Your monthly Social Security deposit and pension payments only represent a fraction of the total economic support available during your post-work years. Thousands of dollars in localized property tax freezes, federal utility subsidies, and targeted healthcare grants sit unclaimed because retirees simply do not know where to look. By digging beyond the obvious income streams, you can uncover substantial retirement benefits that lower your baseline living expenses and stretch your fixed income much further. Finding these hidden resources requires knowing which local, state, and federal agencies distribute them. This guide unpacks exactly where to find senior assistance, government programs, and valuable retiree perks that protect your cash flow and preserve your nest egg.

Defeating High Medical Costs With Targeted Assistance

Healthcare easily ranks as the most significant expense you will face after leaving the workforce. Even with traditional Medicare coverage, premiums, deductibles, and prescription copayments quickly drain a fixed income. Fortunately, the government operates several interlocking safety nets designed specifically to absorb these costs for eligible seniors.

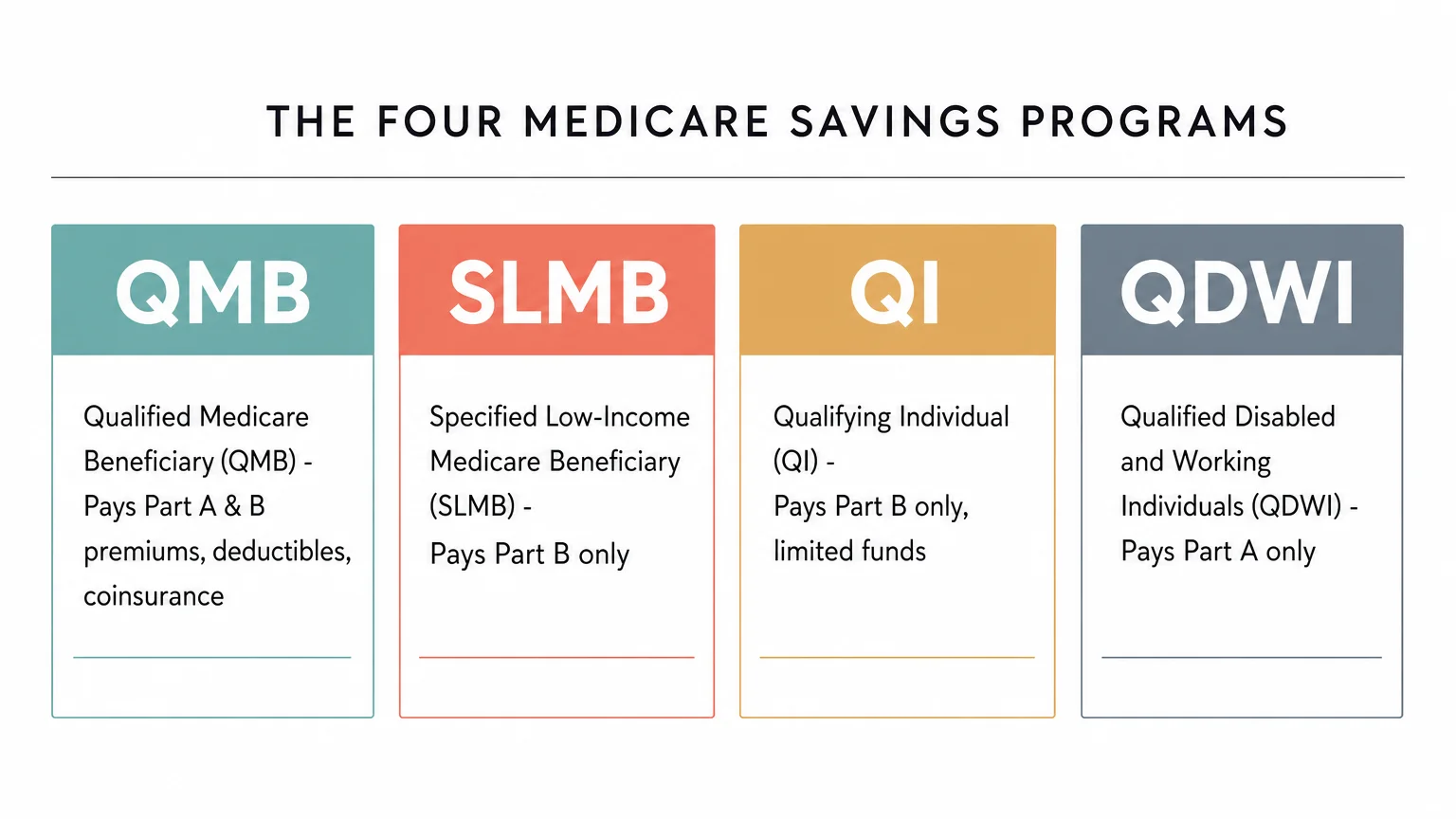

The Medicare Savings Programs (MSPs) exist to help beneficiaries cover their baseline Medicare costs. State governments administer these federal programs, meaning income and asset limits vary depending on your location. Many retirees incorrectly assume they earn too much to qualify. However, certain states have eliminated the asset test entirely, looking only at your monthly income. When you qualify for an MSP, the state pays your Part B premium—instantly adding over $2,000 back into your annual budget.

There are four distinct types of Medicare Savings Programs, each offering different levels of financial relief based on your income bracket:

| Program Name | What It Covers | General Target Audience |

|---|---|---|

| Qualified Medicare Beneficiary (QMB) | Pays Part A premiums, Part B premiums, deductibles, coinsurance, and copayments. | Retirees with income at or below the federal poverty level. |

| Specified Low-Income Medicare Beneficiary (SLMB) | Pays Part B premiums only. | Retirees with income slightly above the federal poverty level. |

| Qualifying Individual (QI) | Pays Part B premiums only (funds are limited and granted on a first-come, first-served basis). | Retirees with income up to 135% of the federal poverty level. |

| Qualified Disabled and Working Individuals (QDWI) | Pays Part A premiums only. | Working disabled individuals under age 65 who lost premium-free Part A. |

If you secure approval for any MSP, you automatically qualify for the federal Extra Help program. Administered by the Social Security Administration, Extra Help specifically targets the exorbitant cost of prescription drugs under Medicare Part D. The program covers your Part D monthly premiums, annual deductibles, and significantly limits your out-of-pocket copayments at the pharmacy counter. Even if you do not qualify for a Medicare Savings Program, you can apply for Extra Help directly through the Social Security Administration.

Beyond federal support, investigate State Pharmaceutical Assistance Programs (SPAPs). Approximately half of all U.S. states fund their own prescription assistance initiatives. These programs wrap around your existing Medicare Part D coverage to pay for medications during coverage gaps or cover specific drugs that federal plans exclude.

Unlocking Property Tax Relief and Home Modification Grants

Remaining in your own home provides stability and comfort, but escalating property taxes can force you into difficult financial corners. Local governments rely heavily on property taxes to fund schools and infrastructure; however, municipalities also recognize that seniors on fixed incomes cannot absorb continuous tax hikes. This reality birthed a variety of property tax relief mechanisms tailored for older homeowners.

Homestead exemptions serve as the first line of defense. While standard homestead exemptions apply to most primary residences, the majority of states offer an enhanced exemption specifically for homeowners aged 65 and older. This enhanced status further reduces the assessed value of your property, directly lowering your annual tax bill. You must proactively apply for this reduction through your county tax assessor’s office—it rarely activates automatically on your 65th birthday.

Property tax freezes take this relief a step further. Under a senior freeze program, the assessed value of your home or the actual tax rate locks into place the year you qualify. While your neighbors watch their tax bills climb alongside rising real estate markets, your obligation remains tethered to a previous, lower baseline. Some municipalities utilize a “circuit breaker” model instead, which refunds a portion of your property taxes through a state income tax credit if your tax bill exceeds a certain percentage of your total income.

Beyond tax relief, the physical maintenance of your home often requires financial support. The federal government funds home modification initiatives through the Department of Housing and Urban Development (HUD) and the Administration for Community Living. These retirement resources provide direct grants to install wheelchair ramps, widen doorways, upgrade lighting, and retrofit bathrooms with grab bars and walk-in showers. Because these are grants rather than loans, you never have to repay the funds, allowing you to age safely in place without draining your savings.

Navigating Utility Subsidies and Weatherization Programs

Keeping your home heated in the winter and cooled in the summer requires immense energy output. Utility expenses function as a hidden tax on retirees, fluctuating wildly with seasonal weather patterns and global energy markets. Federal and localized government programs step in to stabilize these essential costs.

The Low Income Home Energy Assistance Program (LIHEAP) stands as the primary federal mechanism for utility relief. Distributed through state and county agencies, LIHEAP provides direct financial grants paid directly to your utility providers. The program prioritizes vulnerable populations, specifically targeting households containing individuals aged 60 and older. Depending on your state’s funding allocation and your specific financial situation, LIHEAP can cover heating oil, natural gas, electricity, and even emergency HVAC repairs during extreme weather events.

While LIHEAP addresses immediate bills, the Weatherization Assistance Program (WAP) provides long-term energy efficiency upgrades. Authorized energy auditors visit your home to identify exactly where you lose heat or cooled air. The program then funds permanent structural improvements to lower your baseline energy consumption.

- Attic and Wall Insulation: Contractors add high-grade insulation to trap conditioned air inside your living space.

- Air Sealing: Technicians caulk and weatherstrip drafty windows, doors, and foundational gaps.

- System Upgrades: Aging, inefficient furnaces, boilers, and water heaters are repaired or replaced entirely with high-efficiency models.

- Health and Safety Measures: The program includes carbon monoxide testing and the installation of smoke detectors to ensure your indoor environment remains safe.

Telecommunications also represent a vital utility. The federal Lifeline program subsidizes monthly telephone and broadband internet service for low-income consumers. Staying connected to healthcare providers, family members, and emergency services is non-negotiable; securing a subsidized phone plan ensures you never have to choose between communication and groceries.

Maximizing Nutritional Support Through Specialized Programs

Proper nutrition dictates how well you age, how your body metabolizes medications, and how effectively your immune system wards off illness. Unfortunately, food inflation heavily impacts fixed-income households, forcing many seniors to trade fresh produce for highly processed, cheaper alternatives. Recognizing this public health issue, the government created robust nutritional safety nets specifically for older adults.

The Supplemental Nutrition Assistance Program (SNAP) remains the most powerful tool for combating food insecurity, yet it is historically underutilized by the senior population. Many retirees assume the application process is overly complex or that the benefits will only amount to a few dollars a month. This misconception stems from a failure to understand the “excess medical expense deduction.”

When applying for SNAP, seniors and individuals with disabilities can deduct out-of-pocket medical expenses that exceed $35 per month from their gross income calculation. This includes Medicare premiums, prescription copays, transportation to medical appointments, over-the-counter health supplies, and even the cost of a service animal. By thoroughly documenting these medical costs, your countable income drops significantly, often qualifying you for a substantial monthly grocery stipend.

In addition to SNAP, the Senior Farmers’ Market Nutrition Program (SFMNP) provides low-income seniors with specialized coupons that can be exchanged for eligible foods at farmers’ markets, roadside stands, and community-supported agriculture programs. This initiative serves a dual purpose: it injects fresh, locally grown fruits, vegetables, honey, and herbs directly into your diet while simultaneously supporting local agricultural producers in your region.

For those who struggle with mobility or the physical demands of cooking, local Area Agencies on Aging coordinate the delivery of pre-prepared meals. Congregate meal programs serve hot lunches in community centers and senior living facilities, offering vital social interaction alongside nutrition. If you cannot leave your home, programs like Meals on Wheels deliver fresh, nutritionally balanced food directly to your doorstep, accompanied by a brief wellness check from the delivery volunteer.

Claiming Specialized Allowances for Veterans and Surviving Spouses

If you or your spouse served in the United States military, your retirement planning must include an exploration of Department of Veterans Affairs (VA) benefits. Veterans often overlook these programs, assuming they only apply to those who suffered combat-related injuries or retired after twenty years of service. In reality, the VA offers significant financial support for aging veterans dealing with the natural decline of their health.

The VA Pension serves as a foundational benefit for wartime veterans. To qualify, you must meet specific service duration requirements—typically including at least one day of active duty during an official wartime period—and fall below designated income and net worth limits. If approved, the VA provides a tax-free monthly payment to supplement your retirement income.

Within the VA Pension framework exists a highly valuable, yet frequently missed benefit known as Aid and Attendance (A&A). This enhanced pension provides substantial additional funding if you require the regular assistance of another person to perform activities of daily living. You do not need a service-connected disability to qualify for A&A the medical need can stem entirely from aging, such as severe arthritis, vision loss, or cognitive decline.

To qualify for Aid and Attendance, you must meet the basic pension requirements and satisfy at least one of the following clinical criteria:

- You require assistance with fundamental tasks like bathing, feeding yourself, dressing, or navigating your home safely.

- You are bedridden—meaning your medical condition requires you to remain in bed apart from prescribed treatments or therapies.

- You currently reside in a nursing home facility due to the loss of mental or physical abilities.

- Your eyesight is severely limited, even with corrective lenses.

Surviving spouses of wartime veterans may also qualify for Survivors Pension and their own tier of Aid and Attendance benefits. The funds provided by these programs can be used to pay for in-home caregivers, assisted living facility rent, or specialized memory care, offering extraordinary relief to families struggling with long-term care costs.

Taking Advantage of Education Waivers and Travel Discounts

Retirement affords you the time to pursue passions and explore the world—activities that often carry hefty price tags. State legislatures and federal agencies offer unique perks that heavily discount the cost of lifelong learning and domestic travel.

Nearly all fifty states have legislation in place that waives tuition for senior citizens attending public colleges and state universities. The specifics vary by institution: some universities allow you to audit classes completely free of charge, giving you access to the lectures and course materials without the pressure of exams or graded papers. Other state systems offer deeply discounted tuition if you wish to pursue a formal degree and earn collegiate credits. Expanding your knowledge through these university programs keeps your mind sharp and integrates you into a diverse, multigenerational academic community.

When it comes to travel, the federal government offers one of the most cost-effective recreation benefits in existence: the America the Beautiful Senior Pass. Available to U.S. citizens or permanent residents aged 62 or older, this pass grants lifetime access to more than 2,000 federal recreation sites across the country, including all National Parks, National Wildlife Refuges, and lands managed by the Bureau of Land Management and the U.S. Forest Service.

The lifetime pass requires a singular, minimal upfront fee, replacing the need to pay individual entrance fees or day-use fees at national monuments and historic sites. Furthermore, the pass often provides a 50% discount on expanded amenity fees at these locations, such as overnight camping, swimming, boat launching, and specialized guided tours. For retirees who plan to utilize an RV or execute cross-country road trips, this single benefit yields immense financial value year after year.

Common Mistakes to Avoid When Claiming Senior Assistance

The landscape of retirement benefits contains strict eligibility rules and complex application procedures. Navigating these systems requires precision; a single misinterpretation of the guidelines can lead to a rejected application or a sudden loss of critical support.

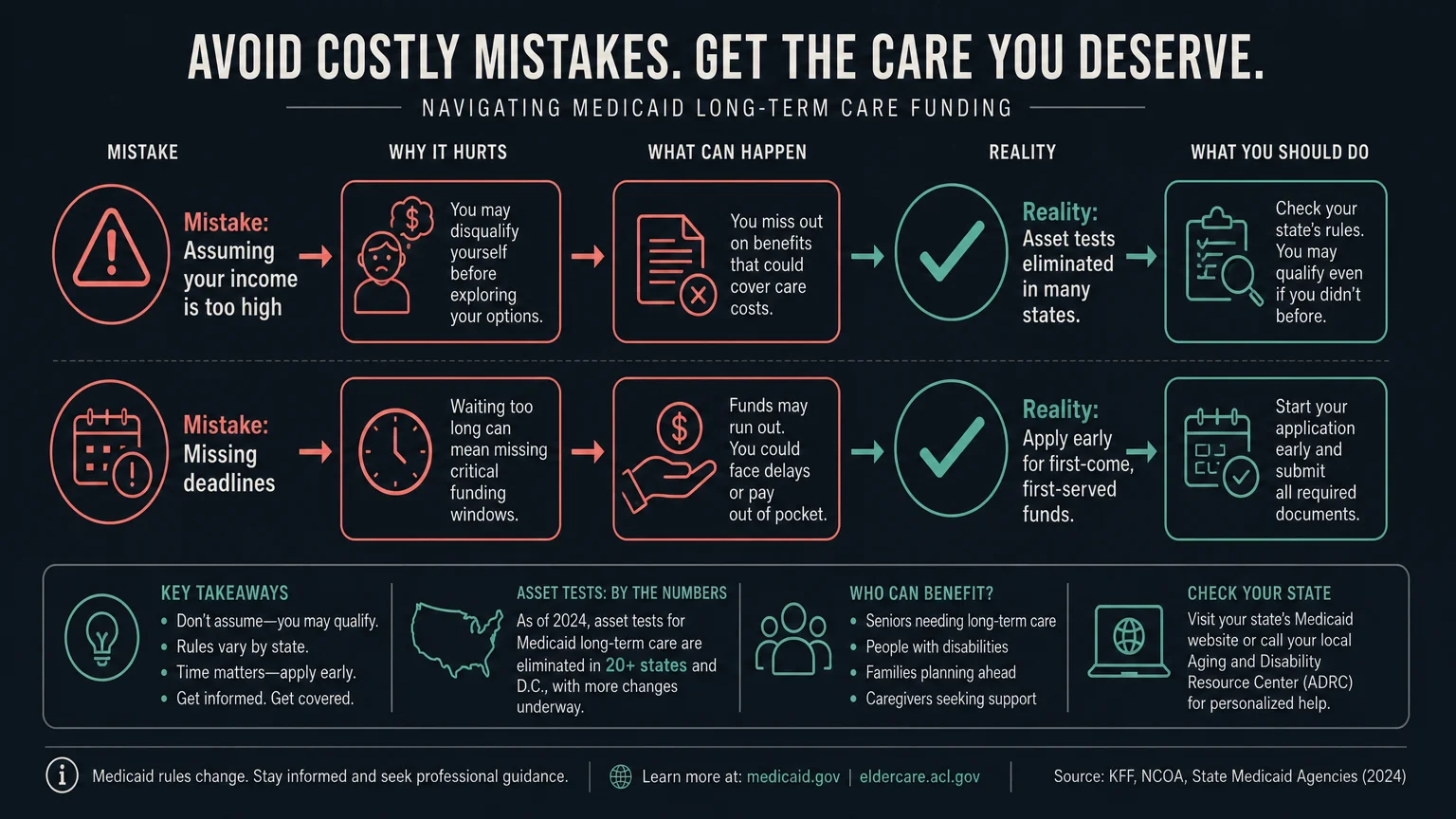

Failing to account for gross versus net income: When assessing your eligibility, federal and state agencies typically look at your gross income—the amount you earn before Medicare premiums, taxes, and other deductions are subtracted. Retirees frequently review their monthly bank deposits (net income) and incorrectly assume they fall under the income limits. Always base your calculations on the gross figures listed on your annual Social Security award letter and pension statements.

Misunderstanding asset limits: Many assistance programs require an evaluation of your financial resources. A common mistake involves assuming all property counts against you. In reality, the vast majority of government programs exempt your primary residence, the land it sits on, your personal belongings, and one vehicle used for primary transportation. Never disqualify yourself without reading the specific exemptions for the program you wish to join.

Missing critical enrollment periods: Certain benefits, particularly those tied to healthcare and Medicare, operate on strict annual calendars. If you fail to submit documentation during the designated open enrollment windows, you may face substantial lock-out periods or permanent financial penalties. Set calendar reminders for the fourth quarter of every year to review your prescription coverage and re-certify your state-level assistance plans.

Neglecting local Area Agencies on Aging: Far too many seniors attempt to navigate the federal bureaucracy alone. Every county in the United States operates under the umbrella of an Area Agency on Aging (AAA). These federally mandated, locally operated organizations employ staff specifically trained to identify and secure benefits for residents in their immediate jurisdiction. Bypassing their free expertise usually results in overlooked localized grants.

Professional vs. Self-Guided: Securing Your Additional Benefits

Once you identify the retirement benefits you wish to pursue, you must decide how to execute the application process. You can manage this entirely on your own, or you can leverage professional advocates to streamline the paperwork and ensure accuracy.

The Self-Guided Approach: If your financial situation is straightforward—comprising standard Social Security benefits, a modest bank account, and a primary residence—you can effectively manage the application process yourself. The National Council on Aging operates a free, confidential online screening tool called BenefitsCheckUp. By answering a series of anonymous questions about your location, age, income, and expenses, the system instantly generates a comprehensive report of every local, state, and federal program you likely qualify for, complete with direct links to the official applications.

Using State Health Insurance Assistance Programs (SHIP): When dealing specifically with Medicare Savings Programs and Extra Help, utilize your local SHIP counselors. These state-funded professionals provide free, unbiased, one-on-one counseling. They do not sell insurance products; their sole mandate involves helping you understand your Medicare options and securing the healthcare subsidies you deserve.

Hiring an Elder Law Attorney: If your net worth borders the upper limits of program thresholds, or if you manage complex assets like multiple properties, family trusts, or business holdings, self-guided applications pose a severe risk. You should consult a licensed elder law attorney. These legal professionals specialize in structuring your assets in ways that comply with state and federal laws while maximizing your eligibility for programs like Medicaid and VA Aid and Attendance. The upfront cost of legal counsel often pays for itself by legally shielding your life savings from aggressive nursing home costs or prolonged medical emergencies.

“A big part of financial freedom is having your heart and mind free from worry about the what-ifs of life.” — Suze Orman, Personal Finance Expert

Frequently Asked Questions About Non-Cash Retirement Benefits

Do these specialized assistance programs reduce my monthly Social Security check?

No. Social Security functions as an earned benefit based on your lifetime tax contributions. Qualifying for utility assistance, food subsidies, or property tax relief will never cause the Social Security Administration to reduce your monthly retirement benefit. These programs exist alongside your standard income to lower your outgoing expenses.

How often must I prove my eligibility for these government programs?

Most localized and federal assistance programs require an annual recertification process. Because your income can fluctuate due to cost-of-living adjustments (COLA) or changes in your medical expenses, agencies must verify that you still meet the foundational requirements. You will typically receive a recertification packet in the mail thirty to sixty days before your benefit year expires.

Are utility subsidies, healthcare grants, and food assistance considered taxable income by the IRS?

Generally, government-provided welfare benefits based strictly on financial need are not considered taxable income. Funds paid directly to your utility company, subsidies for your Medicare premiums, and SNAP benefits do not need to be reported as income on your federal tax return. However, always consult a tax professional regarding complex localized grants or property tax credits.

Can I receive VA Aid and Attendance at the same time as Medicaid?

Navigating dual eligibility between VA benefits and state Medicaid requires careful planning. While you can technically receive both, VA pension payments generally count as income when calculating your Medicaid eligibility. If Medicaid pays for your nursing home care, the VA will typically reduce your pension payment to a minimal monthly allowance. An elder law attorney can help you determine the most advantageous way to utilize both systems without inadvertently violating the income caps of either program.

Take immediate action by gathering your recent tax returns, medical receipts, and utility bills, and scheduling an appointment with your local Area Agency on Aging. The funds for these retirement resources exist entirely to support you—leaving them unclaimed only forces you to pull heavier withdrawals from your hard-earned savings.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, health needs, tax situation, and goals—may require different approaches. When in doubt, consult a licensed professional.

Last updated: March 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply