Transitioning from decades of aggressively saving money to systematically spending it is one of the most psychologically demanding phases of your financial life. You have built a nest egg across various accounts, but pulling money out blindly can trigger massive tax bills and drain your portfolio years ahead of schedule. Your retirement withdrawal strategy—specifically the order in which you tap taxable, tax-deferred, and tax-free accounts—dictates how much of your wealth goes to the IRS and how much stays in your pocket. A thoughtful approach preserves your capital, maximizes compound growth, and keeps your Medicare premiums in check. By strategically structuring your retirement income planning, you can ensure your savings last throughout your golden years while minimizing unnecessary financial friction.

The Conventional Wisdom: A Baseline for Your Strategy

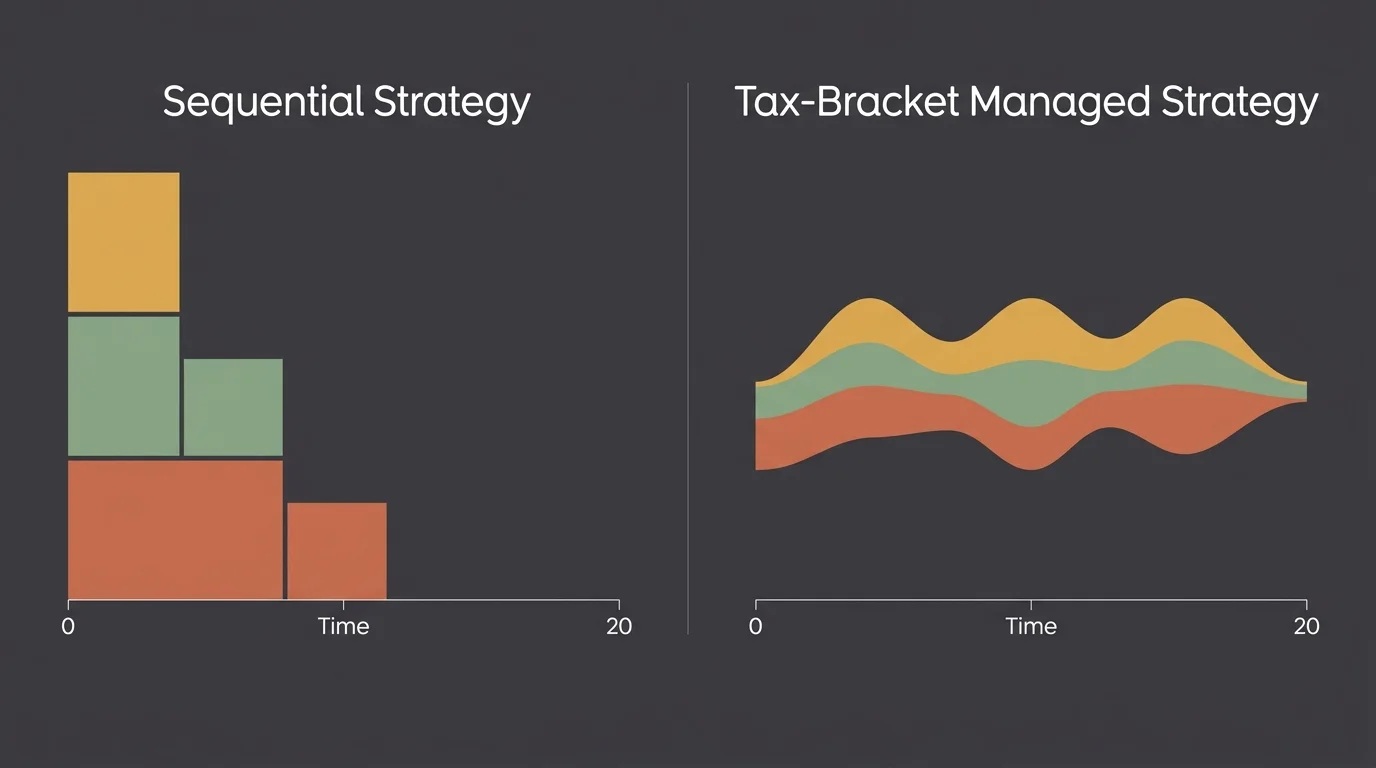

Financial planners have historically relied on a straightforward rule of thumb for retirement withdrawals: drain your taxable accounts first, move on to your tax-deferred accounts second, and leave your tax-free accounts for last. This sequential strategy aims to maximize the tax-advantaged growth of your retirement funds for as long as possible.

The logic behind this conventional approach is mathematically sound in a vacuum. By leaving your tax-advantaged accounts untouched, you allow compound interest to work its magic without the drag of annual taxes. However, relying strictly on this sequential method can sometimes lead to unintended consequences later in retirement. Before exploring the alternatives, you must understand exactly how the sequential strategy works and why financial professionals have recommended it for decades.

Step 1: Drain Taxable Accounts First

Taxable accounts include your standard brokerage accounts, high-yield savings accounts, certificates of deposit (CDs), and regular checking accounts. These accounts offer no special tax shelter. You pay taxes on interest, dividends, and realized capital gains every single year, regardless of whether you withdraw the money or reinvest it.

Because these accounts suffer from “tax drag”—the constant chipping away of returns due to annual taxation—they represent the most efficient place to start funding your retirement lifestyle. Furthermore, when you sell investments in a taxable brokerage account that you have held for longer than a year, you benefit from long-term capital gains tax rates. These rates are generally much more favorable than ordinary income tax rates, often falling at 0%, 15%, or 20%, depending on your total taxable income.

By spending down these accounts first, you eliminate the annual tax drag early in your retirement and allow your sheltered accounts to continue growing uninterrupted.

Step 2: Transition to Tax-Deferred Accounts

Once you deplete your taxable accounts, the conventional strategy dictates that you move to your tax-deferred accounts. These include traditional IRAs, 401(k)s, 403(b)s, and 457 plans. You funded these accounts with pre-tax dollars, meaning you received a tax break during your working years.

The IRS requires you to pay ordinary income tax on every dollar you withdraw from these accounts. Because ordinary income tax brackets are generally higher than long-term capital gains rates, tapping these accounts represents a larger financial penalty. However, you cannot avoid these taxes forever. The government mandates that you begin taking Required Minimum Distributions (RMDs) from these accounts once you reach a certain age—currently 73, pushing to 75 in 2033 under recent legislative changes.

Step 3: Preserve Tax-Free Accounts for Last

Your tax-free accounts—primarily Roth IRAs and Roth 401(k)s—serve as the holy grail of your retirement income planning. You funded these accounts with after-tax dollars, meaning the IRS has already taken its cut. All future growth and qualified withdrawals remain completely tax-free.

The conventional strategy saves these accounts for last because they offer the most powerful wealth-building environment. The longer you leave money in a Roth IRA, the more tax-free compounding you achieve. Additionally, Roth IRAs do not carry Required Minimum Distributions during your lifetime, giving you ultimate control over when and how you use the funds. Many retirees reserve their Roth funds for large, unexpected expenses late in life, such as long-term care, or pass them on to their heirs as a tax-free inheritance.

Why the Sequential Strategy Might Fail You

While the conventional strategy provides a solid foundation, following it rigidly can trap you in a massive tax predicament later in retirement. If you spend your early retirement years strictly draining your taxable accounts, your taxable income might appear artificially low. Meanwhile, your untouched traditional IRAs and 401(k)s continue to grow.

By the time you reach your 70s, those tax-deferred accounts may have doubled in size. When the government finally forces you to take Required Minimum Distributions, the mandatory withdrawals could be enormous. These large RMDs will stack on top of your Social Security benefits, potentially pushing you into a much higher tax bracket than you experienced during your working years.

“In this world nothing can be said to be certain, except death and taxes.” — Benjamin Franklin

Furthermore, large RMDs trigger a domino effect across your financial life. They can cause a larger percentage of your Social Security benefits to become taxable. More importantly, they can trigger Medicare IRMAA (Income-Related Monthly Adjustment Amount) surcharges, which drastically increase your monthly Medicare Part B and Part D premiums. A rigid adherence to the sequential withdrawal strategy often creates a “tax bomb” in your 70s and 80s.

The Tax Bracket Management Strategy: A Smarter Approach

Instead of draining one account type completely before moving to the next, modern retirement withdrawal strategy favors a blended approach known as Tax Bracket Management. This strategy treats the IRS tax brackets as literal buckets that you want to fill strategically each year.

The goal is to maintain a relatively even, predictable taxable income throughout your entire retirement, avoiding massive spikes that push you into punitive tax brackets or trigger Medicare surcharges. You achieve this by pulling from a combination of taxable, tax-deferred, and tax-free accounts simultaneously.

How Bracket Management Works in Practice

Imagine you need $80,000 to cover your living expenses this year. If you pull the entire amount from your traditional IRA, you generate $80,000 of ordinary income, pushing you into a higher tax bracket. If you pull it entirely from your Roth IRA, you pay zero taxes, but you forfeit the tax-free compounding of those funds.

Under the Tax Bracket Management strategy, you look at the current federal tax brackets. You might pull just enough from your traditional IRA to fill up the 12% tax bracket. Once you hit the ceiling of the 12% bracket, you stop. To fund the remainder of your lifestyle needs for the year, you pivot to your taxable brokerage accounts (taxed at lower capital gains rates) or your Roth IRA (tax-free).

By actively managing your withdrawals, you effectively choose your own tax rate. You proactively draw down your tax-deferred balances at a low tax rate during your early retirement years, which naturally reduces the size of your future RMDs.

Comparing Retirement Withdrawal Strategies

To help you visualize how these different approaches stack up, review the comparison table below. Every retiree has a unique financial picture, so understanding the trade-offs of each method empowers you to make the best decision for your household.

| Strategy Name | How It Works | Best For… | Biggest Drawback |

|---|---|---|---|

| The Sequential Method | Tap Taxable -> Tax-Deferred -> Tax-Free in order. | Retirees with smaller portfolios who prioritize simplicity and do not face major tax bracket concerns. | Can create massive RMD “tax bombs” and trigger Medicare IRMAA surcharges later in life. |

| The Proportional Method | Withdraw from all three account types each year based on the percentage they make up of your total portfolio. | Retirees who want an automated, balanced approach that provides some tax diversification without complex planning. | Ignores current tax brackets, meaning you might unnecessarily pay higher taxes in certain years. |

| Tax Bracket Management | Fill lower tax brackets with tax-deferred withdrawals, then top off income needs with tax-free or capital gains money. | Retirees with diverse account types who want to maximize their lifetime wealth and minimize taxes. | Requires active, annual tax planning and a deep understanding of tax law (or the help of a professional). |

Capitalizing on the “Gap Years”

One of the most lucrative opportunities in retirement income planning occurs during the “gap years.” These are the years between the date you retire and the date you begin claiming Social Security and taking RMDs. For many Americans, this gap occurs roughly between ages 60 and 70.

During these gap years, your earned income drops to zero, placing you in the lowest tax brackets of your adult life. This presents a golden opportunity to execute Roth conversions. A Roth conversion involves transferring money from your traditional IRA into a Roth IRA, paying the ordinary income taxes on the converted amount in the year you make the transfer.

Why pay taxes voluntarily? Because during the gap years, you can convert traditional IRA funds at the 10% or 12% tax rates. Once the money lands in the Roth IRA, it grows tax-free forever and is immune to future RMDs. By strategically converting portions of your traditional IRA during these low-income years, you defuse the future tax bomb, protect yourself from future tax rate hikes, and ensure your retirement funds stretch further.

The Hidden Power of Health Savings Accounts (HSAs)

When planning your withdrawal order, you must not overlook the Health Savings Account (HSA). If you had access to a high-deductible health plan during your working years and funded an HSA, you possess the most tax-advantaged account in the American financial system.

HSAs offer a triple-tax advantage: your contributions are tax-deductible, the money grows tax-free, and withdrawals are entirely tax-free when used for qualified medical expenses. Because healthcare represents one of the largest expenses in retirement, your HSA should serve as a dedicated bucket for medical costs, Medicare premiums, and out-of-pocket care expenses.

Furthermore, once you turn 65, the rules regarding HSAs change favorably. You can withdraw funds for non-medical expenses without paying the standard 20% penalty. You will simply pay ordinary income tax on non-medical withdrawals, effectively turning your HSA into a traditional IRA. Therefore, keep your HSA invested for as long as possible, using it as a specialized tax-free tool for health costs before tapping it for general lifestyle needs.

Factoring in Social Security and Medicare

Your retirement withdrawal strategy does not exist in a vacuum; it directly interacts with your federal benefits. The way you tap your retirement funds can alter how much money you actually get to keep from Social Security and how much you pay for Medicare.

The Social Security Tax Trap

The IRS uses a specific formula called “Combined Income” to determine how much of your Social Security benefit is subject to taxation. Combined Income equals your Adjusted Gross Income (AGI) plus non-taxable interest, plus half of your Social Security benefits.

If your Combined Income exceeds certain thresholds, up to 85% of your Social Security benefits become taxable. Because withdrawals from traditional IRAs and 401(k)s directly increase your AGI, pulling too much money from tax-deferred accounts can suddenly subject your previously safe Social Security checks to federal taxation. Utilizing tax-free Roth withdrawals keeps your AGI lower, protecting your Social Security benefits from the IRS.

Navigating Medicare IRMAA

The Medicare.gov official guidelines outline the Income-Related Monthly Adjustment Amount (IRMAA). If your Modified Adjusted Gross Income (MAGI) exceeds specific brackets, you must pay a surcharge on your Medicare Part B and Part D premiums. This surcharge can cost you thousands of dollars annually.

Crucially, Medicare looks at your tax return from two years prior to determine your premiums. If a massive traditional IRA withdrawal spikes your income at age 70, you will feel the pain of higher Medicare premiums at age 72. A balanced withdrawal strategy that utilizes Roth accounts to keep your MAGI below the IRMAA thresholds saves you significant money on healthcare costs.

“A big part of financial freedom is having your heart and mind free from worry about the what-ifs of life.” — Suze Orman

Overlaying the Bucket Strategy for Market Protection

Tapping your retirement accounts efficiently requires more than just tax planning; it requires market planning. Sequence of returns risk—the danger of experiencing a major market downturn early in your retirement—can devastate your portfolio if you are forced to sell stocks at a loss to fund your living expenses.

To protect against this, you should overlay a “Bucket Strategy” onto your tax withdrawal strategy. This involves dividing your assets based on when you need the money.

- Bucket 1 (Years 1-3): Hold three years of living expenses in safe, liquid assets like cash, high-yield savings, and short-term CDs. This bucket protects you from market crashes. You draw your daily living expenses from here.

- Bucket 2 (Years 4-10): Invest these funds in moderate-risk assets, such as high-quality bonds and dividend-paying stocks. This bucket aims to outpace inflation while providing a reliable source to replenish Bucket 1.

- Bucket 3 (Years 10+): Keep these funds invested for maximum growth in diversified equities. Because you will not need this money for a decade, you can afford to ride out the inevitable market volatility.

By securing your short-term needs in cash, you give your long-term investments the time they need to recover during bear markets. You dictate the terms of your withdrawals rather than letting Wall Street dictate them for you.

Pitfalls to Watch For

Even with a solid plan, retirees often stumble over a few common traps when executing their withdrawal strategy. Protect your nest egg by avoiding these critical mistakes:

- Ignoring State Taxes: While much of retirement planning focuses on federal tax brackets, state taxes matter immensely. Some states exempt Social Security and pension income but aggressively tax IRA withdrawals. Check your specific state laws before planning your distributions.

- Forgetting About Charitable Giving Tactics: If you are charitably inclined and over age 70½, you can utilize Qualified Charitable Distributions (QCDs). A QCD allows you to transfer funds directly from your traditional IRA to a qualified charity. This satisfies your RMD requirement but does not count toward your taxable income, saving you a fortune in taxes.

- Draining Cash Too Quickly: Some retirees feel nervous about the stock market and drain their cash reserves too early in retirement. Once the cash is gone, they are forced to sell volatile equities to survive, destroying their portfolio’s ability to rebound.

- Misunderstanding the 5-Year Roth Rule: If you perform a Roth conversion, you must wait five years before withdrawing those converted funds without a penalty (if you are under 59½, though other nuances apply). Even after 59½, establishing your first Roth IRA starts a five-year clock on tax-free earnings. Always track your conversion timelines carefully.

Getting Expert Help

Retirement income planning sits at the intersection of investment management, tax law, and federal benefits. While educating yourself is the crucial first step, certain situations require the nuance and precision of a licensed professional. You should strongly consider consulting a fiduciary advisor via the Certified Financial Planner Board or a Certified Public Accountant (CPA) if you encounter the following scenarios:

- You Have a High Net Worth Smeared Across Multiple Account Types: If you hold millions distributed across taxable brokerages, real estate, traditional 401(k)s, and Roth IRAs, the math behind bracket management becomes highly complex. A professional can run Monte Carlo simulations and multi-year tax projections to optimize your drawdowns.

- You Plan to Retire Before Age 59½: Accessing your retirement funds before the standard penalty-free age requires navigating intricate IRS rules, such as Rule 72(t) or the Rule of 55. A mistake here triggers a painful 10% early withdrawal penalty.

- You Are Navigating a Business Sale or Major Liquidity Event: If your retirement coincides with selling a business or exercising stock options, the resulting income spike will warp your tax bracket and your withdrawal plan. A CPA can help you structure the sale alongside your retirement distributions to mitigate the tax blow.

Frequently Asked Questions

Does the 4% rule dictate which accounts I should tap first?

No. The famous 4% rule of thumb—which suggests you can safely withdraw 4% of your portfolio in year one and adjust for inflation thereafter—only addresses how much money you can withdraw safely. It provides absolutely no guidance on where that money should come from. You still need a distinct withdrawal strategy to determine the order of accounts to ensure your 4% withdrawal is as tax-efficient as possible.

Should I spend down my traditional IRA before claiming Social Security?

This is a highly effective strategy for many retirees, particularly during the “gap years” in their early 60s. By deferring Social Security, your monthly benefit grows by up to 8% per year until age 70. Using your traditional IRA to fund your lifestyle while you delay Social Security accomplishes two goals: it guarantees a higher lifetime fixed income from the government, and it strategically reduces your pre-tax IRA balance, which lowers your future Required Minimum Distributions.

Can I use capital losses to offset my retirement withdrawals?

Yes, tax-loss harvesting is a vital tool for retirees. If you sell investments in your taxable brokerage account at a loss, you can use those losses to offset capital gains you realize that same year. If your losses exceed your gains, you can use up to $3,000 of those losses to offset ordinary income (such as traditional IRA withdrawals) and carry the remaining losses forward to future tax years. Refer to the IRS guidelines on capital losses for exact reporting requirements.

How do Required Minimum Distributions (RMDs) affect my withdrawal order?

Once you reach RMD age, the government forces your hand. You no longer have full control over your withdrawal order because you must take a specific amount from your traditional tax-deferred accounts every year, whether you need the money or not. Your strategy shifts from “Which account should I tap?” to “How do I optimize the money I am forced to withdraw?” If you don’t need your RMDs for living expenses, you can reinvest the after-tax remainder into a taxable brokerage account or use it for charitable giving via a QCD.

Building a sustainable, tax-efficient retirement withdrawal strategy takes time and careful calculation. The order in which you tap your retirement funds drastically influences the longevity of your portfolio. Take inventory of your current account balances, project your estimated living expenses, and review your projected tax brackets. Consider executing strategic Roth conversions during your lower-income years to shield your future self from unnecessary taxation.

This is educational content based on general retirement and financial principles. Individual results vary based on your situation. Always verify current benefit rules, tax laws, and eligibility requirements with official sources like SSA, Medicare.gov, or the IRS.

Leave a Reply