Rumors of a proposed $2,000 payment have been making headlines, leaving retirees wondering if this sudden windfall might disrupt their carefully planned finances. When lawmakers debate issuing direct checks, the immediate question is how it impacts your bottom line. The good news is that a one-time stimulus payment does not directly reduce your core Social Security benefits. However, a sudden cash bump to your household adjusted gross income could easily trigger unexpected tax liabilities, push you into a higher Medicare premium bracket, or complicate strict asset limits for supplemental benefit programs. Understanding exactly how this proposed cash infusion interacts with your retirement income is essential for protecting your financial stability.

What the Latest Direct Payment Proposals Actually Mean

Federal lawmakers frequently float ideas for direct economic relief; these discussions often surface during periods of high inflation, shifting tariff policies, or major economic transitions. When you hear about a proposed $2,000 payment, it generally refers to a one-time cash disbursement authorized by Congress and distributed by the United States Treasury. Unlike ongoing pension payouts or standard monthly income, these checks are typically structured as advance refundable tax credits. This legal classification determines exactly how the money interacts with the rest of your financial life.

For retirees, navigating a new influx of cash requires distinguishing between earned income, unearned income, and tax-exempt relief. If Congress structures the legislation similarly to the stimulus checks issued during the early 2020s, the payment acts as a nontaxable credit. However, if the legislation ties the payment to specific tax revenues or dividend programs, the Internal Revenue Service might classify it as taxable income. This distinction acts as the primary domino that dictates whether your regular Social Security update will carry negative tax consequences later in the year.

You rely on a predictable budget. Introducing a sudden variable—even a highly positive one like a $2,000 check—forces you to recalibrate your tax strategies, Medicare planning, and daily withdrawal rates. Knowledge acts as your best defense against unexpected financial penalties.

“An investment in knowledge pays the best interest.” — Benjamin Franklin, Statesman and Inventor

Will a Direct Payment Decrease Your Monthly Social Security Checks?

The most immediate fear among retirees is that accepting a direct government payment will trigger a corresponding reduction in their monthly retirement checks. You can set this fear aside. Traditional Social Security benefits—formally known as Old-Age, Survivors, and Disability Insurance (OASDI)—are earned entitlements. You paid into this system through payroll taxes during your working years. The Social Security Administration calculates your primary insurance amount based on your thirty-five highest-earning years and the exact age you chose to claim your benefits.

Because OASDI is not a means-tested welfare program, your accumulated wealth, your current unearned income, and any sudden government stimulus checks have absolutely zero impact on the gross amount the government sends you each month. A proposed $2,000 payment will not cause the Social Security Administration to dock your pay. Your ongoing Social Security benefits remain secure and legally protected from offsets related to general economic stimulus measures.

Furthermore, receiving a direct payment does not interfere with your annual Cost-of-Living Adjustment (COLA). The federal government calculates the COLA using the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). A one-time payment issued to the public does not alter the inflation metrics used to calculate your permanent, long-term benefit increases. Your baseline retirement income remains insulated from these one-off legislative actions.

Clarifying the Earnings Test Confusion

If you claimed your retirement benefits before reaching your full retirement age and you continue to work, you are likely highly aware of the Retirement Earnings Test. The government limits how much you can earn from an employer or self-employment before they begin temporarily withholding a portion of your Social Security payments. Understandably, working retirees often panic at the thought of a $2,000 payment pushing them over that strict annual limit.

You can breathe easy on this front. The Social Security Administration strictly defines what counts toward the earnings limit: W-2 wages and net earnings from self-employment. The earnings test explicitly excludes investment dividends, pension payouts, IRA withdrawals, capital gains, and government stimulus payments. A direct check from the Treasury is unearned income. It will not trigger the earnings test, and it will not cause the government to withhold a single dime of your monthly checks, regardless of your age.

The Tax Torpedo: When Extra Income Makes Benefits Taxable

While your gross monthly benefit remains safe, the net amount you keep after taxes is highly vulnerable. This is where the concept of the “tax torpedo” comes into play. The federal government taxes Social Security benefits based on a specific formula known as “combined income.” To find your combined income, you add your adjusted gross income (AGI), any nontaxable interest you earned, and exactly 50 percent of your annual Social Security benefits.

The Internal Revenue Service uses strict, unadjusted thresholds to determine taxation:

- Individual Filers: If your combined income falls between $25,000 and $34,000, you may have to pay income tax on up to 50 percent of your benefits. If your combined income exceeds $34,000, up to 85 percent of your benefits become taxable.

- Joint Filers: If you and your spouse have a combined income between $32,000 and $44,000, up to 50 percent of your benefits are taxable. If your combined income crosses the $44,000 line, up to 85 percent of your benefits are subject to federal income tax.

If Congress decides to classify a new proposed $2,000 payment as taxable income, it will immediately increase your adjusted gross income. For retirees hovering right on the edge of these taxation cliffs, that extra $2,000 can push a significant portion of their previously untaxed Social Security benefits into the taxable category. This creates a compounding effect; the extra income not only brings its own tax burden but also drags your core benefits into the IRS’s reach. Careful monitoring of your total household income ensures you can adjust your IRA withdrawals or charitable giving to offset this potential tax trap.

How One-Time Windfalls Affect Medicare Part B and D Premiums

Your tax return dictates more than just your obligation to the IRS; it also controls your healthcare costs. Medicare evaluates your modified adjusted gross income (MAGI) to determine if you must pay an Income-Related Monthly Adjustment Amount (IRMAA). This surcharge applies to both Medicare Part B (medical insurance) and Part D (prescription drug coverage) for retirees with higher incomes.

Medicare employs a two-year lookback period. The income you report on your tax return in 2026 will dictate the Medicare premiums you pay in 2028. IRMAA thresholds operate as sheer cliffs rather than gradual slopes. Earning just one dollar over a threshold pushes you into the next premium bracket, which can cost you hundreds of dollars in additional healthcare fees over the course of a year.

If the proposed $2,000 payment is deemed taxable, it increases your MAGI. If that increase pushes you over an IRMAA cliff, the resulting Medicare surcharges could easily wipe out the value of the original payment. Should you find yourself facing an IRMAA surcharge due to a one-time payment, the Medicare.gov official guidelines outline a specific appeals process. You can file Form SSA-44 to request a premium reduction if you experience a life-changing event, though contesting a general government stimulus usually requires proving a permanent reduction in your ongoing income.

The Serious Risk for Supplemental Security Income (SSI) Recipients

While standard retirees can absorb a direct payment with minimal disruption, individuals receiving Supplemental Security Income face severe risks. SSI provides critical financial support for older adults and people with disabilities who have extremely limited income and resources. Unlike standard retirement benefits, SSI is strictly means-tested.

To qualify for SSI, an individual cannot hold more than $2,000 in countable resources; couples are capped at $3,000. If a sudden $2,000 government payment hits an SSI recipient’s bank account, it can instantly push them over the strict resource limit. Exceeding this limit results in an immediate suspension of monthly SSI payments and often triggers the loss of Medicaid coverage, which is catastrophic for those relying on it for long-term care or expensive prescriptions.

Historically, when Congress issues widespread economic relief, the Social Security Administration provides a grace period. For example, previous stimulus measures granted SSI recipients a 12-month window to spend the funds before the money counted against their resource limits. If a new payment is approved, you must pay close attention to the specific grace period rules written into the law. Spending the funds on permissible exempt assets—such as home repairs, medical equipment, or paying down debt—within the allotted timeframe is crucial to preserving your essential benefits.

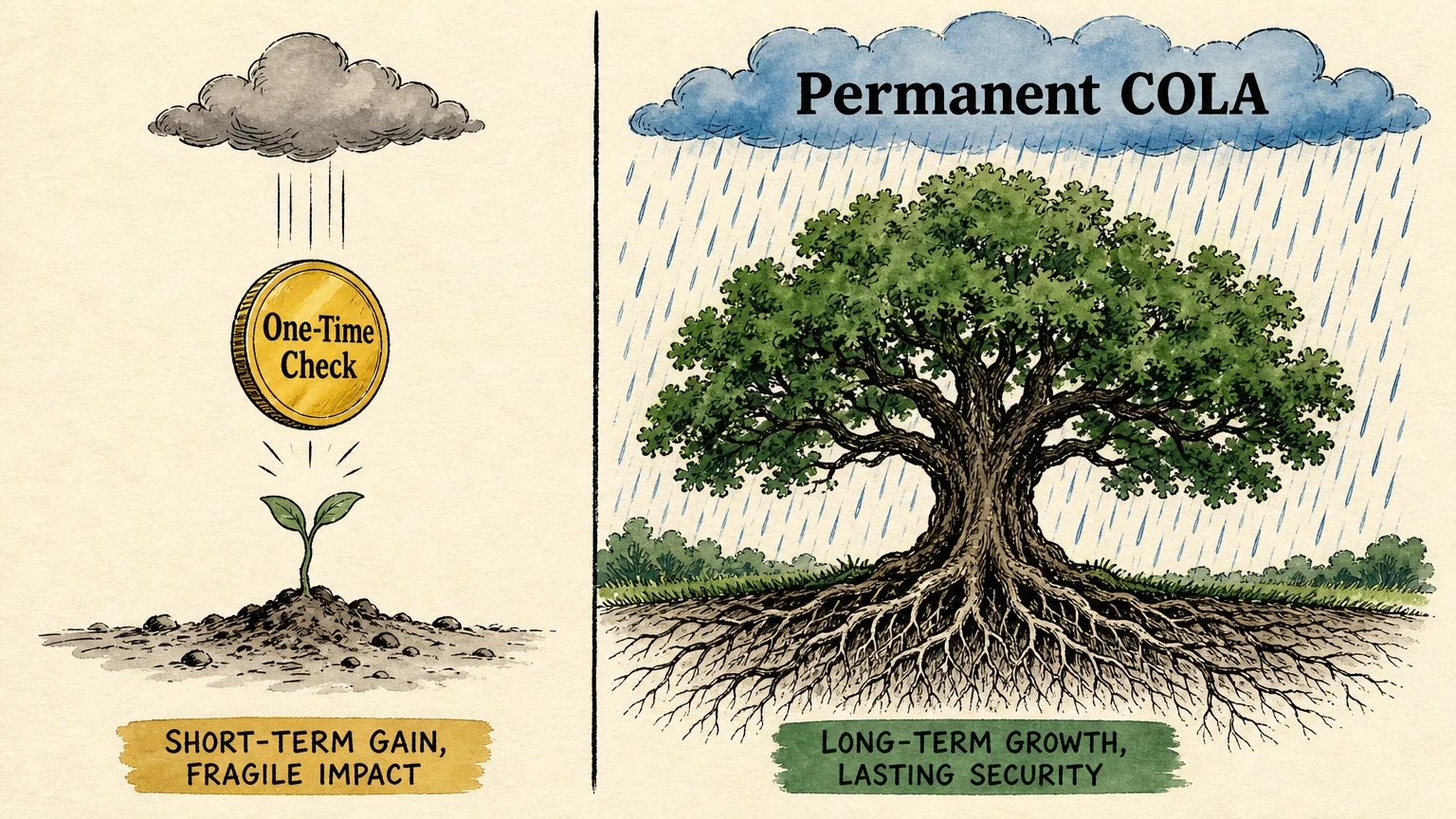

Comparing Direct Checks to Permanent Benefit Adjustments

Retirees often weigh the value of a lump-sum payment against permanent legislative improvements to their benefits. While a direct check provides immediate liquidity, it lacks the compounding power of structural changes to the retirement system. The table below illustrates the core differences between a one-time cash infusion and a permanent Cost-of-Living Adjustment.

| Financial Factor | Proposed $2,000 Direct Payment | Standard Social Security COLA |

|---|---|---|

| Frequency of Payment | One-time, lump-sum distribution | Permanent, recurring monthly increase |

| Inflation Protection | Provides immediate but temporary relief | Compounds annually to protect long-term purchasing power |

| Impact on Taxation | May cause a temporary spike in adjusted gross income | Gradually increases combined income over several years |

| Risk to SSI Limits | High risk of exceeding strict asset limits if not spent quickly | Built into the program; does not threaten baseline resource limits |

| Application Requirement | Usually requires filing a tax return to claim | Applied automatically by the Social Security Administration |

Pitfalls to Watch For

Whenever the government debates issuing broad payments, confusion follows. Con artists treat economic policy changes as a prime opportunity to defraud older adults. Protecting your retirement income requires vigilance against common scams and financial missteps.

First, beware of processing fee scams. Scammers frequently call, email, or text retirees claiming to represent the Treasury or the IRS. They will claim your $2,000 payment is ready, but you must pay a “processing fee” via gift cards or wire transfer to release the funds. The federal government will never ask you to pay money to receive your legal benefits. If you encounter this, report the communication immediately to the Consumer Financial Protection Bureau.

Second, avoid spending the money before it officially clears. The legislative process is slow and highly unpredictable. A proposal discussed on a Monday news broadcast might be significantly altered or entirely scrapped by Friday. Making large purchases on credit with the assumption that a government check will arrive soon is a fast track to high-interest consumer debt.

Finally, do not neglect your state tax laws. While the federal government might declare a specific payment exempt from federal taxes, individual state revenue departments write their own rules. A payment that passes cleanly through the IRS might still trigger a state tax liability depending on where you maintain your primary residence.

Getting Expert Help

Managing the intersection of new government programs, tax thresholds, and healthcare premiums often requires a professional perspective. You do not have to navigate these complex variables alone.

“A big part of financial freedom is having your heart and mind free from worry about the what-ifs of life.” — Suze Orman, Personal Finance Expert

Consider consulting a Certified Financial Planner (CFP) or a Certified Public Accountant (CPA) if you find yourself in the following scenarios:

- You hover near an IRMAA cliff: If you suspect a sudden payment will push you into a higher Medicare premium bracket, a tax professional can help you utilize deductions or adjust your IRA withdrawal schedule to safely lower your MAGI.

- You manage an estate or trust for an SSI recipient: Navigating resource limits is perilous. An elder law attorney can help you establish an ABLE account or a Special Needs Trust, allowing the recipient to benefit from the payment without losing their vital Medicaid and SSI eligibility.

- You are executing a Roth conversion strategy: If you are strategically moving money from a traditional IRA to a Roth IRA, your tax margins are likely very tight. A professional can recalculate your conversion limits to ensure an unexpected $2,000 payment does not throw off your multi-year tax plan.

Frequently Asked Questions

Is a proposed $2,000 payment subject to federal income tax?

The tax status depends entirely on how Congress writes the specific legislation. Historic stimulus checks were structured as refundable tax credits and were completely exempt from federal income tax. However, if a new payment is funded by specific tariffs or structured as a dividend, the IRS may classify it as taxable gross income.

Do I need to file a tax return to receive direct government payments?

Typically, the IRS uses the banking information on file from your most recent tax return to distribute funds. If you rely solely on Social Security and do not normally file taxes, the government usually coordinates with the Social Security Administration to send the money directly to your established direct deposit account. However, you should monitor official IRS announcements to see if a simple non-filer form is required.

Will a direct payment affect my spouse’s survivor benefits?

No. Survivor benefits, much like standard retirement benefits, are calculated based on the deceased worker’s lifetime earnings record. Receiving a direct economic relief payment has no bearing on the formulas used to calculate current or future survivor benefits.

Does this payment count toward the Medicaid look-back period?

Generally, government stimulus payments do not negatively impact Medicaid eligibility provided you adhere to the specific spend-down grace periods enacted with the legislation. Spending the funds on permissible, exempt assets prevents the money from being classified as a countable resource.

Wrapping Up Your Financial Strategy

Economic policies evolve rapidly, and staying informed is your greatest asset. A proposed $2,000 payment represents an opportunity to fortify your emergency savings or handle deferred maintenance on your home. By understanding how this money interacts with your tax brackets, Medicare premiums, and core retirement benefits, you can confidently integrate the funds into your life without jeopardizing your long-term stability. Continue monitoring official legislative updates, keep your direct deposit information current with the federal government, and adjust your annual tax planning as new details emerge.

The information in this guide is meant for educational purposes. Your specific circumstances—including income, health needs, tax situation, and goals—may require different approaches. When in doubt, consult a licensed professional.

Last updated: June 2026. Retirement benefits, tax rules, and healthcare regulations change frequently—verify current details with official sources.

Leave a Reply