For decades, the standard American retirement dream involved downsizing to a quiet condo on a golf course or maintaining the empty family home as a monument to past holidays. Today, a profound shift is reshaping how we age. Driven by evolving economic realities and a desire for deeper familial connection, the number of Americans living in multigenerational households has surged. This return to a historically common way of living is proving that independence does not require isolation.

When you evaluate your retirement housing choice, the decision to share a roof with adult children and grandchildren requires careful consideration. It is a complex blend of financial strategy, architectural planning, and emotional boundary-setting. Done correctly, it provides financial relief, robust social support, and peace of mind for everyone involved. Handled poorly, it can strain relationships and create legal headaches.

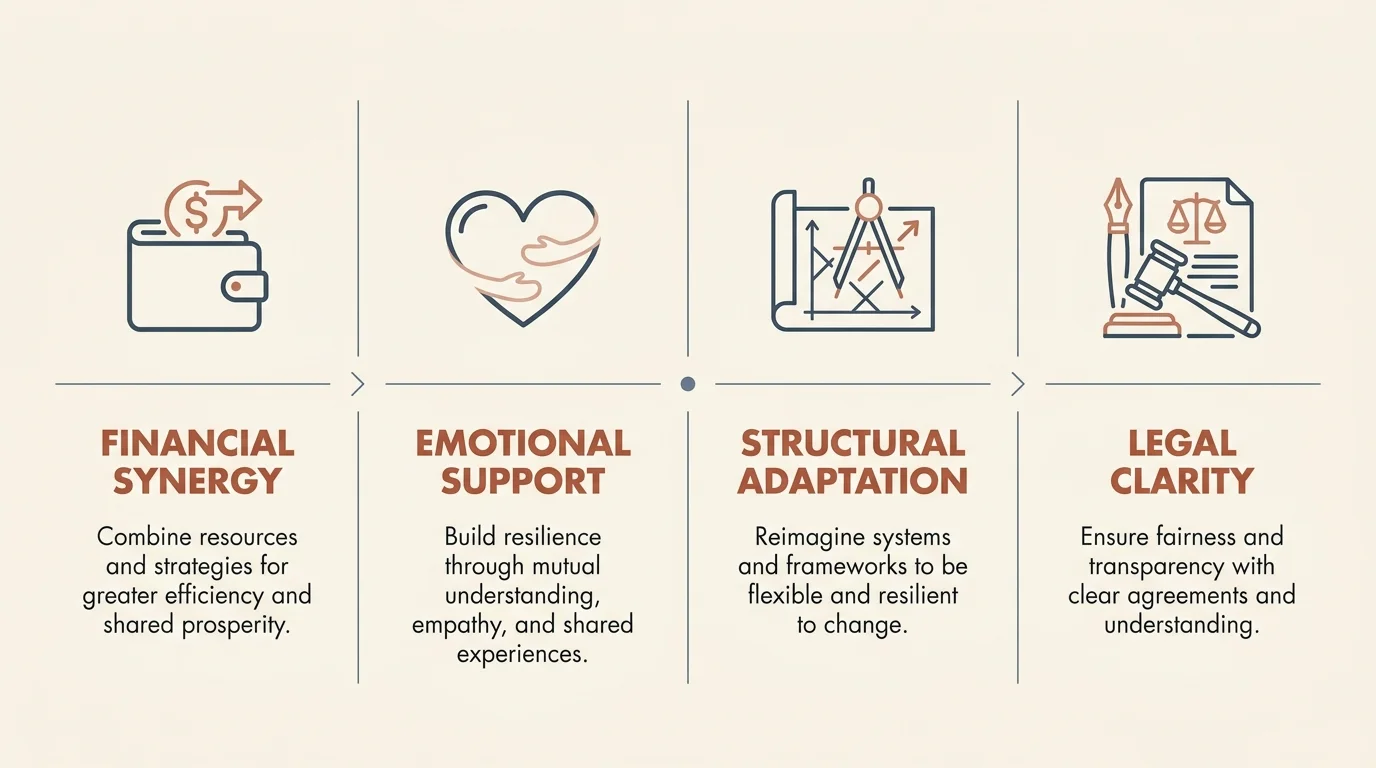

At a Glance: The Essentials of Co-Living

- Financial Synergy: Pooling resources combats the rising costs of housing, utilities, and groceries while allowing both generations to maximize their savings.

- Emotional Support: Daily interaction drastically reduces the risks of senior isolation while providing young families with invaluable support.

- Structural Adaptation: Successful integration usually requires modifying the home environment—such as adding an Accessory Dwelling Unit (ADU) or an in-law suite—to ensure privacy.

- Legal Clarity: Formalizing financial contributions and ownership stakes is crucial to protect your retirement assets and prevent family disputes.

The Financial Catalyst: Sharing the Burden in a Pricey Era

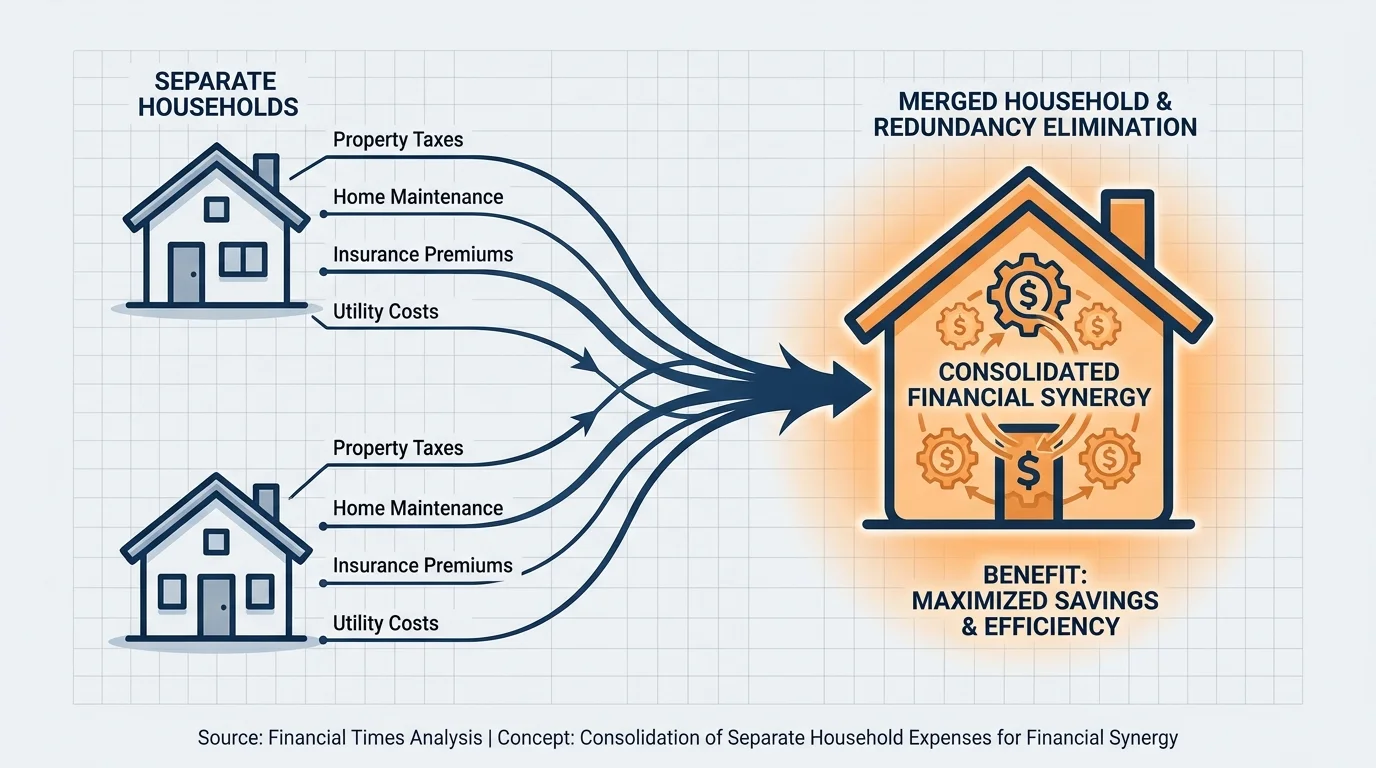

It is no secret that the cost of living has fundamentally altered retirement planning. Property taxes, home maintenance, insurance premiums, and utility costs continue to climb, often outpacing the annual cost-of-living adjustments provided by Social Security. Maintaining a large, largely empty house can quietly drain your retirement portfolio, leaving you house-rich but cash-poor.

Multi generational living offers a powerful economic countermeasure. By consolidating two households into one, families instantly eliminate redundant expenses. You are no longer paying for two separate roofs, two internet bills, or two property tax assessments. This financial synergy allows you to stretch your retirement income further, providing a buffer against market volatility and inflation.

Consider the mechanics of the arrangement. In many cases, retirees sell their primary residence and use a portion of the equity to fund a significant addition or renovation on their adult child’s property. Alternatively, the family might pool their resources to purchase a larger home designed specifically for dual living. This collaborative approach frequently allows both generations to reside in a more desirable neighborhood or a higher-quality home than either could afford independently. Moreover, the adult children benefit from reduced childcare costs, while you may eventually benefit from informal caregiving, delaying or entirely avoiding the staggering costs of assisted living facilities.

Redefining Independence: The Psychological Shift

Historically, American culture attached a certain stigma to moving in with adult children, frequently framing it as a loss of independence or a sign of financial failure. That narrative is rapidly dissolving. Today’s retirees are choosing this lifestyle proactively, recognizing that true independence is about controlling your environment and your choices, not necessarily living alone.

“A big part of financial freedom is having your heart and mind free from worry about the what-ifs of life.” — Suze Orman, Personal Finance Expert

Releasing the burden of solo homeownership can be incredibly liberating. When you no longer have to worry about cleaning the gutters, repairing the HVAC system, or managing a sprawling yard entirely on your own, you free up both time and mental energy. You can redirect that energy toward travel, hobbies, volunteering, or simply enjoying your daily routine without the underlying stress of property maintenance.

Furthermore, the modern approach to co-living prioritizes autonomy. It is less about moving into the spare bedroom down the hall and more about creating distinct, self-sufficient living quarters within a shared property footprint. This structural separation allows you to maintain your privacy and personal schedule while enjoying the security of knowing family is just a few steps away.

Designing the Shared Home: Privacy and Accessibility

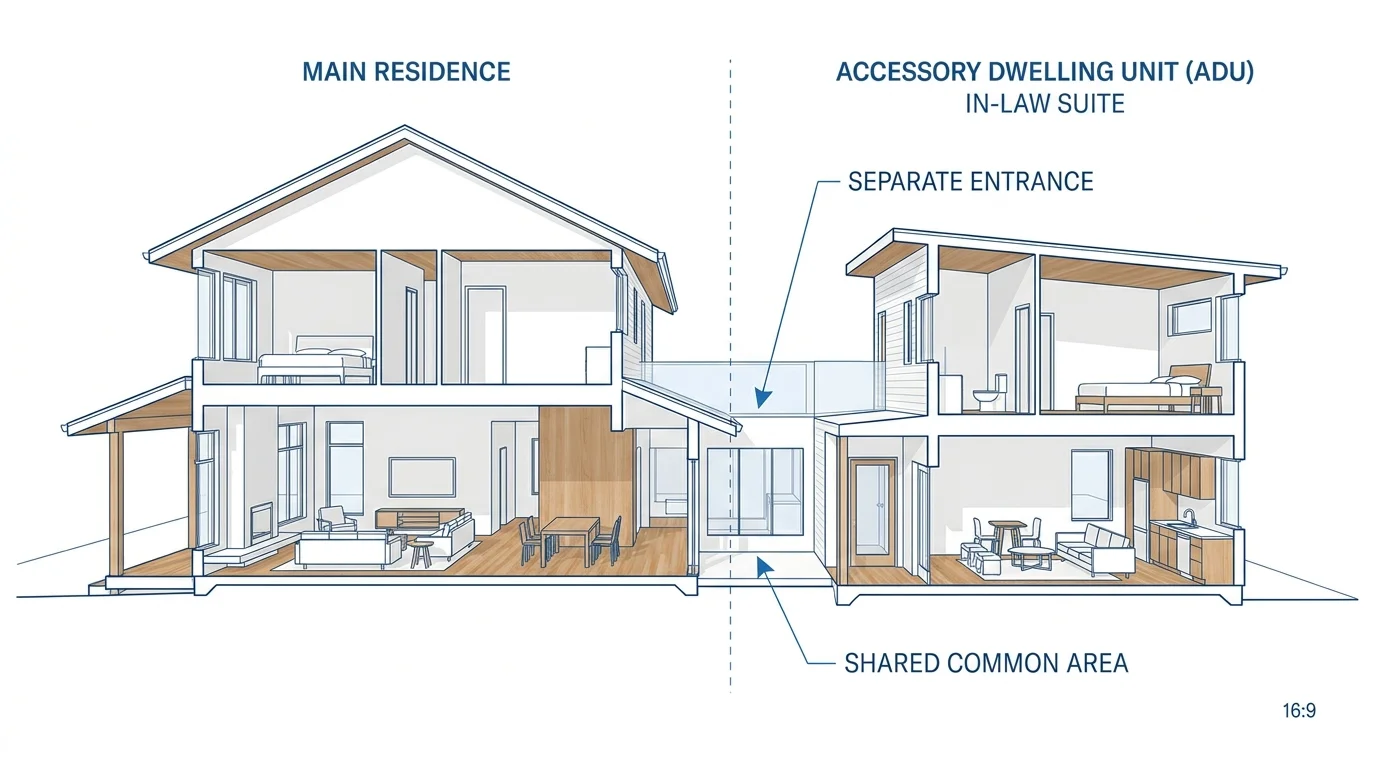

The physical space you inhabit dictates the success of your living arrangement. When retirees move family dynamics into a single property, architectural boundaries become essential. Expecting adults used to decades of autonomy to share a single kitchen, living room, and thermostat without friction is unrealistic. The family home seniors share must be intentionally designed to accommodate distinct lifestyles.

There are several popular structural solutions for creating harmony under one roof (or on one lot):

- Accessory Dwelling Units (ADUs): Frequently referred to as granny flats or backyard cottages, ADUs are standalone structures built on the same property as the main house. They offer the highest level of privacy, featuring their own entrances, kitchens, bathrooms, and living spaces. ADUs are ideal if your adult children have a large enough lot and local zoning laws permit the construction.

- In-Law Suites and Basement Conversions: This involves repurposing an existing section of the main house. A finished basement with a walkout entrance, a converted attached garage, or a built-out space above a garage can serve as a comprehensive apartment. Soundproofing the shared walls or ceilings is highly recommended in these setups.

- Dual-Master Floor Plans: Some families opt to purchase a new home explicitly designed for multi-generational living. These homes feature two distinct primary bedroom suites, often on opposite ends of the house or on different floors, alongside expanded communal areas.

Regardless of the configuration, proactive modifications are vital. You must consider how your mobility needs might change over the next ten to twenty years. Incorporating universal design principles—such as zero-step entries, wider doorways to accommodate walkers or wheelchairs, walk-in showers with grab bars, and slip-resistant flooring—ensures the space remains safe and functional as you age. The AARP provides excellent resources and checklists for modifying homes to support aging in place safely.

The Grandparent Advantage: Deepened Bonds and Daily Purpose

While the financial and practical benefits are easily quantifiable, the emotional rewards of living with kids and grandchildren are profound. Social isolation and loneliness are recognized as significant health risks for older adults, contributing to cognitive decline, depression, and cardiovascular issues. Immersing yourself in the lively, sometimes chaotic environment of a multi-generational home acts as a powerful antidote to isolation.

The daily interactions—sharing a morning coffee, helping a grandchild with homework, or simply being present for family dinners—provide a steady stream of social engagement. This proximity fosters a deep, organic bond between grandparents and grandchildren that occasional holiday visits cannot replicate. You have the opportunity to pass down family history, share your skills, and offer the kind of patient mentorship that busy parents sometimes struggle to provide.

This is a reciprocal relationship. While you provide wisdom, emotional support, and perhaps childcare assistance, the younger generations offer energy, technological assistance, and a direct connection to modern trends. Being needed and having a defined role within the household injects daily life with a strong sense of purpose, which is frequently cited as a key component of a fulfilling retirement.

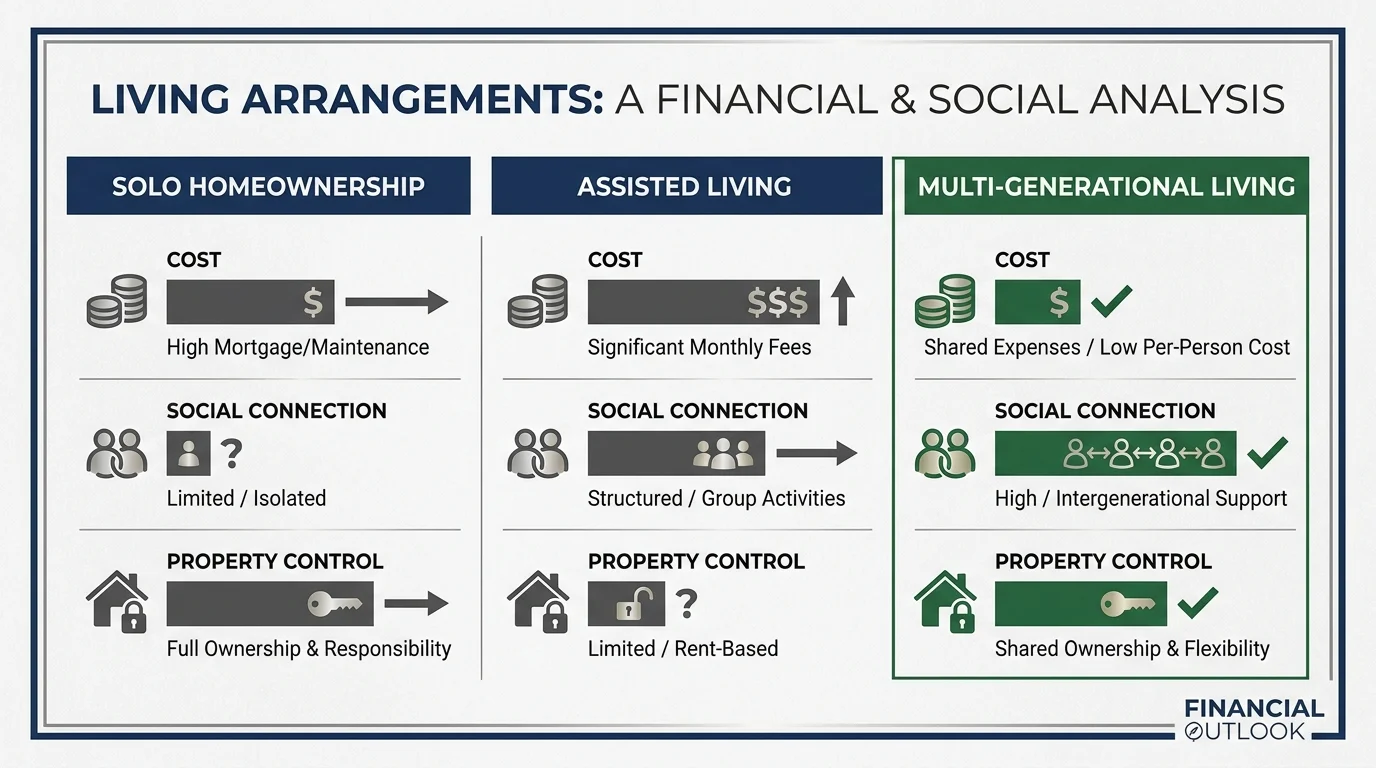

Comparing Retirement Living Options

To fully understand where multi-generational living fits into the broader landscape, it helps to compare it directly with the other standard housing strategies available to retirees.

| Feature | Multi-Generational Living | Downsizing / Aging in Place Alone | Independent Living Facility |

|---|---|---|---|

| Financial Impact | Highly efficient; shared costs reduce overall burden. Equity can be unlocked. | Moderate; lower taxes and maintenance, but you bear all costs alone. | High; monthly fees can be substantial and increase annually. |

| Privacy Level | Varies by design. High in an ADU, moderate in a shared house. Requires strong boundaries. | Maximum privacy and total control over your environment. | High privacy in your unit, but communal living dictates social norms. |

| Social Engagement | Constant, organic interaction with family. Can be noisy or busy. | Requires proactive effort to avoid isolation and maintain a social calendar. | Built-in community with organized events and peer socialization. |

| Care and Support | Informal, daily support from family. Easy coordination for future health needs. | Must hire outside help or rely on long-distance family if health declines. | Varies; easy transition to assisted living usually available on the same campus. |

Navigating the Transition: Essential Legal and Financial Conversations

Enthusiasm and familial love are not enough to sustain a multi-generational living arrangement; you need clear, documented agreements. Treating the integration of two households with the same rigor you would apply to a business partnership protects your assets and preserves your relationships.

Before any moving trucks are booked or contractors are hired, you must sit down with your family to discuss the financial mechanics. If you are selling your home and contributing $150,000 to build an in-law suite on your child’s property, you need to define what that money represents. Is it a gift? Is it a loan to be repaid if the house is sold? Does it grant you an equity stake in the property? These questions are critical because life is unpredictable. If your adult child divorces, faces a lawsuit, or needs to relocate for work, your living situation and your financial investment could be jeopardized.

Consulting with an elder law attorney or a financial advisor is highly recommended to draft a formal agreement. This might involve structuring your contribution as a loan with a lien on the property, or creating a life estate that guarantees your right to live on the premises regardless of who owns the title. The Consumer Financial Protection Bureau (CFPB) offers extensive guidance on managing your money and protecting your assets as you age, which can serve as a helpful starting point for these complex discussions.

Furthermore, you must update your estate plan. If you are investing heavily in the property of one child, you need to consider how this impacts the inheritance of your other children. Failing to address this discrepancy can lead to severe family conflicts after you pass away. Open, transparent communication about your estate planning decisions is the best way to prevent future resentment.

Beyond the big-picture legalities, you must establish an equitable system for managing daily household expenses. Who pays the elevated utility bills? How are property taxes divided? Who buys the groceries, and who pays for the inevitable home repairs? Drafting a simple, written budget and responsibility chart ensures that no one feels taken advantage of as the months turn into years.

Avoiding Common Errors

Even with the best intentions, families frequently stumble into predictable pitfalls when merging households. Being aware of these common errors allows you to proactively engineer solutions before frustrations boil over.

Relying on Unspoken Rules: Assuming everyone shares your definitions of “clean,” “quiet time,” or “helping out” is a recipe for disaster. Different generations have different habits. You must explicitly discuss expectations regarding chores, shared meals, unannounced visitors, and noise levels. Set clear boundaries and agree on a method for resolving disputes calmly.

Overcommitting to Childcare: While being an active grandparent is a joy, you are retiring, not opening a full-time daycare center. It is easy for adult children to lean heavily on your availability, gradually eroding your personal time. Establish firm schedules and boundaries regarding when you are available to watch the grandchildren and when you are “off the clock” to pursue your own interests.

Neglecting Your Peer Network: Moving in with family provides immense social support, but it should not replace your relationships with people your own age. It is vital to maintain your own social life, whether through community centers, hobby groups, volunteering, or religious organizations. Relying exclusively on your adult children for social interaction can lead to feelings of dependency and place undue pressure on the family dynamic. Organizations like the National Council on Aging (NCOA) provide excellent directories for finding local senior centers and volunteer opportunities to keep you connected to your peers.

Frequently Asked Questions

Does contributing to a home addition give me an ownership stake?

Not automatically. If you hand over cash to build an ADU on property owned by your child, the law generally views that as a gift unless you have legal documentation stating otherwise. To protect your investment and secure an ownership stake or a guaranteed right of residency, you must work with an attorney to draft specific legal agreements, such as a tenancy in common agreement or a life estate deed.

How does multi-generational living impact Medicaid eligibility?

Medicaid rules regarding asset transfers are strict and feature a five-year look-back period. If you give your child a large sum of money to modify their home and then require Medicaid for long-term care within five years, that financial transfer could result in a penalty period, delaying your eligibility. It is crucial to structure your financial contributions legally—often through a formal caregiver agreement or a properly documented loan—to avoid jeopardizing future Medicaid benefits.

How do we handle local zoning laws for an in-law suite?

Zoning laws vary wildly by municipality. Before spending any money on architectural plans, you or your family must consult the local zoning board or building department. Some towns encourage ADUs to increase housing density, while others strictly prohibit secondary kitchens or detached living structures on single-family lots. Securing the proper permits is non-negotiable; illegal additions can result in massive fines and complications when the property is eventually sold.

Will my adult child be taxed on the money I give them for the house?

Generally, no. Under current IRS regulations, individuals can gift up to a specific annual limit per recipient without having to file a gift tax return, and the lifetime exemption is substantial. The recipient of a gift typically does not pay income tax on it. However, if the transaction is structured as rent or a formal loan, the tax implications change. Always consult a tax professional to ensure you structure the financial transfer in the most tax-efficient manner possible.

Setting the Stage for Success

Embracing a multi-generational living arrangement represents a return to a community-focused way of aging. By consolidating expenses, sharing responsibilities, and fostering daily connections across generations, you can create a retirement environment that is both financially resilient and emotionally rich. The key to a seamless transition lies in removing assumptions from the equation. Talk openly about money, hire professionals to draft the necessary legal protections, and respect the boundaries of everyone under the shared roof.

Take the time to explore architectural options and draft a realistic household budget with your family before making any binding commitments. With thoughtful preparation, sharing a home can become one of the most rewarding decisions of your retirement journey.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, health needs, tax situation, and goals—may require different approaches. When in doubt, consult a licensed professional.

Last updated: April 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply