Shifting from saving to spending is a massive psychological hurdle, making every financial decision in retirement feel unusually weighty. The secret to a fulfilling post-career life lies in distinguishing the purchases that genuinely enhance your daily joy from those that quickly drain your hard-earned nest egg. New retirees frequently overspend on idealized visions of their future—think massive RVs or high-maintenance vacation properties—only to realize that simplicity offers far greater peace of mind. By directing your retirement budget toward experiences, daily conveniences, and health, you can confidently navigate this financial transition. Let’s explore the specific investments that consistently deliver lasting satisfaction and identify the temptations that typically lead to buyer’s remorse.

Navigating the Spending Shift in Retirement

For decades, your primary financial directive was accumulation. You maxed out your 401(k), paid down your mortgage, and ruthlessly cut unnecessary expenses to secure your future. Once that future arrives, flipping the switch from saver to spender feels unnatural. Many retirees experience “decumulation anxiety,” leading them to either hoard their savings out of fear or aggressively spend to make up for lost time.

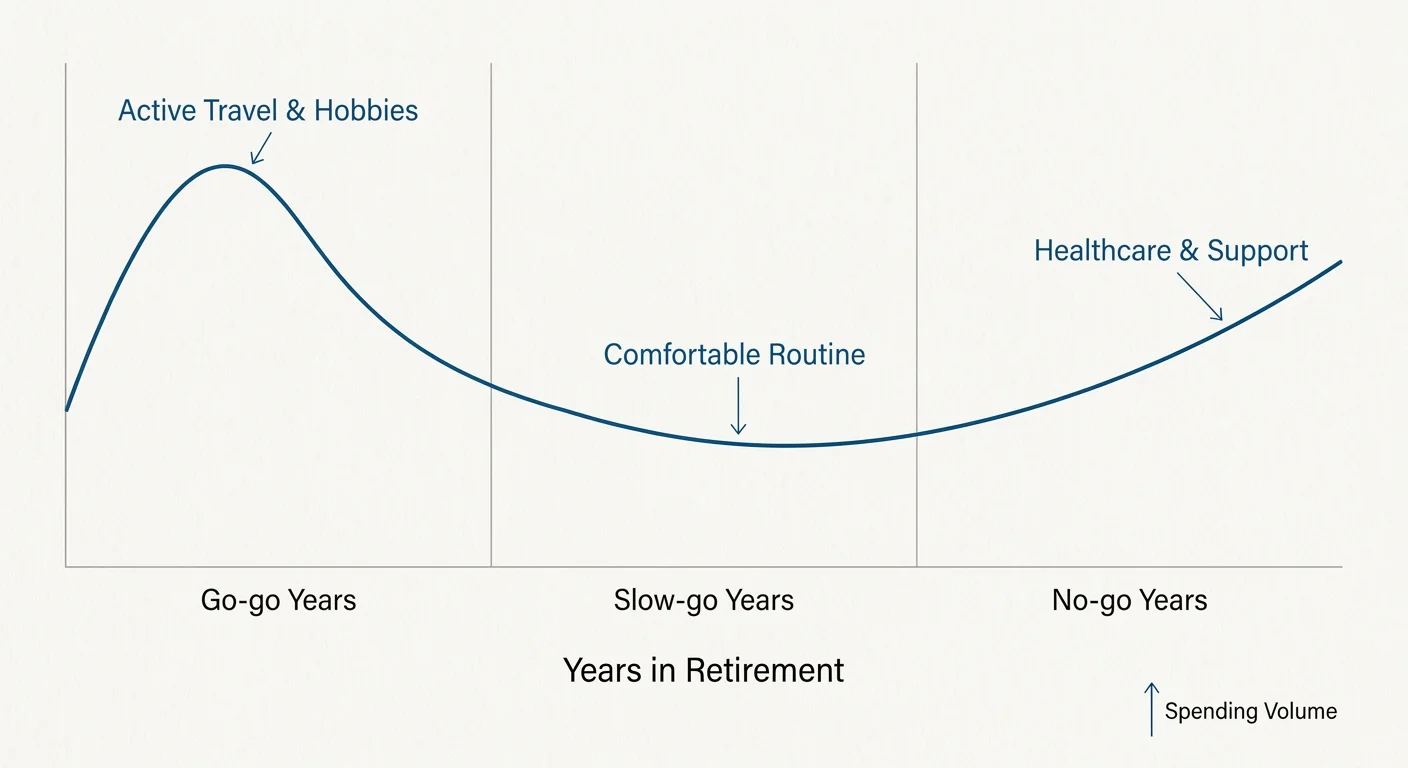

Financial planners often describe retirement spending as a “smile.” During the early, active years—affectionately called the go-go years—spending tends to be high as retirees travel, take up new hobbies, and tackle home projects. In the middle, slow-go years, spending dips significantly as life settles into a quiet, comfortable routine. Finally, in the no-go years, spending curves back up due to rising healthcare and assisted living costs.

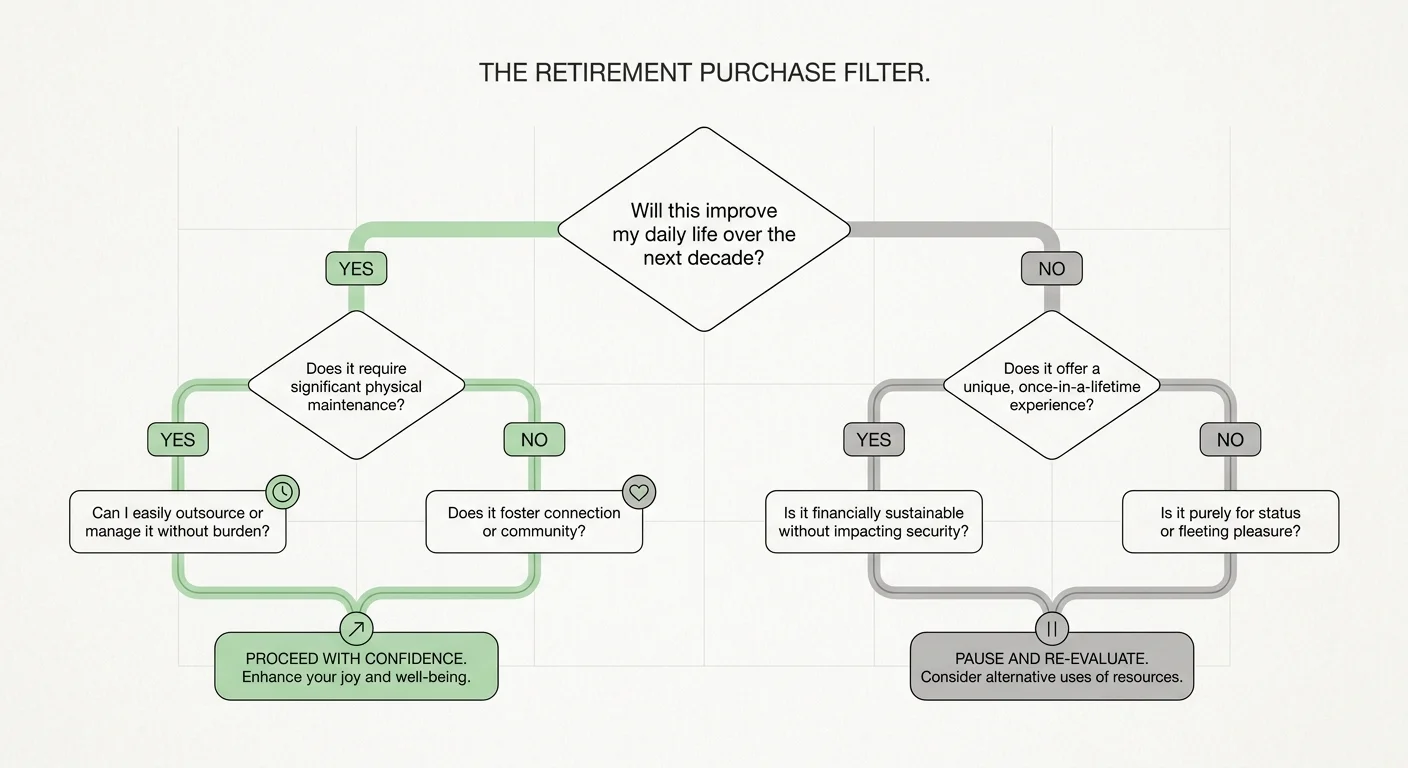

Understanding this trajectory helps clarify why certain purchases make sense while others become burdens. The most successful retirees view their money not as a score to keep, but as a tool to engineer a specific lifestyle. When evaluating a major purchase, the central question changes from “Can I afford this?” to “Will this noticeably improve my daily life over the next decade?”

“A big part of financial freedom is having your heart and mind free from worry about the what-ifs of life.” — Suze Orman, Personal Finance Expert

9 Retirement Purchases That Feel Worth It

The smartest ways to spend your retirement savings usually revolve around preserving your health, buying back your time, and fostering deep social connections. Here are nine categories where retirees rarely regret spending their money.

1. High-Quality Sleep Upgrades

You spend roughly a third of your life in bed, and as you age, the quality of your sleep directly impacts your cognitive function, immune system, and joint health. Investing in a premium mattress, adjustable bed frame, and high-quality cooling linens is one of the most immediate ways to improve your daily quality of life. An adjustable base can help alleviate acid reflux, reduce snoring, and ease lower back pain—issues that frequently interrupt a good night’s rest.

2. Outsourced Home Maintenance

There is no award for cleaning your own gutters at age 70. Paying for services that eliminate tedious, physically demanding, or dangerous chores allows you to redirect your energy toward things you actually enjoy. Hiring a reliable lawn care service, a bi-weekly house cleaner, or a handyman for seasonal maintenance protects you from common household injuries while giving you back hours of free time every week.

3. Preventative Health and Mobility Aids

Spending money to maintain your physical independence is always a sound investment. This might mean paying out-of-pocket for regular sessions with a physical therapist, hiring a personal trainer who specializes in senior fitness, or purchasing customized orthotic footwear. According to the National Council on Aging (NCOA), falls are the leading cause of fatal and non-fatal injuries for older Americans. Investing in supportive shoes instead of flimsy slippers can literally save your life.

4. Home Modifications for Aging in Place

Most retirees want to stay in their own homes for as long as possible. Funding modifications before a health crisis forces your hand is a brilliant use of your retirement budget. Installing a walk-in shower, upgrading to comfort-height toilets, adding discrete grab bars, and replacing difficult doorknobs with lever handles creates a safer environment that extends your ability to live independently.

5. Meaningful Experiences and Travel

Material goods depreciate, but memories appreciate. Budgeting for travel, whether it means taking the grandchildren to a national park or finally booking that river cruise through Europe, consistently ranks high on retiree satisfaction surveys. Rather than flying first class or staying in luxury resorts, many retirees find the most joy in extended, slow-paced travel—renting a modest apartment in a new city for a month to experience life like a local.

6. Reliable, Low-Maintenance Transportation

Dealing with frequent car repairs is stressful and unpredictable. Trading in an older, unreliable vehicle for a newer model equipped with modern safety features—like blind-spot monitoring, lane-assist, and automatic emergency braking—provides immense peace of mind. A practical, comfortable vehicle that gets you safely to appointments and social engagements is worth the expenditure.

7. Premium Technology That Keeps You Connected

Upgrading your smartphone, tablet, or home computer is no longer a luxury; it is a vital tool for managing your life. High-quality technology allows you to easily navigate telehealth appointments, manage your investment portfolios, and video chat with family members across the country. Paying a little extra for a device with a larger, brighter screen and an intuitive interface prevents daily frustration.

8. Professional Financial and Tax Advice

Navigating the transition from earning an income to drawing down assets is incredibly complex. Paying a fee-only fiduciary to build a tax-efficient withdrawal strategy, optimize your Social Security claiming strategy, and manage your required minimum distributions (RMDs) often saves you far more than it costs. Resources like Investopedia frequently highlight how strategic tax planning in retirement can add years of longevity to your portfolio.

9. “Warm Giving” to Family and Causes

If your retirement is fully funded and secure, giving money to your children, grandchildren, or favorite charities while you are still alive—often called “warm giving”—brings tremendous joy. Watching your grandson use your gift to buy his first home, or seeing a local charity utilize your donation, offers an emotional return on investment that leaving a massive inheritance behind simply cannot match.

7 Purchases Retirees Frequently Regret

On the flip side, some purchases sound like the ultimate retirement dream but quickly transform into financial nightmares. Avoiding these common traps can protect hundreds of thousands of dollars.

1. The Massive RV or Motorhome

The vision of selling everything and driving a luxury land yacht across the country is enticing. The reality often involves navigating stressful traffic in a vehicle the size of a city bus, paying exorbitant fuel costs, and dealing with constant, expensive repairs. A new luxury RV depreciates faster than almost any other asset. Retirees often find that renting an RV for a few weeks a year satisfies the itch without the massive capital commitment and ongoing storage fees.

2. Timeshares

Timeshares are notoriously easy to buy and nearly impossible to sell. While the upfront presentation makes it sound like a guaranteed annual vacation, the reality is far darker. Maintenance fees inevitably rise year after year, blackout dates make booking difficult, and the resale market is virtually nonexistent. You are almost always better off simply booking hotels or short-term rentals wherever you wish to travel.

3. The Over-Sized “Dream” Retirement Home

Many retirees decide to build or buy a sprawling house, imagining it will become the ultimate hub for family holidays. In practice, the children and grandchildren only visit a few times a year. For the remaining 340 days, you are left paying higher property taxes, astronomical utility bills, and increased maintenance costs for empty bedrooms. Downsizing to a comfortable, manageable space frees up cash flow for daily enjoyment.

4. Complex, High-Fee Annuities

While simple single-premium immediate annuities (SPIAs) can provide a solid baseline of guaranteed income, the financial industry aggressively pushes complex variable or indexed annuities. These products often come with steep surrender charges, high internal fees, and confusing payout structures that limit your access to your own money. Never buy an investment product you cannot easily explain to a friend in three sentences.

5. A Boat

There is an old joke that the two happiest days of a boat owner’s life are the day they buy the boat and the day they sell it. Unless you have a lifelong history of boating and marine maintenance, purchasing a boat in retirement is a reliable way to drain your savings. Between docking fees, winterizing, insurance, and routine mechanical failures, the cost-per-use is staggeringly high.

6. Funding Adult Children’s Lifestyles

Helping your children in an emergency is one thing; subsidizing their lifestyle to the detriment of your own financial security is another. Paying off a child’s massive credit card debt, co-signing their mortgage, or continually bailing them out prevents them from learning financial independence while actively jeopardizing your ability to pay for future healthcare needs. You can borrow for almost anything in life, but you cannot borrow for your retirement.

7. Unnecessary Life Insurance Policies

Life insurance is designed to replace lost income if you pass away unexpectedly while dependents are relying on your paycheck. Once you are retired, your children are grown, and you have built sufficient assets to cover your spouse’s living expenses, carrying an expensive whole-life policy often makes little mathematical sense. Many retirees blindly continue paying hefty premiums out of habit rather than necessity.

Evaluating a Retirement Purchase: Needs vs. Wants

When considering a major outlay of cash, it helps to pause and compare the idealized fantasy of the purchase against the practical reality of owning it. Use this framework before liquidating investments for a big-ticket item.

| Purchase Category | The Idealized Fantasy | The Practical Reality | The Better Alternative |

|---|---|---|---|

| Luxury RV | Spontaneous, carefree travel across the country, waking up to mountain views. | High fuel costs, stressful driving, constant repairs, and expensive storage fees. | Rent an RV for a two-week trip, or book comfortable Airbnbs along your route. |

| Vacation Home | A permanent family getaway where everyone gathers for every holiday. | Paying double property taxes, managing two sets of repairs, and feeling guilty if you travel elsewhere. | Rent a large, high-end house in different locations for annual family reunions. |

| High-End Sports Car | Cruising coastal highways, reclaiming a sense of youthful freedom. | Stiff suspension hurts your back, expensive insurance, and fear of parking it anywhere public. | Rent a premium convertible for a special weekend trip. Buy a reliable, comfortable daily driver. |

| Timeshare | Guaranteed luxury vacations at exotic resorts for life. | Rapidly escalating maintenance fees and zero secondary market resale value. | Invest the upfront cost; use the dividends to pay for standard hotel bookings. |

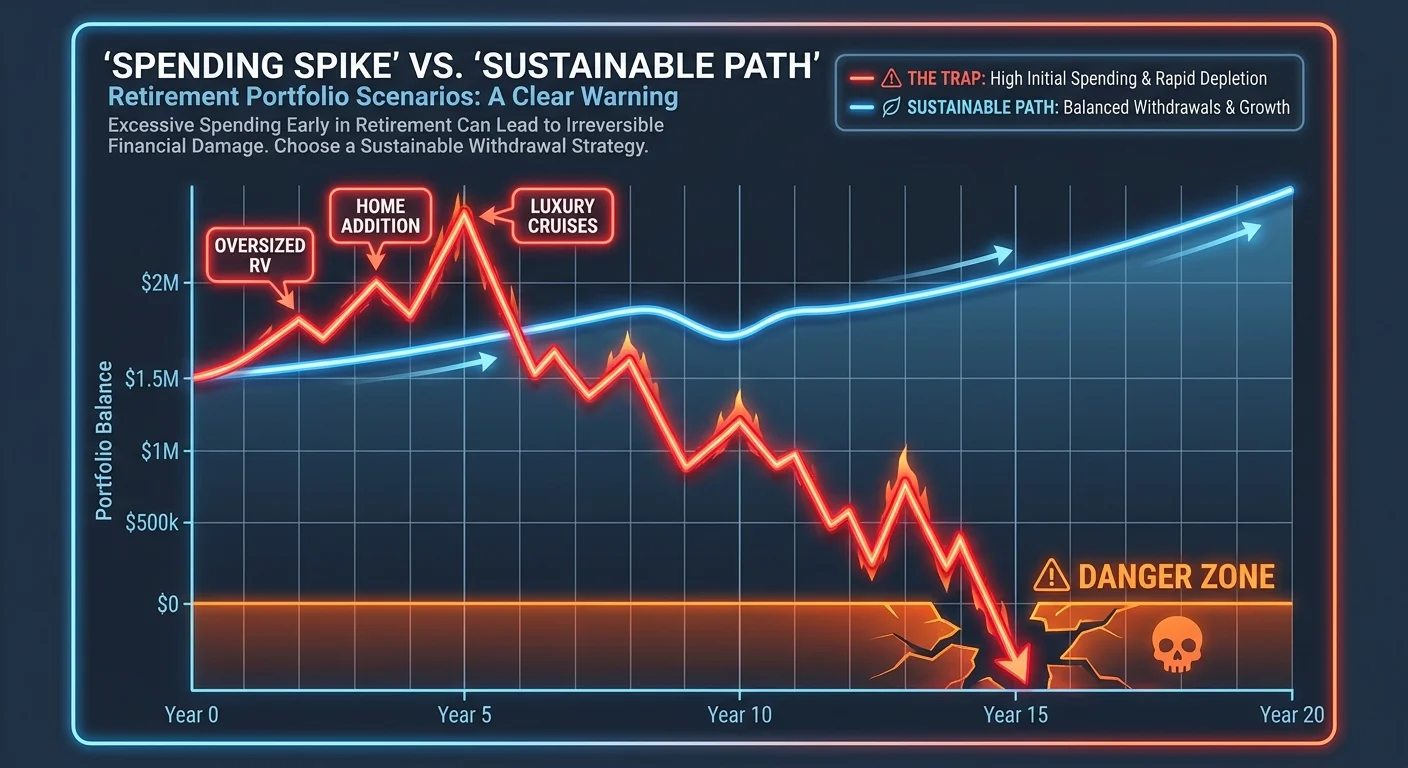

What Can Go Wrong: The “Go-Go” Years Spending Trap

The most common financial mistake new retirees make occurs in the first 24 to 36 months of retirement. Suddenly unshackled from a 40-hour workweek, every day feels like a Saturday. This newly found freedom often triggers the “honeymoon phase” of retirement spending.

Without the structure of a workday, retirees might find themselves eating out for lunch daily, impulsively booking trips, and buying expensive equipment for hobbies they haven’t fully committed to. While you absolutely should enjoy your early retirement, spending at an unsustainable rate during these crucial first few years can severely damage your portfolio through a phenomenon known as sequence of returns risk. If you are withdrawing heavily while the stock market happens to be in a downturn, your portfolio may never recover, severely limiting your options later in life.

To avoid this trap, track your spending meticulously during your first year. Treat your initial withdrawal rate as a trial run, making adjustments as you discover what your new, unstructured life actually costs.

Frequently Asked Questions

How much of my retirement budget should go toward “fun” or discretionary spending?

A common guideline is the 50/30/20 rule adapted for retirees: 50% for essential needs (housing, groceries, Medicare premiums), 30% for discretionary wants (travel, dining out, hobbies), and 20% reserved for future healthcare costs or legacy planning. If your fixed expenses are low—for instance, if your mortgage is fully paid off—you may safely allocate a larger percentage to travel and experiences.

Is it financially smart to downsize my home immediately after retiring?

Downsizing can dramatically reduce your property taxes, utility bills, and maintenance expenses, freeing up cash for your lifestyle. However, it is usually wise to wait six to twelve months after you retire before making a major real estate move. This buffer gives you time to understand how you actually spend your days and ensures you don’t move away from a social network you rely on more than you realized.

How do I gracefully say no when adult children ask for financial help?

Transparency is your best tool. Explain that your retirement funds are fixed and that preserving your own financial independence is the greatest gift you can give them, as it ensures you will never become a financial burden on them in your later years. Offer non-financial support, such as babysitting grandchildren or offering advice, but remain firm on protecting your core retirement assets.

Making Your Money Work for Your Life

Your retirement savings represent decades of sacrifice, discipline, and hard work. Now that you have crossed the finish line of your career, you have earned the right to spend that money in ways that bring you genuine comfort and joy. Focus on purchasing time, ease, and health, and boldly ignore societal pressures to buy flashy, depreciating assets that only add stress to your life.

Take an afternoon to review your current spending patterns. Identify one recurring expense that brings you no joy and redirect those funds toward something that makes your daily routine noticeably better—whether that means hiring a house cleaner, upgrading your mattress, or setting aside a dedicated travel fund.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, health needs, tax situation, and goals—may require different approaches. When in doubt, consult a licensed professional.

Last updated: May 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply