Packing up your life to retire abroad offers an exciting path to lower living costs, a richer culture, and a warmer climate. Before you trade your suburban mortgage for a beachfront villa in Portugal or a mountain retreat in Costa Rica, you must understand the complex logistical realities of living as an expatriate. Retiring overseas transforms everything from how you access your money and file taxes to how you manage healthcare as you age. This guide breaks down the ten essential financial and lifestyle factors you must evaluate to ensure your international relocation succeeds. Preparing for these hurdles now prevents expensive surprises later, letting you focus entirely on enjoying your hard-earned global adventure.

1. Medicare Rarely Crosses International Borders

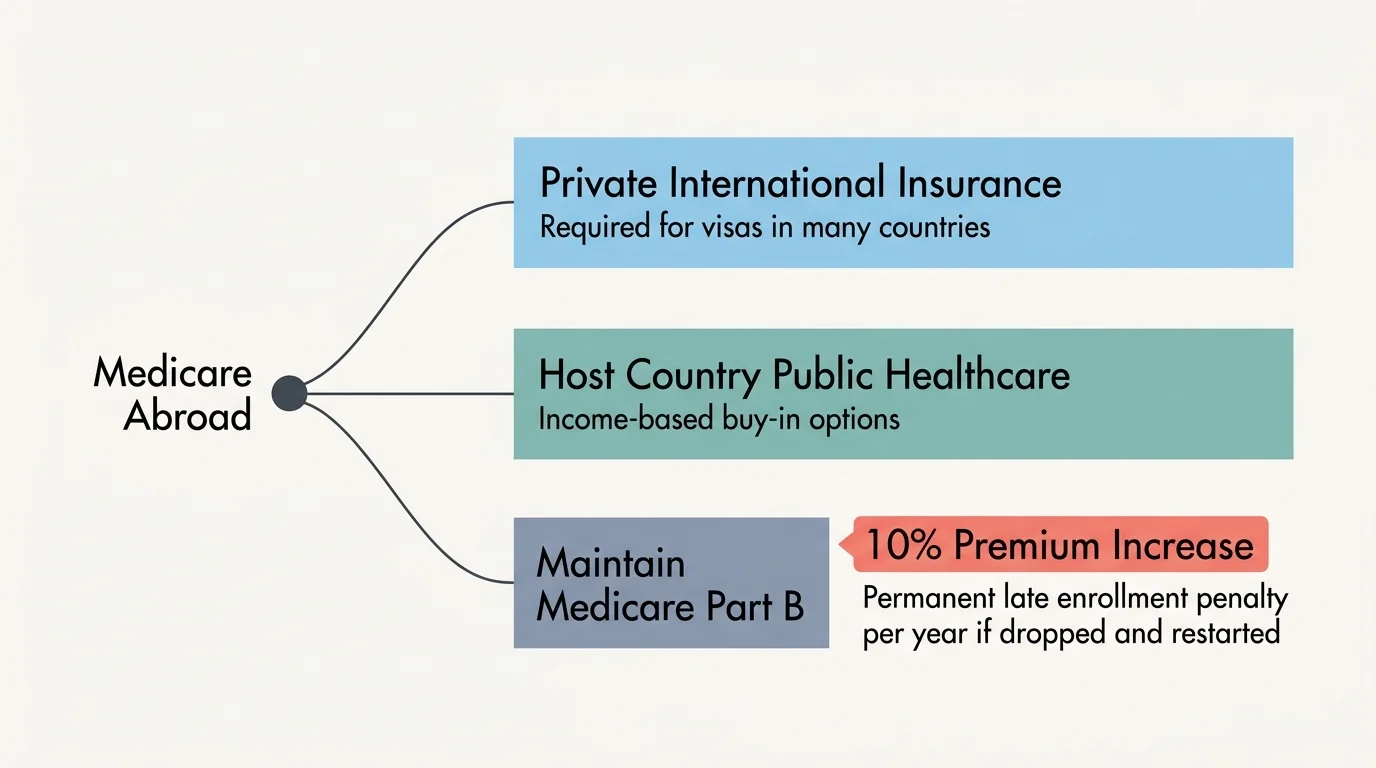

One of the biggest shocks for Americans considering an expat retirement is realizing their standard government healthcare does not follow them. With very few exceptions, traditional Medicare—including Parts A, B, and D—does not cover healthcare costs outside the United States and its territories. If you have a medical emergency in Spain or need regular prescriptions in Panama, your Medicare card will not help you pay the bill.

This reality leaves you with a few distinct options. First, you can purchase comprehensive international private health insurance. These policies are designed specifically for expatriates and often provide excellent coverage at a fraction of the cost of private insurance in the United States. Many popular retirement destinations require you to show proof of private health insurance before they will grant you a residency visa.

Alternatively, many retirees opt to join the national healthcare system of their host country once they achieve permanent residency. Countries like Italy, France, and Costa Rica offer high-quality public healthcare systems that you can buy into for a modest monthly fee based on your income. However, you must carefully evaluate the quality of care in your specific region and the wait times for elective procedures.

Even if you live abroad full-time, carefully consider whether you should continue paying your Medicare Part B premiums. If you drop Part B and later decide to return to the United States, you will face a permanent late enrollment penalty—a 10% premium increase for every full 12-month period you were eligible but not enrolled. Maintaining Part B acts as an insurance policy for your return, allowing you to fly back to the States for complex treatments or surgeries. You can review the specific rules regarding international coverage directly at Medicare.gov.

2. You Can Still Collect Social Security

Moving out of the country does not mean forfeiting the retirement benefits you spent decades earning. The Social Security Administration (SSA) routinely sends monthly benefit payments to hundreds of thousands of retirees living around the globe. In most cases, your payments will continue seamlessly.

The SSA makes it relatively easy to receive your money through their International Direct Deposit (IDD) program. If your retirement destination is one of the dozens of countries participating in this program, the SSA will electronically deposit your funds directly into your foreign bank account, automatically converting the US dollars to the local currency. This minimizes costly wire transfer fees and ensures your money arrives safely.

However, geopolitical rules apply. The US Treasury prohibits sending Social Security payments to certain restricted countries, including Cuba and North Korea. Furthermore, if you plan to continue working while living abroad before reaching your full retirement age, the standard earnings limits still apply. If you exceed the annual earnings threshold, the SSA will withhold a portion of your benefits just as they would if you were working in Ohio or Texas. You must also complete an annual questionnaire from the SSA proving you are still alive and eligible to receive benefits; failing to return this form promptly will result in suspended payments.

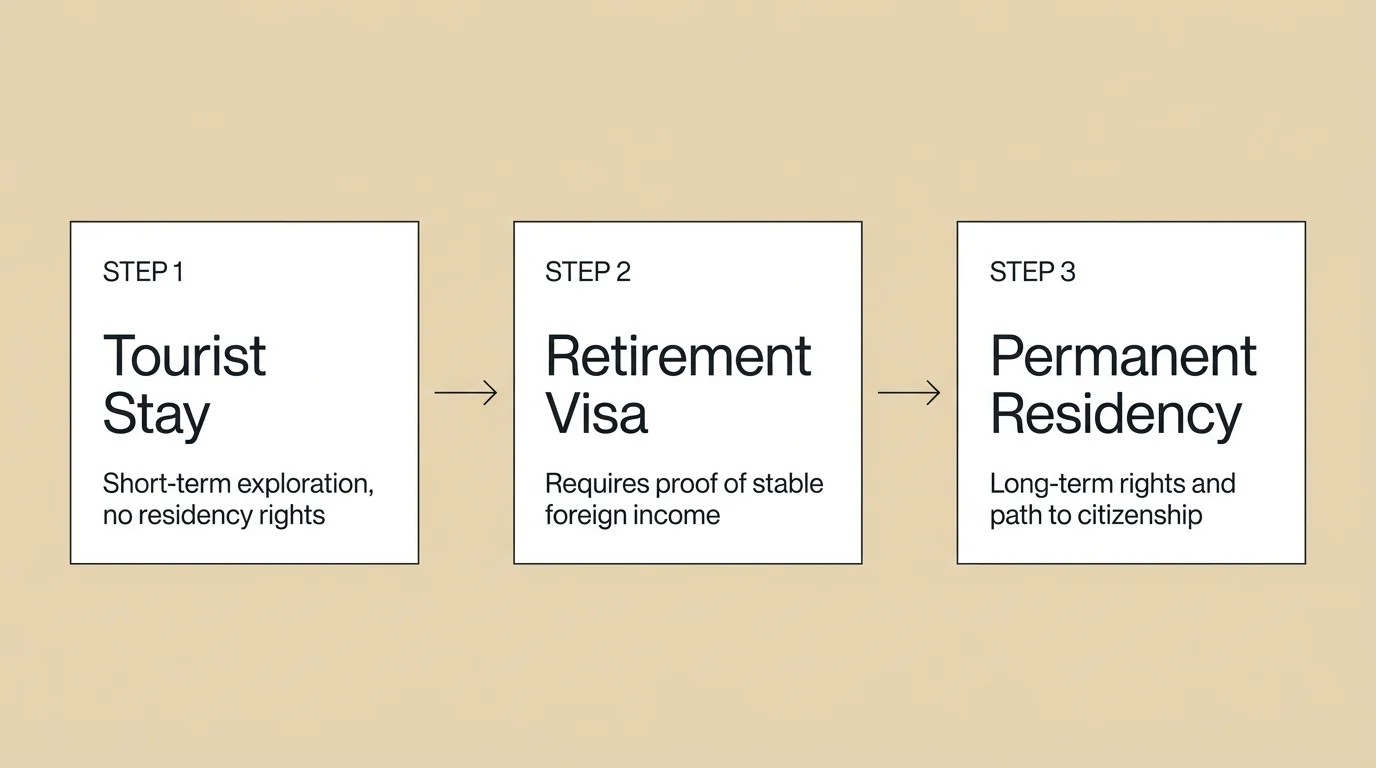

3. Visas Dictate Where You Can Live

You cannot simply arrive in a foreign country on a tourist visa and decide to stay forever. Every nation tightly controls its borders and imposes strict rules on who can reside within them. When evaluating the best countries to retire, the accessibility and cost of their retirement visa programs must be a top consideration.

Many of the most popular expat destinations offer specialized “pensionado” or retirement visas designed specifically to attract foreign capital. To qualify, you must typically prove a steady, guaranteed stream of monthly income—usually from Social Security, a government pension, or a guaranteed annuity. The income threshold varies wildly; some countries require as little as $1,000 per month, while others demand $3,000 or more per person.

If you do not have a guaranteed pension, some countries allow you to qualify by proving a substantial net worth or by making a significant real estate investment in the country (often called a “Golden Visa”). The application process is rarely swift. Expect to submit federal background checks, undergo comprehensive medical exams, and have all your official documents apostilled and translated by certified professionals before you even book your flight.

4. The IRS Will Follow You Everywhere

Unlike almost every other developed nation on earth, the United States practices citizenship-based taxation. This means that as long as you hold an American passport, you must file an annual tax return with the Internal Revenue Service (IRS), reporting your worldwide income, regardless of where you currently reside.

Retiring overseas does not exempt you from American tax obligations. Furthermore, the Foreign Account Tax Compliance Act (FATCA) requires foreign financial institutions to report the account details of their US clients directly to the IRS. You cannot hide money offshore. If the total value of your foreign bank and financial accounts exceeds $10,000 at any point during the calendar year, you are legally required to file a Report of Foreign Bank and Financial Accounts (FBAR) with the Financial Crimes Enforcement Network (FinCEN). The penalties for failing to file an FBAR are severe, often reaching tens of thousands of dollars.

While you must file, you may not necessarily owe double taxes. The US maintains tax treaties with dozens of countries to prevent dual taxation. You can often utilize the Foreign Tax Credit to offset American taxes with the taxes you paid to your host country. However, navigating these international tax codes requires meticulous record-keeping and a deep understanding of tax law.

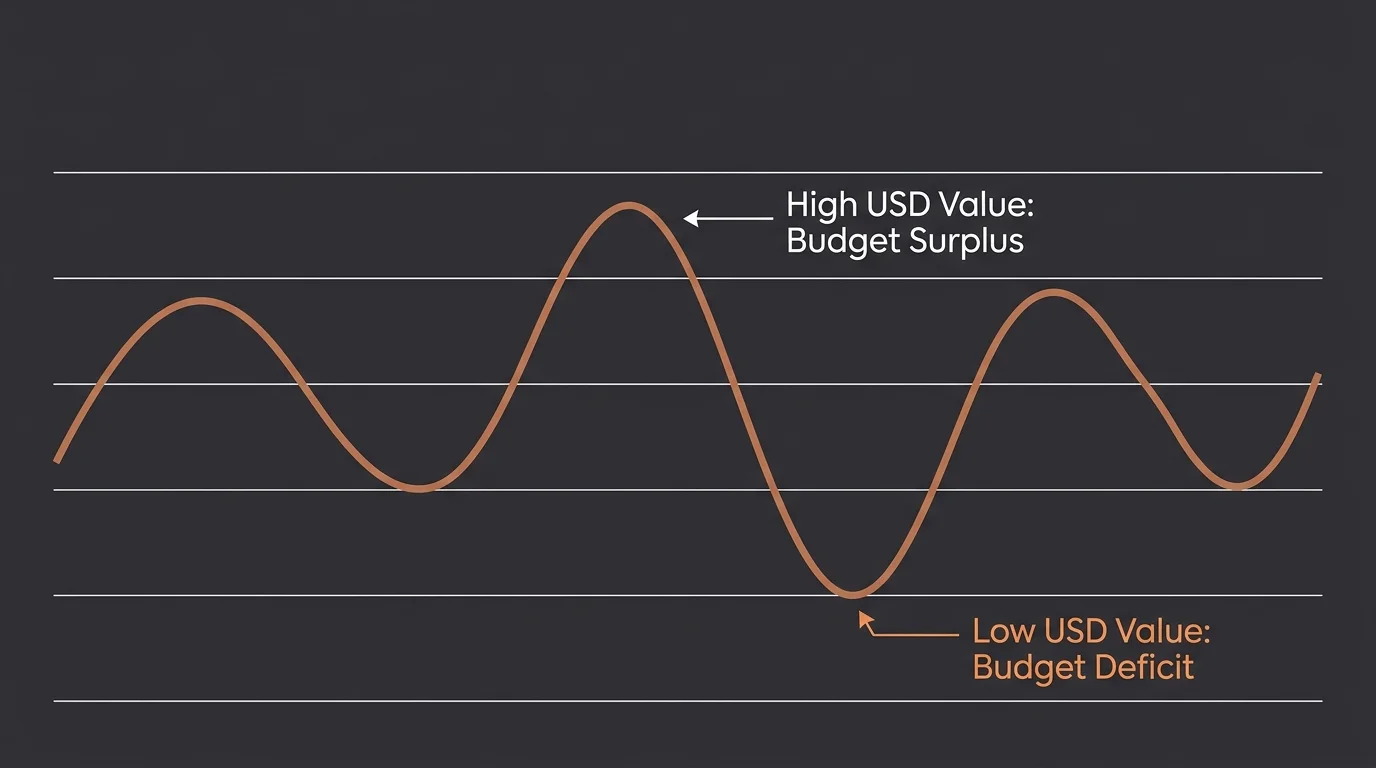

5. Currency Fluctuations Can Destroy a Budget

When you generate your income in US dollars but pay your daily living expenses in a foreign currency, you are inherently taking on currency risk. Exchange rates fluctuate daily based on global economics, inflation, and political events. A favorable exchange rate might make a destination seem incredibly cheap today, but a 15% swing in currency valuation can easily wipe out your carefully planned retirement budget in a matter of months.

Savvy retirees mitigate this risk through strategic banking. Maintaining a US bank account that charges no foreign transaction fees or international ATM fees—such as those offered by Charles Schwab or Fidelity—allows you to withdraw local currency directly from your US funds at the exact daily exchange rate. Alternatively, using international transfer services like Wise or Revolut allows you to move money between your US accounts and local foreign accounts efficiently, minimizing the wide spreads and hidden fees traditional banks charge.

Never lock all your assets into the currency of a developing nation. Maintain the bulk of your retirement portfolio and emergency reserves in US dollars, transferring only what you need for one to two months of living expenses at a time.

6. The Real Estate Market Operates Differently

The rules of buying, selling, and renting property vary dramatically across the globe. Real estate regulations, zoning laws, and buyer protections that you take for granted in the United States often do not exist abroad. In some countries, foreigners cannot directly own land near borders or coastlines; in others, the concept of title insurance is entirely foreign, leaving you vulnerable to claims from long-lost heirs.

Because of these complexities, the golden rule of retiring overseas is straightforward: always rent for at least one full year before buying property.

Comparing Housing Options Abroad

| Housing Strategy | Primary Advantages | Major Drawbacks |

|---|---|---|

| Renting (First 1-2 Years) | Allows you to test different neighborhoods; preserves liquid capital; no exposure to local property market crashes; easy to leave if the country is not a good fit. | Subject to rent increases; limited ability to renovate or modify the home for aging in place; temporary feeling. |

| Buying Property | Provides a permanent base; avoids rent inflation; allows for full customization and mobility modifications; potential for property appreciation. | Locks up significant capital; extremely difficult to sell quickly if you need to repatriate; exposes you to legal and title risks; incurs maintenance and local tax costs. |

Renting long-term gives you time to experience the distinct seasons, understand the nuances of local neighborhoods, and build a network of trusted professionals. You may discover that the coastal town you loved during a one-week vacation is unbearably humid for eight months of the year, or that the charming mountain village lacks reliable electricity.

7. The True Cost of Living Variances

It is easy to be seduced by articles touting locations where you can “live like royalty on $1,500 a month.” While geographical arbitrage—leveraging a strong US dollar in a country with a lower cost of living—is very real, the actual cost depends entirely on your lifestyle choices.

If you adapt fully to the local economy—eating local produce, dining at neighborhood establishments, utilizing public transportation, and living in non-expat neighborhoods—your expenses will plummet. However, if you attempt to replicate your exact American lifestyle abroad, your costs will skyrocket. Imported American goods, from specific brands of peanut butter to large appliances, carry steep tariffs. Maintaining a large, air-conditioned house and running a gas-guzzling SUV will quickly erode the cost-of-living benefits you sought.

You must also factor in the hidden costs of an expat retirement. You will need a budget for frequent flights back to the US, international health insurance premiums, visa renewal fees, and potentially higher costs for specialized legal and tax advice.

8. The Cultural and Language Learning Curve

A vacation is an escape; a relocation is a lifestyle. The honeymoon phase of living abroad eventually fades, replaced by the mundane realities of daily life. Paying utility bills, arguing with a telecom provider over an internet outage, or navigating a complex local bureaucracy to renew a driver’s license requires patience and, ideally, proficiency in the local language.

While you can certainly survive in many popular expat enclaves speaking only English, failing to learn the local language isolates you from the broader community and leaves you entirely dependent on bilingual locals or costly fixers. Learning the language, even at a basic conversational level, demonstrates respect for your host country and opens the door to genuine cultural integration.

You must also adapt to different cultural norms regarding time, customer service, and efficiency. The fast-paced, highly structured American way of doing business is an anomaly in much of the world. Embracing a slower pace of life is part of the appeal of retiring abroad, but it can be intensely frustrating when you need a plumber immediately and are told they might arrive sometime next week.

9. Distance From Family and Friends Takes a Toll

The financial math of a retirement abroad might be flawless, but the emotional math is far more complex. Moving overseas means putting significant physical distance between yourself and your support network. You will inevitably miss out on casual Sunday dinners, school plays, and impromptu gatherings with lifelong friends.

Technology helps bridge this gap. Video calls make it easy to stay in touch, but they cannot replace physical presence, especially as grandchildren grow or aging parents in the US experience health declines. When emergencies happen, jumping on a 12-hour international flight is both physically exhausting and incredibly expensive. You must have honest conversations with your family about your expectations for visiting each other, recognizing that the burden of travel will likely fall mostly on your shoulders.

“A successful retirement isn’t just about the money. It’s about finding purpose, meaning, and a reason to get out of bed every morning.”

— Mitch Anthony, Retirement Expert

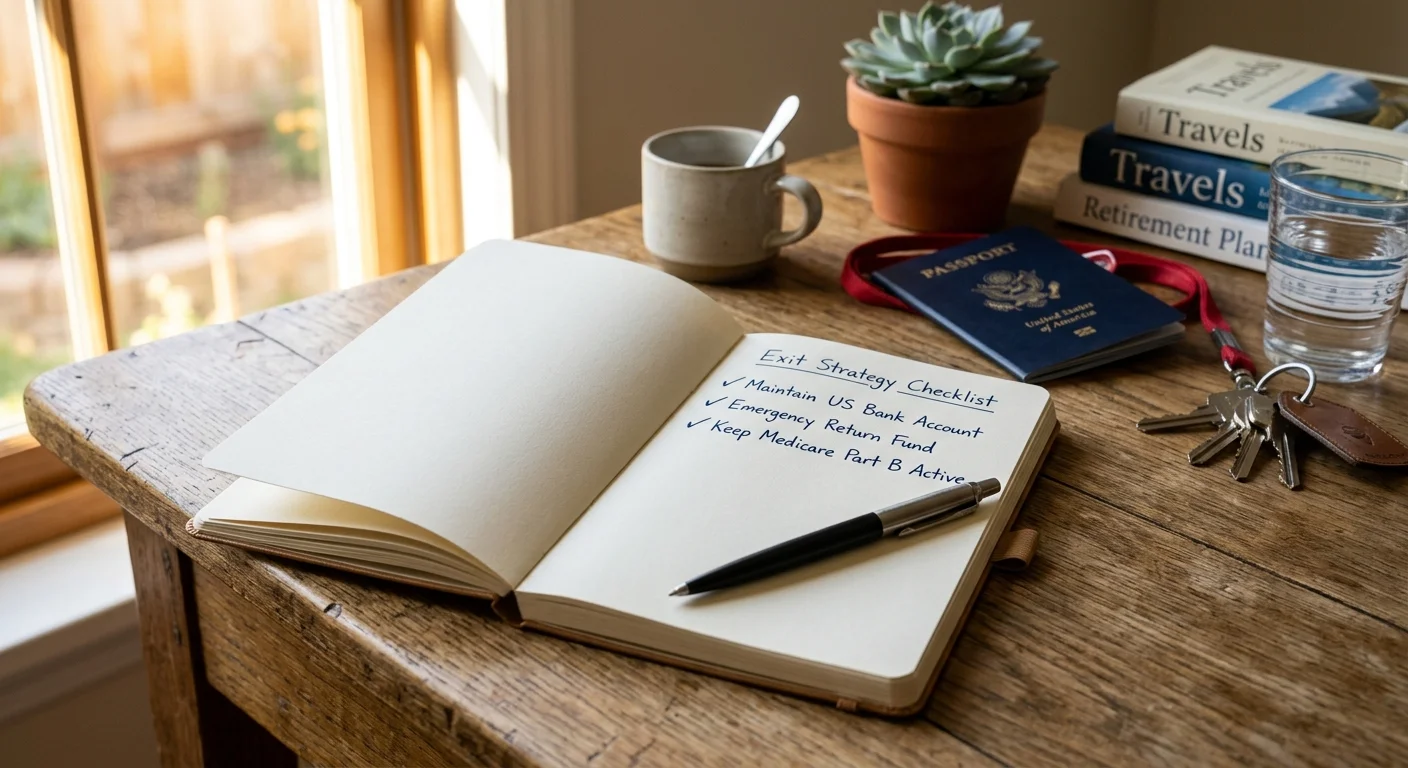

10. You Need an Exit Strategy

Life is unpredictable. Your health may decline, your spouse may pass away, or the political stability of your host country may falter. Many expats live abroad happily for a decade but ultimately decide to return to the United States for their final years to access specialized medical care or to be closer to family.

You must have a contingency plan and the financial resources to execute it. This means maintaining a healthy emergency fund in US dollars, explicitly designated as your “repatriation fund.” Do not tie up all your wealth in foreign illiquid assets. You should also ensure your legal documents, such as your power of attorney and healthcare directives, are valid in both your host country and the United States.

Avoiding Common Errors

Transitioning to an international retirement requires meticulous planning. Sidestepping these frequent missteps will protect your wealth and your sanity:

- Canceling Medicare Part B to save money: While it seems logical to stop paying for insurance you aren’t actively using, dropping Part B permanently severs your safety net. If a severe health crisis forces you back to the US, you will face massive out-of-pocket costs and lifetime penalties if you try to re-enroll later.

- Ignoring foreign bank reporting requirements: The IRS aggressively pursues offshore tax evasion. Assuming your small foreign checking account isn’t worth reporting can trigger massive FBAR penalties. Always report foreign accounts if the aggregate total exceeds $10,000.

- Buying real estate during the honeymoon phase: Purchasing a home within the first few months of arriving is the fastest way to trap yourself in a location that may not suit you long-term. Renting is cheap insurance against buyer’s remorse.

- Failing to test drive the climate: Visiting a tropical destination in January is wonderful; enduring the relentless heat and monsoons of August is entirely different. Experience a location year-round before committing to permanent residency.

When DIY Isn’t Enough

While you can manage many aspects of retirement planning on your own, an international move introduces complex legal and financial liabilities. You should strongly consider hiring professionals for the following scenarios:

- Cross-Border Taxation: Hire a Certified Public Accountant (CPA) who specializes in expat taxes. They will ensure you utilize the Foreign Earned Income Exclusion or Foreign Tax Credit correctly, keeping you compliant with both the IRS and your host country.

- Immigration and Visas: While you can navigate visa paperwork alone, hiring a local immigration attorney speeds up the process, ensures you submit the exact documents required, and helps you avoid bureaucratic roadblocks.

- Estate Planning: Your US-based will may not dictate how your foreign assets are distributed. You likely need a specialized international estate attorney to ensure your assets pass to your heirs smoothly, avoiding probate nightmares in multiple jurisdictions.

Frequently Asked Questions

Will my Social Security benefits be taxed if I live abroad?

Yes, your US tax obligations remain the same regardless of your location. Up to 85% of your Social Security benefits may be subject to US federal income tax depending on your total combined income. Furthermore, depending on the tax treaty the US has with your host country, your new country of residence might also tax those benefits. Always consult a cross-border tax expert to understand your specific liabilities.

Do I still have to pay US state income taxes?

This depends heavily on the state you lived in prior to moving abroad. States like Florida or Texas have no state income tax, making the transition simple. However, states like California and New York have “sticky” residency rules. If you maintain property, a driver’s license, or voter registration in these states, they may still consider you a resident and demand state income taxes. You must formally sever your domicile to avoid this.

Can I use Medicare if I travel back to the US?

Yes. If you continue paying your Medicare Part B premiums while living abroad, your coverage remains active for any care you receive within the United States. Many expats use their host country’s healthcare system for routine daily care but return to the US for major surgeries or specialized treatments, utilizing their intact Medicare coverage.

Mapping Your Next Steps

Retiring abroad is not merely a financial transaction; it is a profound lifestyle transition that demands courage, flexibility, and intensive preparation. Begin by narrowing down your list of potential destinations and planning extended, month-long scouting trips. Focus on the mundane aspects of daily living during these visits—go to grocery stores, visit local pharmacies, and speak with expats who have successfully navigated the transition. By addressing the logistics of healthcare, taxes, and residency head-on, you clear the path for a truly rewarding international retirement.

This is educational content based on general retirement and financial principles. Individual results vary based on your situation. Always verify current benefit rules, tax laws, and eligibility requirements with official sources like SSA, Medicare.gov, or the IRS.

Last updated: July 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply