Relocating for retirement often feels like the ultimate reward for decades of hard work, but moving to a postcard-perfect destination without analyzing the financial and lifestyle realities frequently leads to expensive buyer’s remorse. Every year, thousands of retirees pack up their homes in pursuit of eternal sunshine, lower income taxes, or ocean views, only to discover hidden costs and cultural mismatches that threaten their nest eggs and daily happiness. Soaring homeowners insurance premiums, overtaxed healthcare systems, and extreme weather patterns are forcing many seniors to pack their bags a second time. Before you hire movers and sell your current home, examine why these five popular relocation states consistently generate the highest levels of regret among retirees.

The Hidden Math of Retirement Relocation

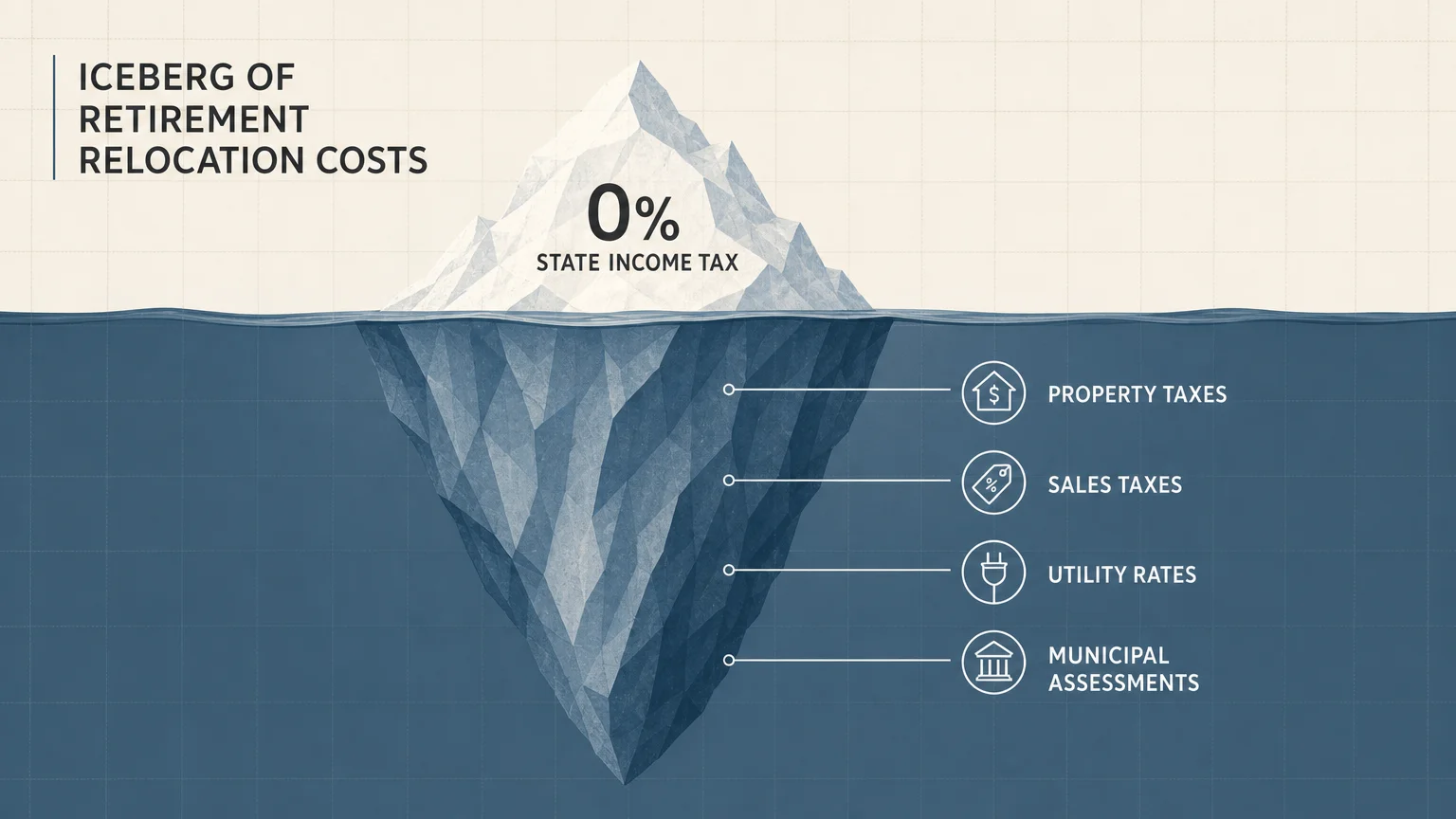

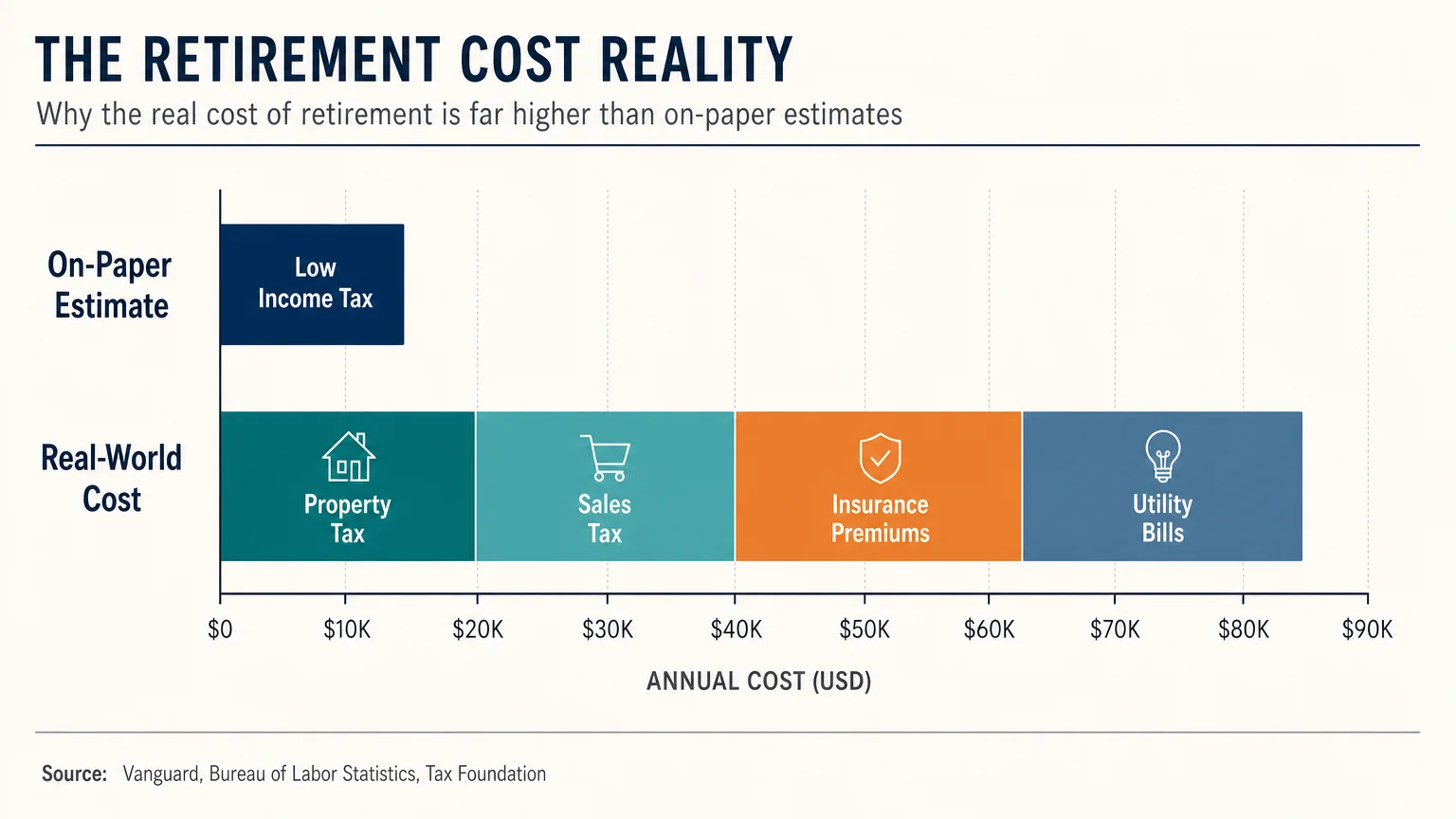

When you start researching the best places to retire, state income tax rates usually dominate the conversation. Financial publications heavily promote the nine states with no individual income tax, framing them as safe havens for your fixed income. Relying solely on income tax data creates a dangerous blind spot. State governments require revenue to maintain infrastructure, fund public schools, and provide emergency services. If a state does not collect income tax, it will inevitably recover that revenue through other channels—typically property taxes, sales taxes, vehicle registration fees, or specialized municipal assessments.

Beyond the tax code, you must evaluate the micro-economy of your target destination. Housing costs, utility rates, and specialized medical care vary wildly not just from state to state, but from county to county. A state that looks incredibly affordable on paper might possess structural flaws—like an unstable insurance market or a severe shortage of primary care physicians—that directly impact your daily quality of life. Evaluating a state requires you to look past the marketing brochures and analyze the actual living conditions experienced by full-time residents.

“A big part of financial freedom is having your heart and mind free from worry about the what-ifs of life.” — Suze Orman, Personal Finance Expert

Florida: The Sunshine State’s Insurance Crisis

Florida has reigned as the undisputed champion of retirement relocation for decades. The promise of warm winters, endless golf courses, and zero state income tax creates an incredibly compelling pitch. However, the modern reality of living in Florida is pushing many retirees to their financial breaking point, sparking a mass exodus of seniors seeking stability elsewhere.

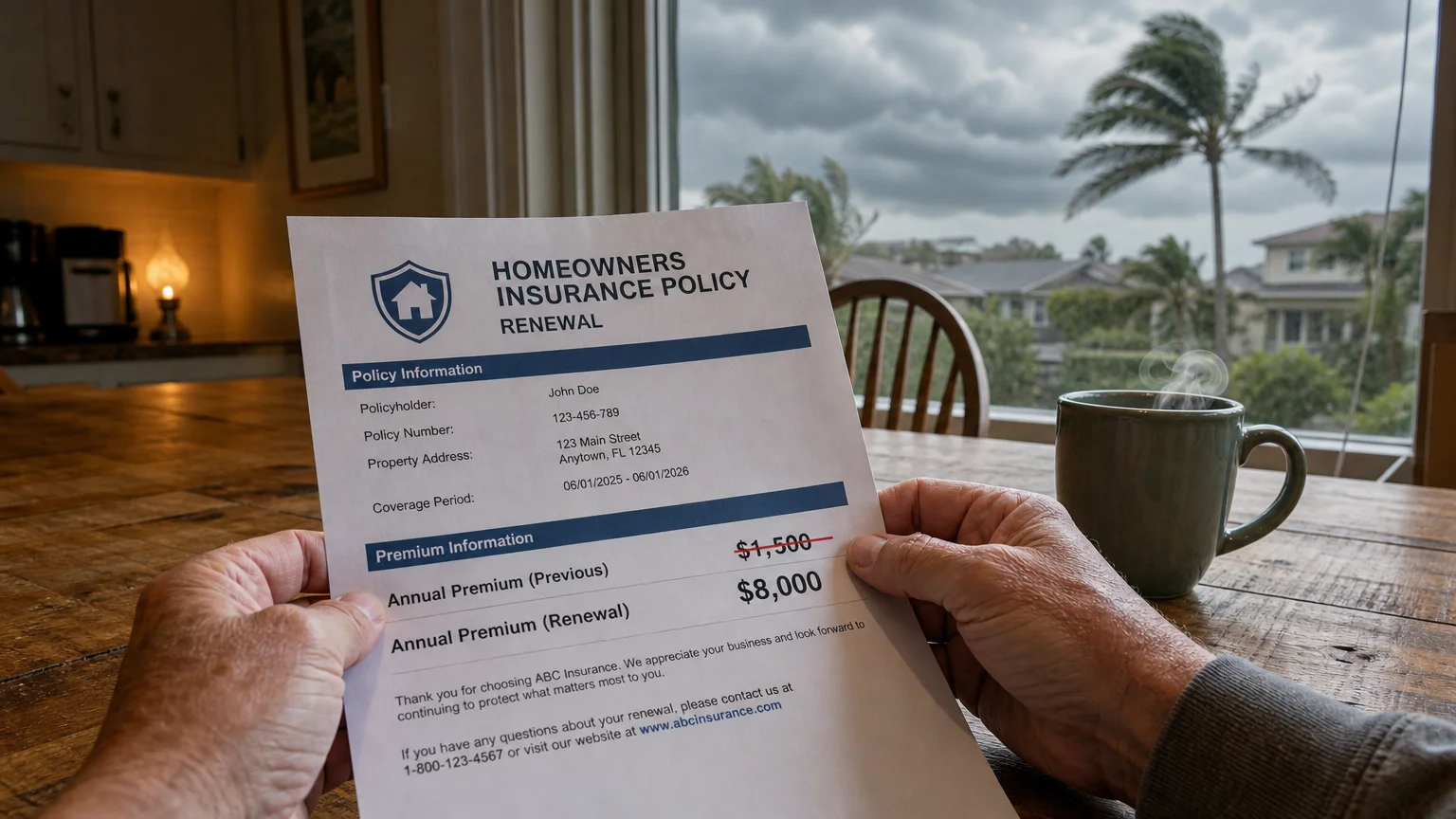

The primary source of regret is the collapse of the property insurance market. Natural disasters and widespread litigation have driven several major insurance carriers out of the state entirely. Retirees who budgeted a modest $1,500 a year for homeowners insurance are suddenly facing premiums exceeding $6,000 to $8,000 annually. If you purchase a home near the coast, mandatory flood insurance adds another massive layer of expense.

Furthermore, condominium living—once the affordable entry point for Florida retirees—has become a financial minefield. Following recent legislative changes aimed at preventing structural failures, condo associations must now fully fund their reserve accounts. Retirees living on fixed incomes are receiving special assessment bills running into the tens of thousands of dollars to cover delayed maintenance on roofs, concrete, and elevators. Add in the increasingly oppressive summer heat and humidity that keeps residents trapped indoors from May through October, and the Florida dream quickly loses its luster.

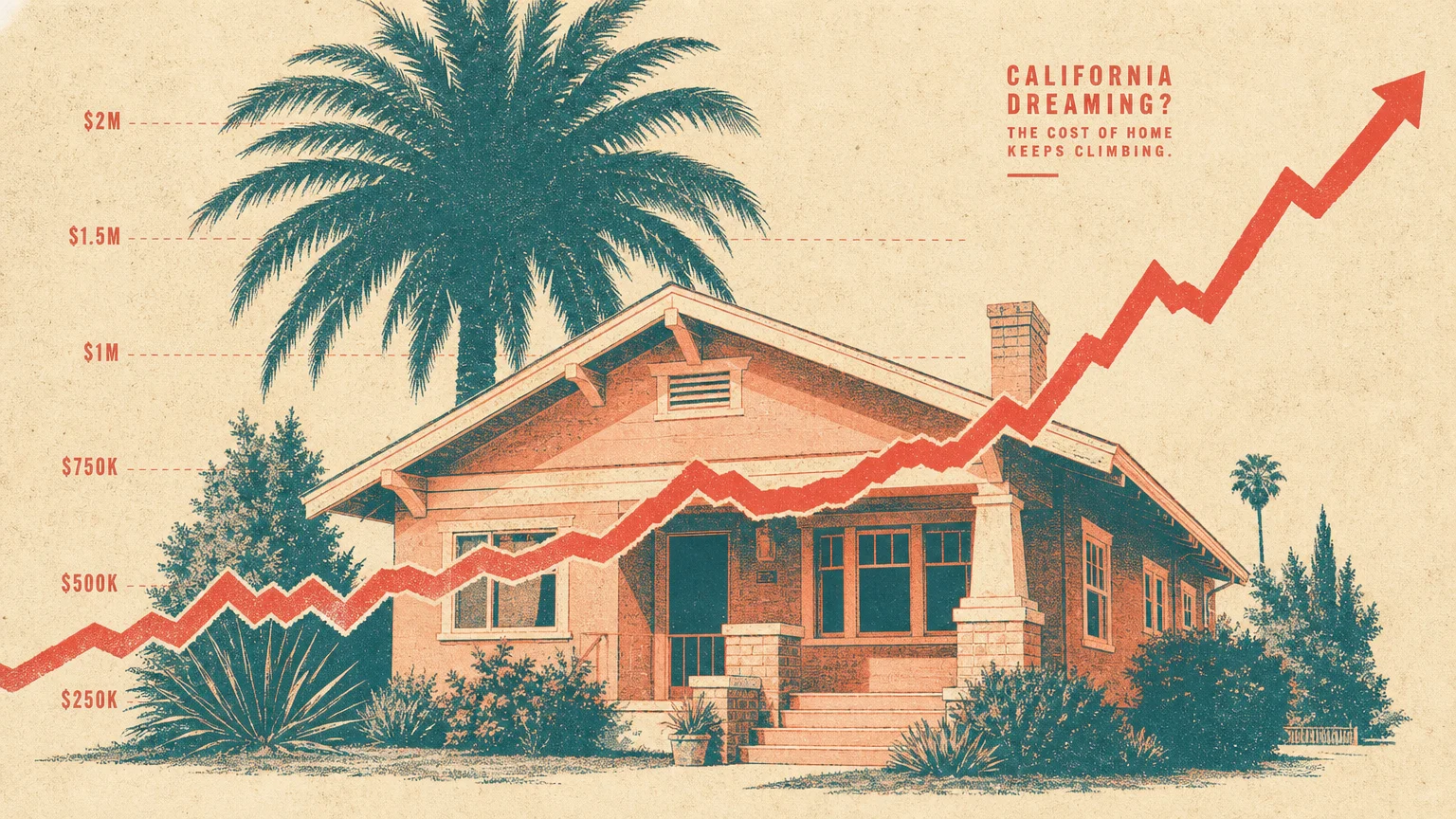

California: Where Housing Costs Devour Fixed Incomes

California offers arguably the best weather in the country, world-class healthcare facilities, and diverse geography ranging from beaches to mountains. Unsurprisingly, it also generates intense regret for retirees who attempt to maintain their previous standard of living while absorbing the state’s punishing cost of living.

Housing is the central issue. Even if you plan to downsize, purchasing a modest home in a desirable California community requires a massive capital outlay. While long-time residents benefit from Proposition 13—which strictly caps property tax increases—new buyers face property tax assessments based on the current, highly inflated purchase price. Tying up the majority of your retirement nest egg in home equity leaves you vulnerable to routine market fluctuations and severely reduces your liquid cash flow.

Daily expenses also erode your budget at an accelerated pace. California consistently ranks among the highest in the nation for state income taxes, and unlike some states, it taxes distributions from traditional IRAs and 401(k)s. Gasoline prices, grocery bills, and utility rates far exceed national averages. For retirees who did not accumulate substantial wealth, the constant financial friction creates pervasive anxiety, forcing many to leave the state simply to preserve their savings.

Arizona: Extreme Heat and Rising Resource Costs

For years, Arizona served as the more affordable, dry-climate alternative to Florida. Retirees flocked to Phoenix, Scottsdale, and Tucson to escape harsh midwestern winters. Today, the sheer volume of people who relocated to the state has fundamentally altered its affordability and livability.

The climate reality is the most frequent shock for new arrivals. The phrase “it is a dry heat” offers little comfort when temperatures exceed 110 degrees for weeks at a time. This extreme weather completely alters the retiree lifestyle. During the summer months, outdoor activities become physically dangerous, leading to a phenomenon known as “summer seasonal affective disorder.” You essentially trade being snowed in for being heat-bound, resulting in soaring electricity bills just to keep your home habitable.

Additionally, water scarcity is a looming economic threat. As levels in the Colorado River decline, municipalities are being forced to invest in expensive water management infrastructure, passing those costs directly to consumers through rising utility rates. Housing prices have also surged as remote workers and out-of-state investors aggressively bought up inventory. Retirees who move to Arizona expecting a low-cost desert oasis often find themselves paying premium prices for an increasingly strained environment.

New York: The Tax Burden That Pushes Retirees Away

Retirees who choose to stay in or move to New York typically do so for cultural reasons, proximity to family, or access to exceptional medical centers. Unfortunately, the sheer expense of remaining in the Empire State frequently forces a painful reassessment. New York routinely ranks near the bottom of retirement affordability metrics, and the burden extends far beyond New York City.

The property tax situation in New York is notoriously severe. Retirees living in upstate communities or the surrounding suburbs often pay well over $10,000 annually in property taxes for moderately priced homes. A significant portion of these taxes funds local school districts. While well-funded schools benefit the community, absorbing constant tax hikes is incredibly difficult when your income relies entirely on Social Security and portfolio withdrawals.

Weather is the other major catalyst for regret. Aging bodies tolerate snow, ice, and freezing winds poorly. The physical demands of winter maintenance—shoveling driveways, managing heating oil deliveries, and winterizing homes—become dangerous burdens. Paying contractors to handle these tasks introduces another recurring expense to the winter budget. When you combine high state income taxes, aggressive local taxes, and brutal winters, New York becomes a highly hostile environment for the average retirement account.

Nevada: Healthcare Shortages in the Desert

Nevada aggressively markets itself to retirees by highlighting its lack of state income tax and the entertainment value of the Las Vegas and Reno areas. While it successfully attracts thousands of seniors looking to shield their pension and investment income, Nevada harbors a major infrastructure problem that deeply impacts aging residents: a critical shortage of medical professionals.

The state’s population growth has vastly outpaced its healthcare infrastructure. Nevada consistently ranks near the bottom nationwide regarding the number of primary care physicians and specialists per capita. When retirees develop complex medical conditions requiring cardiologists, neurologists, or rheumatologists, they frequently encounter wait times stretching for months. In acute medical situations, many Nevada retirees feel forced to cross state lines, seeking treatment in California or traveling to the Mayo Clinic in Arizona.

Financial benefits mean very little if you cannot access quality healthcare when you need it most. Furthermore, the cost of living in Nevada is no longer cheap. Car insurance rates in the Las Vegas valley are among the highest in the country, and housing prices have dramatically escalated. Retirees who moved for the tax breaks often regret trading away the robust healthcare networks they enjoyed in their previous home states.

Comparing the Cost of Living Realities

To understand the trade-offs of these locations, you must look at how different financial pressures interact. A zero percent income tax rate offers no protection against severe housing or healthcare challenges.

| State | State Income Tax | Primary Financial Threat | Major Lifestyle Complaint |

|---|---|---|---|

| Florida | None | Exploding property insurance and HOA assessments | Overcrowding and oppressive summer humidity |

| California | Up to 13.3% (Highest bracket) | Astronomical housing costs and property tax reset upon purchase | Traffic congestion and high daily living costs |

| Arizona | 2.5% (Flat rate) | High summer utility costs and rising water expenses | Extreme heat limiting outdoor activities for half the year |

| New York | Up to 10.9% | Severe local property taxes and school taxes | Harsh winters requiring expensive physical maintenance |

| Nevada | None | High auto insurance and rising housing costs | Severe shortage of medical specialists and primary care doctors |

What Can Go Wrong: The Costs of a Re-Do Move

Failing to accurately assess a relocation destination frequently results in the “halfback” phenomenon—a term originally used to describe retirees who moved all the way from the Northeast to Florida, realized they hated it, and moved “halfway back” to states like the Carolinas or Tennessee. Executing a second move because of buyer’s remorse severely damages your retirement finances.

When you buy and sell real estate in rapid succession, the transaction costs devour your wealth. Consider the standard expenses of selling a home: 5% to 6% in real estate agent commissions, closing costs, staging fees, and local transfer taxes. Next, factor in the cost of hiring professional interstate movers, which easily ranges from $5,000 to $15,000 depending on distance and volume. Moving twice in a three-year period can easily wipe $50,000 to $80,000 off your net worth without generating a single tangible benefit.

Beyond the financial damage, the emotional and physical toll of a failed relocation is heavy. Leaving behind established social circles, beloved local restaurants, and trusted doctors only to realize your new destination does not fit your needs leads to intense isolation. Rebuilding a social network in your late sixties or seventies requires energy; doing it twice due to a geographic mistake can be exhausting.

Strategic Steps to Prevent Relocation Regret

Protecting yourself from an expensive moving mistake requires patience and methodical research. Do not let vacation memories dictate your permanent living arrangements. Spending a week at a resort in Scottsdale in February provides zero insight into what living there in August feels like.

- Rent Before You Buy: The single most effective strategy to prevent regret is signing a six-month or one-year lease in your target community. Renting allows you to experience the local weather, traffic, and culture during the off-season. It also gives you time to understand the local real estate market before committing your capital.

- Calculate the Total Tax Burden: Do not fixate on income tax. Utilize resources from financial organizations like AARP to map out the total local tax burden. Factor in property taxes, sales taxes on groceries and clothing, vehicle registration, and municipal utility taxes.

- Verify Healthcare Availability: Call local primary care clinics in your target zip code and ask if they are accepting new Medicare patients. If the wait list is six months long, you have identified a major systemic issue.

- Test Your Budget: Use cost of living calculators provided by platforms like Bankrate to compare exact expenses between your current city and your destination. Pay specific attention to the cost of groceries and utilities.

When to Consult a Professional

Relocating across state lines involves complex legal and financial mechanics. Seeking professional guidance before you list your house ensures you do not trigger unnecessary tax events or lose crucial benefits.

- Establishing Legal Domicile: If you are moving from a high-tax state to a low-tax state but plan to spend time in both, your former state may aggressively audit you to claim you are still a resident. A Certified Public Accountant (CPA) will help you establish a clear, legally defensible domicile in your new state.

- Evaluating Health Coverage: Medicare Advantage plans and Medicare Part D prescription plans are highly dependent on your specific county and zip code. Before moving, consult a licensed Medicare broker or utilize the tools on Medicare.gov to ensure your preferred doctors and medications are covered in your new location.

- Running Long-Term Projections: A fee-only fiduciary financial planner can run a Monte Carlo simulation on your portfolio. This mathematical stress test will show you exactly how a higher property tax bill or increased insurance premiums will impact your portfolio survival rate over a thirty-year retirement.

Frequently Asked Questions About Retirement Relocation

Is it actually worth moving to a state with no income tax?

It depends entirely on your income structure and the specific state’s alternative taxes. If the bulk of your retirement income comes from tax-free Roth IRA withdrawals or Social Security (which many states do not tax anyway), a no-income-tax state provides very little benefit. You must weigh the income tax savings against the state’s property taxes, sales taxes, and general cost of living.

How do rising homeowners insurance rates impact retirees?

Because retirees live on fixed or carefully managed incomes, sudden spikes in mandatory expenses directly reduce their standard of living. If your insurance goes up by $400 a month, that is $400 you must pull from your grocery, travel, or healthcare budget. If you cannot afford the premium and drop your wind or flood coverage, you risk losing your entire primary asset in a single storm.

What does it mean to be a “halfback” retiree?

A halfback is a retiree who moves from the Northeast or Midwest to the Deep South (typically Florida), experiences regret due to the extreme heat, crowding, or costs, and subsequently moves halfway back up the coast. These retirees often settle in states like North Carolina, South Carolina, or Virginia, seeking a moderate climate with four distinct but mild seasons.

How does moving out of state affect my Medicare coverage?

Original Medicare (Part A and Part B) is a federal program and remains valid at any doctor or hospital that accepts Medicare anywhere in the United States. However, if you use a Medicare Advantage plan (Part C) or a standalone prescription drug plan (Part D), these are managed by private insurers with regional networks. Moving out of your plan’s service area triggers a Special Enrollment Period, requiring you to select a new plan in your new state.

Making the decision to relocate should empower your retirement, not restrict it. Taking the time to aggressively vet a destination protects the wealth you spent a lifetime building. Focus on communities that align with your daily habits, support your health requirements, and respect your financial boundaries. The information in this guide is meant for educational purposes. Your specific circumstances—including income, health needs, tax situation, and goals—may require different approaches. When in doubt, consult a licensed professional.

Last updated: March 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

We are planning to move to NY within this year.

Keeping a small rental in Pa near my work

Where I will need to be for the next 12 months

We are looking at $550,000 to $650,000

High rise costs are about $750 taxes and $850 maintenance

No mortgage

I feel you can live cheaply there and have best medical at you finger tips

Is this not a smart idea