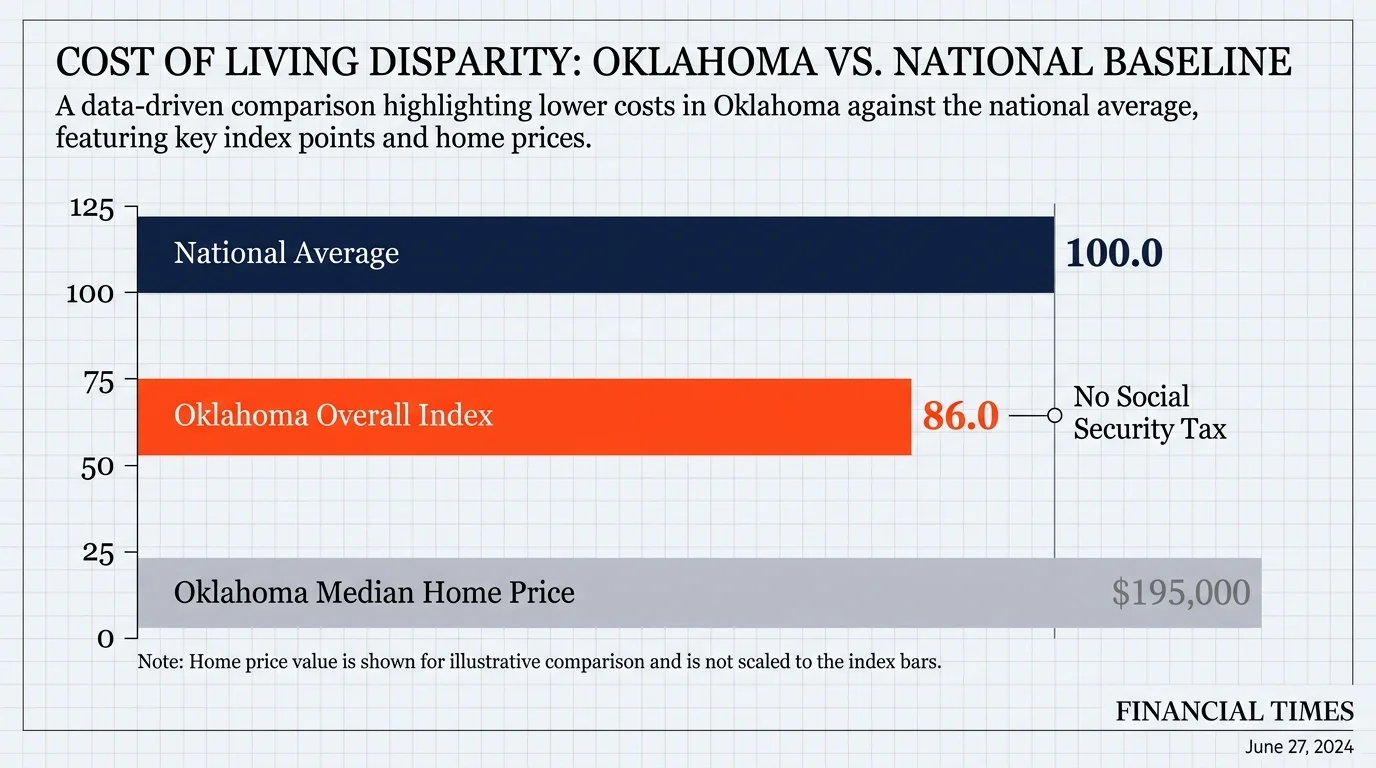

| Oklahoma | 86.0 | $195,000 | No |

| Arkansas | 87.0 | $175,000 | No |

| Alabama | 88.6 | $210,000 | No |

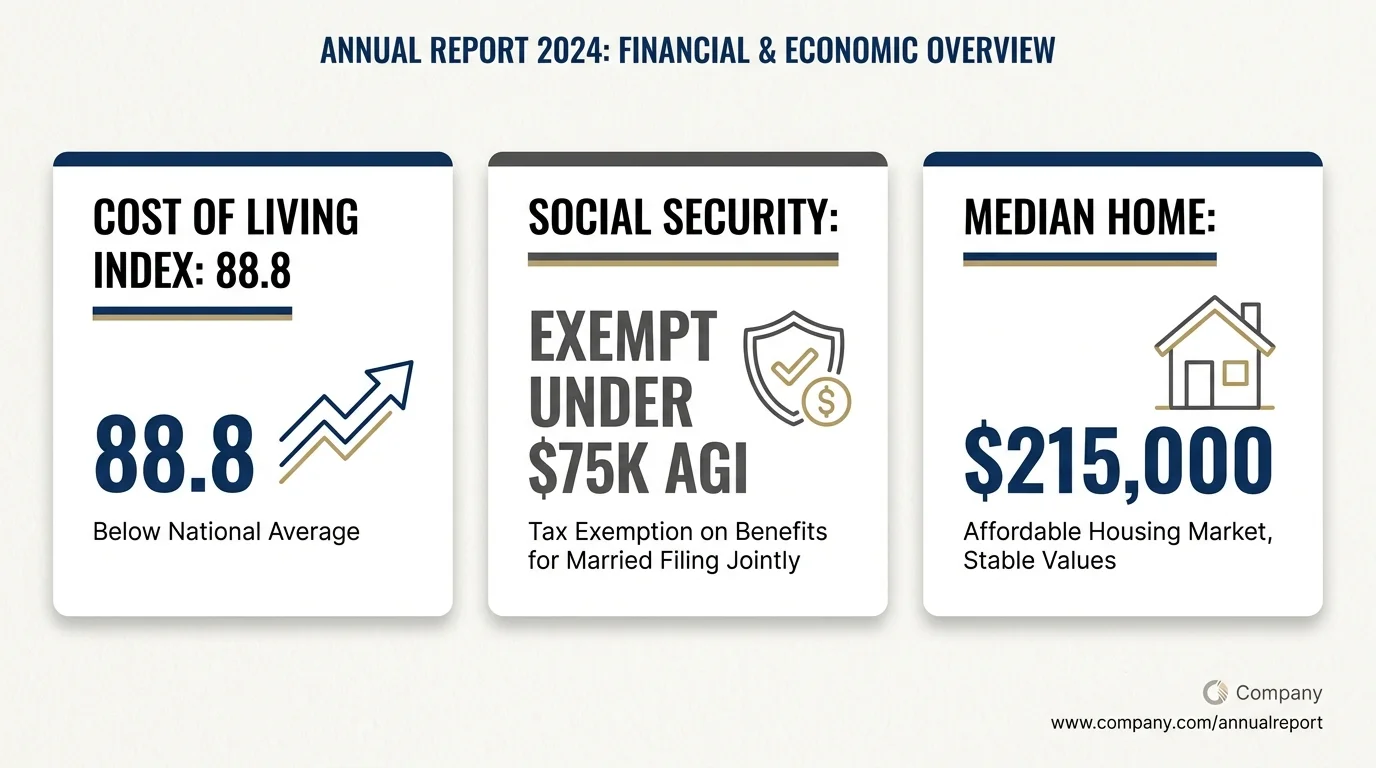

| Kansas | 88.8 | $215,000 | Exempt under $75k AGI |

| West Virginia | 89.0 | $150,000 | No |

| Missouri | 89.0 | $230,000 | No |

1. Mississippi: The Lowest Overall Cost of Living

The Financials: Year after year, Mississippi holds the title for the lowest cost of living in the United States. With housing costs sitting nearly 40 percent below the national average, you can purchase a comfortable home without liquidating your investment portfolio. Beyond cheap real estate, Mississippi offers one of the most generous tax environments for older adults; the state completely exempts all qualified retirement income from state income taxes. This means your Social Security benefits, 401(k) distributions, IRA withdrawals, and pension payouts remain untouched by state tax collectors.

The Lifestyle: Mississippi delivers a slow, relaxed pace of life anchored by rich cultural traditions. Retirees flock to the Gulf Coast for affordable waterfront living, where towns like Ocean Springs offer beautiful beaches and vibrant art scenes. Inland cities like Oxford provide the energy and amenities of a classic college town at a fraction of the cost you would find in other states.

The Catch: The exceptionally low cost of living comes with trade-offs in public infrastructure and healthcare. Rural areas in Mississippi often lack immediate access to specialized medical facilities. If managing chronic health conditions is a priority, you will need to map out proximity to major medical hubs in Jackson or the coastal region before purchasing a home.

2. Oklahoma: Affordable Housing and Energy

The Financials: Oklahoma ranks as a premier destination for low cost living, driven largely by its affordable housing market and low utility costs. A robust local energy sector keeps electricity and natural gas bills manageable during both the hot summers and chilly winters. Oklahoma does not tax Social Security benefits, and it offers a $10,000 exclusion for other types of retirement income. Furthermore, property taxes remain highly competitive, ensuring your monthly carrying costs stay low well into your later years.

The Lifestyle: You will find a blend of Southern charm and Midwestern practicality in Oklahoma. The state features expansive open spaces, beautiful lakes, and friendly communities. Metropolitan areas like Oklahoma City and Tulsa provide exceptional healthcare, diverse dining, and cultural attractions—including thriving arts districts—without the crushing traffic or expense of coastal cities.

The Catch: Oklahoma sits squarely in Tornado Alley. While your property taxes and mortgage might be incredibly low, you must budget for higher homeowners insurance premiums. Severe weather events drive up insurance rates, so you should obtain concrete insurance quotes on prospective properties before committing to a move.

3. Arkansas: Natural Beauty on a Budget

The Financials: Arkansas offers a cost of living that sits comfortably 13 percent below the national average. Home prices routinely fall under $200,000, making it an attractive destination for retirees looking to downsize and pocket the equity from their previous homes. The state does not tax Social Security benefits and allows you to exclude up to $6,000 of employer-sponsored pension or IRA income. Property taxes in Arkansas are exceptionally low, easing the long-term burden of homeownership.

The Lifestyle: Known as The Natural State, Arkansas appeals directly to active retirees who want to spend their time outdoors. The Ozark Mountains offer world-class hiking, fishing, and boating. Towns like Hot Springs provide historic charm, while the rapid growth in Northwest Arkansas (around Bentonville and Fayetteville) has introduced incredible culinary and cultural amenities funded by corporate investments in the region.

The Catch: Arkansas relies heavily on sales tax to generate revenue. The combined state and average local sales tax rate frequently exceeds 9 percent. While your housing and property taxes remain low, you will feel the pinch at the cash register when buying clothing, household goods, and vehicles.

4. Alabama: Extremely Low Property Taxes

The Financials: Alabama is a powerhouse for retirees aiming to drastically reduce their housing expenses. The state boasts the second-lowest property tax rate in the country, averaging around 0.38 percent of a home’s assessed value. Like its neighbors, Alabama exempts Social Security benefits from state income tax. Furthermore, traditional defined-benefit pensions are entirely exempt, making this state a paradise for retired teachers, government workers, and union members.

The Lifestyle: Alabama offers tremendous geographic diversity. You can choose to retire along the white sand beaches of the Gulf Shores, settle in the Appalachian foothills of Huntsville, or enjoy the rich history of Montgomery. The climate is warm year-round, which drastically reduces heating bills and allows for constant outdoor recreation.

The Catch: Alabama is one of the few remaining states that taxes groceries. While legislative efforts continue to slowly reduce this tax, paying sales tax on your weekly food shopping adds up over time. Additionally, summer humidity can be oppressive, leading to elevated air conditioning costs during peak months.

5. West Virginia: The Cheapest Real Estate in America

The Financials: If securing cheap property is your primary goal, West Virginia demands your attention. The median home price hovers around $150,000, presenting the most affordable real estate market in the nation. Property taxes are remarkably low, and the state has fully phased out income taxes on Social Security benefits for most retirees. The overall cost of utilities, groceries, and transportation keeps daily living incredibly cheap.

The Lifestyle: West Virginia offers peace, quiet, and breathtaking scenery. It is an ideal retreat for introverts and nature lovers who want to escape the congestion of modern suburban life. The changing seasons provide beautiful autumn foliage and mild summers, creating a perfect backdrop for a serene retirement.

The Catch: The rugged terrain that makes West Virginia beautiful also makes it isolated. Major airports are few and far between, which can complicate travel if you plan to frequently visit family out of state. Furthermore, high-speed broadband access and top-tier medical specialists can be difficult to find outside of larger towns like Morgantown or Charleston.

6. Kansas: Midwestern Stability and Low Unemployment

The Financials: Kansas balances affordability with excellent local infrastructure. The cost of living is roughly 11 percent below the national average. Kansas exempts Social Security benefits from state taxation for retirees with an adjusted gross income under $75,000. Everyday expenses, from gasoline to groceries, are highly manageable, allowing your retirement savings to generate reliable, lasting income.

The Lifestyle: Kansas is defined by safe, family-friendly communities and wide-open spaces. Suburban areas outside of Kansas City and Wichita offer fantastic amenities, great local restaurants, and engaging community centers. It is a practical, no-nonsense state where neighbors know each other and community ties run deep.

The Catch: Property taxes in Kansas are noticeably higher than in neighboring affordable states like Missouri or Oklahoma. Additionally, the state taxes other forms of retirement income, including IRA withdrawals and out-of-state public pensions. You must calculate your specific tax liability rather than assuming all your income will remain untouched.

7. Missouri: Favorable Tax Changes and Cultural Hubs

The Financials: Missouri offers an attractive combination of low housing costs and recent, highly favorable tax legislation. In 2024, the state eliminated income taxes on Social Security benefits for all retirees, regardless of their income level. Public pensions also receive generous exemptions. The median home price sits well below the national average, and everyday goods remain cheap due to strong local agriculture and logistics networks.

The Lifestyle: Missouri gives you the option to choose between quiet lake living and vibrant urban centers. The Lake of the Ozarks is a massive draw for boating enthusiasts, while Branson provides endless live entertainment. Alternatively, retiring near St. Louis or Kansas City grants you access to major league sports, incredible museums, and world-class hospitals.

The Catch: Like many states in the Midwest, Missouri experiences extreme weather on both ends of the spectrum—freezing, icy winters and intensely humid summers. You must budget for high utility bills during peak seasonal months to keep your home comfortable.

What Can Go Wrong: The Hidden Costs of Relocation

Moving to one of the premier retirement savings states seems like a foolproof way to preserve your nest egg, but relocating purely based on a low cost of living index can backfire if you ignore the hidden variables.

- Soaring Homeowners Insurance: States with low property taxes often sit in regions vulnerable to natural disasters. The money you save on property taxes in Oklahoma or coastal Mississippi can easily be wiped out by massive spikes in homeowners and flood insurance premiums.

- Healthcare Networks and Out-of-Pocket Costs: Medicare operates differently depending on your zip code. If you rely on a Medicare Advantage plan, moving to a rural area in West Virginia or Arkansas might mean losing access to your preferred specialists. You can research regional plan availability and network limits directly through Medicare.gov before making a move.

- The Distance Penalty: Moving halfway across the country to save money on housing might result in a ballooning travel budget. If you find yourself flying back to your home state four times a year to see your grandchildren, those airline tickets and hotel stays will quickly eat into your cost-of-living savings.

- Homeowners Association (HOA) Fees: Many affordable housing developments in the South and Midwest offset low municipal taxes by shifting infrastructure costs to HOAs. A cheap house can become quite expensive if the monthly HOA fee is several hundred dollars.

“The single most important factor in determining your readiness for retirement is your ability to manage your spending.” — Jean Chatzky, Financial Editor and Author

When to Consult a Professional

Before packing up the moving truck, it pays to have an expert review your relocation plan. A professional can identify tax traps and insurance hurdles you might overlook. Seek guidance in the following scenarios:

- Consulting a Certified Public Accountant (CPA): Ask a CPA to run a mock tax return using your projected retirement income in your new target state. Because each state treats pensions, 401(k) withdrawals, and Social Security differently, a mock return reveals exactly how much you will owe. You can learn more about federal taxation of your benefits through the Social Security Administration.

- Working with a Fee-Only Fiduciary: A financial planner can stress-test your portfolio. They will help you understand if the equity from selling your current home will generate enough yield to cover your living expenses in the new state, factoring in regional inflation.

- Meeting with a Medicare Broker: If you are planning a long-distance move, a licensed Medicare insurance broker can explain how your healthcare coverage will transition. This is especially vital if you use Medicare Advantage (Part C) or a standalone Part D prescription drug plan, as these are entirely localized by county.

Frequently Asked Questions

Do the cheapest states to retire in also have the lowest taxes?

Not always. A state might boast zero income tax but make up for the lost revenue by implementing high property taxes, vehicle registration fees, or sales taxes on groceries. You must evaluate the total tax burden—including exactly how a state treats your specific type of retirement income—rather than looking at a single metric.

Does a low cost of living mean lower quality healthcare?

Affordability does not automatically equate to poor healthcare, but many low-cost states feature vast rural areas where access to specialized medical facilities is severely limited. To balance costs and health, look for affordable towns located within a 45-minute drive of regional hospitals or major medical hubs.

How do rising insurance premiums affect affordable retirement in the USA?

Homeowners and auto insurance premiums have surged in states prone to severe weather, such as tornadoes in Oklahoma or hurricanes in Mississippi. These rising insurance premiums can easily erase the financial benefits of cheap housing, making it vital to secure insurance quotes before purchasing property.

How can I compare the livability of different affordable states?

Beyond basic housing costs, you should evaluate community engagement, public transportation, and neighborhood safety. Organizations provide excellent tools to measure these factors; for example, you can explore community scoring through the AARP Livability Index to see how well a specific town supports older adults.

Planning Your Relocation

Protecting your savings requires strategic choices about where you live. The states highlighted above offer fantastic opportunities to lower your monthly expenses, allowing you to focus on enjoying your time rather than stressing over bills. Take the time to visit these states during their worst weather seasons, tour local grocery stores to check prices, and speak with local retirees about their lived experiences.

By conducting thorough research and testing out communities before you buy, you can secure a financially stable and deeply fulfilling retirement. This is educational content based on general retirement and financial principles. Individual results vary based on your situation. Always verify current benefit rules, tax laws, and eligibility requirements with official sources like SSA, Medicare.gov, or the IRS.

Last updated: May 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply