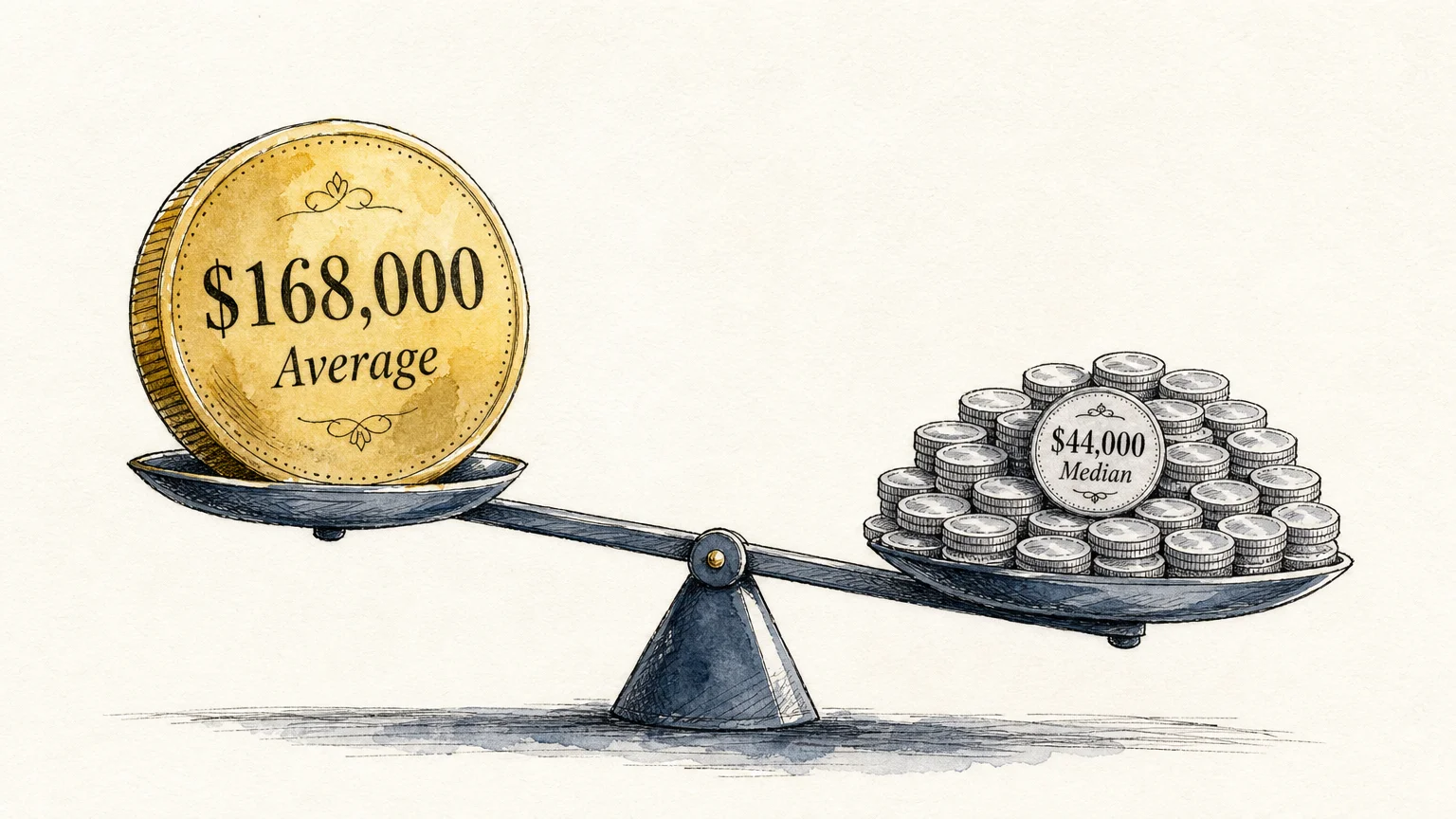

Are your retirement savings keeping pace with your age, or are you quietly falling behind? Comparing your 401(k) balance against national averages is a highly effective way to gauge your financial health and course-correct before retirement arrives. In 2026, data reveals a stark reality: while the average overall 401(k) balance sits near $168,000, the median balance is just over $44,000. That massive gap means a small group of super-savers is skewing the numbers, leaving everyday workers wondering where they truly stand. Understanding the exact benchmarks for your specific age group empowers you to set realistic goals, adjust your contribution rates, and take full advantage of the latest IRS limits to secure your financial future.

The Difference Between Average and Median 401(k) Balances

When reviewing financial statistics, the distinction between the average and the median fundamentally changes how you interpret the data. The average, or mean, is calculated by adding all account balances together and dividing by the total number of accounts. Because workplace retirement plans have no maximum limit on the total balance you can accumulate over a lifetime, a small percentage of highly compensated executives with multi-million-dollar portfolios pulls the mathematical average dramatically upward. This distortion often leaves ordinary savers feeling hopelessly behind.

The median represents the exact middle point of all savers. If you line up every 401(k) participant from the lowest balance to the highest, the median is the person standing dead center. Half of the people have more; half have less. If your balance aligns with or exceeds the median for your age group, you are effectively ahead of 50 percent of your peers. While the average shows what is possible with a high income and aggressive saving habits, the median paints a much more accurate, grounded picture of the typical American worker’s financial reality.

Average 401(k) Balance by Age in 2026

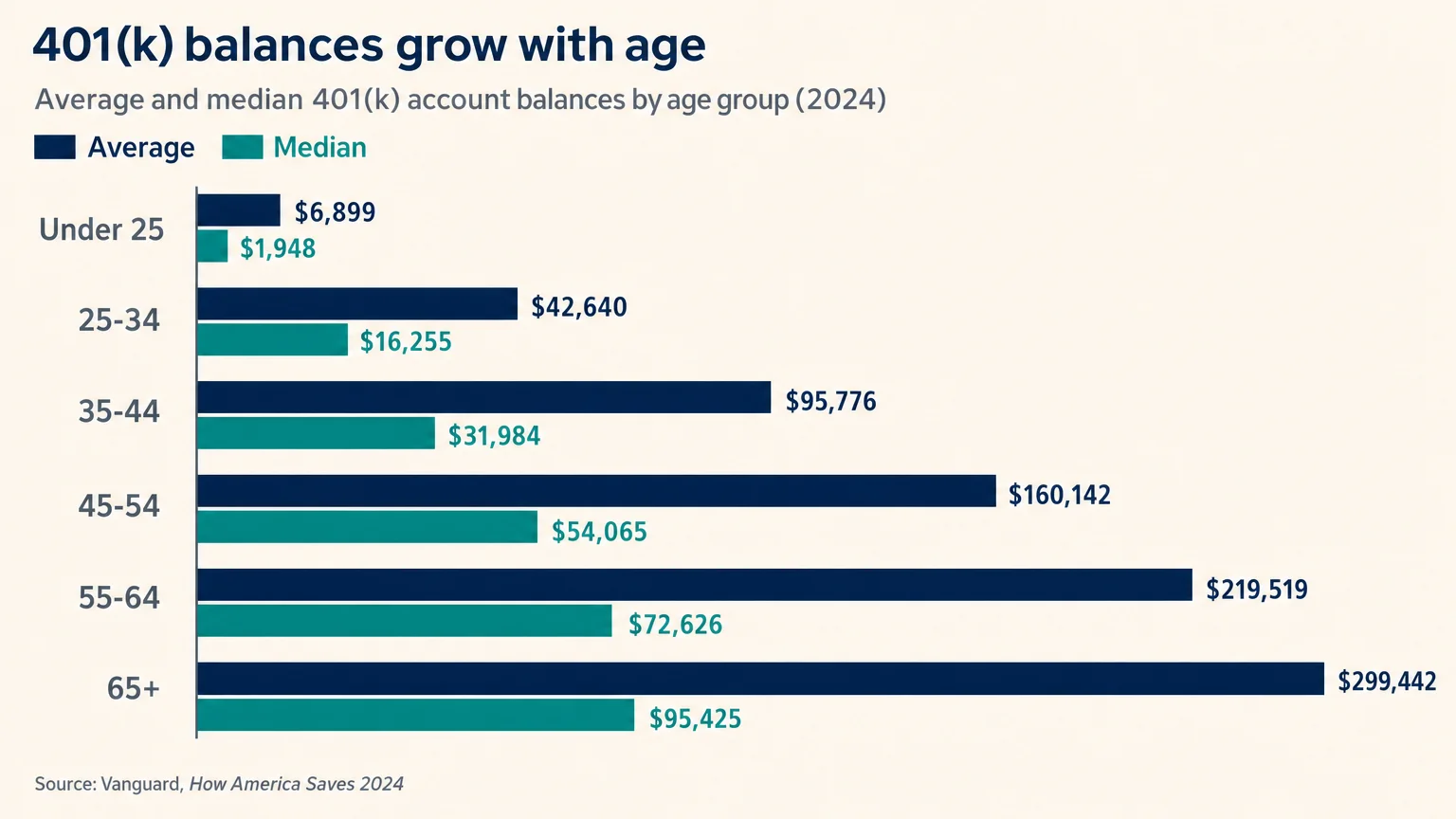

To accurately benchmark your progress, you need data that reflects a broad swath of the American workforce. Vanguard, one of the largest retirement plan administrators in the country, consistently tracks millions of participant accounts to compile its comprehensive annual data. Their latest figures reveal exactly how much people hold in their workplace accounts across different stages of life.

| Age Bracket | Average 401(k) Balance | Median 401(k) Balance |

|---|---|---|

| Under 25 | $6,899 | $1,948 |

| 25 to 34 | $42,640 | $16,255 |

| 35 to 44 | $103,552 | $39,958 |

| 45 to 54 | $188,643 | $67,796 |

| 55 to 64 | $271,320 | $95,642 |

| 65 and older | $299,442 | $95,425 |

Decoding the Numbers: Where You Stand by Decade

Looking at raw numbers only tells part of the story. Your financial priorities, challenges, and strategies must evolve as you move through each decade of your career. Here is what the data implies for your current stage of life.

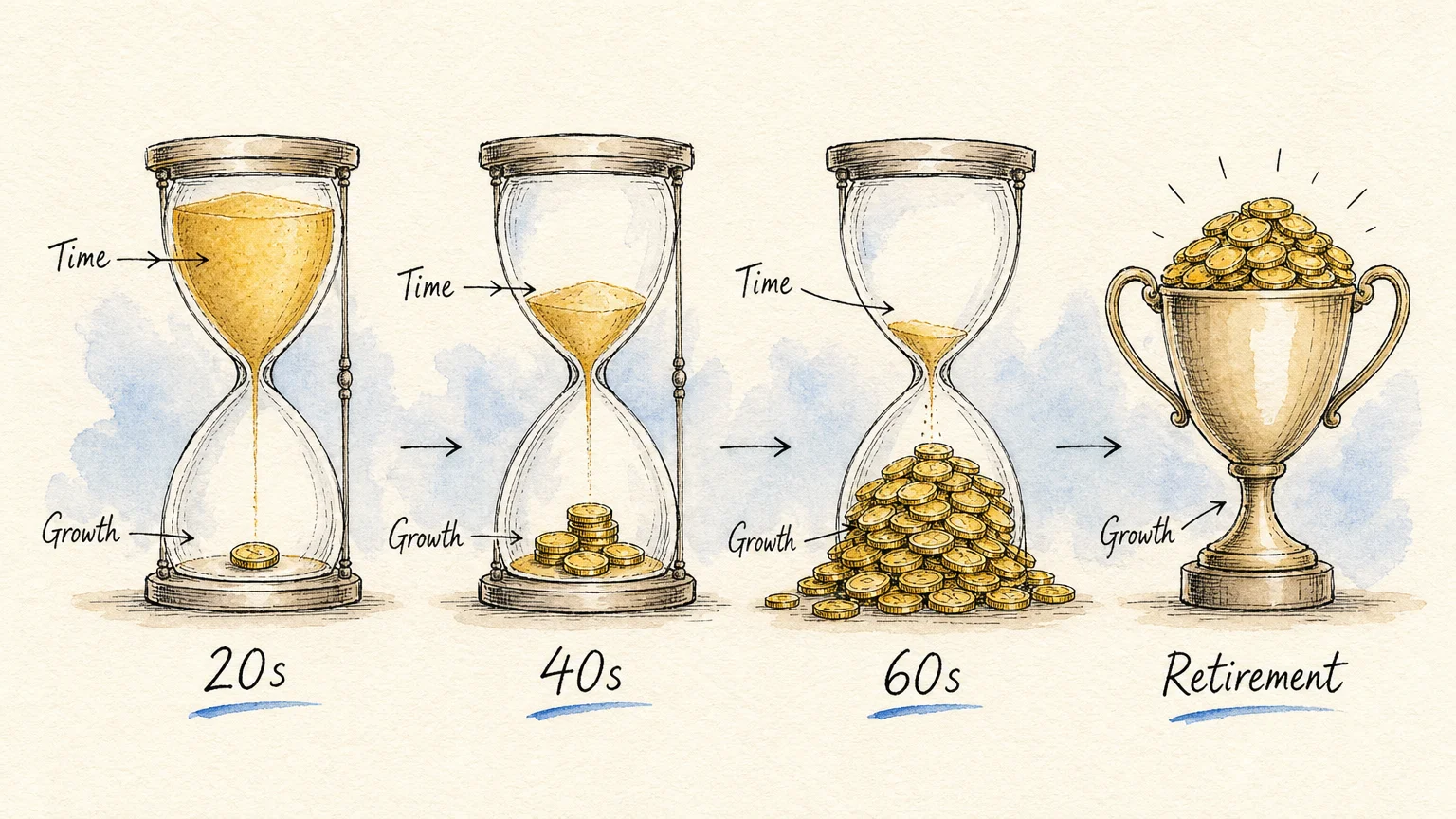

Your 20s: The Starting Line. You might look at a median balance of less than $2,000 and wonder why you should even bother participating. In your twenties, the actual dollar amount matters far less than the habit of saving and the length of your investing runway—time is your greatest asset. Every dollar invested in your early twenties has four decades to compound. Securing your employer match at this stage is the most critical move you can make.

Your 30s: The Balancing Act. Your thirties often bring significant life changes, including buying a home, getting married, or starting a family. These competing financial priorities can make retirement saving feel like an impossible stretch; however, the key during this decade is to prevent lifestyle creep from absorbing your raises. A median balance of around $16,000 indicates that many young professionals temporarily pause their contributions to fund immediate lifestyle goals—a costly mistake that sacrifices prime compounding years.

Your 40s: The Acceleration Phase. Entering your peak earning years, your forties represent a critical window for wealth accumulation. The median balance jumps to nearly $40,000, but many financial planners suggest you should aim much higher. This is the time to aggressively monitor your investment fees, ensure your portfolio is appropriately weighted toward growth assets, and systematically increase your contribution rate each time you receive a salary bump.

Your 50s: The Catch-Up Era. With the median balance approaching $68,000, workers in their fifties realize retirement is no longer a distant concept. The tax code provides a distinct advantage here: catch-up contributions. If you fell behind during your thirties and forties, your fifties offer a structured path to rapidly pad your nest egg. This is also the decade to begin visualizing exactly what your retirement lifestyle will cost.

Your 60s: The Transition Phase. As you approach traditional retirement age, your focus naturally shifts from pure growth to capital preservation and income planning. With a median balance hovering around $95,000, it becomes abundantly clear that for most Americans, a 401(k) is designed to supplement Social Security and other assets rather than fully replace a working income. Protecting your portfolio from severe market downturns becomes paramount.

Are You Actually on Track? The Salary Multiplier Benchmark

Comparing yourself to national averages can sometimes lead to a false sense of security. If you earn $150,000 a year, holding the median balance of $67,000 in your fifties is nowhere near enough to sustain your current standard of living. Instead of relying solely on peer comparisons, evaluate your savings against your own income.

Fidelity Investments established a widely respected benchmark based on pre-tax salary multipliers. To maintain your current lifestyle in retirement, they suggest aiming for the following targets:

- By age 30: Have 1x your annual salary saved.

- By age 40: Have 3x your annual salary saved.

- By age 50: Have 6x your annual salary saved.

- By age 60: Have 8x your annual salary saved.

- By age 67: Have 10x your annual salary saved.

If these targets seem intimidating, remember that they account for all your retirement accounts combined—not just your current 401(k). This multiplier includes old 401(k) accounts from previous employers, Traditional IRAs, Roth IRAs, and even spousal retirement accounts.

2026 IRS Contribution Limits to Boost Your Savings

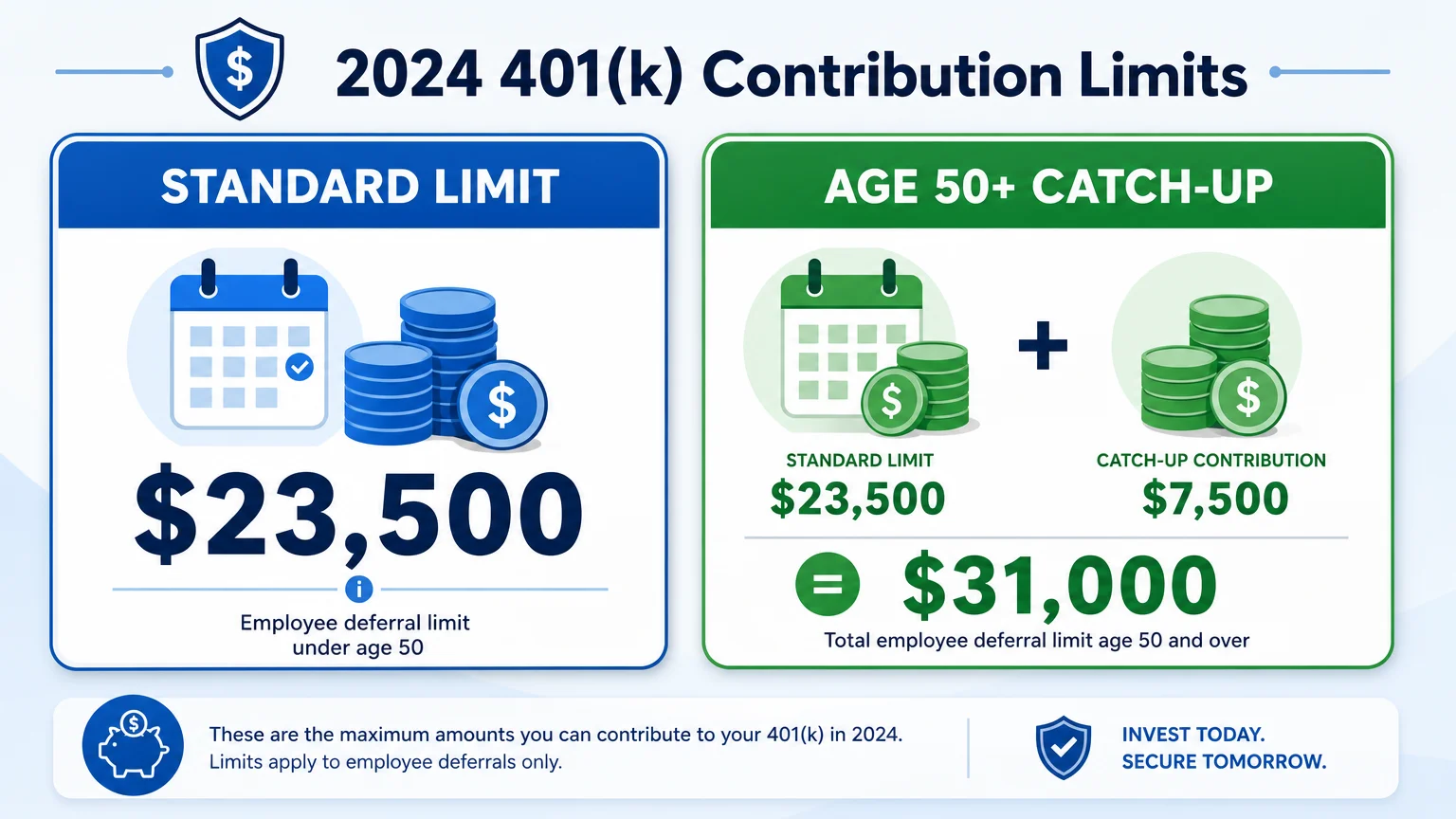

Understanding and utilizing the maximum contribution limits allows you to shelter more of your income from current taxes while accelerating your portfolio’s growth. In 2026, the standard employee deferral limit stands at $24,500. This is the maximum amount you can contribute from your paycheck, excluding any matching funds your employer provides.

If you are age 50 or older, you are eligible for a standard catch-up contribution of $8,000, bringing your total potential employee contribution to $32,500.

Crucially, recent legislative changes under the SECURE 2.0 Act created a special opportunity for workers nearing the finish line. If you are ages 60, 61, 62, or 63, you qualify for a “super catch-up” contribution. For 2026, this elevated limit sits at $11,250 on top of the standard deferral. High-earning participants should note that complex phase-out rules apply, often requiring these specific catch-up funds to be deposited as Roth (after-tax) contributions. Always verify your eligibility and current tax rules directly with the Internal Revenue Service (IRS) to avoid overcontribution penalties.

The Power of the Employer Match

A guaranteed return on investment is virtually impossible to find in the stock market, yet millions of workers pass it up every year by failing to secure their full employer match. If your company offers a 100 percent match on the first 5 percent of your salary you contribute, contributing only 3 percent is equivalent to refusing a portion of your compensation.

Always view the employer match as part of your total salary package. If you earn $80,000 and your company offers a 5 percent match, that is $4,000 of free money deposited into your account annually. Over twenty years, assuming an average market return, that “free” money alone could grow to hundreds of thousands of dollars. Structuring your budget to capture every matching dollar is the single most effective action you can take to grow your balance.

Pitfalls to Watch For

Even dedicated savers can derail their progress through common, avoidable mistakes. Protecting your wealth is just as important as accumulating it. Watch out for these major stumbling blocks.

Cashing Out Between Jobs: The modern worker changes employers frequently. When you leave a job, you often receive a notice regarding your 401(k) balance. Many people choose to cash out a small account to pay off a credit card or fund a vacation. Doing so triggers ordinary income taxes, plus a steep 10 percent early withdrawal penalty if you are under age 59½. More destructively, it resets your compounding timeline to zero. Always roll your old account into your new employer’s plan or a personal IRA.

Ignoring Investment Fees: While a 1 percent administrative fee sounds trivial, over thirty years, it consumes a massive portion of your total potential returns. High mutual fund expense ratios silently drag down your performance year after year. Review your plan’s fee disclosure document, and consider utilizing the free educational resources at Investor.gov to better understand how hidden fees erode long-term growth.

Misusing Target-Date Funds: Many 401(k) plans automatically default your contributions into a target-date fund based on your projected retirement year. These funds are designed to automatically shift from aggressive stocks to conservative bonds as you age. However, they rely on a generic glide path. If you plan to work until 70 but are enrolled in a 2030 fund, your portfolio may become too conservative too quickly, causing you to miss out on vital market gains during your final working years.

Taking Unnecessary 401(k) Loans: Borrowing against your retirement account might seem appealing because you pay the interest back to yourself. However, the money you borrow is removed from the market, meaning you lose out on compound growth during the repayment period. Furthermore, if you leave your job before the loan is repaid, the outstanding balance often becomes due immediately; if you cannot pay it, it is treated as a taxable distribution.

Strategies to Get Your 401(k) Back on Track

If you are currently falling short of your age-based benchmarks, panic will not help you—but a structured action plan will. Implementing a few mechanical changes to how you manage your account can drastically alter your trajectory.

“Do not save what is left after spending, but spend what is left after saving.” — Warren Buffett, Investor and Philanthropist

- Implement Auto-Escalation: Most modern 401(k) portals allow you to automatically increase your contribution rate by 1 or 2 percent each year. Time this automatic increase to coincide with your annual salary raise. You will never feel the pinch in your monthly paycheck, but your retirement account will experience exponential growth over time.

- Direct Windfalls Wisely: Whenever you receive a year-end bonus, a tax refund, or an inheritance, commit to depositing a substantial portion of it into your retirement accounts. Treating windfalls as wealth-building tools rather than spending money accelerates your progress without impacting your day-to-day budget.

- Audit Your Asset Allocation: The stock market rewards long-term patience. A portfolio overly concentrated in stable value funds or bonds during your thirties will almost certainly fail to outpace inflation. Log into your portal and ensure your investments match your actual time horizon.

- Consolidate Orphaned Accounts: Leaving money in a former employer’s plan often leads to neglected asset allocation and redundant administrative fees. Consolidating your accounts through a direct rollover gives you a clear, centralized view of your total wealth.

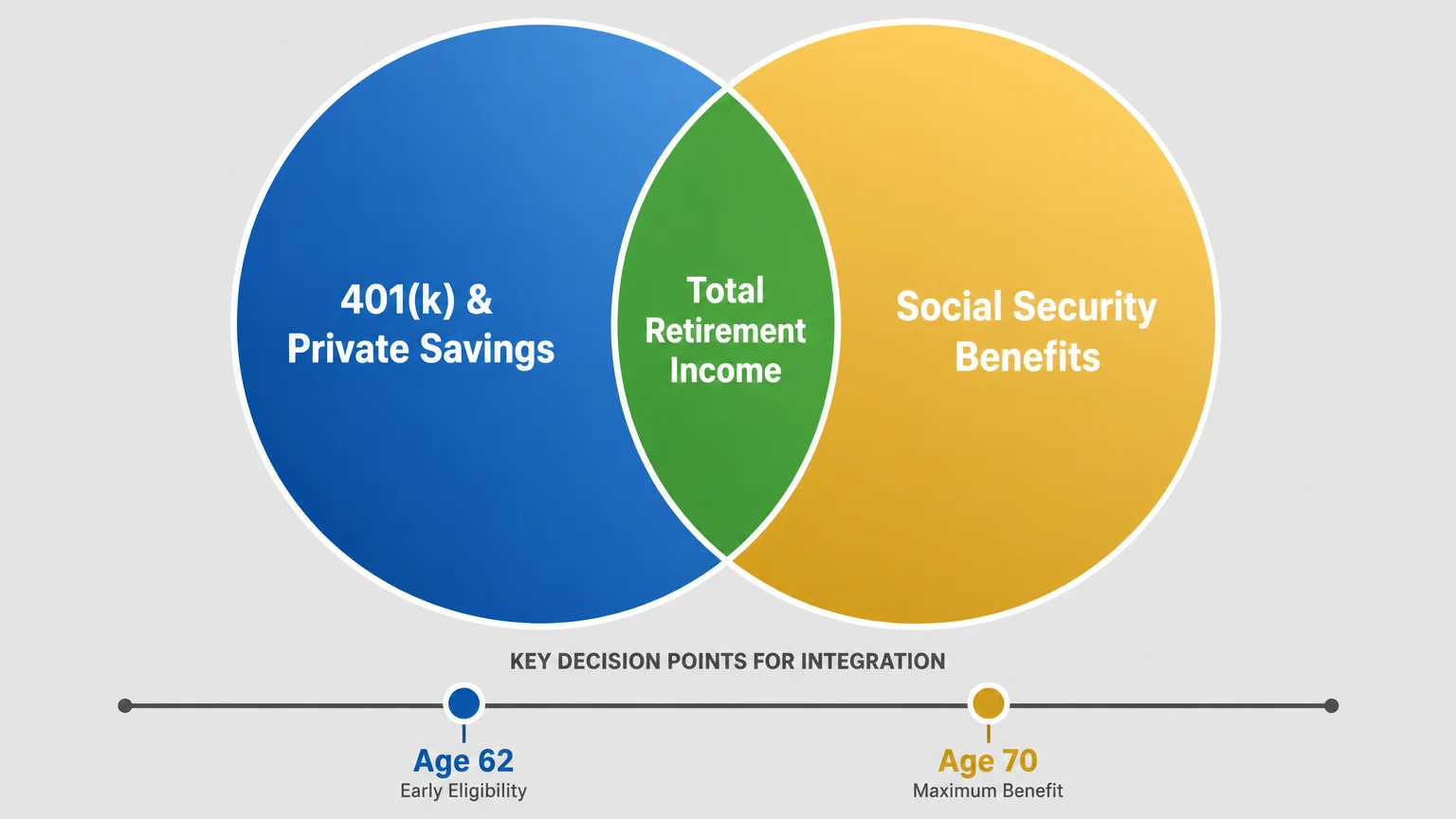

Integrating Your 401(k) With Social Security

Your 401(k) does not operate in a vacuum; it is part of a broader financial ecosystem that includes your expected government benefits. Understanding your estimated monthly benefit directly from the Social Security Administration (SSA) allows you to calculate the exact income gap your 401(k) needs to fill.

For example, if you determine you require $6,000 a month to live comfortably, and Social Security will provide $2,500, your 401(k) and other personal investments must reliably generate $3,500 a month. Knowing this specific target prevents you from saving blindly and helps you construct a withdrawal rate that will not deplete your principal too early in retirement.

Getting Expert Help

Navigating your 401(k) allocation is relatively straightforward in your twenties, but the complexity spikes dramatically as you approach your final working years. Transitioning from saving money to safely spending it requires precision.

“A big part of financial freedom is having your heart and mind free from worry about the what-ifs of life.” — Suze Orman, Financial Expert

Consider hiring a fiduciary financial planner if you fall into one of the following scenarios:

- You need a tax-efficient withdrawal strategy: Deciding which accounts to tap first—your Traditional 401(k), Roth IRA, or taxable brokerage—requires intricate tax planning. A professional helps you avoid bumping yourself into a higher tax bracket or triggering costly Medicare premium surcharges (IRMAA).

- You are navigating a major life transition: A divorce, the loss of a spouse, or an unexpected early retirement buyout offer can drastically alter your financial landscape. Expert guidance provides objective clarity during highly emotional periods.

- You want to maximize Roth conversions: If you hold a massive balance in a pre-tax 401(k), moving portions of it to a Roth account during low-income years can save you thousands in future taxes. An advisor can calculate the exact conversion amounts to execute without generating a massive tax bill today.

- You are concerned about fraud and high fees: As your balance grows, you become a larger target for predatory financial products. Verify the credentials of anyone advising you on rollovers, and consult the Consumer Financial Protection Bureau (CFPB) for guidelines on protecting your retirement assets from bad actors.

Frequently Asked Questions

What happens to my 401(k) if the stock market crashes right before I retire?

Market volatility is a normal, unavoidable part of investing. If a downturn occurs right before you retire, you do not actually lose your money unless you panic and sell your investments at a loss. A properly diversified portfolio is designed to have a portion of its assets sitting in bonds or cash equivalents. These stable assets cover your initial retirement living expenses, granting your stock investments the necessary time to recover and grow again.

Can I withdraw money from my 401(k) penalty-free before age 59½?

Generally, withdrawing funds before age 59½ triggers ordinary income taxes and a steep 10 percent early withdrawal penalty. However, the IRS “Rule of 55” provides a specific exception. If you leave your job—whether you quit, are fired, or are laid off—in or after the year you turn 55, you can take penalty-free distributions from that specific employer’s 401(k) plan. Note that this rule does not apply to IRAs or old 401(k)s from previous employers.

Should I choose a Traditional 401(k) or a Roth 401(k)?

The decision ultimately comes down to when you want to pay the IRS. A Traditional 401(k) offers an upfront tax deduction, meaning your contributions lower your taxable income today; however, your withdrawals in retirement are taxed as ordinary income. A Roth 401(k) requires you to pay taxes on your contributions immediately, but your money grows entirely tax-free, and qualified withdrawals in retirement are completely tax-free. Many financial experts recommend holding a mix of both to provide maximum tax flexibility during retirement.

How many 401(k) accounts does the average person have?

Because the modern worker changes jobs frequently, it is highly common to accumulate three or four different 401(k) accounts over a full career. While leaving money in a former employer’s plan is an available option, it often leads to neglected asset allocation, forgotten balances, and redundant administrative fees. Consolidating these accounts through a direct rollover into your current 401(k) or a personal IRA is usually the most efficient way to manage your retirement wealth.

Building a robust 401(k) balance is a marathon of consistency rather than a sprint of timing the market. Whether you find yourself far ahead of your age-group average or trailing behind the median, the most crucial step you can take today is to act. Small, calculated adjustments—increasing your contribution rate by a single percentage point, optimizing your asset allocation, or capturing your full employer match—compound over time to create massive shifts in your eventual financial freedom.

Focus strictly on the variables you control. You cannot dictate market returns, control inflation, or prevent legislative shifts, but you hold complete authority over your personal savings rate and your financial education. Treat your 401(k) not as a passive deduction from your paycheck, but as the foundational engine of your future independence.

Last updated: June 2026. This is educational content based on general retirement and financial principles. Individual results vary based on your situation. Always verify current benefit rules, tax laws, and eligibility requirements with official sources like SSA, Medicare.gov, or the IRS.

Leave a Reply