Shifting your mindset from accumulating wealth to managing a fixed income requires a sharp eye for hidden costs. Trimming recurring expenses and eliminating unnecessary fees is the most reliable way to stretch your savings without sacrificing the retirement lifestyle you worked decades to build. Many retirees unintentionally drain their portfolios by leaving expensive habits on autopilot, missing new benefit tiers, or paying for financial products they have simply outgrown. Auditing your spending habits helps protect your financial independence. Review these common areas where you might be quietly overpaying so you can redirect those funds toward experiences that actually enhance your daily life.

Healthcare and Insurance Expenses

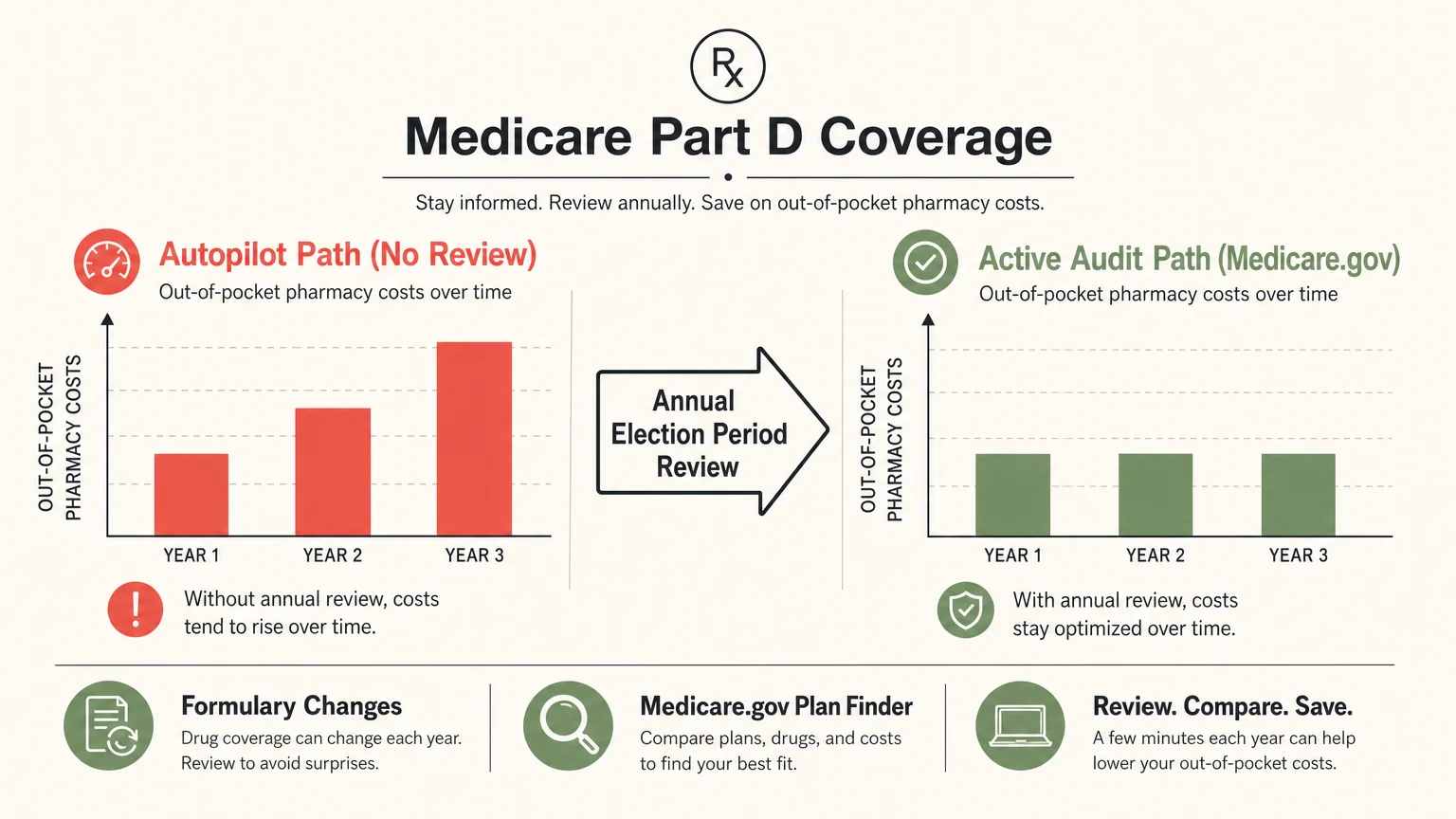

1. Medicare Prescription Drug Coverage (Part D)

Setting your Medicare Part D plan on autopilot is one of the costliest oversights in retirement. Insurance providers frequently change their formularies, meaning a medication covered fully this year might move to a more expensive pricing tier next year. Even if your premium stays the same, your out-of-pocket costs at the pharmacy counter can skyrocket. Use the official plan finder tool on Medicare.gov during the Annual Election Period to compare your exact medications against available plans. Changing providers takes only a few minutes and regularly saves retirees hundreds of dollars annually.

2. Irrelevant Life Insurance Premiums

Life insurance serves a specific purpose: replacing lost income to protect dependents if you pass away unexpectedly. Once you retire, pay off your mortgage, and watch your children become financially independent, that original need disappears. Continuing to pay premiums on a term life insurance policy drains cash that you could use for daily living expenses or healthcare. While some permanent or whole life policies hold cash value that requires a strategic approach, pure term policies can usually be dropped once your primary financial obligations are cleared.

3. Name-Brand Prescription Medications

Direct-to-consumer pharmaceutical advertising convinces many patients that name-brand drugs work better than their generic equivalents. The U.S. Food and Drug Administration requires generic medications to have the identical active ingredients, strength, and performance characteristics as brand-name drugs. Paying a premium for a recognizable label drains your healthcare budget unnecessarily. Always ask your physician or pharmacist if a generic alternative exists for your prescriptions. Furthermore, consult your doctor about “therapeutic alternatives”—different medications in the same class that treat the same condition but cost a fraction of the price under your specific insurance plan.

4. Dental and Vision Insurance Plans

Standalone dental and vision insurance policies often cost more in annual premiums than they pay out in benefits. These policies typically come with strict waiting periods, low annual maximum payouts, and high deductibles for major procedures. Run the numbers on your policy. If you pay $600 a year in premiums but only receive two routine cleanings that would cost $250 out of pocket, you are losing money. Many retirees find better value by dropping the insurance, negotiating cash-pay discounts directly with their dentist, or using a low-cost discount dental savings plan.

Investment and Financial Fees

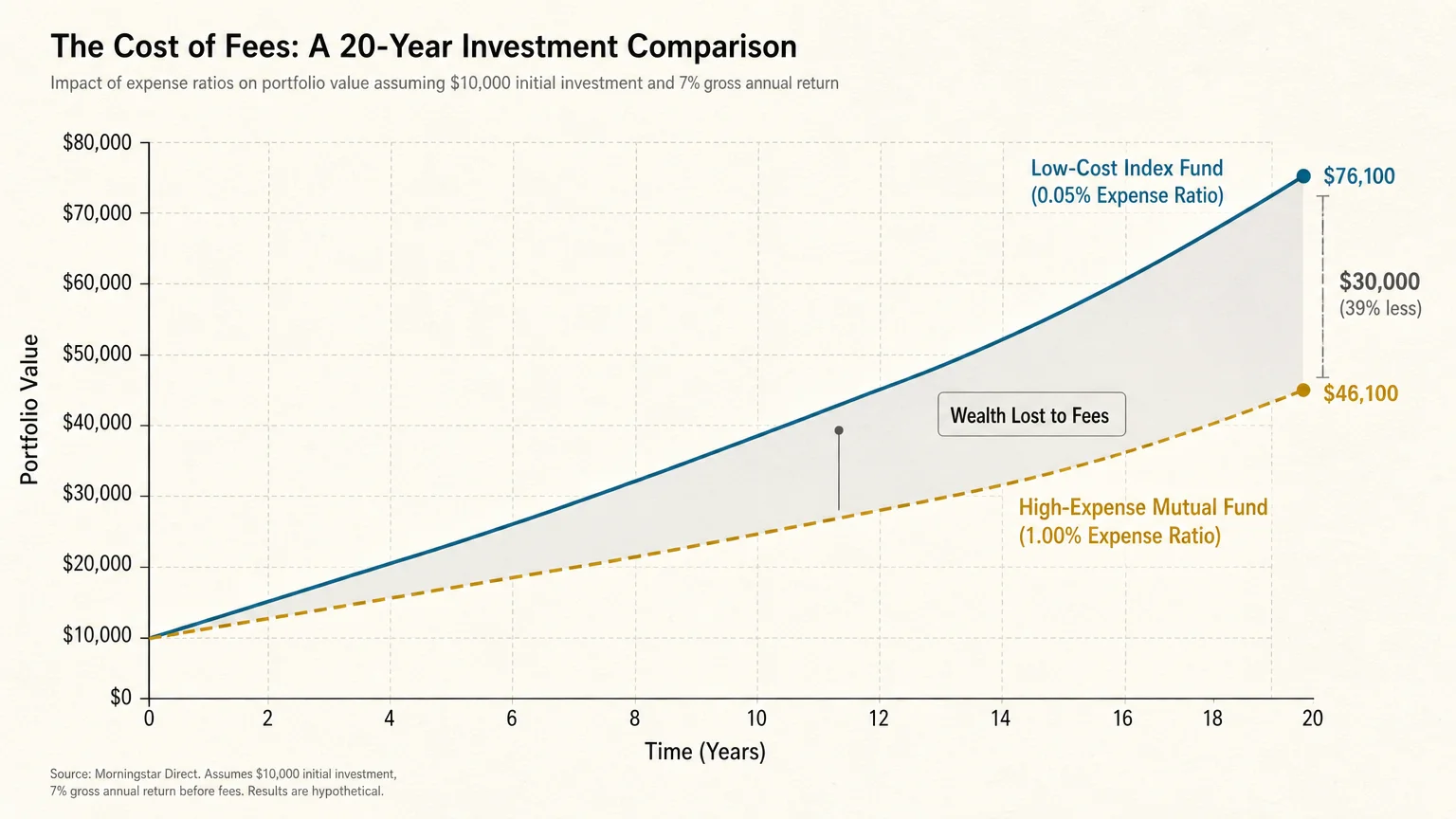

5. High-Expense Mutual Funds

Hidden investment fees destroy wealth quietly. Many retirees hold legacy mutual funds with expense ratios exceeding 1.00% without realizing the long-term damage to their portfolios. Active fund managers charge these high fees to try and beat the market, but data consistently shows that low-cost index funds tracking major benchmarks perform better over time. Swapping an actively managed fund for a broad-market index fund with an expense ratio of 0.05% leaves significantly more money compounding in your account.

“Performance comes, performance goes. Fees never falter.” — Warren Buffett, Chairman and CEO of Berkshire Hathaway

| Investment Strategy | Annual Expense Ratio | Estimated Fees Paid Over 10 Years ($100,000 Balance, 6% Return) |

|---|---|---|

| Actively Managed Fund | 1.00% | $14,500+ |

| Low-Cost Index Fund | 0.05% | $750+ |

6. Asset Under Management (AUM) Fees

Paying a financial advisor a standard 1% to 1.5% AUM fee makes sense when you are actively building wealth and require complex tax strategies, stock options management, or business succession planning. However, once you transition into a predictable distribution phase with a simplified portfolio, that ongoing percentage fee becomes exorbitant. On a $750,000 portfolio, a 1% fee costs $7,500 every single year. Consider shifting to a fee-only fiduciary who charges an hourly rate or a flat retainer. FINRA Investor Education provides excellent resources for understanding exactly how financial professionals charge for their services.

7. Unnecessary Tax Preparation Costs

If your retirement income consists primarily of Social Security benefits, pension payouts, and standard IRA distributions, your tax situation is likely quite simple. Yet, many retirees continue paying CPAs hundreds of dollars out of habit. The Internal Revenue Service (IRS) offers the Free File program for individuals below a certain income threshold. Additionally, the AARP Foundation Tax-Aide program provides free, in-person, and virtual tax preparation services explicitly designed for taxpayers aged 50 and older. Leveraging these free services keeps more of your money in your pocket.

8. Bank Account Maintenance and Paper Statement Fees

Traditional brick-and-mortar banks frequently charge monthly maintenance fees if your balance dips below a certain threshold. They also nickel-and-dime account holders with fees for printing and mailing paper statements. Over a year, these minor charges add up to a substantial sum. Move your primary checking and savings accounts to an online bank, local credit union, or a major institution that explicitly waives fees for seniors or direct-deposit customers. Opting into electronic statements eliminates mailing surcharges instantly.

Household and Property Costs

9. Property Tax Overpayments

Property taxes represent a massive, ongoing expense for retirees who own their homes. Unfortunately, local tax assessors frequently overvalue properties, and few homeowners bother to challenge the assessment. Beyond appealing your assessment, you might be missing out on valuable municipal exemptions. Most states offer senior citizen property tax exemptions, homestead exemptions, or property tax freezes for residents over age 65 who meet specific income guidelines. Visit your county tax assessor’s office to ensure you receive every exemption you are legally entitled to claim.

10. Empty Bedrooms and Excess Square Footage

Staying in a large family home long after the children move out drains your retirement finances from multiple angles. You pay higher property taxes, larger homeowner’s insurance premiums, and heavier utility bills to heat and cool empty rooms. Maintenance costs also scale with the size of the house. Downsizing to a smaller home, condo, or townhouse reduces these recurring costs drastically. The equity freed up from a home sale can then be reinvested to generate additional monthly income.

11. Outdated Cable and Telecom Packages

Telecom providers thrive on subscriber inertia. If you have had the same premium cable and landline bundle for the last decade, you are almost certainly paying too much. The landscape of home entertainment and communication has changed, offering cheaper, more flexible alternatives.

- Call your provider’s retention department annually to negotiate promotional rates.

- Cut the cord entirely and subscribe only to two or three streaming services you actually watch.

- Replace expensive landlines with Voice over Internet Protocol (VoIP) services or rely strictly on your cell phone.

- Audit your subscriptions every six months and aggressively cancel services you no longer use.

12. Overpriced Cell Phone Data Plans

Major cellular carriers routinely push unlimited data plans that cost $80 to $100 per month for a single line. If you spend most of your time at home or in locations with free Wi-Fi, you use very little cellular data. Switch to a Mobile Virtual Network Operator (MVNO). These companies rent space on the major cellular towers and offer identical coverage for $15 to $30 a month. You retain your current phone number and your exact smartphone, but your monthly bill drops significantly.

Everyday Lifestyle and Consumer Choices

13. Extended Warranties on Appliances and Electronics

Retailers push extended warranties relentlessly because they represent pure profit. Statistically, modern appliances and electronics rarely break during the extended warranty window, and when they do, the repair costs are often lower than the price of the warranty itself. Furthermore, the credit card you use to purchase the item likely provides a complimentary warranty extension as a cardholder benefit. Save the money you would spend on extended warranties in a dedicated emergency fund and self-insure against broken appliances.

14. Missed Senior Discounts

Pride often prevents retirees from asking for age-based discounts, leaving free money on the table at grocery stores, restaurants, hotels, and entertainment venues. You do not always need an AARP membership to secure these lower rates. Many businesses lower their prices for customers starting at age 55, but they require you to ask for the discount at the register. Make it a habit to politely inquire about senior pricing before completing any transaction.

15. New Car Depreciation

Buying a brand-new vehicle is one of the fastest ways to destroy wealth. A new car loses roughly 20% of its value the moment you drive it off the lot, and depreciation continues aggressively for the first three years. In retirement, you no longer face a daily work commute, meaning your annual mileage drops significantly. Purchasing a reliable, three-year-old used vehicle allows you to bypass the steepest depreciation curve while still enjoying modern safety features and a long mechanical lifespan.

16. Travel Bookings During Peak Seasons

Working professionals must plan vacations around school calendars and strict corporate holiday schedules, forcing them to pay premium rates during peak travel seasons. Retirees possess the ultimate luxury: schedule flexibility. Traveling during “shoulder seasons”—the periods right before or after peak season—yields massive savings on airfare, lodging, and excursions. Booking Tuesday flights, staying at resorts during mid-week slumps, and utilizing flexible-date search engines will drastically reduce your travel budget while providing a less crowded, more enjoyable experience.

Pitfalls to Watch For

When executing a plan to reduce your retirement expenses, avoid cutting costs so aggressively that you expose yourself to unnecessary risk. The most common trap involves dropping crucial insurance coverage, such as a personal umbrella policy or adequate homeowners insurance, just to save a few dollars a month. One major liability claim or natural disaster can wipe out a carefully protected portfolio.

Another prevalent pitfall is chasing yield or “free” financial services. Scammers frequently target retirees with promises of zero-fee investments that guarantee high returns. If a financial product sounds entirely too good to be true, it is likely masking hidden surrender charges, illiquid structures, or outright fraud. Always verify the credentials of any financial professional through official regulatory databases before moving your money.

Getting Expert Help

While you can handle most expense audits on your own, certain situations justify bringing in a professional. Knowing when to pay for good advice is just as important as knowing when to cut unnecessary fees.

Hire a Fee-Only Fiduciary when: You need a comprehensive withdrawal strategy, you are deciding when to claim Social Security for maximum benefit, or you need to rebalance a complex portfolio without triggering massive capital gains taxes.

Consult a Medicare Broker when: You are turning 65 and facing your initial enrollment period, or you have developed a complex medical condition that requires highly specific specialist networks and expensive prescription coverage.

Engage a Tax Professional when: You are selling real estate, exercising stock options, navigating inheritance issues, or executing a Roth IRA conversion strategy. Complex tax moves require precision to avoid severe penalties.

Frequently Asked Questions

How often should I review my retirement budget?

Conduct a deep audit of your recurring expenses at least once a year. The weeks leading up to Medicare Open Enrollment (October 15 to December 7) provide a natural reminder to review your healthcare choices, subscriptions, insurance premiums, and investment fees all at once.

Is it ever smart to keep term life insurance in retirement?

Yes, but only in specific scenarios. If you carry a massive mortgage that your spouse could not afford on a single income, or if you selected a pension payout option that ends upon your death, maintaining a term policy protects your surviving spouse from immediate financial hardship.

What is the quickest way to reduce my monthly retirement expenses?

Start with your telecom and subscription services. Canceling unused streaming platforms, dropping premium cable, and switching to an MVNO cell phone provider can put $100 to $200 back into your checking account every month with less than an hour of effort.

Mastering retiree budgeting is not about restricting your lifestyle; it is about eliminating waste so your money serves your actual priorities. By auditing these 16 common financial leaks, you take active control of your cash flow. Redirect those recovered funds into your travel budget, hobbies, or legacy goals to ensure your savings provide the maximum possible joy.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, health needs, tax situation, and goals—may require different approaches. When in doubt, consult a licensed professional.

Last updated: March 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply