If you are struggling to make ends meet with limited income, Supplemental Security Income (SSI) provides a vital financial lifeline that pays up to $994 per month for individuals in 2026. This program is frequently confused with traditional Social Security retirement benefits; however, SSI is strictly a need-based program funded by general tax revenues rather than your lifetime work history. Navigating the stringent eligibility rules requires precise attention to detail, as even a minor oversight regarding your bank balance can trigger a suspension of your payments. Understanding exactly how the government measures your countable income and resources empowers you to secure the monthly assistance you need without falling into common regulatory traps.

Understanding the Difference: SSI vs. Traditional Social Security

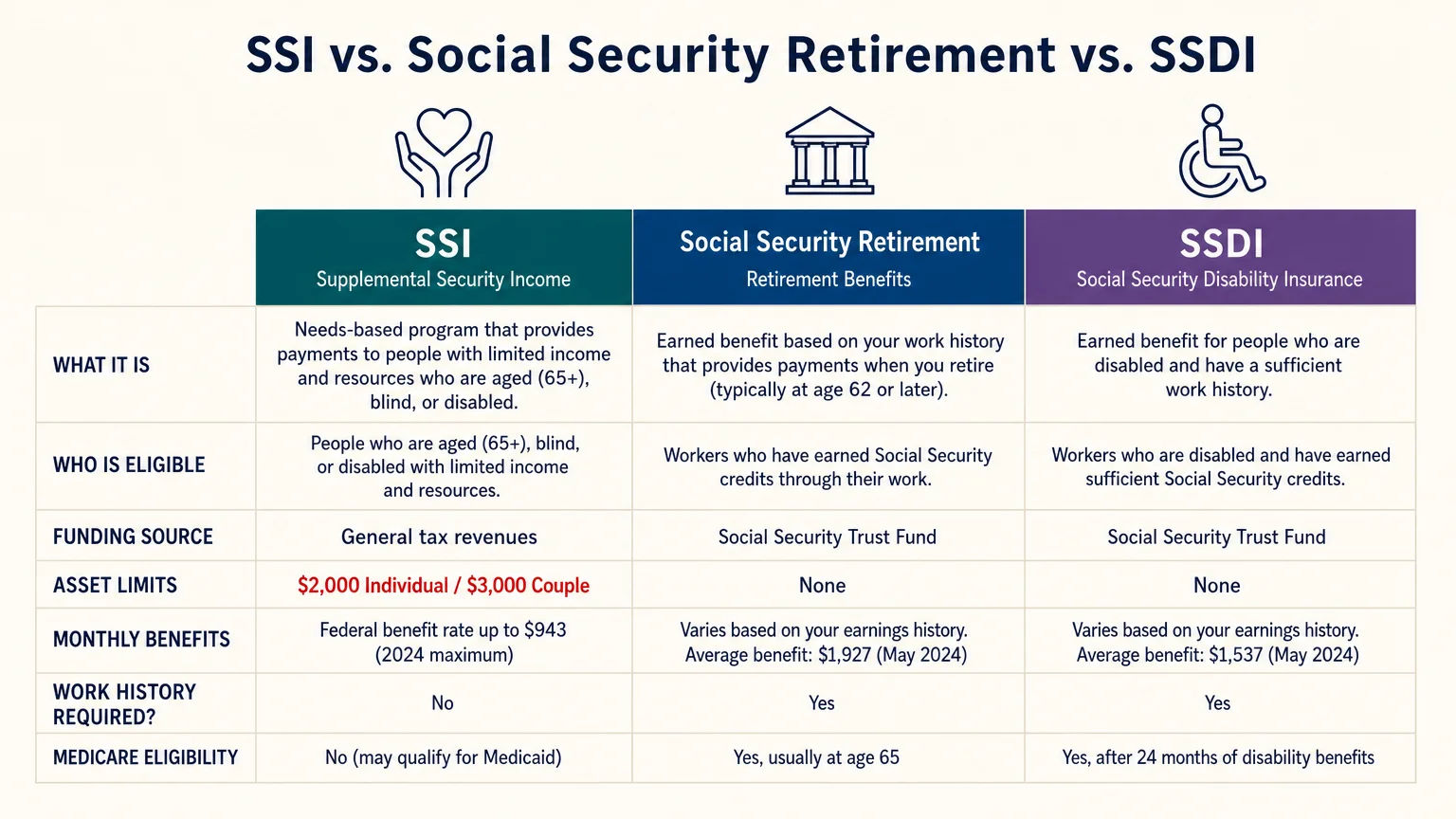

Many Americans use the term “Social Security” as a catch-all phrase for any government check sent to seniors. This creates massive confusion, particularly when you try to figure out which program you actually qualify for. To get the financial help you need, you must definitively separate Supplemental Security Income (SSI) from traditional Social Security Retirement and Social Security Disability Insurance (SSDI).

Traditional Social Security Retirement acts as an earned benefit. You spend decades working, paying payroll taxes into the Social Security Trust Fund, and accumulating work credits. Once you reach your early sixties, you can claim a monthly benefit based on your highest 35 years of earnings. Your personal wealth does not factor into this calculation at all; you could have millions sitting in a brokerage account and still collect your full Social Security Retirement check every month.

SSI operates under completely different operational rules. It functions as a safety net of absolute last resort. The federal government funds SSI through general tax revenues, not the dedicated Social Security taxes deducted from your weekly paycheck. You do not need a single day of work history to qualify. Instead, the program strictly evaluates your current state of financial distress. If you have almost no income and very few assets, SSI steps in to ensure you can afford basic survival needs like food and shelter.

SSDI sits somewhere in the middle of these two extremes. Like traditional retirement, SSDI requires a solid work history and regular payroll tax contributions. However, it pays out early if a severe medical condition forces you out of the workforce prematurely. Like regular Social Security, SSDI does not care how much money you have saved in your bank account, whereas SSI absolutely penalizes excess savings.

Here is a clear breakdown of how the three programs compare:

| Feature | SSI (Supplemental Security) | Social Security Retirement | SSDI (Disability Insurance) |

|---|---|---|---|

| Funding Source | General tax revenues | Social Security Trust Fund | Social Security Trust Fund |

| Primary Requirement | Extreme financial need and specific age/health criteria | Age (62+) and 40 lifetime work credits | Severe disability and sufficient work credits |

| Asset Limits | Strict ($2,000 individual / $3,000 couple) | None | None |

| Medical Review | Only required if applying under age 65 | None | Strict ongoing medical reviews |

Who Actually Qualifies for Supplemental Security Income?

The Social Security Administration enforces strict demographic and medical requirements before they even look at your wallet. To pass the first hurdle for SSI, you must meet specific age or health criteria, alongside rigid citizenship and residency rules.

You must fall into at least one of three specific categories:

- Age 65 or older: If you meet this age threshold, the process is straightforward. The SSA does not require you to prove a disability; your age alone satisfies this requirement.

- Legally blind: You must meet the federal definition of statutory blindness.

- Disabled: If you are under 65, you must prove that you have a severe physical or mental impairment that prevents you from performing any substantial gainful activity. This impairment must be expected to last at least 12 continuous months or result in death.

SSI is exclusively designed to support people living within the United States. You must be a U.S. citizen or national, or fall into a very specific category of qualified noncitizens. Furthermore, you must reside in one of the 50 states, the District of Columbia, or the Northern Mariana Islands. Interestingly, residents of Puerto Rico, the U.S. Virgin Islands, Guam, and American Samoa do not currently qualify for SSI, though legislative efforts continuously aim to change this exclusion.

If you leave the United States for a full calendar month or for 30 consecutive days, the SSA will immediately suspend your SSI benefits. You cannot receive payments again until you have been back in the country for 30 consecutive days.

Navigating the Strict Income Limits

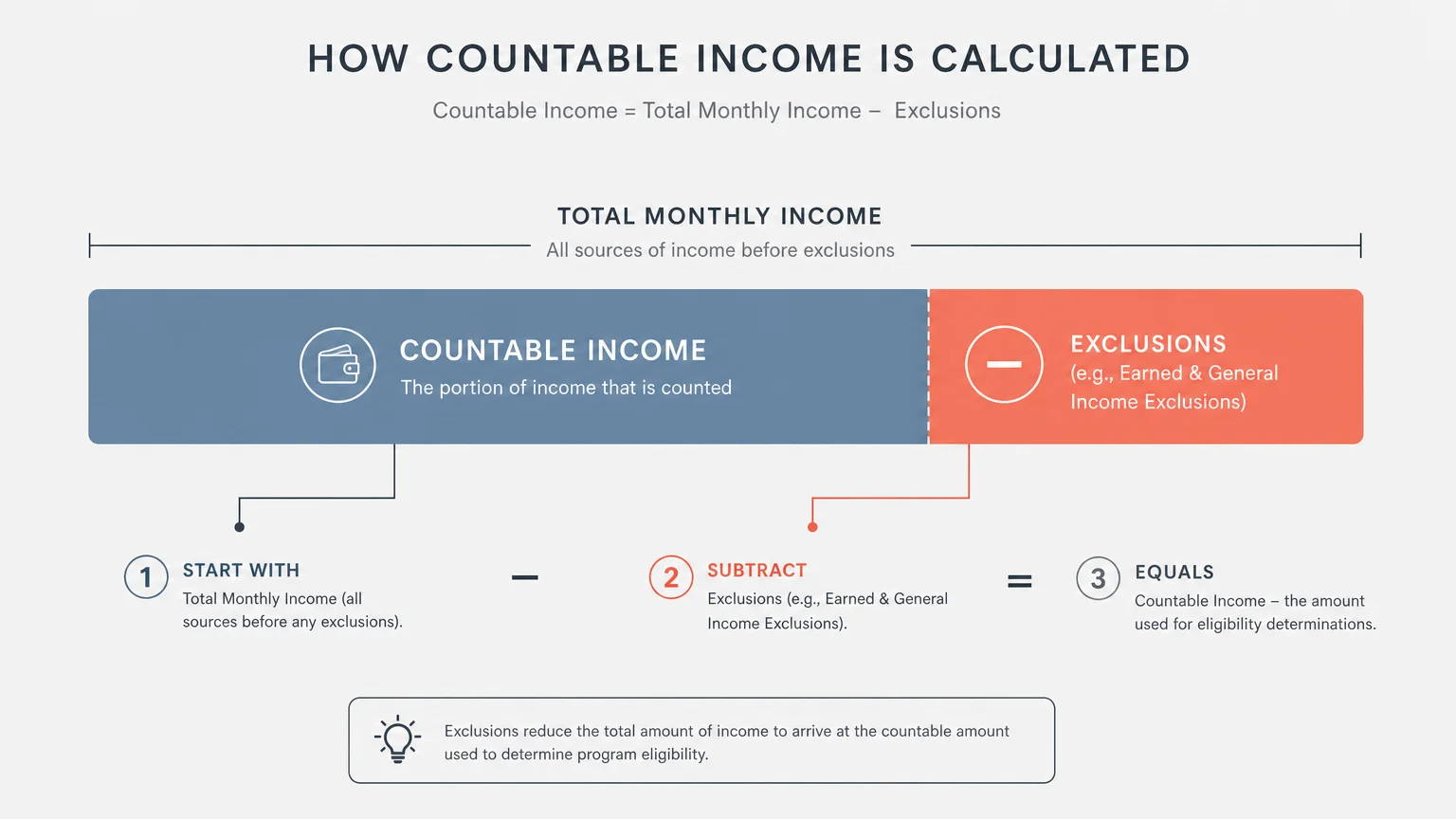

Passing the age or disability test is only the beginning. Next, the SSA places your daily finances under a microscope. The concept of “income” for SSI purposes is vastly broader than what you report to the IRS on tax day. The SSA defines income as anything you receive during a calendar month that you can use to pay for food or shelter.

The system treats the money you work for entirely differently than the money given to you. Unearned income includes pensions, unemployment benefits, state disability payments, gifts from family members, and even traditional Social Security checks. The SSA subtracts your unearned income from your maximum SSI benefit almost dollar-for-dollar. They do allow a small grace amount—the first $20 of general income you receive each month does not count against your benefit.

Earned income receives far more favorable treatment because the government actively wants to encourage recipients to work if they are physically capable. If you hold a job, the SSA ignores the first $65 of your monthly earnings (in addition to the $20 general exclusion, provided you did not use it on unearned income). After that initial exclusion, they only reduce your SSI benefit by $1 for every $2 you earn. This incentive structure ensures that working even a few hours a week leaves you financially better off than relying on benefits alone.

This is where many applicants get tripped up: In-Kind Support and Maintenance (ISM). If you live with an adult child who lets you stay in a spare bedroom rent-free and buys your weekly groceries, the SSA considers this financial support. Because someone else covers your basic survival needs, the SSA assigns a monetary value to that help and reduces your SSI check—often by exactly one-third of the maximum federal benefit rate.

Calculating Your Benefit: Practical Examples

Assume you live independently and receive a $400 monthly pension. Your countable income is $380 (the $400 pension minus the $20 general exclusion). To find your SSI payment, you subtract your countable income from the 2026 federal maximum of $994. In this scenario, you would receive an SSI check of $614 per month.

If you are married and both you and your spouse are eligible for SSI, the SSA looks at your combined household income. Suppose you have a combined unearned income of $600 from a small pension. First, you apply the single $20 general exclusion to the household, bringing your countable combined income to $580. You then subtract this $580 from the 2026 couple’s maximum benefit of $1,491. Your household would receive a monthly SSI check of $911. This combined calculation often frustrates applicants because the maximum benefit for a married couple is significantly less than two individual benefits added together—a systemic quirk commonly referred to as the SSI marriage penalty.

Demystifying the Resource Limit (The Asset Test)

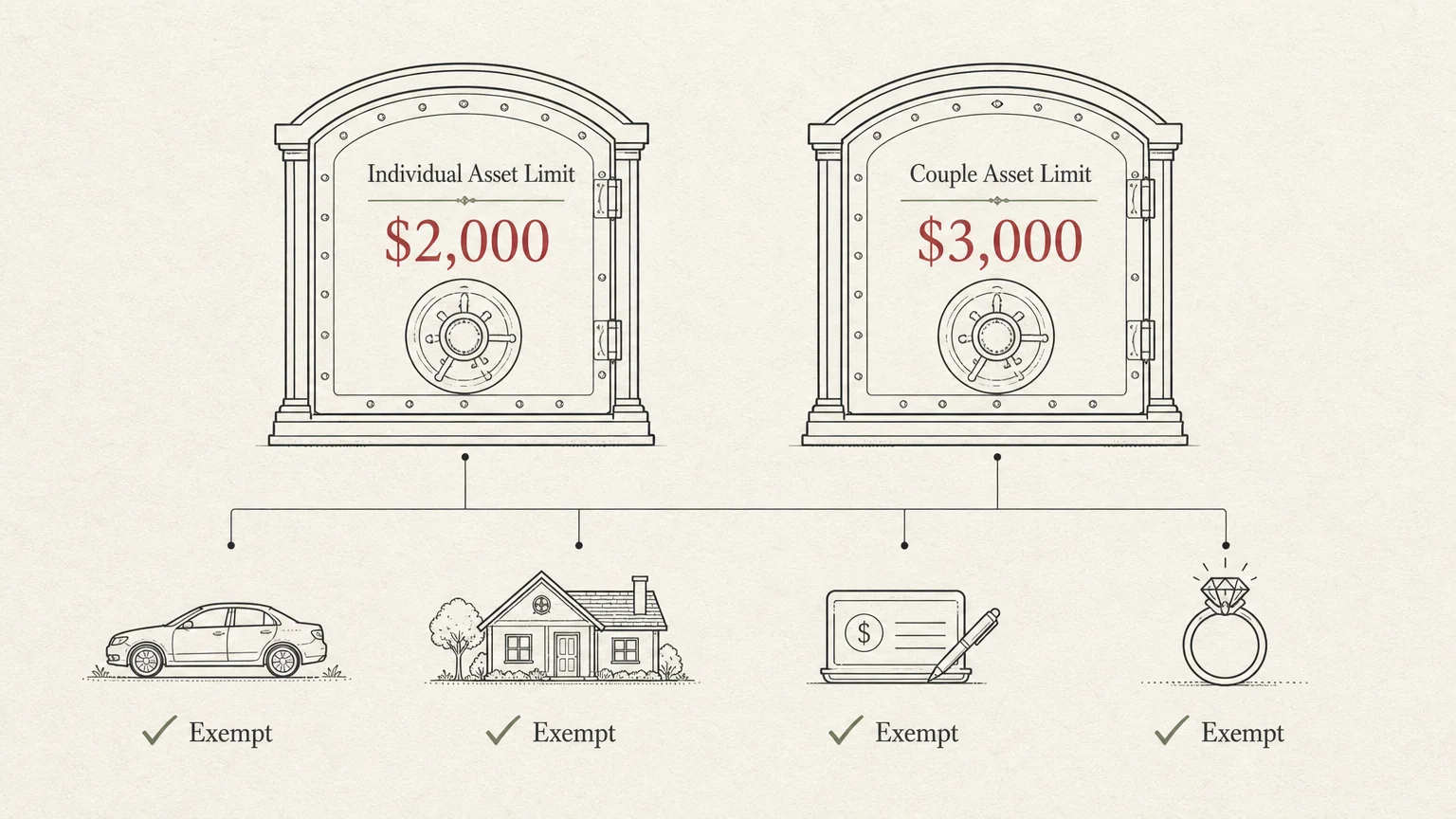

The resource limit stands as the most restrictive, heavily criticized, and unforgiving aspect of the entire SSI program. To qualify, your countable resources must not exceed $2,000 for an individual or $3,000 for a married couple where both spouses are eligible. These limits have remained entirely frozen since 1989, effectively punishing disabled and elderly individuals who manage to save even a tiny emergency fund.

Resources include cash on hand, bank account balances, stocks, bonds, mutual funds, and any real estate you own other than your primary residence. If you possess anything that could quickly be converted to cash to buy food or shelter, the SSA counts it against your limit.

Fortunately, the government recognizes that you need basic tools to survive and participate in society. Several significant assets are entirely excluded from the strict resource test. You do not have to count:

- The primary home you live in and the land it sits on, regardless of its current market value.

- One vehicle used for transportation for you or a member of your household.

- Household goods, furniture, and personal effects like clothing and wedding rings.

- Life insurance policies with a combined face value of $1,500 or less per person.

- Burial plots for yourself and your immediate family, plus up to $1,500 in dedicated burial funds.

- Property essential to self-support, such as tools used for a specific trade.

- Funds held in an ABLE (Achieving a Better Life Experience) account, up to $100,000.

What happens if you own two vehicles? The SSA will automatically exclude the vehicle with the highest equity value, provided it is used for transportation. The equity value of the second vehicle counts directly toward your $2,000 or $3,000 resource limit. Because used car prices remain robust, owning a second vehicle almost always disqualifies an applicant. You must either sell the second car for fair market value and spend down the cash on allowable expenses, or risk losing your monthly payments entirely.

ABLE accounts offer a unique workaround for specific individuals. If your qualifying disability began before you turned 46 (a threshold that expanded recently from the older age 26 limit), you can shelter substantial funds in an ABLE account without jeopardizing your SSI benefits.

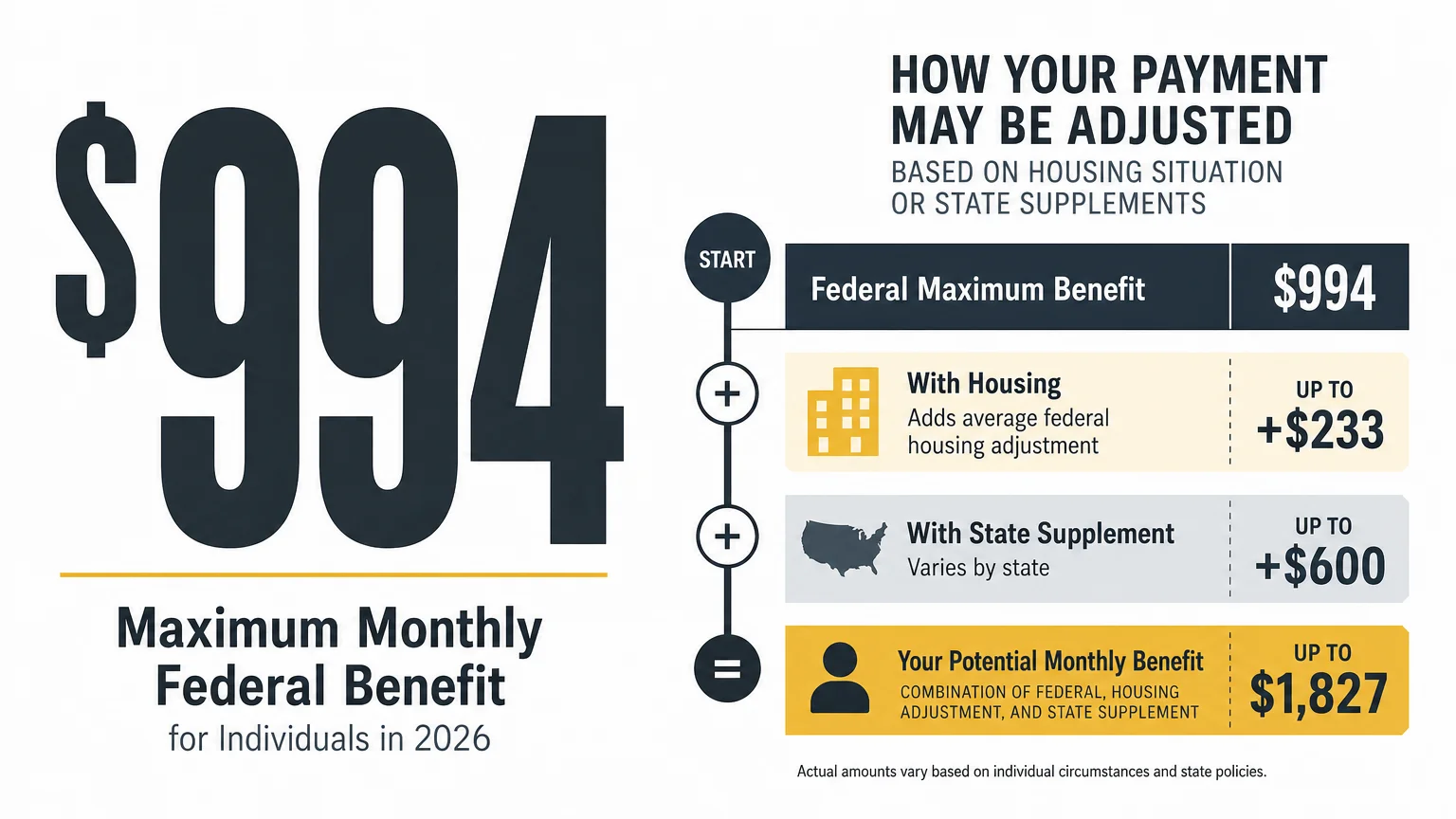

How Much Does SSI Pay in 2026?

Because SSI is tied directly to the cost of living, the maximum federal benefit rate increases in years when inflation drives up consumer prices. For 2026, after factoring in the annual cost-of-living adjustment, the federal maximum stands at $994 per month for an eligible individual and $1,491 per month for an eligible married couple.

Keep in mind that these figures represent the absolute ceiling, not a flat guaranteed payment. As demonstrated in the income section, the SSA aggressively deducts your countable income from this maximum baseline amount.

Where you live plays a major role in your final monthly payment. Recognizing that $994 does not stretch far in high-cost areas, many states provide a State Supplementary Payment that stacks directly on top of the federal base. California, New York, Massachusetts, and New Jersey, among others, add varying amounts depending on your specific living arrangement. For instance, a state might offer a significantly higher supplement if you live in an assisted living facility rather than your own independent apartment.

Conversely, residents of states like Arizona, Mississippi, North Dakota, and West Virginia receive only the federal amount, as these states do not offer a supplement of any kind. When you apply, the SSA or your state’s human services department will determine if you qualify for this extra financial boost.

The dollar amount printed on your SSI check represents only half the story. In most states, qualifying for even $1 of SSI automatically qualifies you for Medicaid, overseen by the Centers for Medicare & Medicaid Services (CMS). This healthcare coverage is incredibly comprehensive, covering doctor visits, hospital stays, prescription drugs, and even long-term nursing home care—expenses that routinely bankrupt seniors. Additionally, SSI recipients generally find it much easier to qualify for the Supplemental Nutrition Assistance Program (SNAP) to help cover escalating grocery costs.

The Application Process Explained

Do not let the complexity of the bureaucratic rules prevent you from applying. If you suspect you meet the income and resource limits, start the application process immediately. The SSA does not backdate benefits to the day you became disabled or turned 65; they only pay back to the exact month you formally submit your application.

You have three convenient options to begin the process:

- Online: You can start the process on the official Social Security Administration (SSA) website. The online portal allows you to complete the bulk of the application at your own pace from home.

- By Phone: You can call the SSA’s toll-free number to schedule a telephone appointment with a representative who will patiently walk you through the forms.

- In Person: You can schedule an appointment at your local Social Security office for direct face-to-face assistance.

The SSA demands hard evidence to verify your claims. Before your interview, assemble your birth certificate, proof of U.S. citizenship or lawful alien status, your Social Security card, and a copy of your current lease or mortgage. You must also provide exhaustive financial records. Bring statements for all checking and savings accounts, life insurance policies, vehicle registrations, and proof of any income you currently receive. If you are applying based on a disability rather than age, you must also submit extensive medical records, contact information for all your doctors, and a detailed chronological work history.

Pitfalls to Watch For

The severe constraints of the SSI program make it a dangerous minefield for the uninformed. A single innocent mistake can trigger a devastating overpayment notice, legally requiring you to pay back thousands of dollars to the federal government.

If you realize you have $5,000 in the bank and decide to simply give $3,000 to your grandchild so you can slip under the $2,000 resource limit, stop immediately. The SSA strictly enforces a 36-month lookback period. If you transfer assets for less than fair market value within three years of applying, the SSA imposes a penalty period. You will be disqualified from receiving benefits for up to 36 months, directly depending on the monetary value of the assets you gave away.

The SSA tests your resources on the very first moment of the first day of the calendar month. If your bank account balance reads $2,050 at 12:01 AM on October 1st, you are disqualified for the entire month of October. It does not matter if you pay your $800 rent later that exact same afternoon. You must aggressively manage your cash flow to ensure your balance drops below the threshold before the month turns over.

“By failing to prepare, you are preparing to fail.” — Benjamin Franklin

Many seniors share a joint bank account with an adult child for convenience, allowing the child to help pay bills or buy groceries. The SSA treats all money in a joint account as fully belonging to the SSI applicant, regardless of who actually deposited the funds. If your daughter keeps $3,000 of her own money in your shared checking account, the SSA views that as your money, immediately pushing you over the resource limit. You must keep your finances strictly separated from anyone whose income should not be counted against you.

Failing to report changes in income, resources, or living arrangements is the most common cause of benefit suspensions. If your spouse gets a part-time job, or if an adult child moves in and starts paying half the rent, you must report this to the SSA within 10 days of the end of the month in which the change occurred.

Getting Expert Help

Because the rules surrounding SSI are so rigid, certain situations absolutely require professional intervention. You do not have to navigate complex bureaucratic hurdles alone. Seeking help from a qualified disability attorney, a certified financial planner, or a local senior advocate—such as those affiliated with the National Council on Aging (NCOA)—can protect your vital lifeline.

Consider seeking professional guidance in these specific scenarios:

You Receive an Overpayment Notice

If the SSA determines they paid you too much due to a fluctuating bank balance or a miscalculated income stream, they will demand the money back. Do not ignore these threatening letters. An advocate can help you immediately file a Request for Reconsideration or a Request for Waiver of Overpayment Recovery, especially if the error was not your fault and repaying it would cause severe financial hardship.

Your Living Arrangements Trigger an ISM Reduction

If your benefits are slashed by one-third because the SSA claims someone else is paying for your food and shelter, a professional can help you document your living situation differently. Structuring a formal, legally binding rental agreement with your family members or proving that you pay your fair pro-rata share of household expenses can successfully restore your full benefit amount.

You Need to Establish a Special Needs Trust

If you expect to receive a sudden influx of cash—such as an inheritance, a legal settlement, or a life insurance payout—it will immediately push you over the $2,000 resource limit. An attorney who specializes in elder law can help you quickly establish a Special Needs Trust. This legal vehicle holds the funds for your supplemental care without counting as a resource against your ongoing SSI eligibility.

You Are Applying for SSDI and SSI Concurrently

If your work history is sporadic, you might qualify for a small SSDI check that does not reach the SSI maximum. You can apply for both programs simultaneously. A disability advocate can ensure the applications are coordinated properly so you receive the absolute maximum combined benefit allowed by law.

Frequently Asked Questions About SSI

Can I receive both regular Social Security and SSI at the same time?

Yes, provided your traditional Social Security check is low enough. If your regular retirement or disability benefit is less than the SSI maximum ($994 in 2026), you can receive SSI to bridge the gap. The SSA counts your regular Social Security as unearned income, subtracts the $20 general exclusion, and uses SSI to top off your total income to the federal limit.

Do I have to pay taxes on my SSI benefits?

No. Unlike traditional Social Security benefits, which can be subject to federal income tax if your overall income is high enough, Supplemental Security Income is never taxable. You do not even need to report it as income on your annual federal tax return.

Will my spouse’s income affect my eligibility?

Absolutely. The SSA uses a process called “deeming.” If you are married and living with your spouse, the SSA automatically assumes a portion of your spouse’s income and resources are available to you, even if they aggressively keep their money in a completely separate bank account. This combined evaluation can easily push you over the strict asset and income limits.

How long does the application process take?

If you apply based purely on age (65+), the process is relatively quick and can be successfully resolved in a matter of weeks. If you apply based on disability, it routinely takes three to six months for the state Disability Determination Services to review your extensive medical records. If your initial application is denied and you must formally appeal, the process can stretch over a year.

What happens if I inherit money while receiving SSI?

An inheritance is considered unearned income in the exact month you receive it. If the amount pushes your total income over the limit, your SSI benefit will be suspended for that specific month. If you retain the funds into the following month, the remaining balance counts directly as a resource. If that balance pushes you over the $2,000 limit, your benefits remain suspended until you spend down the money on allowable expenses or transfer it into a protected vehicle like a Special Needs Trust.

Taking the Next Step

Navigating the complexities of Supplemental Security Income requires patience, meticulous daily record-keeping, and a clear understanding of the strict federal guidelines. While the income and asset limits are undeniably frustrating to manage, the resulting monthly financial assistance and automatic healthcare coverage can completely transform your daily quality of life.

Do not let the fear of bureaucratic paperwork keep you from accessing the vital support you deserve. Gather your financial documents, honestly evaluate your countable resources, and reach out to the Social Security Administration or a local senior advocate to begin your application process today. This is educational content based on general retirement and financial principles. Individual results vary based on your situation. Always verify current benefit rules, tax laws, and eligibility requirements with official sources like SSA, Medicare.gov, or the IRS.

Last updated: June 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply