Leaving the workforce alters the daily mechanics of your marriage, stripping away the structured routines that previously defined your boundaries and individual space. When forty hours of the week suddenly open up, the transition often exposes hidden friction points regarding money, schedule management, and personal identity. Navigating this new phase requires renegotiating the silent contracts you built during your working years, shifting from weekend companions to full-time co-managers of your retirement life. Unpacking these emerging conflicts early prevents minor irritations from snowballing into deep-seated resentment. By understanding the specific triggers that frequently disrupt retirement relationships, you can proactively design a shared lifestyle that respects both individual autonomy and your collective vision for the future.

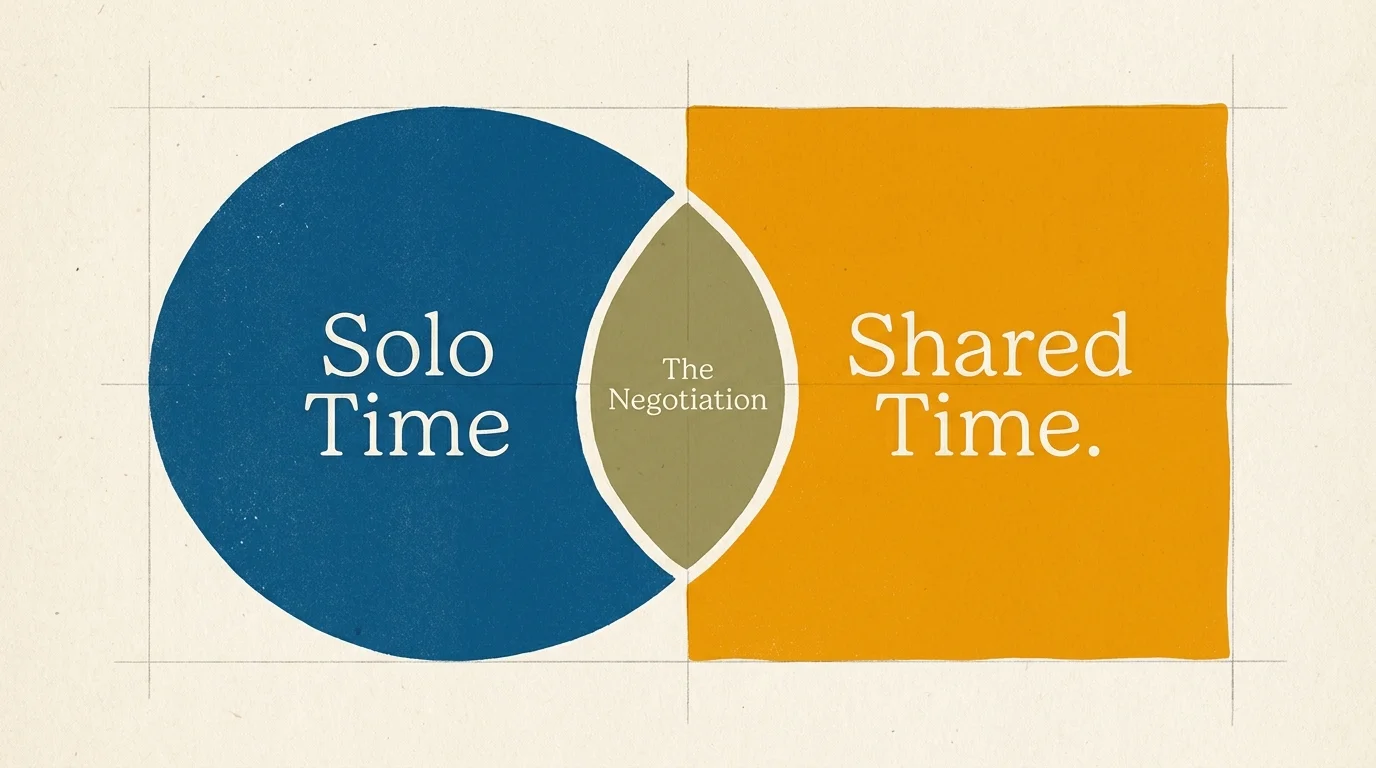

1. The Ratio of Shared Time to Solo Time

During your working years, your schedule dictated how much time you spent with your spouse. The office, commutes, and professional obligations naturally enforced physical distance, making your evenings and weekends feel valuable. When those external boundaries vanish, you face a sudden and overwhelming abundance of togetherness. Many retirement couples quickly discover the reality behind the old adage: “I married you for better or for worse, but not for lunch.”

Conflicts often arise when one partner views retirement as an opportunity to do everything together, while the other desperately craves alone time. The partner seeking independence might feel smothered, retreating to the garage, the garden, or another room just to find quiet. Meanwhile, the partner seeking companionship interprets this withdrawal as rejection.

To resolve this, you must explicitly negotiate your daily calendar. Treat solo time not as an escape from your marriage, but as a necessary ingredient for a healthy relationship. Establish routines where you pursue individual interests in the morning and reconvene for shared activities in the afternoon. Creating a structured yet flexible daily rhythm ensures both partners get their social and solitary needs met without harboring silent resentment.

2. Financial Boundaries and the Shift to Spending

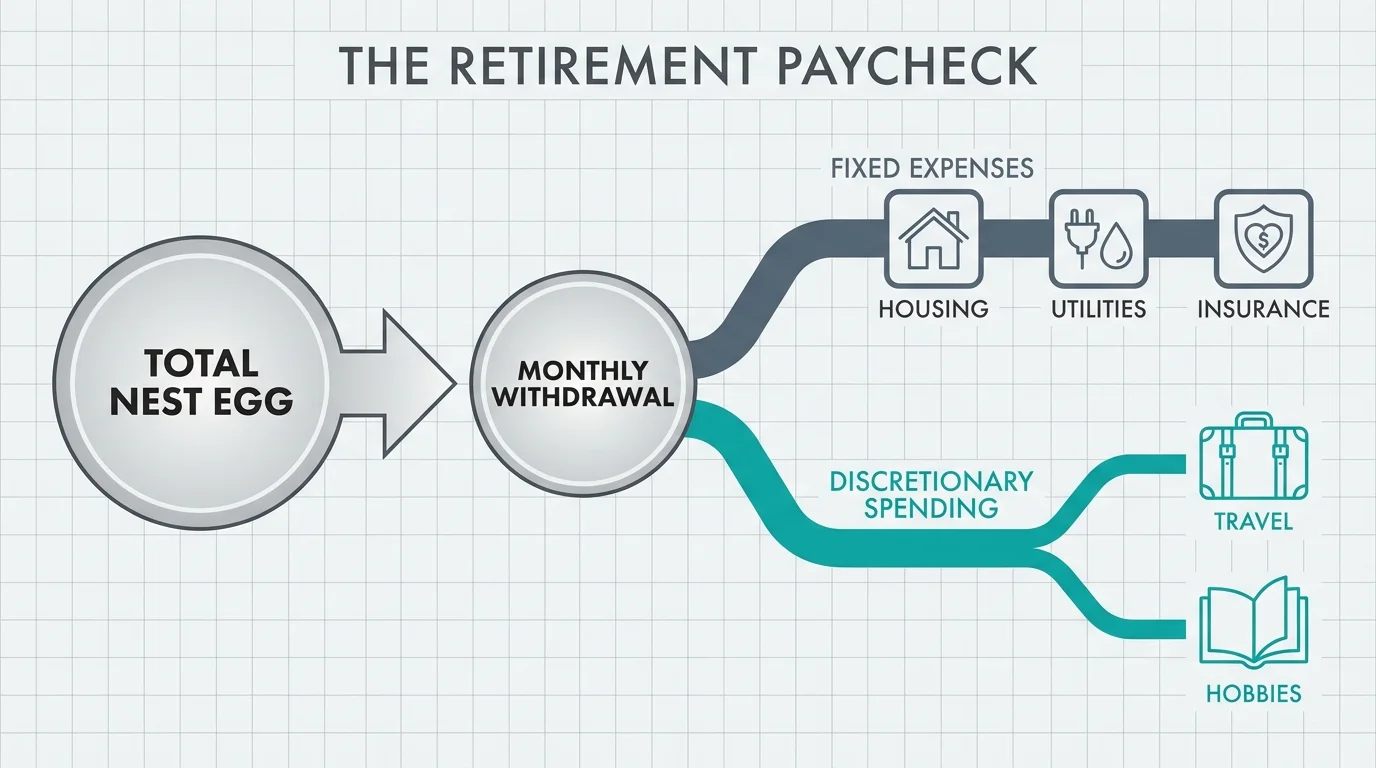

For decades, your primary financial goal was accumulation. You saved, invested, and watched your nest egg grow. Retiring forces an abrupt psychological shift from accumulating wealth to decumulating it—a transition that terrifies many seniors. This fundamental shift in financial mechanics frequently causes massive friction, especially if you and your spouse have different risk tolerances.

One partner might argue that it is finally time to enjoy the money they worked so hard to build, advocating for luxury travel, home upgrades, or expensive hobbies. The other partner, haunted by the fear of running out of money, might suddenly become hyper-frugal, questioning every grocery receipt and utility bill. This dynamic turns daily spending into a perpetual battleground.

You can neutralize this conflict by establishing a formal “retirement paycheck.” Work together to determine a safe, agreed-upon monthly withdrawal rate that covers fixed expenses and discretionary spending. If you need help structuring safe withdrawal strategies, resources from the Consumer Financial Protection Bureau (CFPB) offer excellent guidance on managing money in later life. Consider maintaining separate discretionary accounts with an agreed-upon monthly allowance for each spouse. This allows both of you to spend a portion of your wealth guilt-free, without triggering your partner’s financial anxieties.

3. The Reorganization of Household Duties

When one or both partners retire, the previous division of household labor immediately becomes obsolete. If one spouse managed the home while the other worked, the sudden presence of the newly retired spouse can feel like an invasion of territory. The home-manager might feel scrutinized or micromanaged, while the newly retired spouse might feel useless or restless, attempting to “fix” systems that were never broken.

Conversely, if both partners worked full-time and shared chores equally on weekends, the expectation of who does what on a random Tuesday can cause friction. One partner might assume that because they are retired, they are officially exempt from domestic duties, leaving the other to shoulder the entire burden.

A successful transition requires a complete reset of domestic expectations. Sit down and perform a post-retirement chore audit. List every household responsibility—from managing investments and paying bills to grocery shopping, cooking, and yard work. Divide these tasks based on your current energy levels, interests, and physical abilities rather than defaulting to your historical roles. Rebalancing these responsibilities turns you back into a team.

4. The Decision to Downsize or Age in Place

Housing decisions carry heavy emotional and financial weight, making them a prime catalyst for arguments. The family home often represents deep sentimental value, filled with decades of memories, neighborhood ties, and a sense of permanence. However, it also represents property taxes, continuous maintenance, and potential mobility challenges as you age.

Arguments typically erupt when one spouse desperately wants to sell the large home to eliminate yard work and unlock home equity, while the other absolutely refuses to leave the space where they raised their children. One envisions a maintenance-free condo near the beach; the other envisions hosting grandchildren in their familiar backyard.

To navigate this impasse, remove the immediate pressure of putting a “For Sale” sign in the yard. Instead, evaluate the objective realities of your current home against your future physical and financial needs. Discuss the following factors:

- Maintenance costs: Calculate the actual annual cost of upkeep, repairs, and property taxes.

- Physical accessibility: Assess the home for long-term safety, including stairs, bathroom setups, and doorway widths.

- Proximity to services: Evaluate how close you are to preferred healthcare providers, grocery stores, and social hubs.

- Social isolation: Consider whether your current neighborhood still provides the social interaction you need as neighbors move away.

If you decide to stay, commit to modifying the home for aging in place. If you decide to move, rent an Airbnb in your desired destination for a month to test the reality of the new lifestyle before committing permanently.

5. Setting Boundaries with Adult Children

Your relationships with your adult children and grandchildren can unexpectedly strain your marriage during retirement. Without the built-in excuse of work, adult children might begin viewing you as a permanent, free resource for childcare, home repairs, or financial bailouts.

Conflict strikes when you and your spouse disagree on where to draw the line. One partner might revel in the role of full-time babysitter, happy to provide daily care for grandchildren. The other partner might feel that their long-awaited retirement freedom has been hijacked by a new, unpaid job. Financial support creates even deeper rifts; one spouse may want to dip into retirement savings to help a child buy a house or pay off debt, while the other fiercely protects their nest egg.

You must present a united front. Before agreeing to ongoing childcare, discuss how many days per week you are truly willing to commit, ensuring you protect time for your own travel and hobbies. Regarding financial assistance, establish a firm rule that neither of you will offer loans or gifts to adult children without consulting the other first. Your financial security must remain the priority, as becoming a financial burden to your children later in life is a much worse outcome than saying “no” to them today.

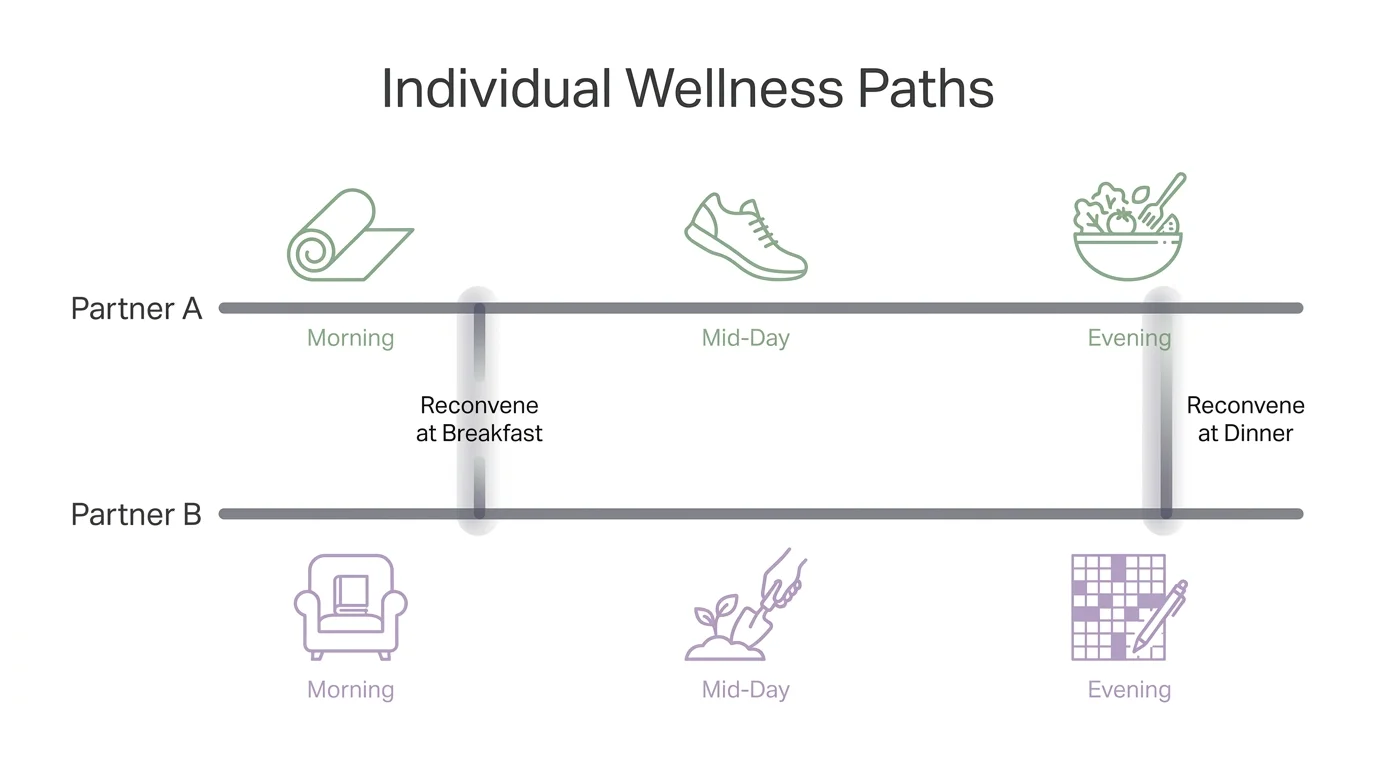

6. Diverging Health and Wellness Habits

Health becomes the central pillar of retirement life. How you maintain it—or neglect it—directly impacts your shared future. Arguments frequently stem from mismatched commitments to diet, exercise, and preventative care.

If one partner embraces an active lifestyle—joining walking groups, eating cleanly, and prioritizing longevity—while the other partner embraces a sedentary lifestyle of television and junk food, resentment builds rapidly. The active partner fears they will become an early caregiver or lose out on travel opportunities because their spouse cannot keep up. The sedentary partner feels nagged, judged, and controlled.

You cannot force your spouse to change their habits, but you can communicate the real-world consequences of their choices on your shared plans. Frame the conversation around shared goals rather than criticism. Instead of attacking their diet, express your desire to hike together in a national park next year and discuss what physical steps you both need to take to make that happen. For authoritative guidance on maintaining mobility and vitality, the National Institute on Aging (NIA) provides excellent, evidence-based exercise and nutrition frameworks designed specifically for older adults.

7. The Pursuit of Individual Purpose

Losing your professional identity creates a profound psychological void. For decades, your job provided structure, social interaction, and a sense of achievement. When that disappears, finding a new purpose becomes essential for your mental health.

When only one spouse successfully finds a new passion, the marriage suffers. The partner who discovers a fulfilling second act—perhaps through volunteering, starting a small business, or mastering a complex hobby—thrives. The partner who struggles to find meaning often falls into mild depression, listlessness, or excessive dependency on their spouse for entertainment.

“Retirement isn’t a finish line—it’s a transition into a new way of living where couples must actively redesign their purpose together.” — Mitch Anthony, Retirement Expert

Support your spouse in their search for meaning without taking responsibility for their happiness. Encourage them to explore local community college classes, join civic organizations, or mentor young professionals. A thriving marriage consists of two individuals who bring their own unique energy, stories, and experiences back to the dinner table. If both partners sit at home waiting for the other to generate excitement, the relationship stagnates.

8. Conflicting Travel and Leisure Dreams

Travel routinely dominates retirement bucket lists, but the definition of an ideal vacation varies wildly between individuals. You might have assumed you were on the same page for forty years, only to discover completely divergent travel styles once you actually have the time to go.

One spouse might envision selling the house and touring the country in a Class-A motorhome, embracing a nomadic lifestyle. The other might strongly prefer luxury river cruises in Europe or simply taking short weekend road trips while sleeping in comfortable hotels. Budgetary disagreements further complicate travel plans; one partner wants to fly first-class and stay in resorts, while the other wants to stretch the travel budget by flying economy and staying in modest rentals.

Compromise requires creativity. You do not have to adopt a single travel style. Implement a “take turns” approach to vacation planning, where one spouse plans the spring trip according to their preferences, and the other plans the fall trip. Alternatively, find middle ground: take the river cruise, but book the standard cabin instead of the luxury suite. Acknowledge that you do not have to take every trip together. If one partner desperately wants to take a rugged fishing trip and the other wants a museum tour in Paris, pursuing separate trips occasionally can be incredibly healthy for your marriage.

Common Relationship Mistakes to Avoid in Retirement

Awareness of behavioral traps can save you from months of unnecessary arguing. Pay attention to these frequent missteps as you settle into your new lifestyle:

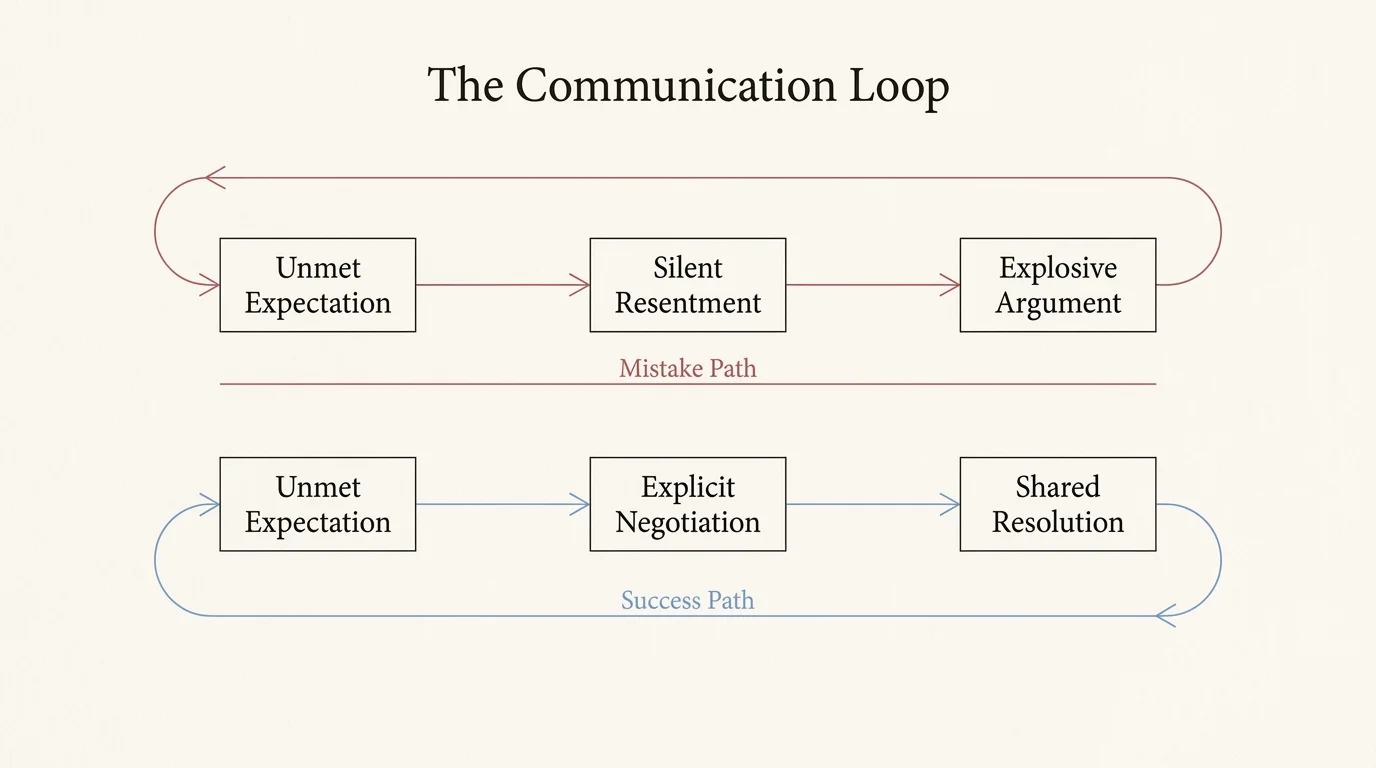

Expecting your spouse to read your mind. Do not assume your partner knows how you want to spend your days. State your preferences clearly. If you want Saturday mornings to remain quiet reading time, communicate that directly.

Failing to update your budget dynamically. Retirement spending is rarely a flat line. The first few years (the “go-go” years) often feature high travel and entertainment costs, while later years skew toward healthcare. Revisit your financial boundaries annually to ensure neither partner harbors hidden financial anxiety.

Keeping score. With more free time, it becomes dangerously easy to track who loaded the dishwasher last or who initiated the last social outing. Drop the ledger. Focus on contributing to the household rather than auditing your partner’s contributions.

Shifting Dynamics: Working Years vs. Retirement

Understanding how your relationship mechanics change can help you identify why you might be arguing more. The shift is systemic, affecting nearly every aspect of daily life.

| Relationship Dynamic | During Working Years | During Retirement Life | Adjustment Strategy |

|---|---|---|---|

| Time Management | External schedules dictated your routine; weekends were premium shared time. | 168 hours of completely unstructured time per week. | Block out specific hours for solo hobbies; actively schedule dates. |

| Financial Focus | Earning, saving, and investing for the distant future. | Managing withdrawals, spending down assets, managing tax brackets. | Create a rigid monthly “paycheck” system to allow guilt-free spending. |

| Identity & Status | Tied heavily to career titles, professional achievements, and parenting. | Defined by personal interests, community involvement, and legacy. | Give each other grace while navigating the loss of professional identity. |

| Conflict Resolution | Often deferred due to exhaustion or lack of time during the workweek. | Conflicts surface immediately and demand real-time attention. | Address irritations promptly before they compound into major arguments. |

Frequently Asked Questions About Retirement Relationships

How do we compromise on retirement spending without constantly fighting?

The most effective strategy is separating your mandatory expenses from your discretionary funds. Once you agree on the budget for housing, healthcare, and groceries, allocate a specific monthly allowance to each partner for their personal use. This prevents the frugal partner from scrutinizing the spending partner’s hobby purchases.

Is it normal to feel smothered by my spouse after they retire?

Yes, this is an incredibly common phenomenon. It is completely normal to feel overwhelmed when your personal space is suddenly occupied 24/7. Communicate your need for alone time gently but firmly, framing it as a tool to recharge rather than a desire to avoid them.

Should we combine our retirement accounts or keep them separate?

While the accounts themselves (like IRAs or 401ks) are legally held in individual names, the planning should be entirely combined. You must view your distinct accounts as one unified household portfolio to optimize tax strategies and withdrawal sequences. Transparency is mandatory, even if the accounts remain separate.

How can we find shared hobbies if we have vastly different interests?

Stop trying to force your spouse into your existing hobbies. Instead, look for a “neutral ground” activity that is entirely new to both of you. If you take a cooking class, learn a new language, or start volunteering for a local charity together, you start on equal footing without one partner acting as the impatient instructor.

A thriving marriage in your later years requires intentional design. The habits and routines that carried you through your working years will not automatically sustain you when your professional lives end. By addressing these eight common friction points head-on—setting clear boundaries around time, money, and personal space—you clear the path for a truly rewarding shared future. Communicate openly, give each other room to grow, and embrace the opportunity to reinvent your partnership.

This is educational content based on general retirement and financial principles. Individual results vary based on your situation. Always verify current benefit rules, tax laws, and eligibility requirements with official sources like SSA, Medicare.gov, or the IRS.

Last updated: May 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply